AEKKARAT DOUNGMANEERATTANA

AEKKARAT DOUNGMANEERATTANA

Formula for success: rise early, work hard, strike oil." - J. Paul Getty.

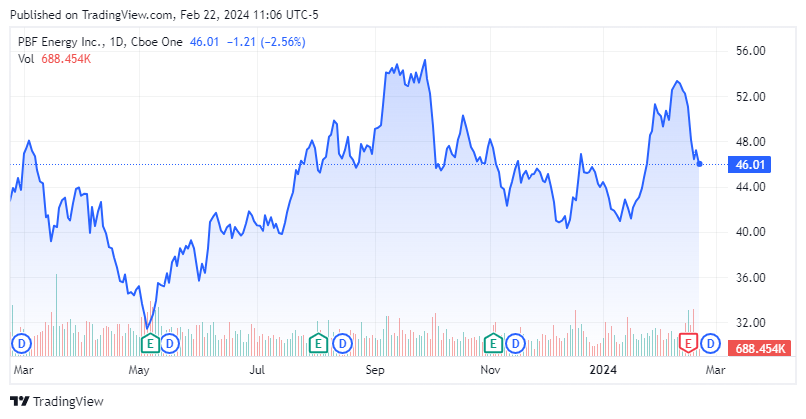

Shares of domestic refiner PBF Energy Inc. (NYSE:PBF) are down by a quarter since hitting an all-time high in September 2023 even after posting a blowout Q3 2023 in early December, which was followed by disappointing Q4 results last week. A historic two-year run of outsized crack spreads have compressed recently as well. With more cash than debt, a 2.2% current dividend yield, but little in terms of throughput capacity growth prospects, the recent insider buying in PBF merited a deeper dive.

Seeking Alpha

Company Presentation

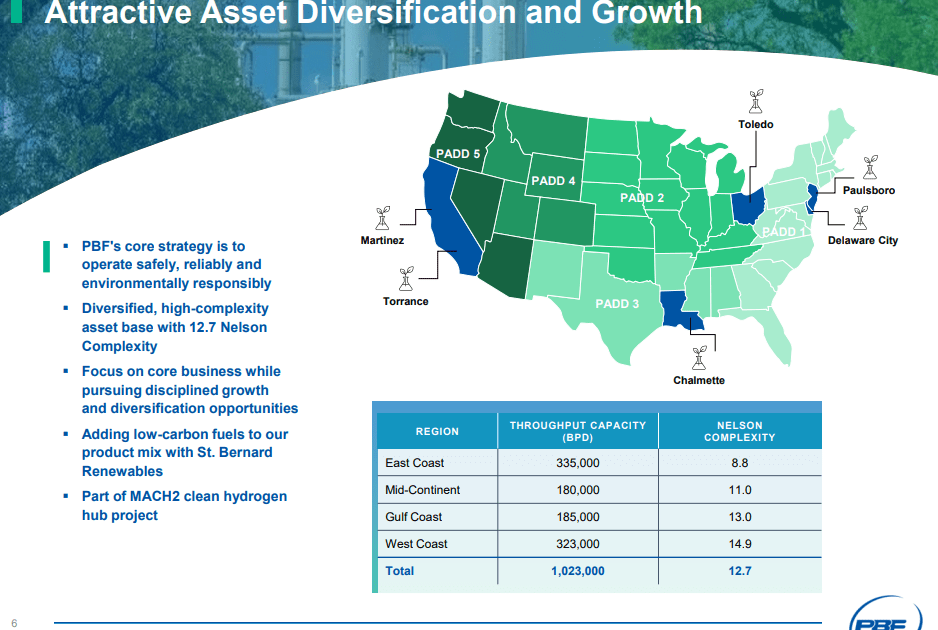

PBF Energy Inc. is a Parsippany, New Jersey-based independent petroleum refiner and supplier of unbranded gasoline, distillates, petrochemical feedstocks, and lubricants, amongst other products. The company owns six refineries in the U.S. with an aggregate refining (throughput) capacity of 1.02 million barrels per day. PBF was a joint venture formed in 2008 between Petroplus Holdings (OTC:PEPFF) and private equity firms Blackstone (BX) and First Reserve – thus, the initials PBF – with each contributing $667 million in equity. It went public in 2012, raising net proceeds of $612.8 million at $26 per share. The stock currently trades around $46.00 a share, translating to a market cap of just over $5.7 billion. Blackrock still owns 10% of the shares outstanding.

Company Presentation

Although the company is essentially a refiner, it views its operations through two segments: Refining and Logistics. However, the Logistics unit, which charges fees for terminaling, storage, and pipeline services, generates the vast majority of its revenues from intercompany transactions that are thus eliminated in consolidation.

Company Presentation

Refining consists of the six facilities, three of which were purchased prior to its IPO. The unit generates margin by selling its distilled products (gasoline, heating oil, asphalt, etc.) for more than it paid for its crude oil input, known as a crack spread. Factors influencing the multiple crack spreads are manifold, including geopolitical issues, transportation costs, and seasonal factors. That said, crack spreads generally floated between $12 and $16 a barrel during the 2010s, dipped into the high-single digits during the bizarre industry events like negative oil prices in 2020 and returned to their normal range in 2021. From a longer perspective, they averaged ~$10.50 a barrel 1985 to 2021.

However, events set in motion by the pandemic and a new administration in 2020 and 2021 (respectively) resulted in record refining margins in 2022, triggered by the Russia-Ukraine conflict. With the economy effectively locked down by the pandemic, refiners elected to shut in capacity (or shut down altogether) in response as demand for petroleum products cratered. With Joe Biden ascending to the presidency on campaign promises to end fossil fuels, there wasn’t as much incentive to reopen the shuttered refineries. As such, U.S. refining capacity hit an all-time high of 19.0 million barrels a day in 2020 but fell below 18.0 million entering 2022 – part of a larger 4.5 million barrels a day decline of refining capacity worldwide.

Just as demand was normalizing, Russia invaded Ukraine early in 2022, triggering a series of sanctions against the former, including a ban on the importation of Russian refined products. With Europe fearing that it would freeze without natural gas and refined products (like heating oil) from Russia, it began to stock up in anticipation, purchasing from capacity-constrained U.S. refineries. These actions established a very tight balance – or imbalance – between global refined product demand and global refining capacity, resulting in extremely low finished gas and finished distillate stocks versus their 2017-2021 average. Factor in the release of over 40% of the Strategic Petroleum Reserve, which dampened crude oil (input) prices, and a refiner’s Goldilocks scenario was fashioned, turning 2022 into a massive boon for refiners, with crack spreads widening from $16 to $20 in FY21 to $31 to $40 in FY22. These dynamics continued for a good portion of FY23, with crack spreads dropping $3 to $9 per barrel during the first nine months of 2023 (YTD23), but still ~$15 to ~$20 a barrel above their historical averages.

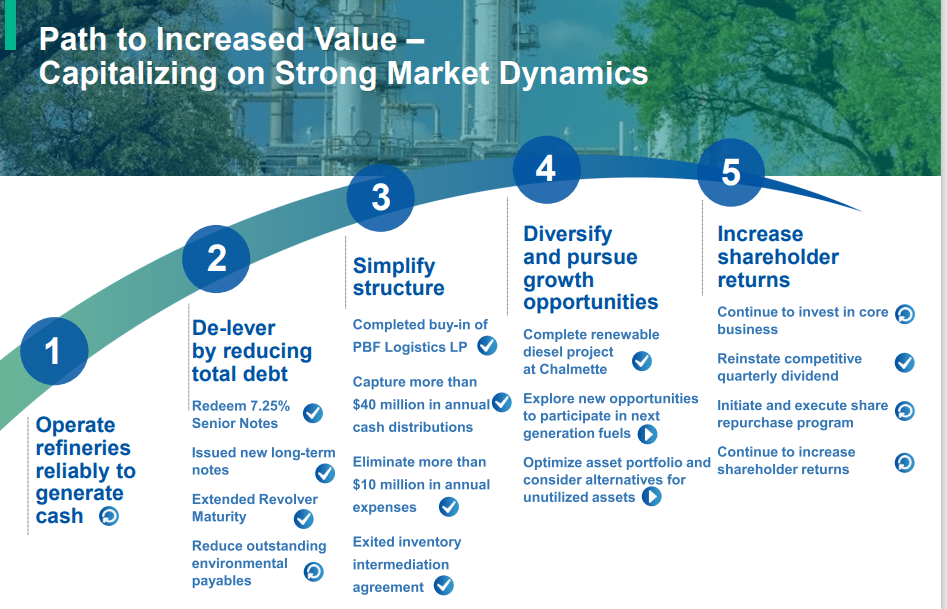

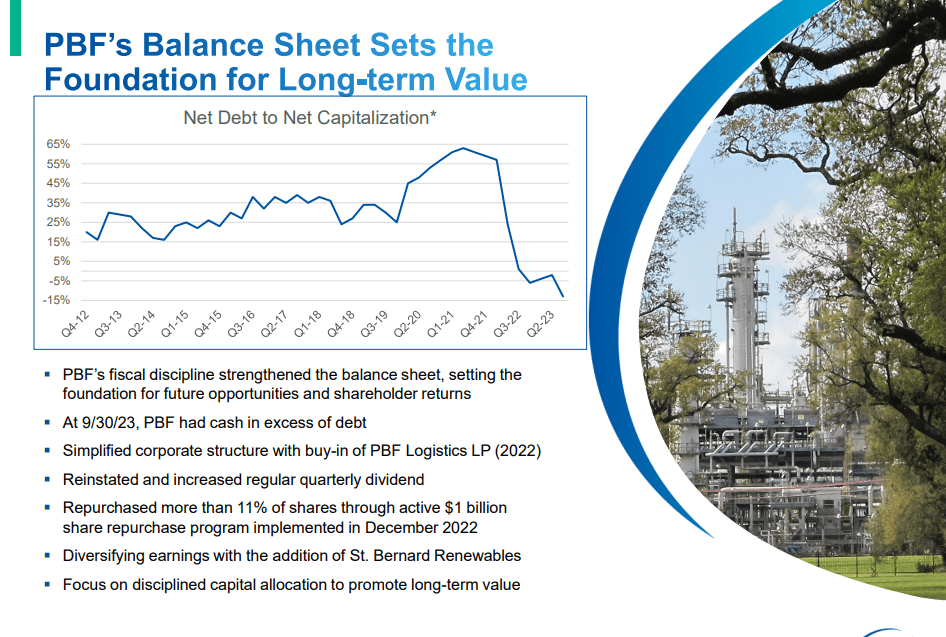

These favorable circumstances permitted PBF to significantly de-lever its balance sheet and reinstate its quarterly dividend (at $0.20) in October 2022, which had been suspended at the onset of the pandemic.

Not surprisingly, shareholders of PBF have enjoyed a significant return on investment since the industry recovered from the negative oil price madness of April 2020, with their stock rallying 1,289% trough ($4.06 a share in October 2020) to peak ($56.38 a share in September 2023). However, as strong as that performance has been, many would argue that it should be substantially greater. At its peak, PBF stock was trading at a FY23E P/E multiple of 4.8 and a microscopic EV/TTM EBITDA of 1.7. Since that time, shares of PBF have retreated more than 20% since.

The explanation for this head-scratching performance is manifold, but can be distilled down to the market’s skepticism regarding the sustainability of outsized crack spreads, owing to the fact that China, which already possesses the most nameplate refining capacity worldwide, is expected to add 1.5 million barrels per day 2022-2028. (Volume wise, the U.S. is still the world’s largest refiner, thanks to capacity utilization rates around 90% versus ~70% in China.) Also, as it relates to PBF, there is not much on the drawing board regarding growth initiatives after it completed a renewable diesel project at its Chalmette, Louisiana facility that added ~20,000 barrels of daily output – more or less to onboard EPA-mandated renewable fuel credits, known as RINs. There is also concern that the company’s Martinez, California refinery is susceptible to a lawsuit, owing to three releases of coke dust since November 2022, elevating concerns from neighboring homeowners regarding their soil quality.

That said, from a financial perspective, there was not much to dislike in the company’s 3Q23 report of November 2, 2023. It posted earnings of $6.11 a share (non-GAAP) and Adj. EBITDA of $1.30 billion on revenue of $10.7 billion versus $8.40 a share (non-GAAP) and Adj. EBITDA of $1.54 billion on revenue of $12.8 billion in 3Q22. Although down 27%, 16%, and 16% (respectively) from the prior year period, it bested Street consensus by $1.24 at the bottom line and $440 million at the top, as crack spreads (save WTI (Chicago) 4-3-1, which was down 26%) remained comparable.

That said, throughput volume was down 5% year-over-year to 939,700 barrels per day due to increased maintenance activity and lower demand. That volume is anticipated to further decrease to 900,000 barrels per day in Q4 '23 (based on a range midpoint) due to extensive turnaround work at the company’s two California refineries.

PBF Energy posted its Q4 numbers on February 15th. Revenues fell just under 16% on a year-over-year basis to $9.14 billion, which beat the consensus estimate by nearly $500 million. Earnings, on the other hand, deeply disappointed investors. PBF delivered a GAAP loss of 41 cents a share, instead of the six cent a share profit that was expected. This resulted in a net loss of $48.4 million in the quarter. However, PBF Energy posted net income of $2.971 billion for FY2023. Management noted the following for the earnings miss:

Consolidated gross refining margin plunged 90% to $1.04/bbl of throughput in the quarter, citing unfavorable movements in crack spreads, crude oil differentials as well as planned and unplanned maintenance, primarily at West Coast refineries."

There will be some extensive maintenance scheduled on PBF's core facilities in 2024, mostly in the first half of the year. Management provided the following initial guidance for FY2024.

February Company Presentation

In addition to the reinstatement of its quarterly dividend, which PBF increased 25% to $0.25 a share for a current yield of 2.3%, the company ended the year with $1.8 billion of net cash on its balance sheet. Management reduced debt by $700 million and returned $640 million to its shareholders primarily through stock buybacks. Management just added another $750 million to its stock buyback authorization as well.

Third Quarter Company Presentation

Since fourth quarter results posted, four analyst firms including TD Cowen and Piper Sandler have reissued/assigned Hold ratings on the stock. Price targets proffered range from $39 to $52 a share. Wells Fargo ($64 price target), JPMorgan ($54 price target), and Mizuho Securities ($52 price target) have maintained Buy ratings on PBF. On average, they project earnings of $6.01 a share in FY2024 as revenues dropped 17% to just over $31.7 billion.

That said, Seeking Alpha’s quant screen listed PBF as 2024’s seventh most attractive value name with a market cap above $1 billion in late November of last year.

The wealthiest man in Latin America, Carlos Slim Helu, is decidedly bullish on PBF’s prospects, having purchased 1.26 million shares at an average price of $42.77 per share on January 12-16, 2024. Those additions pushed his ownership interest to slightly over 10%.

Trading at under eight times FY24E EPS and sporting a 2.2% annual dividend yield, PBF Energy Inc. is more than a reasonable value play here. That said, after two historic years, refining margins are likely to contract in FY24 and the company’s growth prospects for nameplate capacity are non-existent – at least for now. That said, its balance sheet is in excellent shape and its downside is arguably limited, making PBF a solid longer-term investment at current trading levels.

I like PBF as a covered call play here at current trading levels. In addition, given the U.S. has not built a large refinery since the late 70's, I think refinery assets have good long-term value.

An indispensable good transported to the far corners of the world, black gold had become the very vector of the industrial vascular network, the blood of human technology.”― Matthieu Auzanneau.