Sashkinw/iStock via Getty Images

Sashkinw/iStock via Getty Images

The Invesco Global Clean Energy ETF (NYSEARCA:PBD) is a small cap fund that seeks to track the returns of the WilderHill New Energy Global Innovation Index. The portfolio contains equities of companies located in developed and emerging markets that engage in clean energy conservation. These companies are involved in wind, solar, hydro, tidal wave, biofuels and other sources of renewable energy, as well as businesses related to energy conversion, storage, conservation, efficiency, carbon and greenhouse gas reduction and pollution control.

While this type of ETF is a consideration for investors wanting to allocate to the space for either socially responsible reasons or in the belief that clean energy promises great returns, we believe there are better choices than PBD. Its portfolio allocation is spread too broadly and we believe that is what is eroding performance. We rate the fund a Sell.

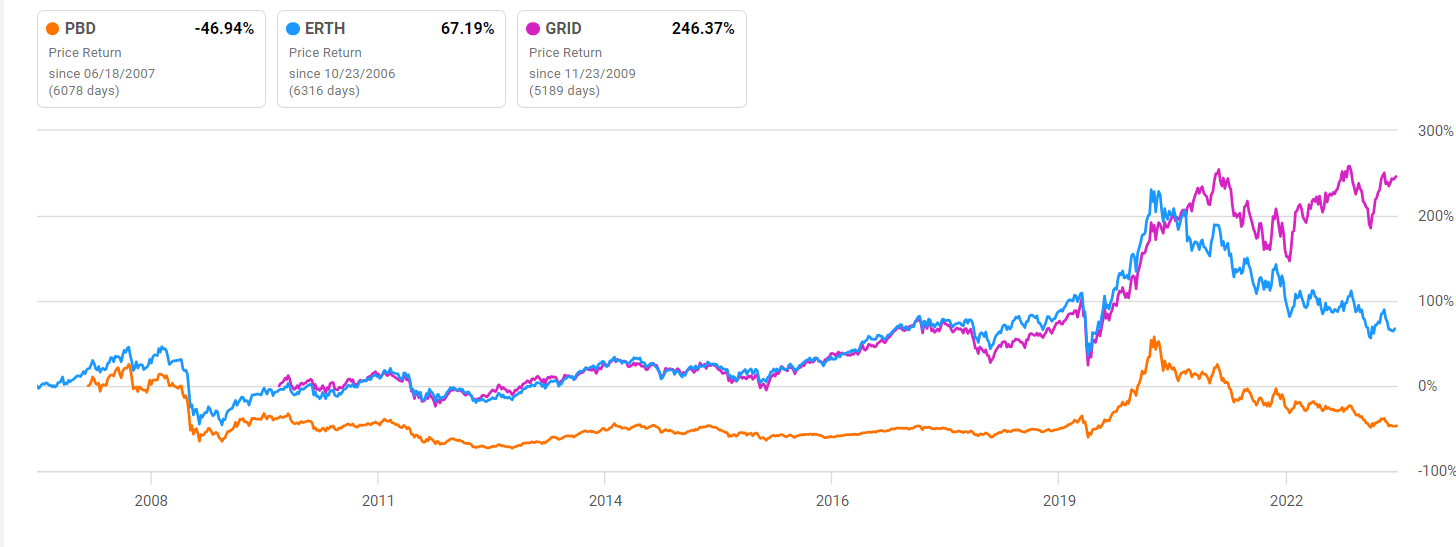

PBD is one of the oldest funds in the space with an inception date of 2007. Though it may be a seasoned ETF, it has continued to underperform its peers and benchmarks time and time again.

Take a look at PBD against GRID and ERTH:

Seeking Alpha

The problem is with PBD’s portfolio construction. Sector diversification is rarely a bad idea for an ETF that aims to cover more than an isolated piece of a big global stock market. However, when it comes to a specific style, like renewable energy, not discriminating enough in choosing stocks seems to be a hindrance. Other better-performing funds are more narrowly focused. Since ETFs of this type are more likely to be a portion of a larger equity portfolio, there's little value added by owning so many stocks.

PBD’s attempt to more loosely define alternative energy means it ends up owning equities that may not offer the best capital appreciation potential from a fundamental perspective. A more bottom-up approach to stock selection would seem to better benefit the fund. But that's not happening here.

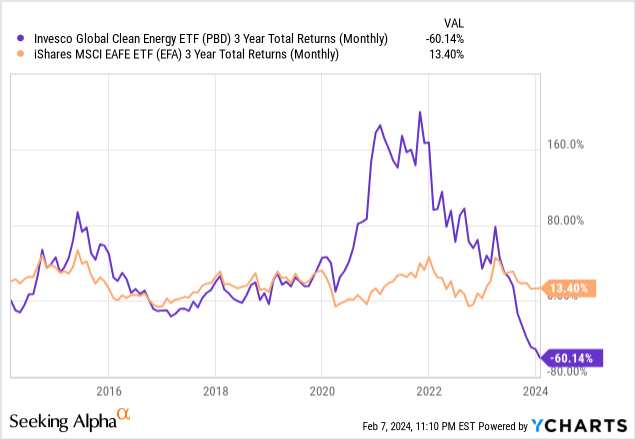

Another problem is the fund’s rules-based investing approach. Called a "smart beta" ETF, PBD employs a blend of active and passive investing as it attempts to track an index that is not market cap weighted. Investors choose this strategy to generate returns that beat the broad market. In PBD’s case, its benchmark is the MSCI EAFE. If we compare PBD to that index, the smart beta approach is clearly not working.

While PBD did outperform the EAFE index by a very wide margin during 2021, this is most likely due to President Biden’s signing of the infrastructure bill which provides billions of dollars in funding for renewable energy projects.

The rules-based approach of the WilderHill New Energy Global Innovation Index seems to be doing a disservice to the PBD as it doesn’t entail any fundamental analysis. The inclusion rules for the index include exceeding certain minimums for market cap and liquidity as well as “...exposure to clean energy with a company being required to have the primary part of its business activities with a focus on new energy innovation as described in the sector definitions – and without fossil fuel exposure…”

According to the above, as long as a company is in the green energy space, as defined by the Index Committee, and meets liquidity and market cap requirements, it is subject to inclusion. This process seems to preclude any financial analysis of these stocks.

PBD’s standard deviation of returns falls in line with the category average, but for a fund whose returns lag the majority of its peers, that is an unacceptable level of volatility.

Though less of a consideration when analyzing risk, PBD’s turnover percentage really stands out from the rest at 64%. This is the highest of all of its peers and even more importantly, well exceeds the acceptable level of trading for a passively managed fund, which should be around 30%.

I don’t obsess over expense ratios because I believe that you pay for what you get with an ETF. However, PBD’s ratio is the second-most expensive in its category and that is unreasonable given its risk/return profile. In this fund’s case, you’re NOT getting what you’re paying for.

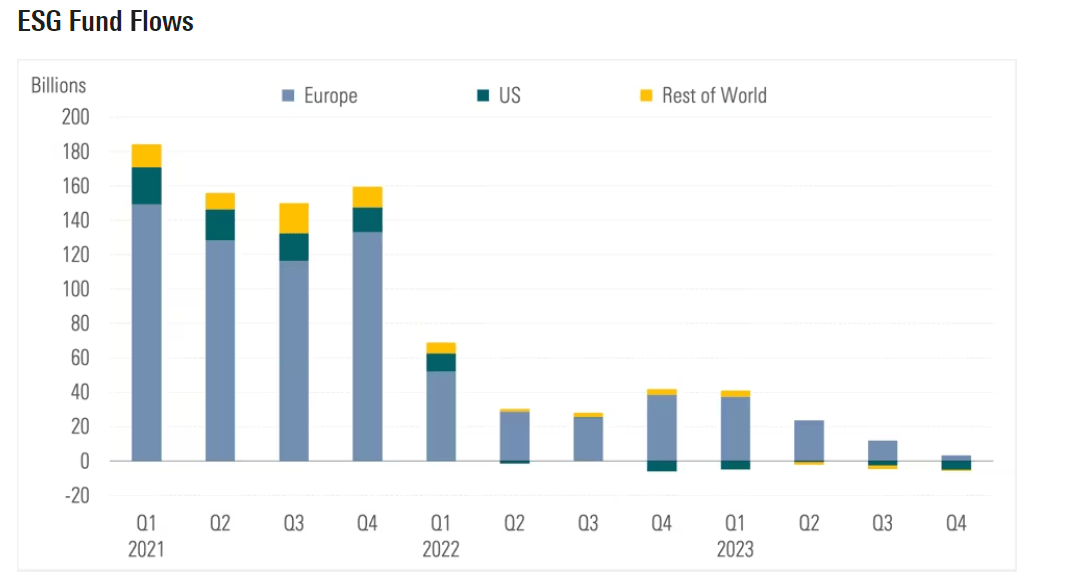

In 2021, renewable energy stocks were all the rage when Biden pledged support for renewable energy projects through his infrastructure bill. The excitement abated after many of these names suffered price inflation from the temporary run up and stocks were sold off. To compound the hurt, a challenging macroeconomic environment of enduring inflationary pressures, the threat of future rate increases, and recession fears drew cash away from green energy. Fund inflows from the ESG space reached a nadir in the fourth quarter of 2023. See the chart below:

Morningstar

In terms of energy as a sector, many investors who were putting cash in ESG energy names as a subsector bet began to move their money into traditional energy names for the same reasons as outlined above.

See the convergence of returns in the chart below:

Charles Schwab

For investors that want to buy into the clean energy space, whether for social responsibility reasons or for the belief in outsized returns, waiting on the sidelines a bit until the macro landscape settles might be prudent. When the opportunity to invest does arrive the menu of ETFs dedicated to the space is long.

Given PBD’s stock selection strategy, a portfolio whose allocation is too broad and its unattractive risk/return profile, we are avoiding it. In fact, for all the reasons discussed above, we are assigning this green energy ETF a Sell rating.