wolv

wolv

Note: All amounts discussed are in Canadian Dollars. All stock prices referenced are from TSX.

On our last coverage of Pembina Pipeline Corporation (NYSE:PBA, TSX:PPL:CA), we viewed the shares as attractive and they got our third consecutive Buy rating.

Seeking Alpha

We expected a modest move over the next 12 months and admired the financial discipline the company was exhibiting. Specifically we said,

The self-funded model is the right one here and PBA is showing the same discipline it did when it walked away from the Interpipeline purchase with a boatload of cash. We continue to believe this is a "Buy" and think that we will eventually see at least a 10X AFFO multiple.

Source: "Preferreds Deliver Fantastic Returns, Where To Go Next."

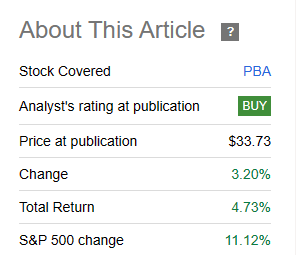

The shares have done all right since then, but heavily lagged the broader markets.

Seeking Alpha

We look at the Q4 2023 results and tell you why a big hike is probable for this stock in 2024.

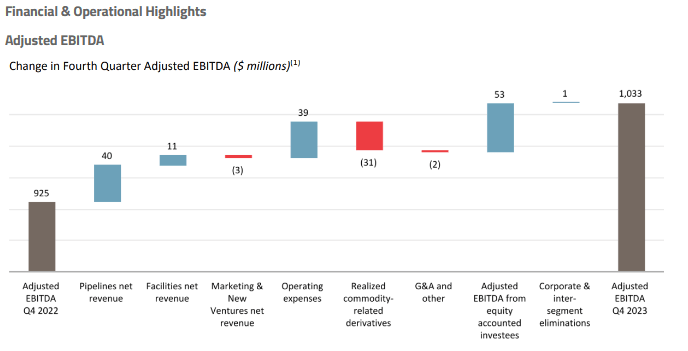

Pembina's Q4 2023 was slightly ahead of consensus estimates, and adjusted funds from operations, or AFFO, came in at $1.36 per share vs. expectations of $1.34 per share. It also marked a 7% growth year-over-year as the Facilities segment benefitted from the asset acquisitions post Q4 2022 (from PGI). Marketing was powered by double-digit volume growth, and even though corporate expenses were heavier than usual, Pembina closed off with $4.81 AFFO per share. While the EBITDA walkthrough is not the same as what happened to AFFO, it highlights the same trends.

Pembina

The company made a number of notable announcements that focused on the growth side of the ledger for 2024.

Ethane Supply and Transportation Agreements - Pembina has entered into long-term agreements with Dow Chemical Canada (DOW) to supply and transport up to 50,000 barrels per day ("bpd") of ethane to support their recently announced Path2Zero Project.

Nipisi Pipeline Contracting - signed an incremental long-term contract on the recently reactivated Nipisi Pipeline, with line of sight to the asset being fully contracted by the end of 2024.

Wapiti Expansion - Pembina Gas Infrastructure ("PGI") has approved a $140 million (net to Pembina) expansion of the Wapiti Plant that will increase natural gas processing capacity by 115 million cubic feet per day ("mmcf/d") (gross to PGI).

Phase VIII Peace Pipeline Expansion - the estimated project cost has been further reduced to $430 million (previously $475 million; original budget of $530 million).

Source: Pembina Q4-2023 Press Release.

The Ethane supply agreement is a substantial win, as Pembina has likely picked up 50% of the total that DOW is likely to transport in this project. This will also likely help on the storage side of Pembina's assets. One relative negative announcement was on the CEDAR LNG. The final investment decision was postponed, and it is possible that PBA backs off with a loss on this.

Though numerous milestones have been achieved, the Cedar LNG project still faces a number of schedule driven interconnected elements that require resolution prior to making a final investment decision ("FID"), including binding commercial offtake, obtaining certain third-party consents, and project financing. On this basis, a final investment decision is now expected in the middle of 2024.As a result of the revised FID timing, current year net contributions to Cedar LNG through to the middle of 2024 are expected to be approximately $200 to $300 million.

Source: Pembina Q4-2023 Press Release.

Pembina guided for 2024 adjusted EBITDA range of $3.725 billion to $4.025 billion. If this looks way below where consensus is, you are not hallucinating. Most estimates are in the $4.0 billion plus range with some as high as $4.3 billion.

There are two factors driving this. The first being that Pembina is being extremely conservative for some reason. Most companies like to "beat and raise" and probably that is playing a role here. The second is that the guidance above excludes Alliance/Aux Sable Acquisition. The timing of closing that is uncertain, so Pembina has left it out of its guidance. If you used the multiples given at the time of Alliance/Aux Sable Acquisition and added the equity dilution (Pembina issued shares to keep debt levels controlled), you can estimate that the company's whole year run-rate. That estimate would be about $4.4 billion. Based on that, the company is trading around 9.0X EV to EBITDA. Not particularly expensive, considering that the debt part of the equation is close to 3.2X.

The more popular measure here is the price to AFFO multiple, which is useful, assuming that the debt side of the equation is in line. Again, adjusting for a full year run-rate, would give us close to $5.00 in AFFO per share. If we go with our prior 10X multiple, you would get to $50.00 per share. Pembina is within striking distance of that. While investors have in the past tended to equate AFFO multiples with P/E multiples and argued that midstream assets are far cheaper than the market as a whole, we don't see it that way. You will generally get some push back if you start pushing past 11X or 12X on these, especially in a time of 5% interest rates. Circling back to the other metric, 10X EV to EBITDA has been a good middle multiple for both quality midstream and for the stock market.

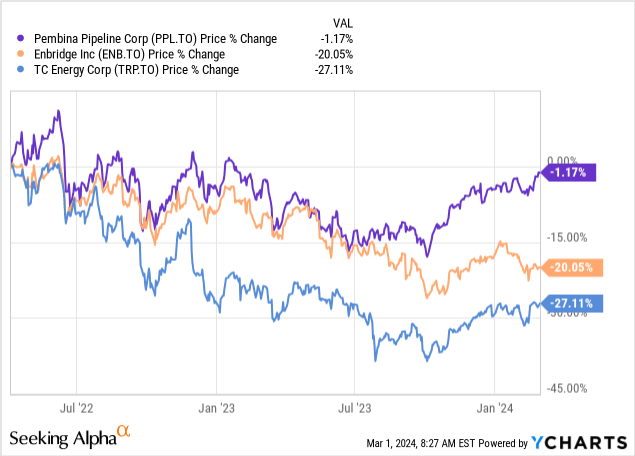

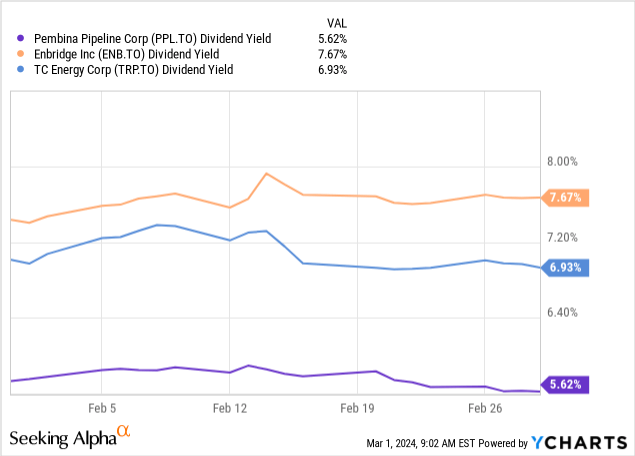

Our overall point here is that Pembina is not stunningly cheap, as many would like to believe. Yes, there is a path here to 10X AFFO, which would give you about 11% total return from here. Investors may recall that around this price point (in Canadian dollars) was when we had our two "hold" ratings for this company (see here for an example). What is interesting is the path these shares have taken, relative to both Enbridge Inc. (ENB) and TC Energy Corp (TRP), since that 2022 article.

We looked at both Enbridge and TC Energy Corp recently, and it is hard here to favor Pembina over Enbridge. Yes, Enbridge is carrying the higher debt load, but it has also historically proven to be the better capital allocator and has far better assets. Pembina also lags the other two in terms of dividend yield, though we think a big hike may be in store for 2024 from this company.

Pembina Pipeline Corporation's AFFO payout ratio is really low and deleveraging has been accomplished, so outside the unnecessary, expensive acquisition, what else is there to do but hike the dividend? That hike aside, our overall thesis on valuation stands. With limited upside ahead of Pembina, we are moving this to a "hold." We maintain our "Strong Buy" on Enbridge.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.