Wolterk

Wolterk

Paychex (NASDAQ:PAYX) is a provider of human capital management solutions that has underperformed the S&P 500 and the Nasdaq 100 YTD. The company is set to report its Q3 FY24 earnings on March 27. The company is expected to grow its revenue by 5-6% in FY24 while maintaining its operating profit margin between 41-42%. At the same time, the company continues to invest in strategic partnerships and integrate AI to improve its solution suite, thus ensuring its market leadership position. However, I believe that macroeconomic uncertainty could be a sizable threat, especially as the company caters to small and medium-sized businesses, which are often the most exposed to economic downturns.

After assessing both the “good” and the "bad," I have no doubt about the company’s track record of operational excellence so far. However, given where the stock is currently trading, I would be waiting on the sidelines for a better entry point in order to drive meaningful long-term upside in my portfolio. As a result, I would rate the stock a “hold” at the moment.

Paychex provides integrated human capital management (HCM) solutions for human resources, payroll, and benefits-related services for small and medium-sized businesses.

Paychex breaks down its solutions into two segments:

1) Management Solutions: One of the core offerings in this segment is Paychex Flex, which is a subscription-based product that allows businesses to process payroll when and how they want and on any device.

2) Professional Employer Organization (PEO) & Insurance Solutions: This offers businesses a combined suite of services that include payroll, employer compliance, HR, and employee benefits administration, among other services, essentially acting as a co-employer of their customers’ employees by providing a more comprehensive set of benefits.

In FY23, the company generated $5B in revenue, which grew 9% YoY. Out of that, service revenue contributed 98% to total revenue. Service revenue is made up of Management and PEO Solutions, which contributed 75% and 25% to service revenue, respectively.

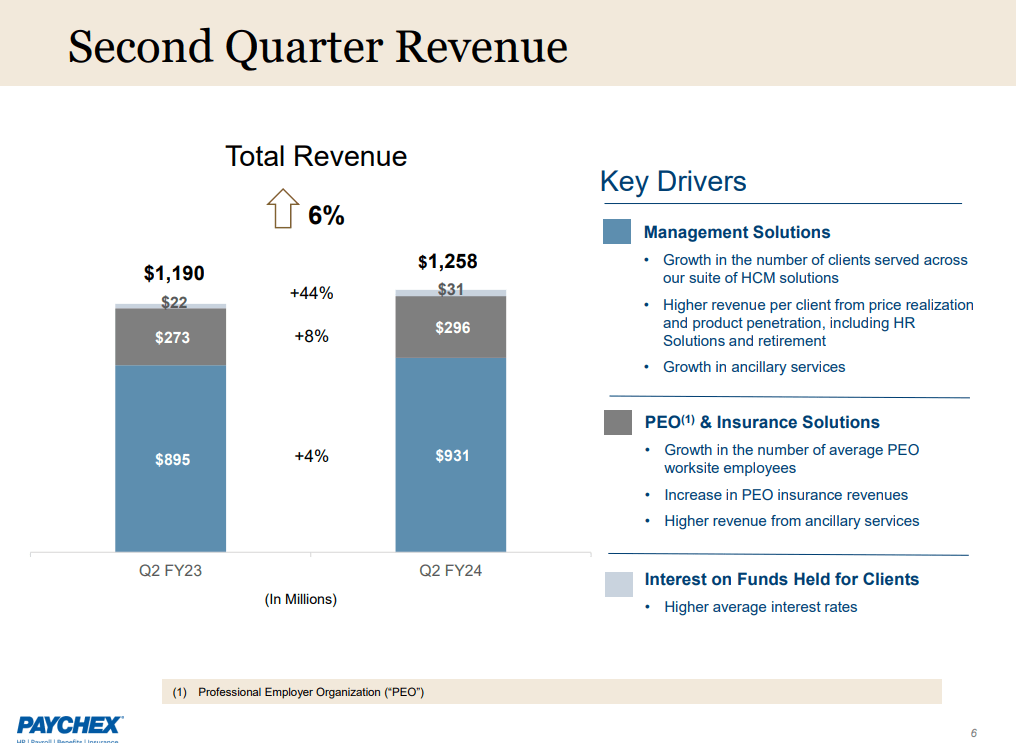

The company posted its Q2 FY24 earnings last year and is due to report its Q3 FY24 earnings on March 27th. In Q2, the company generated $1.25B in revenue, up 6% YoY. Out of $1.25B, Management Solutions contributed $931M, growing 4% YoY, and PEO Solutions contributed $296M, up 8% YoY.

While the management noted that the demand for their HR technology and advisory solutions remains strong amidst a challenging environment for small and midsize businesses, a tight labor market, and rising healthcare and benefit costs, I would like to point out that I particularly like the pick-up in PEO Solutions segment revenue growth, which grew 8% YoY. I believe that the shift in revenue mix has a positive impact on customer lifetime value, especially when clients attach insurance benefits. During the earnings call, John Gibson, CEO of Paychex, talked about the specific actions the company has taken to revamp its PEO Solutions after last year’s challenges.

We previously discussed actions we took to help the PEO recover after last year's challenges including: one, redesigning our health offerings; second, leveraging AI to revamp our sales and marketing models and to identify and attract high-value prospects; three, putting more focus on upgrading existing HCM and ASO clients to the PEO model; and finally, improved sales execution. As mentioned earlier, our insurance enrollment is underway and the tax rates are up after a challenging year last year. I want to specifically thank and congratulate our PEO team for all the hard work and success the past year so far.

Q2 FY24 Earnings Slides: Paychex's Revenue growth across segments

At the same time, revenue retention is above pre-pandemic levels, and the company continues to see improvement in client retention rates YoY. I believe that the company’s robust product innovation culture has a significant role to play here. With Paychex Flex consistently rated as a leader in the HCM industry, the company is also making targeted investments in GenAI to leverage vast data sets to improve efficiency and enhance the customer experience. The company recently partnered with Visier, an analytics and workforce solutions company, to enhance their reporting and analytics in Paychex Flex, thus resulting in superior business outcomes for their clients.

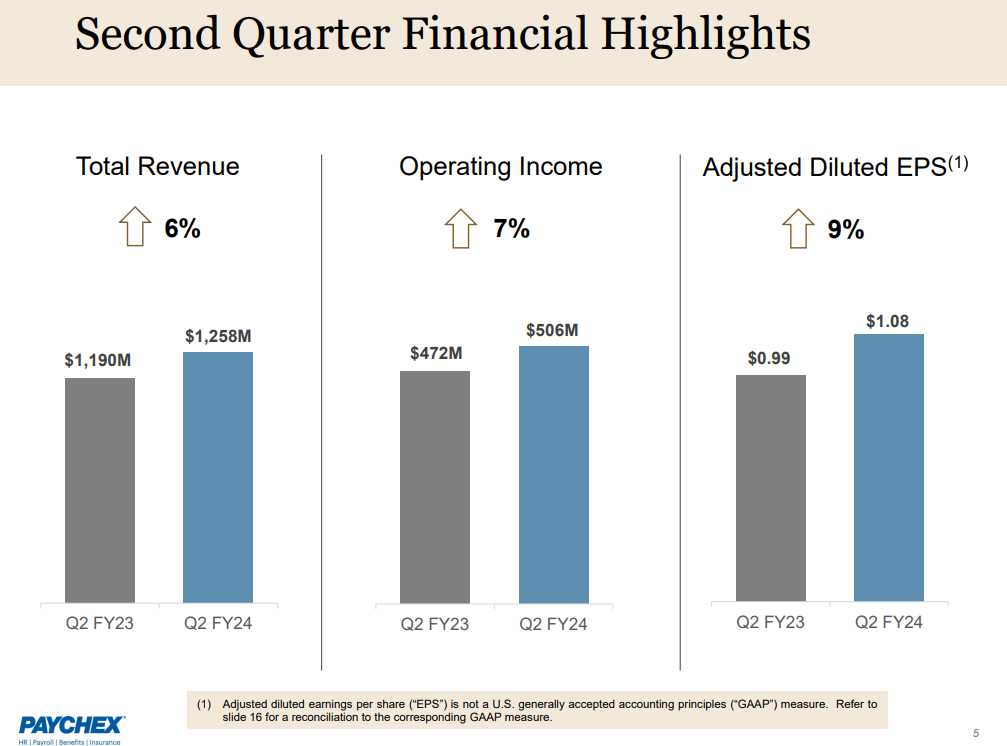

Shifting gears to profitability, the company has a long history of operational excellence. Over the last 5 years, while it has grown its revenue at a compound annual growth rate (CAGR) of 8%, it has simultaneously expanded its diluted earnings per share (EPS) by a CAGR of 11%. On a GAAP basis, the company generated $506M in operating profit in Q2 FY24, growing 7% YoY with a margin of 40%. There is no doubt that the company is a mature business at the moment, but much of the strength in its operational efficiency comes from its economies of scale, driven by strong product penetration across customers coupled with pricing power. This has translated to the company generating strong free cash flow, which it returns to its shareholders in the form of dividends. Over the last 10 years, dividends have grown at a CAGR of 12.99%, and the current dividend yield stands at 2.94%.

Q2 FY24 Earnings Slides: Paychex's robust profitability

Looking forward, the company expects to grow its revenue 5-6% YoY to approximately $5.3B in FY24 while maintaining a GAAP Operating Margin of 41-42%. I believe that the company should be able to achieve this as it continues to spearhead its product innovation cycle by investing in strategic partnerships and AI to drive deeper adoption of its solutions suite. As a result, I believe that the company should continue to return capital to its shareholders in the form of dividends, keeping pace with earnings growth in FY24.

Given that Paychex caters to small and medium-sized businesses, any slowdown, or worse, a recession, will negatively impact the company’s growth prospects. With the Fed keeping rates higher for longer as inflation continues to remain stubbornly above the Fed’s target of 2.2%, small and midsize businesses are especially exposed, as they are often subject to high costs of capital. Therefore, should the US economy tip into a sizable downturn, we can expect to see small and medium-sized businesses laying off their workers and cutting costs, especially their tech stack, in order to protect margins and avoid bankruptcy. In this case, we can expect to see customer churn and lower retention rates, which will negatively affect Paychex’s growth trajectory as well as its overall profitability.

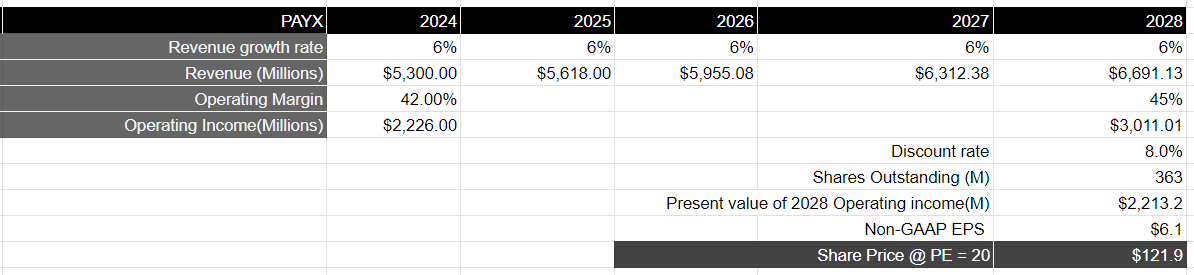

Assuming that the company grows its revenues in the mid-single digits over the next 5 years, it should produce a total revenue of approximately $6.7B by FY28. Meanwhile, assuming that the US economy does not tip into a deep recession and that the company continues to drive its operational excellence by growing its operating margin from 42% to 45%, it should generate close to $3B in operating profit in FY28, which would translate to a present value of $2.2B when discounted by 8%.

Taking S&P 500 as a proxy, where it grows its earnings on average by 8% over a 10-year period with a price-to-earnings ratio of 15-18, I believe that Paychex should be trading at a forward multiple that is 1.2–1.3x the multiple of S&P 500. This would translate to a price target of $122, which is where the stock is currently trading.

Author's Valuation Model

There is no doubt that Paychex has a great track record of operational excellence. Despite the strong fundamentals, I believe that the stock does not provide an attractive entry point at the moment for sizable upside, and as a result, I will be waiting on the sidelines and rate the stock a “hold” at the moment.