metamorworks

metamorworks

No matter what Payoneer Global Inc. (NASDAQ:PAYO) has accomplished in the last couple of years, the stock is still trading below $5. The global payments company faces some headwinds in 2024 due to lower interest rate expectations, but the business remains in growth mode. My investment thesis remains ultra Bullish on the stock.

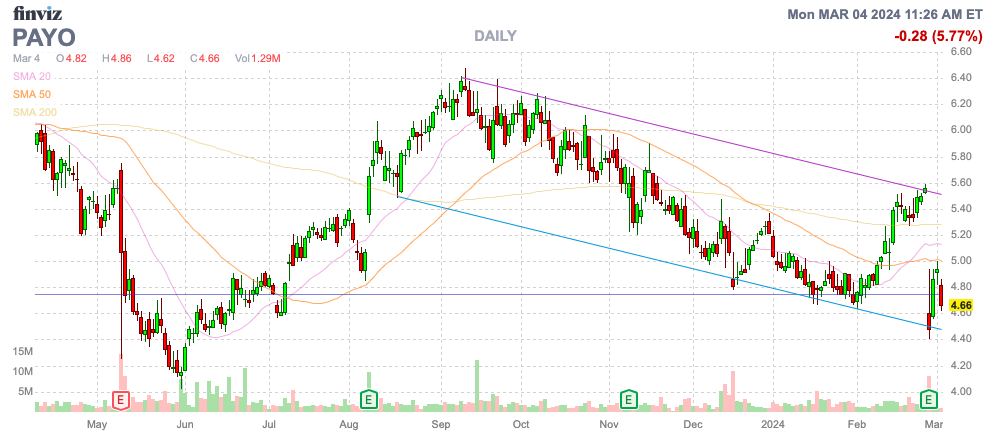

Source: Finviz

Payoneer Global slumped following Q4 '23 results after the payments company again reported strong growth as follows:

Source: Seeking Alpha

The company grew 2024 revenues an incredible 32% to $831 million and generated 25% adjusted EBITDA margins at $205 million. By all measures, Payoneer Global has generated impressive results since going public via a SPAC and the market has completely ignored the results over and over.

The global payments company has grown revenues via both expanding the customer base and increasing interest income from customers funds. The management team did a great job with the Q4 '23 presentation breaking out the different revenue trends.

Payoneer Global definitely benefitted substantially over the last couple of years from the higher interest rates, but the company has a solid payments business with substantial growth opportunities ahead. The company has a $6 trillion TAM in global payments with a current focus on the contractor/freelancer market with a 20% market share in a $300 billion portion of the market.

In the last year, key customers, labeled as ICPs, grew 6% while ARPU was optimized within the relatively flat active customer base for 36% growth led by interest income gains. Payoneer Global has worked on shifting away from money-losing accounts to focus on the higher quality ICPs.

Source: Payoneer Global Q4'23 presentation

The market is likely fretting how interest income has likely peaked with lower interest rates expected in 2024 and beyond. Customer funds grew 9% YoY to $6.4 billion generating $65 million in Q4 '23 interest income.

The bad news is that Payoneer Global guided to 2024 interest income of only $235 million, or ~$59 million per quarter. Considering customer funds have been growing at near 10% annual clip similar to payments volumes, the company is effectively guiding to a material dip in the average interest rate obtained on those funds.

Since around 75% of customers funds are at U.S. domestic institutions, Payoneer is likely too negative on the interest income impact. After the strong jobs report for January, the Fed is likely to keep interest rates higher for longer with no signs of cutting interest rates any time soon.

Payoneer Global guided to the following 2024 numbers:

The key understanding is that the global payments company faces a year of interest income normalization. Interest income will take a step back from the Q4 peak levels, reducing the profit margins and impacting growth rates.

Also remember, Payoneer has a history of conservative guidance. Even throwing out the very weak guidance when Russia invaded Ukraine, the company initially guided to 2023 revenues of just $800 to $810 million and ended up reaching $831 million.

Payoneer Global expects to return to 15% growth in payments related revenues over the midterm and the company should actually expect interest income to boost total revenues again over time. In essence, 15% payments growth should provide up to 20% total revenue growth with the expansion of customer funds over time and the general assumption of flat interest rates once normalized.

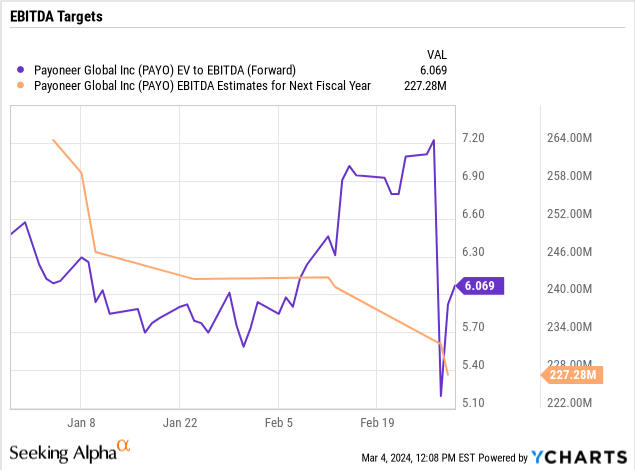

The company guided to an adjusted EBITDA dip of $15 million for 2024 due to the normalization of interest rates. Even with the lower numbers, Payoneer Global trades at only 6x EV/EBITDA targets with a cash balance of $614 million.

If one assumes Payoneer Global can achieve the 15% growth rate, the stock should trade at least with a similar multiple. Payoneer has a long way to go in order to trade at 15x EV/EBITDA targets.

Assuming about 15% EBITDA growth in 2025, Payoneer Global would generate $225 million in EBITDA next year. With ~390 million shares outstanding, the stock would have the following valuations:

The key here is that a payments company typically trades at a premium valuation due to the recurring nature of most digital payments. The stock trading at 15x to 20x forward adjusted EBITDA estimates is more of a base valuation case.

The key investor takeaway is that Payoneer has traded nowhere but down the last couple of years despite strong results. The global payments company will face some headwinds in 2024 led primarily by lower interest rates. Ultimately though, the stock is priced for a disaster, not a business set for 15%+ growth in the future. Investors should use the weakness to continue loading up on a mispriced payments company with catalysts for solid growth for the years ahead.