Kameleon007/iStock via Getty Images

Kameleon007/iStock via Getty Images

Paycom (NYSE:PAYC) recently reported FY23 numbers, so I wanted to take a look at the company’s progress throughout the year and see if this pullback in share prices presents an opportunity to start a position. The company has been going steady over the year, with slight inefficiencies apparent in EBIT margins, and while being financially sound, the company’s top-line growth has somewhat slowed down and a miss on guidance is not a good sign. I am assigning a hold rating until I see substantial improvements in either revenue growth or profitability, but preferably both.

Paycom is a human capital management company that provides cloud-based solutions, primarily in the United States, with plenty of potential to expand internationally. Founded in 1998, the company is a pioneer in offering online payroll services. The company’s services include payroll, talent acquisition, HR management, and time and labor management. The company’s self-service app allows employees to request time off, manage their benefits, and view their pay slips.

As of Q4 ’23 reported on February 7th, PAYC had around $294m in cash and no long-term debt. This is a great position to be in. No worrying about the annual interest expenses which weigh on the company’s potential for further growth. The management can allocate the cash flow as they see fit. Furthermore, many investors don’t like investing in companies with excess leverage, so this should bode well for PAYC and will attract many more debt-averse investors if there is a potential for the company to perform well in the future.

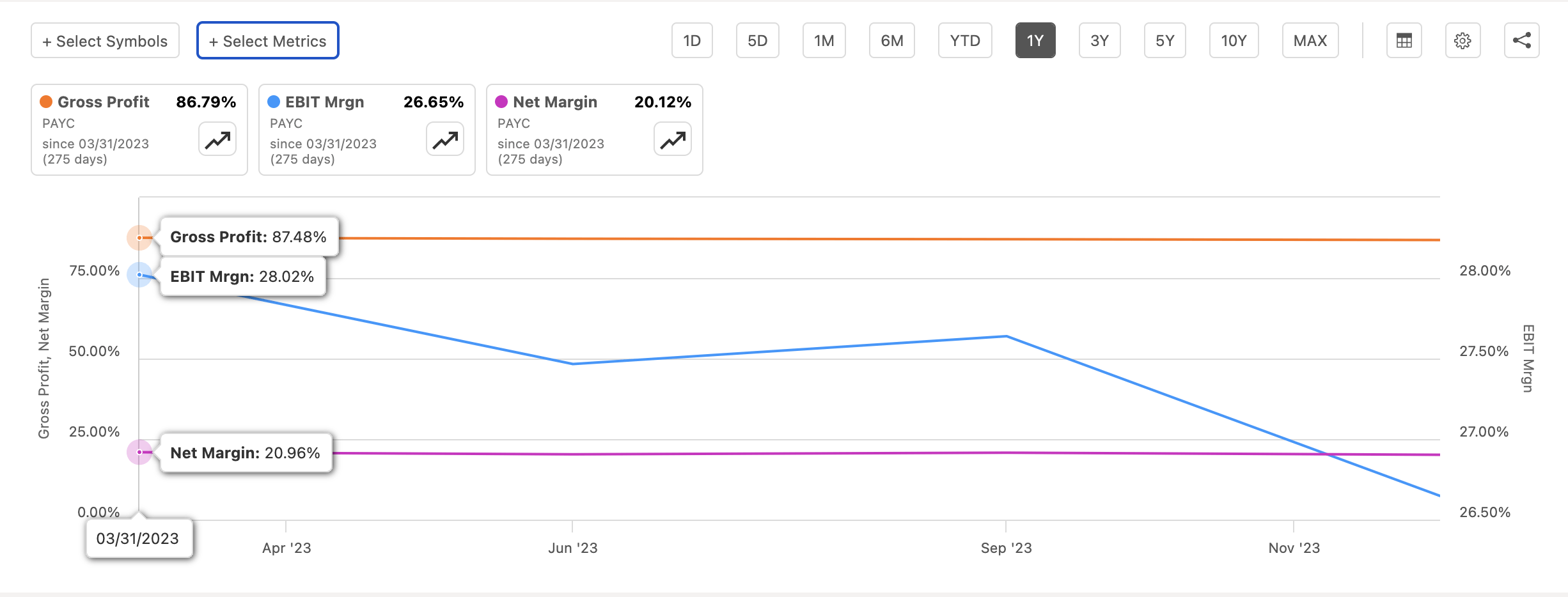

Let’s look at how the company’s profitability and efficiency metrics developed over the last year.

In terms of margins, these have been relatively steady, with EBIT coming down slightly, which tells me that operating expenses slightly increased compared to a year ago. I don’t think it’s anything to worry about for now, but if this continues, we will have to check why these expenses increasing. The variance so far is quite small.

Margins (SA)

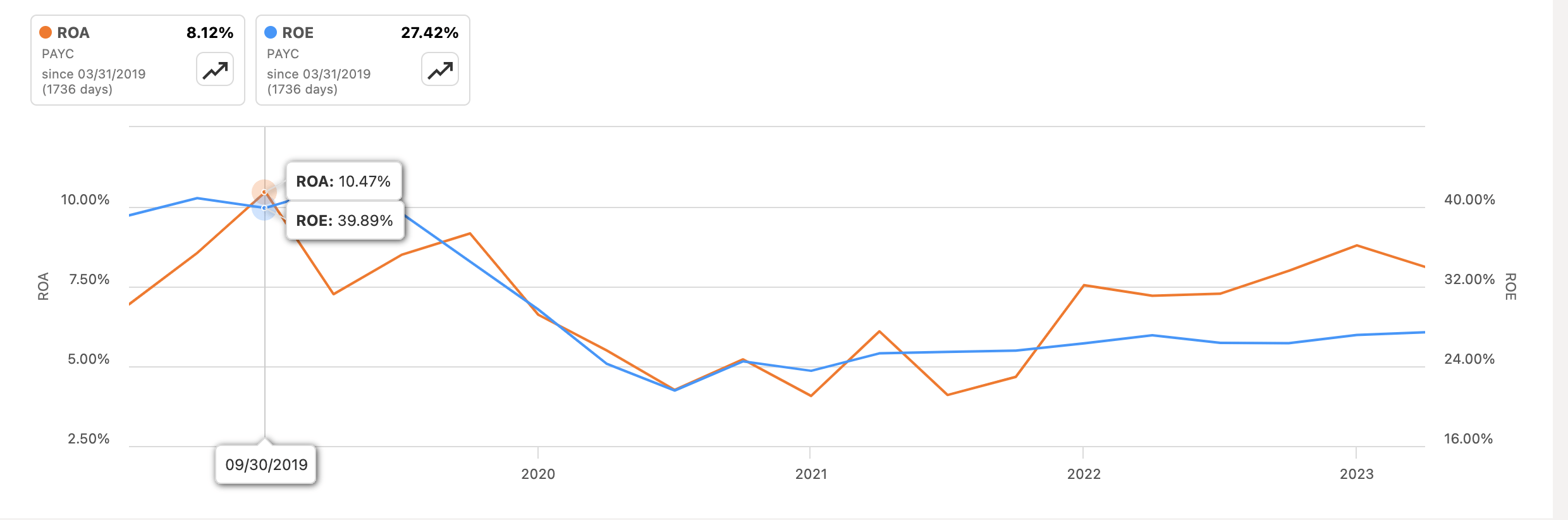

Continuing with efficiency and profitability, the company’s ROA and ROE have been steady also, which is much better than a downtrend, however, if we zoom out a little, we can see that these metrics have not reached the numbers it saw a few years ago, but if the company can improve its bottom line going forward, these should improve also. Nevertheless, it seems that the management is capable of allocating the company’s assets and shareholder capital efficiently (although not as efficiently as before).

ROA and ROE (SA)

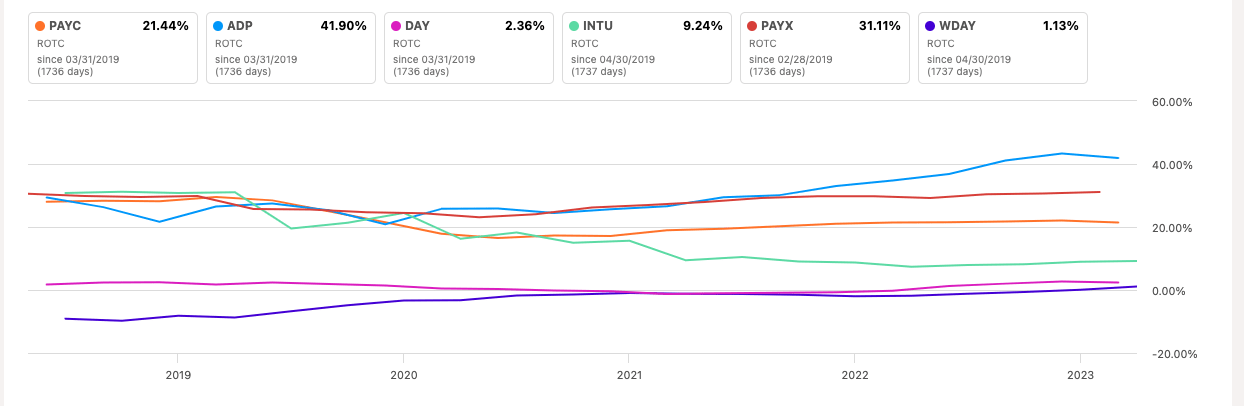

In terms of competition, the company’s ROTC compared to some of its peers found on their 10K report, is somewhere in the middle of the pack, which is not bad, given that it’s over 20%. I usually look for at least 10%, so the company seems decent in that regard. Furthermore, the peers may not be 100% comparable given the fact that some of them are much bigger in terms of market capitalization, which means they have much more resources to outperform. The closest of the peers below is Dayforce Inc. (DAY), which PAYC blows out of the water.

ROTC vs Peers (SA)

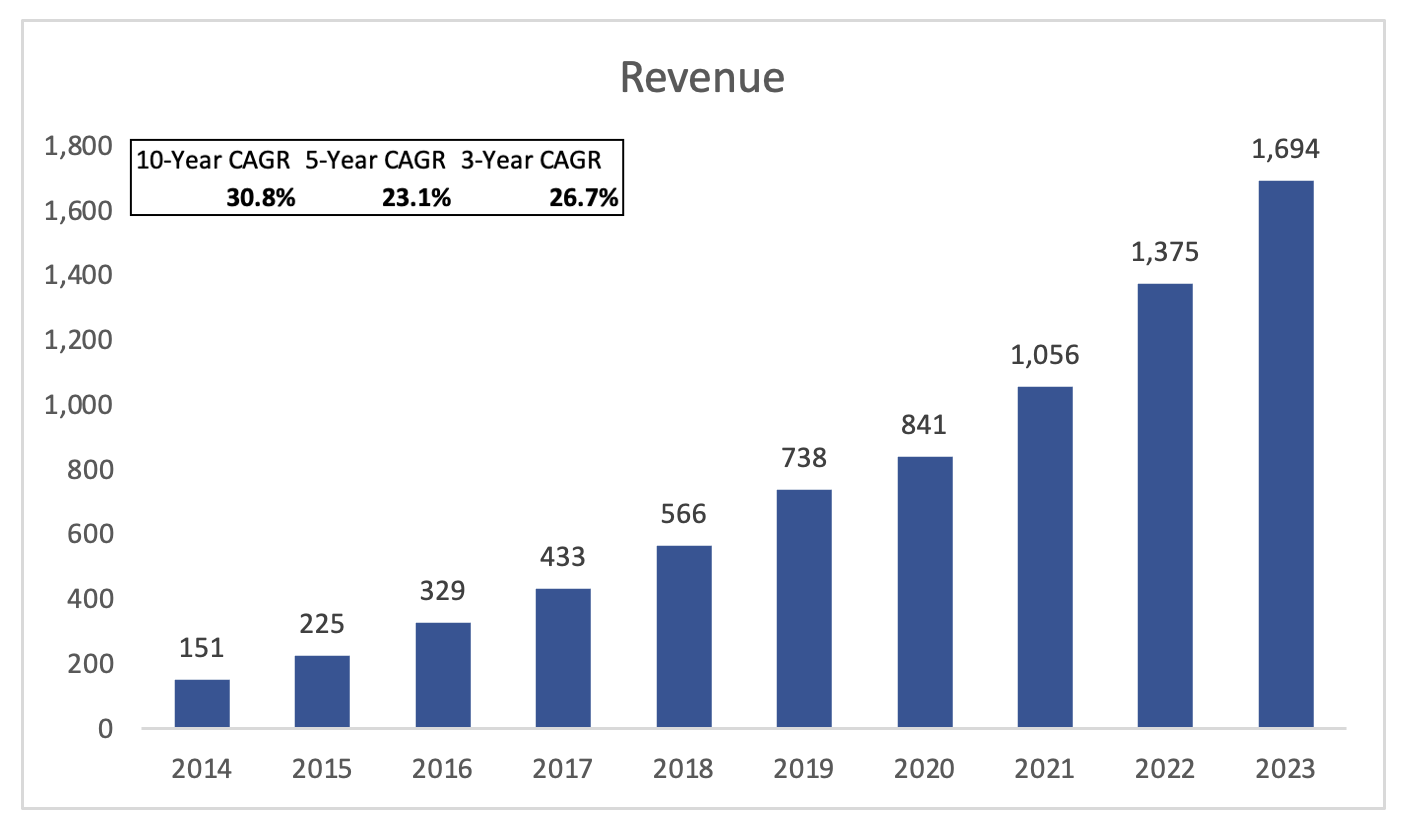

In terms of revenue, I am very impressed with how the company grew over the last decade. I see very steady growth and at a decent pace, nonetheless. So, I was a little surprised to see that analysts are estimating quite a drop in growth over the next couple of years. It seems that a tougher year is coming for the company, which will slow its growth in half if we go by these estimates, and that will affect my valuation model dramatically. The management is guiding around 11% for the next year, which is quite a decline, but given the uncertainty in the economy, an 11% growth is still rather commendable where many companies see declines in such uncertain times. I believe that the company is not able to cross-sell to existing clients as much as they did in the past, and the number of clients is not growing very quickly, just at around 1% in the latest quarter. The management didn't specify why the top-line growth will be around 11%, but that would be my guess.

Revenue Growth (Author)

Overall, the company has been performing rather well in my opinion. Very steady revenue growth, with steady efficiency and profitability. On top of that, the company’s financial position is also very healthy, which should help it survive any sort of downturn in the economy.

Paycom beat on EPS and revenue. Non-GAAP EPS came in at $1.93, a beat of 15 cents, while revenue came in at $434.6m, a beat of $12.21m. A beat on the top and bottom lines, so why did the stock plummet? As usual in these markets, guidance is what matters, and the company has disappointed on that front. The management guided the top line to come in at $494m to $497m, which is below the consensus of $499.64m. I don’t think the guidance was all that bad and it didn’t warrant such a selloff. Still, in such a market any slight miss on guidance will be reflected greatly on the share price, which can present a good opportunity to get in for the long haul if the company is not overvalued, which we will get to see shortly.

It's good to see that a company like Paycom managed to beat on both ends, in such a tough macro environment. It tells me that the company's services are in very high demand, which means that once the economic uncertainties fade, the company should see its services to be in even higher demand. However, seeing that the management guided for a slight slowdown in the top line, these economic uncertainties are rearing their heads. They may affect the company's profitability for at least the next quarter. Inflation is still not where the Fed wants it to be, so I would expect subpar performance for a little longer.

In terms of guidance, I think the overreaction was not warranted as the company just barely missed the consensus. What I took from the report is that the revenue growth will continue to slow down, which will affect the company's valuation in the short term quite a bit.

My main concern is the company’s ability to retain its strong top-line growth going forward. We saw that the company managed to grow much slower than in the past, which is not ideal.

The company’s new initiative Beti (Better Employee Transaction Interface) was meant to be the thing that will bring about growth in the long run, however, it has been a little bit of a rollercoaster ride. While initially, Beti did contribute to growth overall, automation and efficiency helped attract new clients, however, the self-efficiency of Beti has reduced revenues from non-recurring services. It is getting tough to convert the remainder of its clients to Beti, which weighs down on its potential overall. I do think that this is going to be a short-term obstacle that eventually will start to contribute much more to the top-line growth, however, is the top-line growth going to return to its historical 3-year average as shown above? Only time will tell, so I will have to keep my assumptions quite conservative to account for this uncertainty.

The company has a lot of opportunities for growth outside of the US. The recent entry into the UK, and the global HCM product, coupled with Beti, will open a lot of doors and should translate into many more clients in the future, which I believe will help the company maintain its high-double-digit revenue growth for a while. That is if the management doesn’t drop the ball. So let’s look at what kind of valuation would be appropriate.

As I alluded to earlier, I will have to take a cautious approach to the company’s top-line growth potential, mainly because I don’t like being overly optimistic about any company’s prospects. That way I am getting a built-in margin of safety and a better risk/reward outcome. So, for revenue growth, I decided to go with around 10% CAGR over the next decade, which accounts for the less-than-exciting growth potential of Beti and international expansion. To cover my bases, I am also modeling a more conservative scenario and a more optimistic one, to give myself a range of possible outcomes. Mind you my optimistic case is still rather on a more conservative end. Below are those estimates, with their respective CAGRs.

Revenue Assumptions (Author)

In terms of margins and EPS, I also decided to go with lower estimates than what the analysts are estimating the company will manage to achieve, just to be on the safer side of things. Over the next decade, the company will see slight improvements in its margins but very small, around 100bps on gross margins, and I decided to keep EBIT margins as seen at the end of FY23 just to keep it even more conservative. Below are those estimates, as compared to FY23.

Margins and EPS Assumptions (Author)

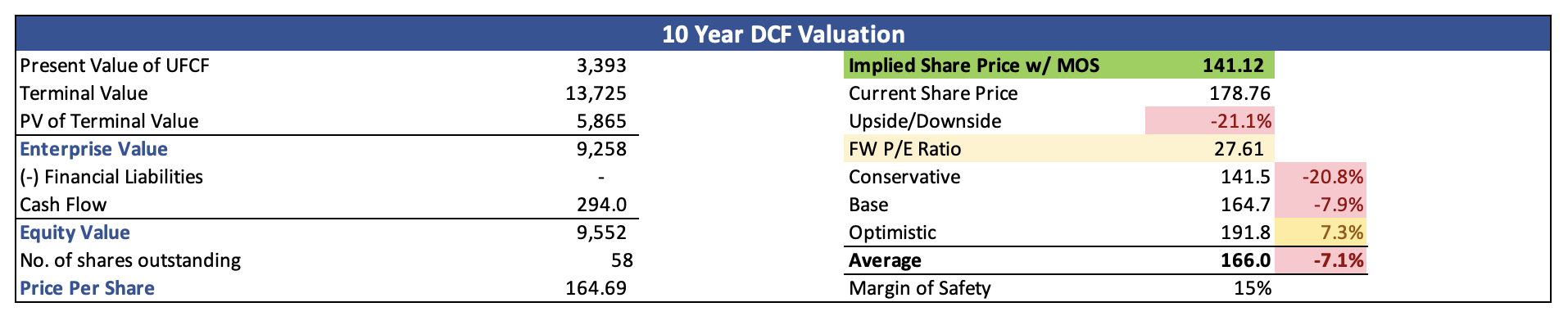

For the DCF model, I went with the company’s WACC of around 9% as my discount rate and 2.5% as my terminal growth rate. I usually like to go with a 10% discount but since I beat down the estimates above, I think the company’s WACC will do the trick. Furthermore, I added another 15% discount to the final calculation just to really be safe in case my assumptions are off. With that said, Paycom’s conservative intrinsic value is around $141 a share, which means that the company is trading at a slight premium to its fair value.

Intrinsic Value (Author)

So, it looks like the company is slightly overvalued according to these conservative estimates. The key here is “conservative”. I believe the company is worth a lot more than what I modeled, however, to keep it on the more cautious side, I would need to see growth reaccelerate and margins start to improve considerably. Furthermore, the uncertainty in the markets and economy will play a big role in deciding where the shares of the company will be trading in the short term. I believe that the company is worth a lot more because the slowdown in revenues and deterioration in margins is a short-term problem. I also believe that the company will successfully penetrate a bigger market internationally, which should reaccelerate its top-line growth potential but that is also a big problem if PAYC doesn't manage to grow its client base. As I mentioned earlier, the company saw a 1% increase in clients y/y. That is not the growth I'd like to see, as that puts a damper on my revenue estimates.

I believe the company will be able to achieve my requirements, however, I am not the one to hope for improvements, as I would like to see these numbers improving before I jump in with my capital for the long haul. Therefore, I am assigning a hold rating for now, until the company shows me tangible proof that operations are trending in the right direction. Once I see the results, I will be updating my model, to reflect such changes. If the company manages to grow at around 19% CAGR while keeping the same margins as they have now, the company could easily have around 40% upside from today's prices, but that is not how I like to look at valuation because that is just wishful thinking.

I will be following the company's financials over the next couple of quarters to see how its operations are progressing and would like to see growth reaccelerate and margins improve. I will also be very interested in seeing how Beti is progressing along, and if the company succeeds in bringing most of its clients to use it, as that seems to be their biggest catalyst and the most promising development so far, besides continuing to expand internationally.