Nils Jacobi/iStock via Getty Images

Nils Jacobi/iStock via Getty Images

Pet humanization is a potent secular trend. During the pandemic, this statement, which I personally firmly believe in, allowed some investors to hypothesize that pet care equities, with direct or indirect exposure and regardless of their sector classification and valuation, are defensive in nature, and that they would be growing at outsized rates ad infinitum, which is a bit specious, to say the least. This mistake cost them dearly.

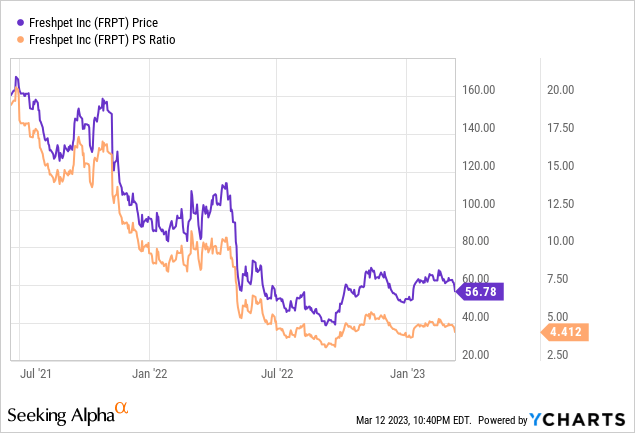

In my 2021 article on the ProShares Pet Care ETF (BATS:PAWZ), I touched upon valuation risks that surrounded this investment vehicle back then. With the pandemic supercharging a few trends like remote work that, in turn, resulted in growing pet ownership, multiples of stocks related to the theme soared, with Freshpet (FRPT) perhaps being the best example of a pet food name that traded with a growth tech-ish valuation, with ~22x Price/Sales in May 2021, a ratio completely disconnected from the reality that since then has shrunk to ~4x as realists prevailed amid inflation and other headwinds.

And as PAWZ was too richly priced back then, I opted for a conservative Hold rating.

And now? A great deal of froth has been removed, so multiples might have normalized, with pet humanization still being a trend I have hard time believing will disappear any time soon. Have PAWZ become a Buy then? Not exactly. There are a lot of moving parts here. Let me elaborate on that.

The cornerstone of PAWZ's investment strategy is the FactSet Pet Care Index. As mentioned on the fund's website, the idea is to amalgamate stocks "that potentially stand to benefit from interest in, and resources spent on, pet ownership." Importantly, both U.S. and international stocks can compete for a place in it, which adds a few FX-related risks to the fund's strategy (in the current iteration, I see the risks stemming mostly from the pound sterling exposure). For more details on the methodology, which is rather nuanced, I strongly recommend reading the prospectus which is available on the fund's website.

Since my June 2021 coverage, the PAWZ portfolio has seen thorough recalibration, owing to both additions/deletions and capital appreciation/depreciation of the holdings. More specifically, as its market value has cratered, Freshpet is no longer amongst its top five holdings, with a 4.4% weight vs. almost 10% previously. I also noticed that four stocks were removed, including Tractor Supply Company (TSCO) and Boqii (BQ). Covetrus, a heavyweight animal health industry player operating globally, is absent since it was acquired by Clayton, Dubilier & Rice and TPG in 2022. By the same token, owing to a takeover, the ETF now has no exposure to previously Frankfurt-quoted Zooplus. Meanwhile, I found eight additions (8.5% weight), with the most notable being Pet Valu (PET:CA) (OTCPK:PTVLF), a Canadian pet products retailer.

During the July 2021 - February 2023 period, PAWZ delivered a negative 24.3% compound annual growth rate as inflation and FX headwinds conflated to send share prices of its holdings cratering. It is not to be overlooked that this horrible rate is principally the consequence of its 40% decline in 2022. And though the tech-heavy iShares Core S&P 500 ETF (IVV) was also down during that period, its negative 3.2% CAGR does not look that harrowing.

| Portfolio | IVV | PAWZ |

| Initial Balance | $10,000 | $10,000 |

| Final Balance | $9,471 | $6,284 |

| CAGR | -3.21% | -24.33% |

| Stdev | 20.55% | 25.69% |

| Best Year | 11.73% | 7.54% |

| Worst Year | -18.16% | -40.07% |

| Max. Drawdown | -23.93% | -47.10% |

| Sharpe Ratio | -0.14 | -1.01 |

| Sortino Ratio | -0.19 | -1.19 |

| Market Correlation | 1 | 0.9 |

Created by the author using data from Portfolio Visualizer

So even with the spectacular 61.7% total return in 2020, PAWZ, which was incepted in November 2018, is now way behind IVV (the period below is December 2018 - February 2023).

| Portfolio | IVV | PAWZ |

| Initial Balance | $10,000 | $10,000 |

| Final Balance | $15,459 | $13,056 |

| CAGR | 10.79% | 6.48% |

| Stdev | 19.70% | 22.79% |

| Best Year | 31.25% | 61.69% |

| Worst Year | -18.16% | -40.07% |

| Max. Drawdown | -23.93% | -47.10% |

| Sharpe Ratio | 0.55 | 0.33 |

| Sortino Ratio | 0.83 | 0.5 |

| Market Correlation | 1 | 0.88 |

Created by the author using data from Portfolio Visualizer

Obviously, it seems most excesses have been removed, with the portfolio now looking different from its pre-bear market version. So is PAWZ an adequately valued play to consider now? Hardly. There are a few issues to discuss here.

As usual, let me start with the Quant data. Please take notice that for non-U.S. companies, I used American Depositary Receipts instead of the ordinary share tickers in my analysis. One of the examples is Nestlé (OTCPK:NSRGY), a Swiss consumer staples mammoth; PAWZ holds Zurich-quoted NESN shares, while I used NSRGY in my adjusted dataset.

First, over 71% of the holdings has a Seeking Alpha Quant rating. In that group, five players have a B- Valuation grade and better, together accounting for ~11.1% of the net assets, a fairly small amount. A nice example here is Patterson Companies (PDCO), a dental and animal products distributor with an A grade, which can be explained by its rather sluggish growth profile. When I analyzed the fund the previous time, ~19% was undervalued.

Next, ~56% (11 stocks) are obviously imperfectly priced, with the market expecting too much from them, which is reflected in their D+ grade and worse. In my opinion, this is intolerably large for the current environment as growth premium is still a concern owing to uncertainty surrounding the interest rate question. One example of a dangerously valued stock is Zoetis (ZTS), a global leader in the animal health industry and the fund's top holding with 11.1% weight.

Of course, we can use traditional multiples taken separately instead of looking at composites. So with the weighted-average market cap of around $46.5 billion, PAWZ has an earnings yield of less than 2%, as per my calculations. It should also be noted that the fund's website shows an index P/E of ~29.7x as of 30 December 2022, which translates into a ~3.3% earnings yield.

PAWZ website; the screenshot taken March 12, Eastern Time

Next, looking at Price/Sales, which, according to my computations, stands at ~4x, I believe investors would concur that the margin of safety is non-existent here. This is especially interesting as the WA forward revenue growth rate is only ~9.4%.

Finally, we should not forget about quality. One of the issues is that about 29% of the companies in the portfolio are loss-making, while more than 14% are outspending net operating cash flow. The ~28.7% difference between Return on Equity and Return on Assets (only ~6.6%) points to the fact that most holdings actively used debt, so ROE is unreliable. The silver lining is that ~51% have a B- Quant Profitability grade and better.

Overall, I do not believe PAWZ's valuation match its growth and quality characteristics.

With pet humanization being a potent, hardly reversible trend, investors might consider allocating capital to portfolios centered on pet care exposure to reap benefits longer-term.

With that being said, I am of the opinion that if one is looking to benefit from that trend, it is worth being exceedingly picky, proceeding with extreme caution, probably skipping tech-ish plays for more defensive names like Nestlé, also paying attention to valuation and other risks involved.

That is to say, PAWZ is not the best option to consider buying into today. A solid deal of froth has been removed, no doubt, especially when it comes to FRPT, but the risks have not completely evaporated, and the fund's earnings yield below 2%, as per my calculations, is a perfect illustration. In sum, this ETF is a pass.