SvetaZi/iStock via Getty Images

SvetaZi/iStock via Getty Images

UiPath (NYSE:PATH) is a stock that a few people reached out to me for insights, on the back of its Q4 2024 results.

I very much like this business, given that it has no debt on its balance sheet. For me, that's a very important starting position. These considerations don't matter in ebullient markets. But I know from experience that one can't always rely on such strong and exuberant markets. More specifically, this highly free cash flow producing company carries approximately 7% of its market cap as cash.

Furthermore, after a rocky few years, UiPath is turning around its prospects, and for now, the stock is attractively valued. More specifically, I believe that PATH is priced at 35x forward non-GAAP operating profits.

Last month, I stated in a bullish analysis:

I argue that [UiPath] is still reasonably priced, even though it operates in what's arguably the hottest sector of the market.

As you'll soon see from my reasoning, I strive to be very conservative with my assumptions to allow me plenty of room for error.

Accordingly, I believe that UiPath is an attractive stock, while it's priced at 47x forward non-GAAP operating income.

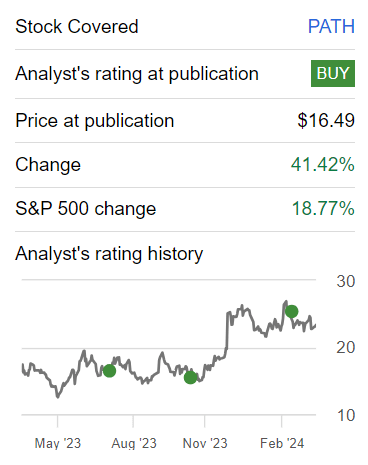

Author's work on PATH

It turns out that UiPath is actually slightly cheaper than I previously presumed, at closer to 35x forward non-GAAP operating profits. Furthermore, as you can see above, I've been recommending this stock for a while and it is up 41%, nicely outpacing the S&P 500, which is up 19%.

UiPath creates software to help businesses automate repetitive tasks. Essentially, they develop tools that use artificial intelligence to teach computers how to perform tasks that humans usually do, like processing invoices or organizing data. This automation frees up time for employees to focus on more important while improving efficiency and reducing errors. In simpler terms, UiPath's technology helps businesses save time and money by having computers handle mundane tasks.

UiPath's near-term prospects appear promising. Firstly, their strong financial performance, including surpassing guidance for both top and bottom-line metrics, reflects robust demand for their automation platform.

With a focus on customer success, UiPath has the right narrative of a company that seeks to capitalize on the growing importance of AI-driven automation in fulfilling organizations' strategic objectives. The increasing adoption of their business automation platform by both large enterprises and smaller businesses underscores the broad applicability and value proposition.

Moreover, UiPath's strategic partnerships with industry leaders like SAP (SAP) further enhance their market presence and open up avenues for collaboration and expansion.

Additionally, the introduction of innovative products like Autopilot, which simplifies automation development and process improvements, demonstrates UiPath's commitment to driving innovation.

However, UiPath faces headwinds too. One challenge is the intensifying competition in the automation market. This is likely to lead to UiPath encountering pricing pressure, from the likes of Microsoft's Power Automate (MSFT).

Given this background, let's now discuss its fundamentals.

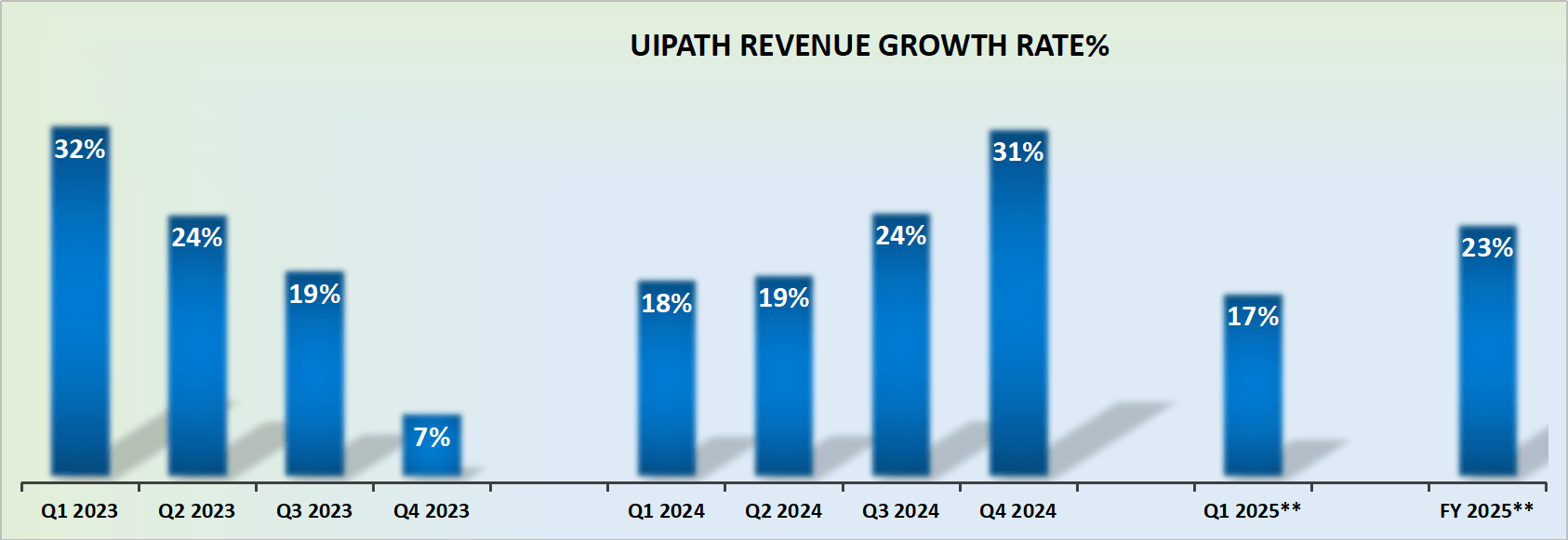

PATH revenue growth rates

In my previous article, I wrote:

Author's work on PATH

I stand by this contention. What you see here is a business that was always going to finish Q4 2024 with very strong revenue growth rates, given that the comparables with the prior year were remarkably easy.

But this is where this investment thesis could get derailed. Fiscal H1 2024 was supposed to be very strong, given that the comparables with the prior year were relatively easier than fiscal H2 2024. While I don't believe this is a significant consideration, it is something to keep in mind.

Next, we'll turn our focus to its valuation.

Before we discuss its valuation, let's get some further context.

Q4 2024

What you see here is that fiscal Q4 2024 ended with 27% non-GAAP operating margins, a 500 basis points expansion from the same period a year ago.

Naturally, these margins are already quite high and this means that on a go-forward basis, it will be difficult for UiPath to squeeze out a lot more efficiencies.

That being said, when UiPath guides for fiscal 2025 to see its underlying non-GAAP operating margins reaching 19%, I believe this echoes my assertion. Meanwhile, the fact that this early in the game UiPath has already delivered 27% non-GAAP operating margins does imply that there's scope for increased profitability and that we should, in actuality, see UiPath's 19% non-GAAP operating margins as a base.

And I believe that there's the potential for this profitability profile to be upwards revised higher in the coming quarters.

Therefore, I believe that UiPath is capable of reporting around 23% non-GAAP operating margins at some point this year. To be clear, this doesn't necessarily mean this happens this year. Rather, there's a potential for it to happen as a forward run-rate starting in the next twelve months.

Altogether, I believe this puts UiPath on a path towards $370 million of non-GAAP operating income.

This would be a 55% to 60% increase in profitability relative to fiscal 2024 (the year just completed).

Therefore, this implies that UiPath is priced at 35x forward non-GAAP operating profits. This is not expensive for a business that is well positioned, with an alluring narrative, that's growing in the mid-20s% CAGR.

In conclusion, UiPath presents an enticing investment opportunity with its clean balance sheet, attractive valuation, and impressive growth rates.

With no debt on its balance sheet and approximately 7% of its market cap held as cash, UiPath stands on a solid financial foundation.

Priced at approximately 35x forward non-GAAP operating profits, the company's robust revenue growth rates and expanding non-GAAP operating margins, point to a promising future trajectory.

As UiPath continues to capitalize on the growing demand for AI-driven automation and strengthen its strategic partnerships, it is well-positioned to sustain its growth momentum and deliver substantial shareholder value in the near term.