JulPo

JulPo

My recommendation for PAR Technology (NYSE:PAR) is a buy rating, as I expect growth to continue into the near term. Especially with the addition of Stuzo and potentially TASK, I believe the growth outlook has gotten a lot more positive than when I last looked at the company. Note that I previously rated buy rating for PAR as I believed the TAM was large enough for PAR to continue winning share and upsell its products to drive ARPU expansion. Underlying its ability to do so was a set of strong product portfolios that helped restaurants achieve digitalization.

PAR reported 4Q23 revenue of $107.7 million, just a touch above consensus of $106 million. Contract revenue came in at $38 million; service revenue came in at $46 million; and product revenue came in at $24 million. As for ARR (annual recurring revenue), it came in at $137 million. Overall gross profit grew to $26 million, with gross margin coming in 100bps above consensus (25% vs. 24%). That said, operating expenses came in at $41 million, which led to adj EBITDA falling below consensus expectations (-$4 million), and adjusted net income came in at -$9 million (adj EPS of -$0.33).

I would say this is a pretty strong set of results that continue to support my bullish view on the business. Several operating metrics and underlying performance continue to point to continued growth ahead. Firstly, PAR reported a total ARR of $137 million, which equates to 23% y/y growth, with strength coming from OS (operator solutions) ARR of $60 million (grew 45% vs. 4Q22). This, along with management's comment that Brink's win rates were on the rise, suggests that PAR is successfully winning share from legacy point-of-sale [POS] systems. PAR also continues to see strong adoption across the product portfolio. As current customers continued to implement the Payments module, OS bookings saw 3.4k (a sharp acceleration from the 1.1k additions seen in 3Q23). In addition, there were 70.8k active sites at the end of 2023, with 3,200 site activations in 4Q23 and 1,000 in 3Q23. Twelve new logos were also added to Punchh during the quarter, and MENU celebrated its first logo go-live. This, again, supports my view that PAR is able to up-sell or cross-sell its products to existing customers to drive up ARPU. Indeed, OS ARPU increased 15% y/y while ARR per site increased 21% y/y to ~$2.6k. These are clear evidences of PAR success in driving effective price increases (50% of ARPU lift), driving up adoption of payment modules, upselling higher-value deals, etc. With the continued launch of larger deals at a higher ARPU, I would expect PAR to sustain this pricing momentum.

With the addition of Stuzo and the potential acquisition of TASK, I have become more bullish on the business. For background, PAR closed its acquisition of Stuzo for $190 million in cash and stock. Stuzo is a digital engagement software provider for convenience and fuel retailers and has entered into an agreement to acquire TASK Group (expected to close in 3Q24) for $206 million, an Australian global foodservice transaction platform that includes commerce solutions and customer engagement tools.

My opinion is that the addition of Stuzo to the PAR portfolio will help PAR accelerate its penetration in the convenience store segment. In particular, I believe that PAR will be able to rationalize Punchh costs and create synergies in the C-store segment through the integration of products. Keep in mind that management has previously mentioned that the convenience store segment is the fastest-growing category. With Stuzo, PAR should be in a better position to take advantage of this opportunity. It should also be noted that this deal will not dilute unit economics because Stuzo was already operating above the rule of 40 (ARR growth + adj. EBITDA margin) before the acquisition. In the LTM-to-October 2023 period, the company reported over $40 million in ARR, $14 million in EBITDA, and a net retention rate [NRR] of over 111%.

So I feel very good about it. And in many ways, C-store, as I said, is our fastest-growing category at PAR, and we just haven't given it the oomph that it needs, and this certainly does that. TASK acquisition call

Regarding TASK, I am even more positive about this deal than the one with Stuzo. With TASK's all-in-one unified platform, PAR's international exposure will be immediately expanded, reaching over 110 enterprise customers in 70 countries. Notably, TASK has a long list of notable clients, including McDonald's and Starbucks; with this acquisition, PAR will be able to cross-sell international expansion to its current domestic clientele and acquire new international logos with greater efficiency. Besides international markets, management also highlighted foodservice formats like stadiums, hotels, and travel as potential avenues for expanded TAM.

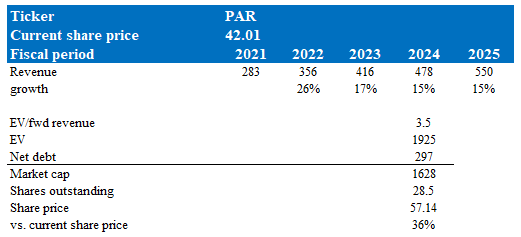

Author's valuation model

According to my model, PAR is valued at $57.14 in FY24, representing a 36% increase. This target price is based on my growth forecast of 15% over the next two years. The rationale for the mid-teens growth rate is that underlying momentum continues to be strong, and PAR’s FY23 results actually came in a lot better than I originally expected (17% vs. my expectation of 13%). With the inclusion of Stuzo and, potentially, TASK, I expect growth to be higher than my previous expectation of 13%. The addition of these two deals, as I talked about above, structurally improves the business in terms of its ability to continue upselling and capture a larger part of the TAM. As such, I think the PAR valuation multiple deserves to trade at a premium to where it is trading today. Over the past 2 years, PAR has traded at an average of around 3.2x forward revenue, and I assume it will trade at 3.5x (just modestly above).

The potential downside risk is execution. Suppose the TASK deal goes through, PAR needs to integrate two acquisitions this year that increase execution risk. While I view both TASK and Stuzo as solid acquisitions with the potential to drive ARR acceleration in the medium term, any misintegration could delay the potential acceleration in growth.

Summarizing this post, the recommendation for PAR is buy. PAR remains a buy as the business fundamentals are strong, with robust ARR growth and successful upselling. The Stuzo acquisition strengthens PAR's presence in the high-growth convenience store segment, and the potential TASK acquisition unlocks significant international expansion and cross-selling opportunities. While integrating two acquisitions in one year presents some execution risk, the long-term benefits are positive.