da-kuk

da-kuk

Check Point Software Technologies Ltd. (NASDAQ:CHKP) stock has had a solid past 12 months on the back of easing macro headwinds and growing investor confidence in the company's expanding portfolio of modern cyber security solutions. The recent rise in earnings multiple appears to be driven more by general investor enthusiasm for cyber security than anything company-specific.

While Check Point's valuation isn't overly high, the company continues to generate weak revenue growth and faces declining margins. It also should be kept in mind that this growth comes after a number of acquisitions and new products. There is also the prospect of increased competition, as larger platforms are forced to fight for market share to maintain growth.

While there has been increased optimism surrounding cyber security in recent months, it is not clear that this is really warranted. Traffic and cloud workload growth should remain solid, while seat growth is likely to remain weak. Growth should also be supported by an ongoing need for protection against increasingly sophisticated attacks. Customers are coming out of a period of heavy investment though, which will continue to weigh on things like hardware sales for some time. For example, Fortinet, Inc. (FTNT) believes that it is only around halfway through the current firewall down cycle.

Check Point has suggested that its bookings began to pick up in the third quarter, with this becoming more noticeable in Q4. This strength should translate into billings and revenue over the next few quarters.

In comparison, Palo Alto Networks, Inc.'s (PANW) performance continues to soften, although this has largely been attributed to the company's Federal Government business. Palo Alto has also suggested that customers have spending fatigue from investing in point solutions to try and create better security outcomes. Despite this weakness, Palo Alto has suggested that the demand environment has been fairly consistent in recent quarters and is improving at the margin.

Figure 1: Job Openings Mentioning Cyber Security in the Job Requirements (Source: Revealera.com)

Investor expectations for cybersecurity in general appear to be unrealistically high at the moment. This is probably the result of an increased probability of looser monetary policy, a reduction in customer cost-cutting efforts, and tailwinds from SEC reporting requirements.

While investor expectations are high, current market conditions remain soft and this appears to be increasing competition. Check Point has suggested that competitors are offering more flexible terms. Palo Alto has also stated that some legacy vendors and startups are resorting to uneconomic pricing in order to win customers.

Palo Alto is not completely innocent here either, though, using its financial strength to attract customers through things like financing. This looks like it is going to step up significantly going forward though, with Palo Alto wanting to accelerate consolidation. Proposed programs include legacy trade-ins, no-cost introductory offers and product add-ons, and incentives to accelerate standardization. If Palo Alto is serious, and peers retaliate, this could create significant headwinds, particularly for legacy vendors with weaker product offerings.

Check Point's portfolio includes:

Refresh projects in Quantum appliances have been weak, with customers choosing to delay deals as a result of the macro environment. Outside of current macro weakness, Fortinet and Palo Alto are formidable firewall competitors and I would expect them to continue to take market share.

Check Point's customer base provides it with a large opportunity to sell more modern security solutions, like SASE and AI-powered security operations. This should support growth in the near term, but it doesn't ultimately change the long-term prospects of the business. This situation is not dissimilar to Palo Alto, where 70% of its SASE deals are coming from existing customers. Check Point's new business growth was in the double-digits in the fourth quarter of 2023 though, which may refute this idea.

Check Point's Infinity platform and Harmony E-mail continue to be areas of strength. Infinity revenue now contributes more than 10% of Check Point's total revenue.

Check Point's growth is also being driven by new product introductions and acquisitions, including Horizon Playblocks, Infinity Global Services, Perimeter 81, and Atmosec. Horizon is a prevention-first security operations security suite, which includes an MDR SOC service and an XDR SOC platform. Playblocks is a collaborative security platform that automates security, helping to save time and resources. It aims to prevent attacks from spreading by eliminating siloes. Check Point also launched Infinity Global Services at the start of 2023, which provides customers with a range of services that help to alleviate problems caused by a shortage of cybersecurity talent.

Perimeter 81 was nearly a half a billion USD acquisition which forms the basis of Check Point's SASE solution. Check Point also recently acquired Atmosec to expand its technology portfolio. Atmosec is a SaaS security vendor that provides technology to secure applications that are being run from the cloud.

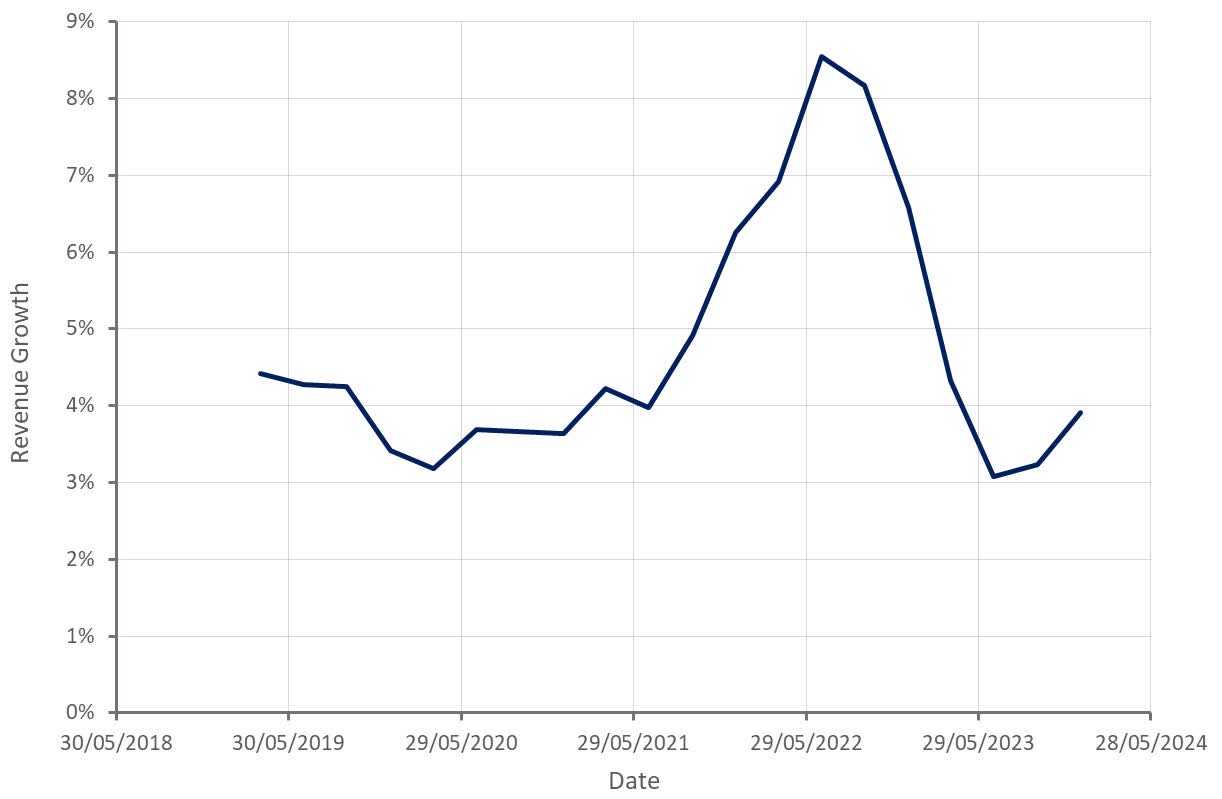

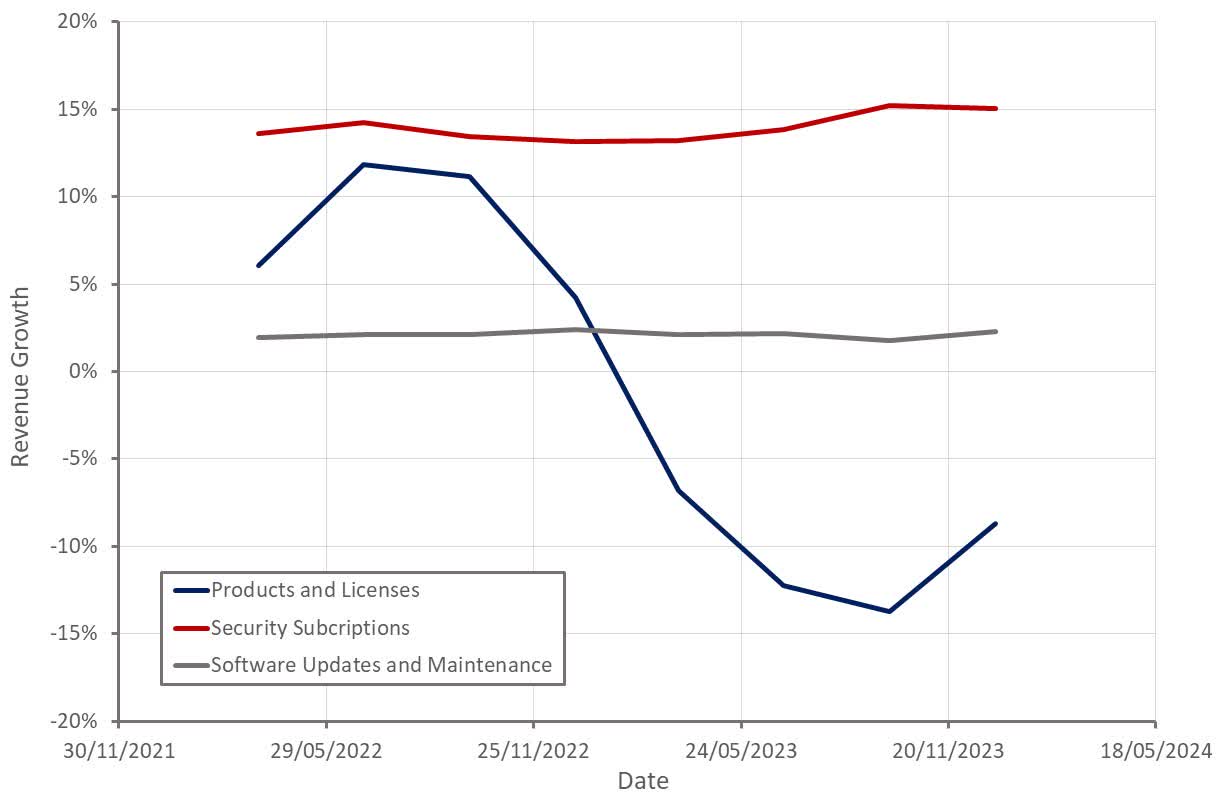

Revenue growth continues to be driven by subscriptions, which were up 15% YoY to $266 million USD in the fourth quarter. Check Point expects $2.475-2.625 billion USD in revenue in 2024, up 5.6% at the midpoint. First quarter revenue is expected to be between $575 and $610 million USD, representing an increase of 4.6% YoY at the midpoint. This suggests a continuation of the recent growth acceleration that Check Point has witnessed, largely driven by subscription strength and a moderation in product and license declines. It is likely that a significant portion of this increase in growth is attributable to the Perimeter 81 acquisition, though.

Figure 2: Check Point Revenue Growth (Source: Created by author using data from Check Point) Figure 3: Check Point Revenue Growth by Segment (Source: Created by author using data from Check Point)

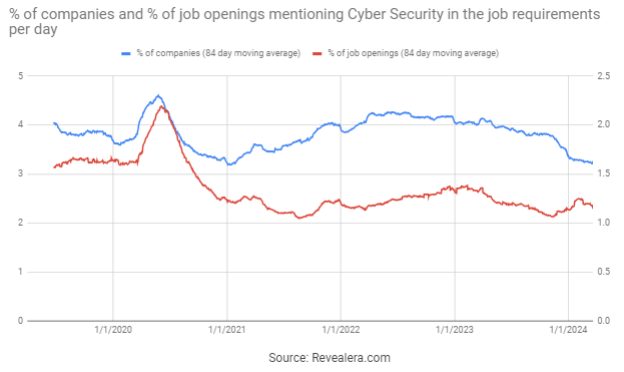

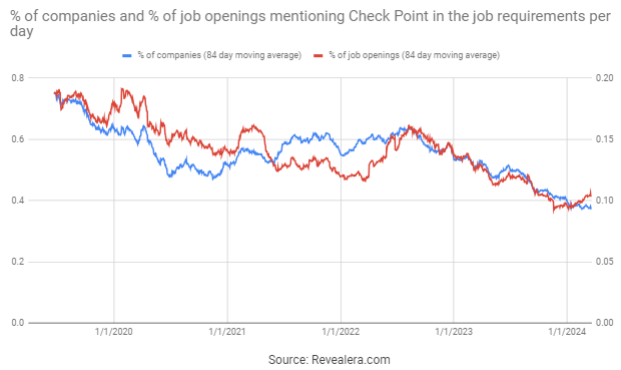

The number of job openings mentioning Check Point in the job requirements also possibly points to a stabilization or possible increase in demand in early 2024.

Figure 4: Job Openings Mentioning Check Point in the Job Requirements (Source: Revealera.com)

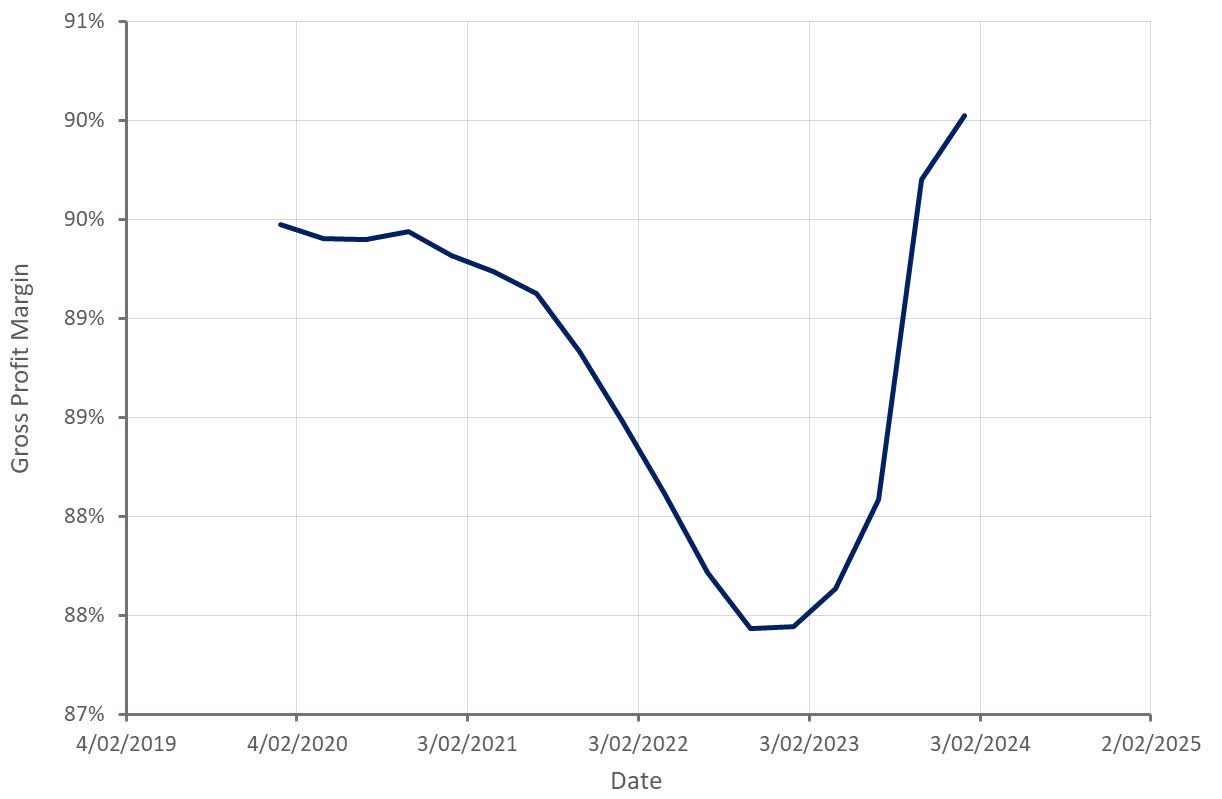

Check Point's gross profit margins have now fully recovered from pandemic-related supply chain issues. This is helping to support the company's bottom line, even as the burden of operating expenses continues to increase. Success in areas like SASE and security operations could weigh on gross profit margins in the future though.

Figure 5: Check Point Gross Profit Margin (Source: Created by author using data from Check Point)

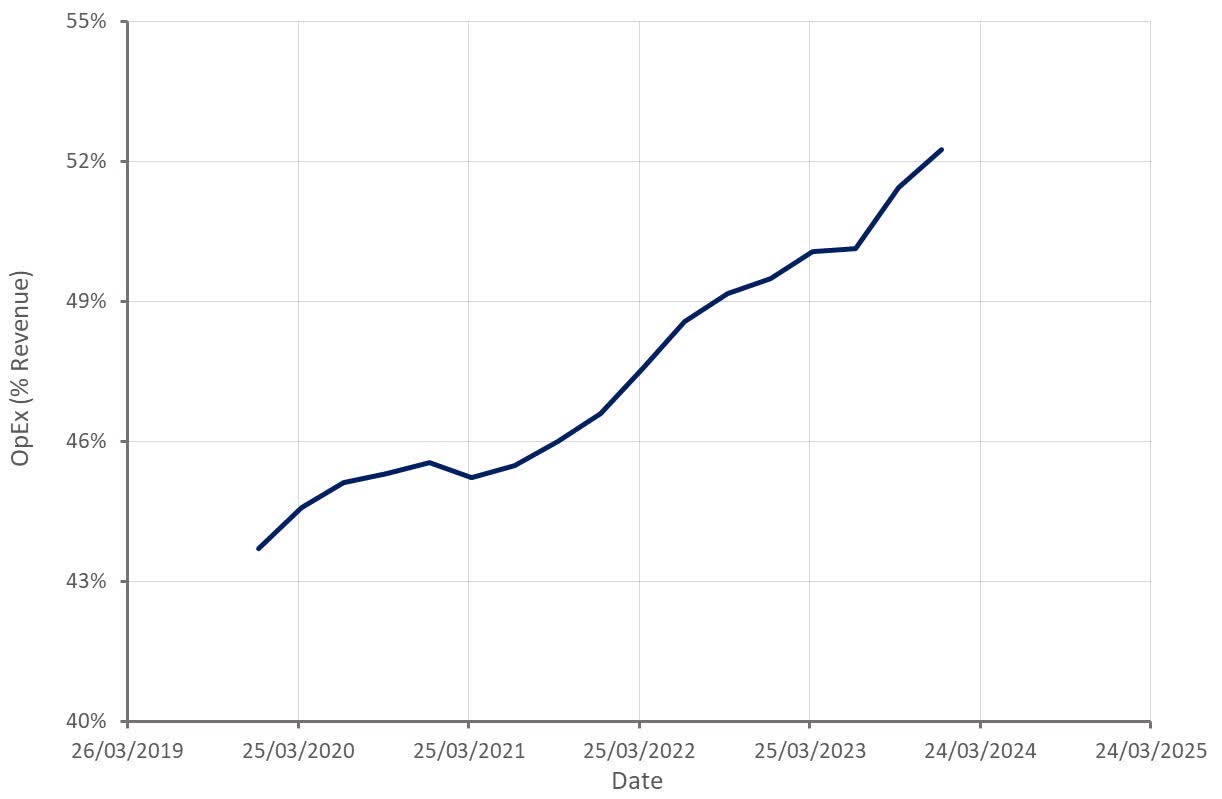

Check Point's operating expenses continue to rise, driven in large part by R&D expenses. This is not surprising given the soft demand environment and Check Point's attempts to modernize its product portfolio.

Figure 6: Check Point Operating Expenses (Source: Created by author using data from Check Point)

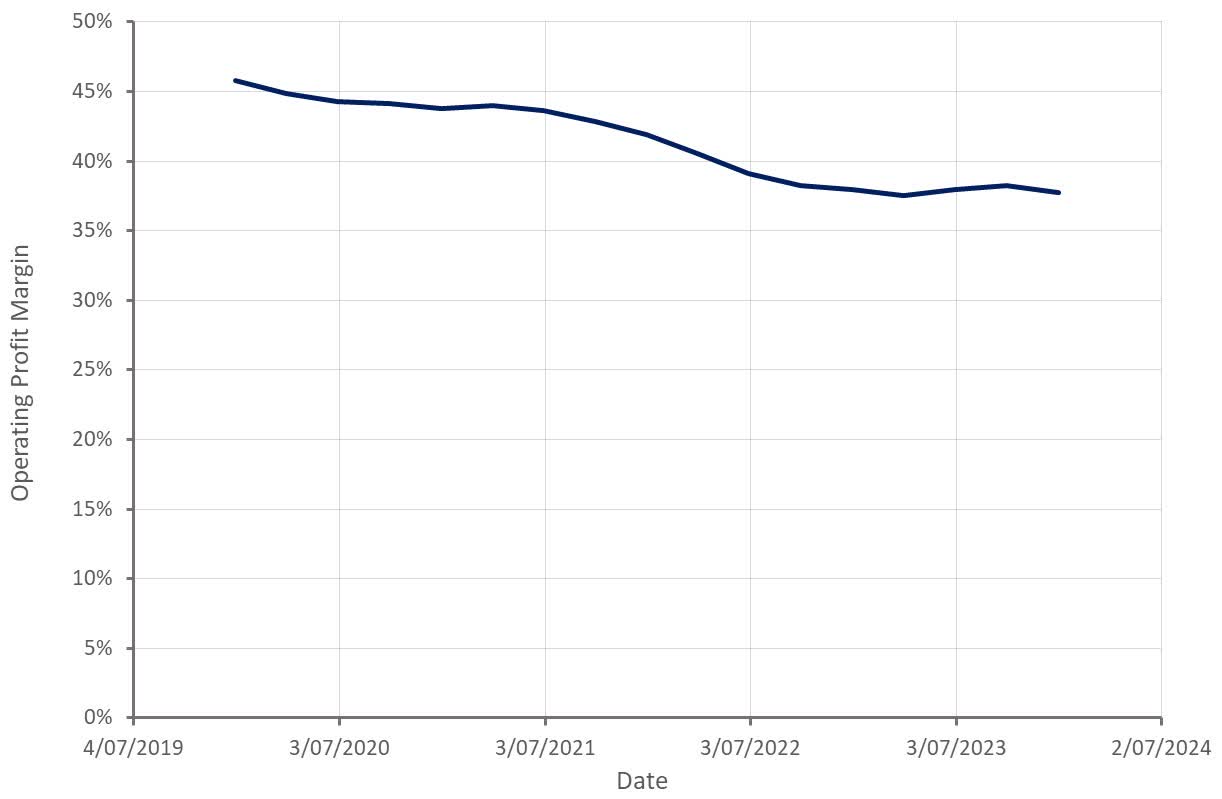

The net effect of fairly flat gross profit margins and rising operating expenses has been a substantial decline in operating profitability. While margins have stabilized somewhat over the past 12 months, I expect further downward pressure as Check Point's revenue shifts more towards SaaS-type products.

Figure 7: Check Point Operating Profit Margin (Source: Created by author using data from Check Point)

Check Point Software Technologies Ltd.'s valuation isn't particularly high for a profitable cyber security company, but this is not surprising given that Check Point failed to capitalize on the enormous growth opportunity of the last few years. While Check Point remains highly profitable and is still growing, it is having to work increasingly hard for this growth. The company's margins continue to compress, and acquisitions and new products are only providing a modest benefit so far.

Investors may be counting on a combination of share buybacks and continued growth to help drive Check Point's share price higher. I don't believe that the company's valuation is low enough to make this a compelling investment thesis though. Check Point doesn't pay a dividend, and buybacks are simply a way to return unneeded capital to shareholders.

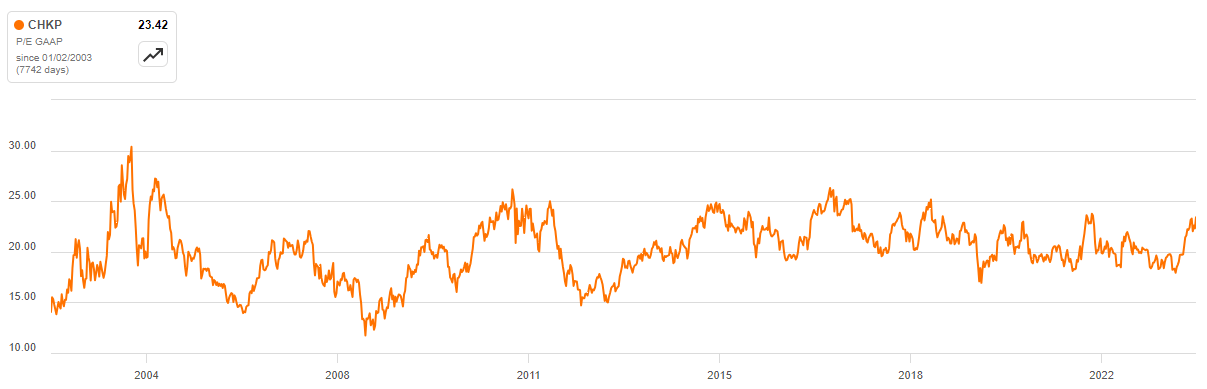

Figure 8: Check Point PE Ratio (Source: Seeking Alpha)