CloudVisual

CloudVisual

Note: I have previously covered Seanergy Maritime Holdings Corp. (NASDAQ:SHIP), so investors should view this as an update to my earlier articles on the company.

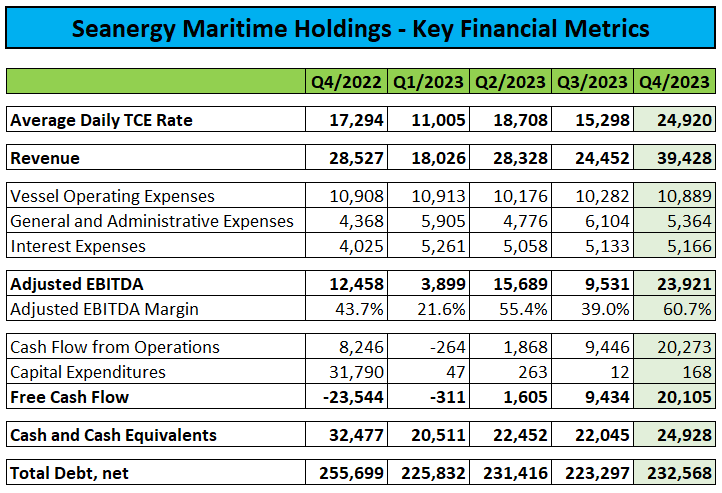

Last week, leading dry bulk shipper Seanergy Maritime Holdings ("Seanergy" or "Seanergy Maritime") reported decent fourth quarter results well above consensus expectations:

Company Press Releases / Regulatory Filings

Thanks to a vastly improved Capesize charter rate environment, the company was solidly profitable and generated more than $20 million in free cash flow, which was partially utilized to repurchase the remaining $3.2 million in outstanding convertible notes.

Company Presentation

Seanergy also made $9.4 million in regular debt amortization payments and a second $3.5 million down payment upon the recent delivery of a chartered-in Newcastlemax carrier which the company intends to acquire later this year against a final payment of $20.9 million.

In addition, Seanergy Maritime declared a regular quarterly cash dividend of $0.025 as well as a special cash dividend of $0.075 per common share to all shareholders of record as of March 25 which is expected to be paid on April 10.

The company finished the year with $24.9 million in cash and cash equivalents and $235.5 million in debt.

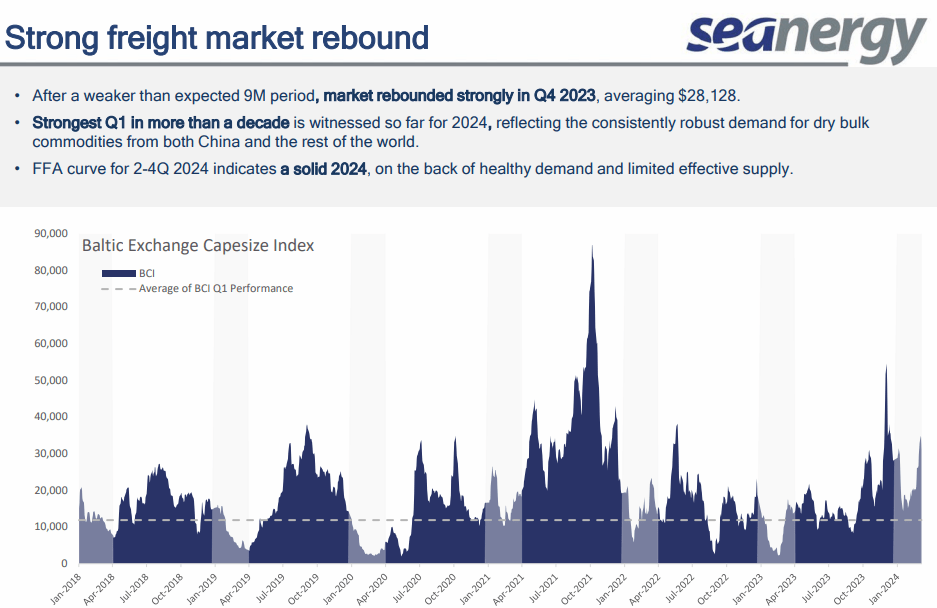

With the Capesize market currently undergoing the strongest first quarter since 2011, Seanergy is going to report another solid financial performance (emphasis added by author):

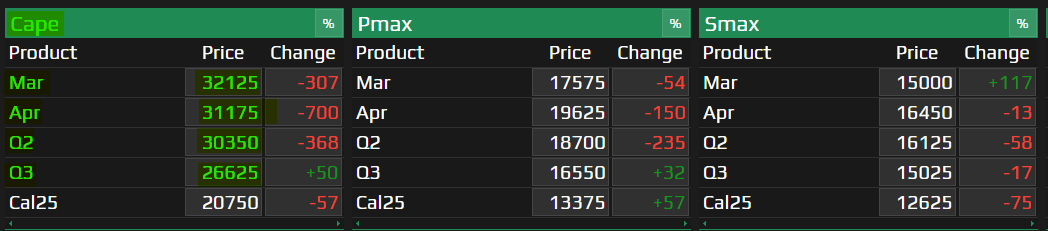

In terms of guidance for the first quarter of 2024, assuming that the remaining days of March are consistent with current FFA levels, we expect our daily TCE to be equal to about $23,219.

Additionally, we have taken advantage of the recent upswing in freight futures levels by converting about half of our second-quarter ownership days at a fixed gross rate of approximately $28,300 in order to secure additional strong cash-flow for the Company.

Without the unfortunate decision to fix five vessels for Q1 at an average daily time charter equivalent ("TCE") rate just $18,683, the company's first quarter TCE rate would have been even higher.

At these charter rate levels, I would expect the company to generate at least $20 million in Adjusted EBITDA for Q1 and approximately $15 million in free cash flow of which some has already been used to make an advance payment related to the recent $33.7 million acquisition of a 2013 Japan-built Capesize carrier which will be renamed Iconship with delivery expected in the second quarter.

On February 5, 2024, the Company agreed to acquire the 181,392 dwt Capesize bulk carrier, built in 2013 in Japan, which will be renamed M/V Iconship. The purchase price of $33.7 million is expected to be funded through a combination of cash on hand and debt financing. The M/V Iconship is expected to be delivered to the Company between April to June 2024.

Kudos to management for the decent timing of recent fleet additions as second hand vessel values have appreciated quite meaningfully over the past month.

During the questions-and-answers session of the conference call, management emphasized the company's focus on returning capital to shareholders:

Well, for us, it's very important to reward our shareholders, and we have demonstrated historically that we've paid hefty dividends to our shareholders to the extent that, cash flow and cash balances allows. (...)

However, as we've stated in our release, we have already fixed the number of our vessels for Q1 and of course for Q2. So, we have crystallized a big amount of our cash flow.

And if the situation allows, we might incorporate the special dividend into the regular dividend or further increase the special dividend. We have not decided yet. We will wait and see. But the overall strategy is to reward the shareholders as much as we can.

However, I was perplexed by Seanergy Maritime's decision to utilize its recently announced $30 million "at-the-market” equity offering program ("ATM-Program") with a division of B. Riley Financial (RILY).

Since the beginning of the year, the company has issued and sold 288,874 common shares under the ATM Program well below estimated net asset value ("NAV") per share, resulting in gross proceeds of $2.3 million.

Company Press Release / Value Investor's Edge

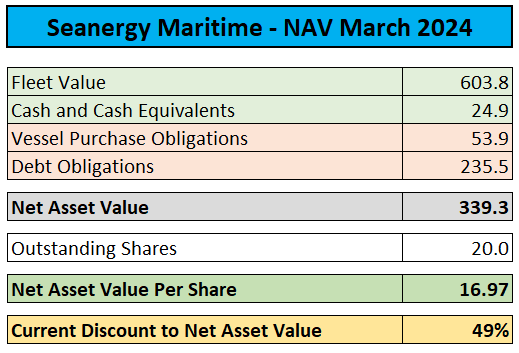

To be fair, soaring second hand vessel values have increased the company's NAV quite meaningfully in recent weeks but even my November 30 update on Seanergy shows an estimated NAV of close to $12 per share.

Rather than selling new shares into the open market at a large discount to net asset value, the company should actually consider buying back more shares under its existing $25 million repurchase program but management might be looking to increase the company's liquidity buffer ahead of the expected Iconship delivery in Q2.

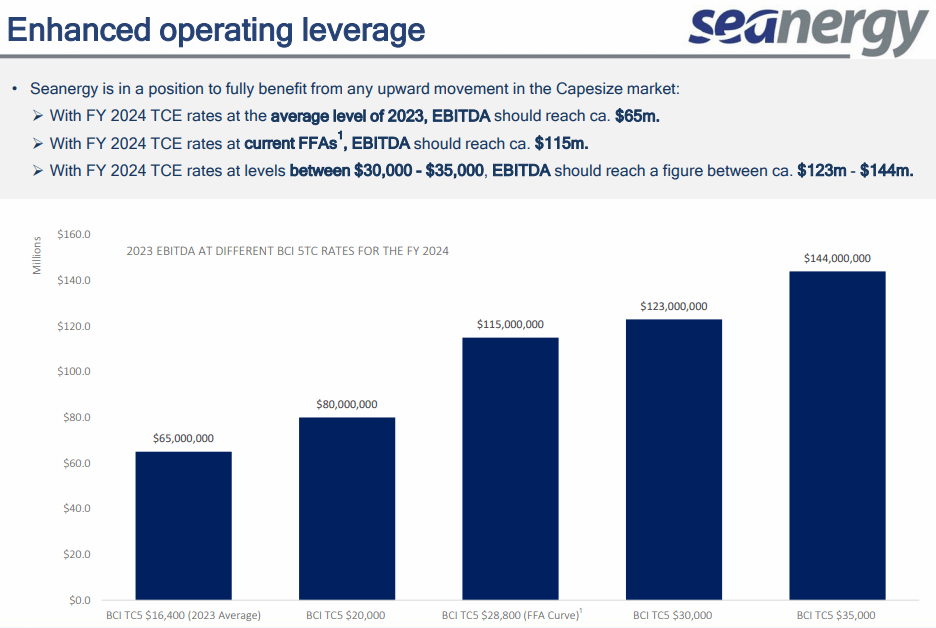

While I view the precipitant fixture of five vessels for Q1 at less-than-stellar rates and particularly the surprise decision to sell new shares into the open market as negative, these issues should not distract investors from the bigger picture, as the Capesize market is widely expected to remain strong for the balance of the year:

Company Presentation

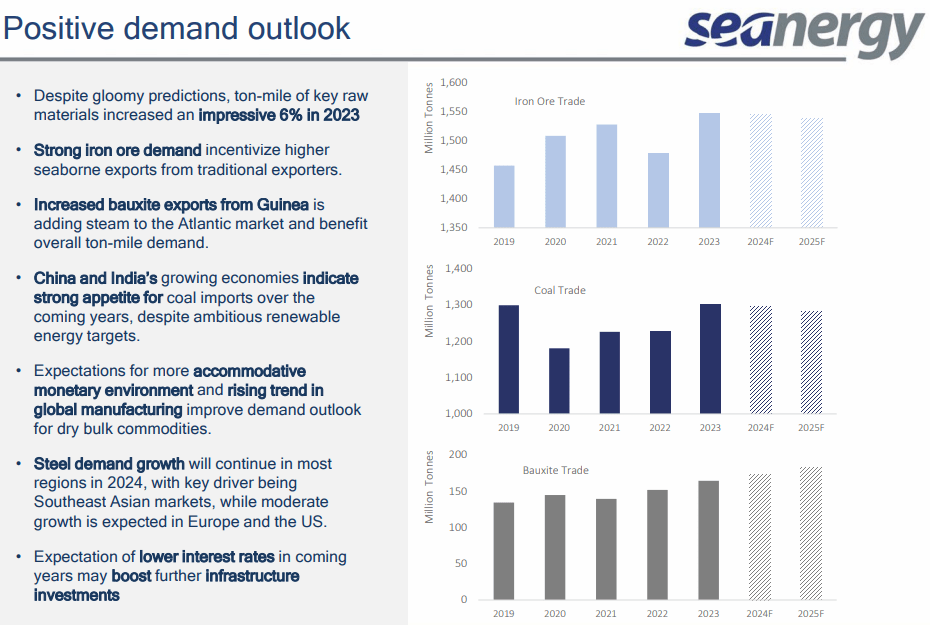

With strong Chinese demand for key commodities like iron ore, bauxite and coal expected to continue and vessel supply limited by a record low orderbook, slow-steaming and ongoing disruptions in the Red Sea and the Panama Canal, current forward freight agreement ("FFA") rates indicate a year of strong profitability and cash flow generation for dry bulk shippers:

Braemar Atlantic Securities

At current rates, Seanergy would generate well above $100 million in Adjusted EBITDA this year, approximately double the number achieved in 2023.

Company Presentation

Considering the amount of resulting cash flow generation, the company could easily afford a quarterly cash dividend of $0.25 per share (approximately $5 million).

However, given the requirement to pay for two vessel acquisitions later this year, I do not expect Seanergy to raise the quarterly distribution above $0.10 per share.

Assuming at least stable charter rates and second hand vessel values, I would expect the company's NAV to increase by more than 20% to approximately $20.50 by the end of this year.

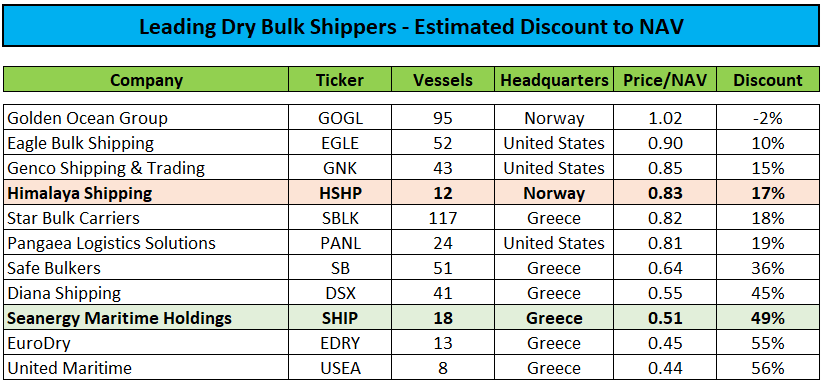

With the stock trading at just 51% of estimated net asset value, I am reiterating my "Buy" rating on the shares.

Please note that the company is one of just two U.S.-exchange listed Capesize/Newcastlemax pure plays with peer Himalaya Shipping (HSHP) currently valued at 83% of NAV:

Value Investor's Edge / Author's Calculations

Last but not least, Greek shipping magnate George Economou recently accumulated a 9.5% stake in the company and is currently challenging CEO Stamatis Tsantanis' supervoting rights in court thus adding some spice to the story.

Seanergy Maritime Holdings delivered decent fourth quarter results with solid profitability and very strong cash generation.

In addition, management provided a constructive outlook for the balance of the year due to a combination of strong commodity demand out of Asia and limited vessel supply.

While the company's decision to sell new shares into the open market well below net asset value is disappointing, impact on the big picture remains limited.

Considering the strong outlook for the Capesize market and the company's still heavily discounted valuation, I am reiterating my "Buy" rating on the shares.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.