ThitareeSarmkasat

ThitareeSarmkasat

Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferred stock and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as the top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the first week of March.

Be sure to check out our other weekly updates covering the business development company ("BDC") as well as the closed-end fund ("CEF") markets for perspectives across the broader income space.

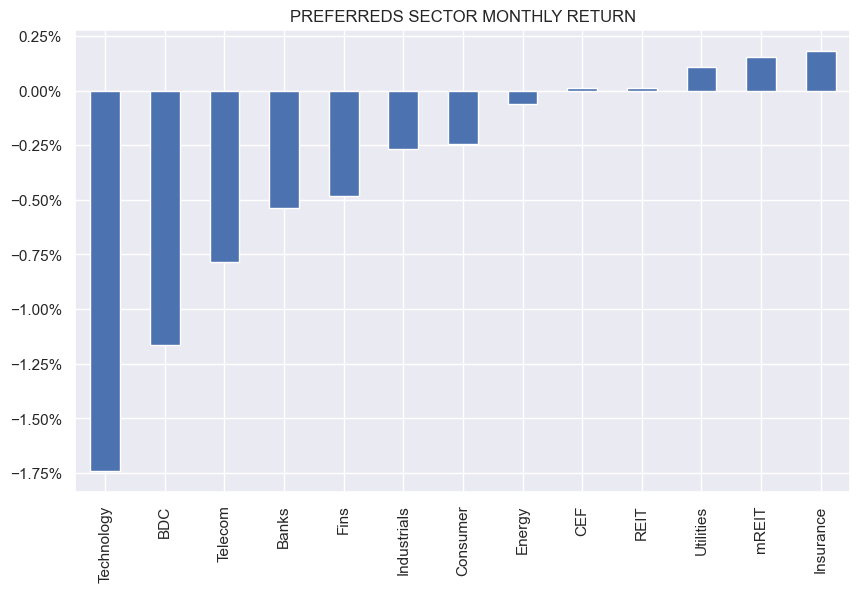

Preferreds were slightly lower this week and over February. The Banks sector remained broadly unfazed by the NYCB dumpster fire, which reignited once again this week.

Systematic Income

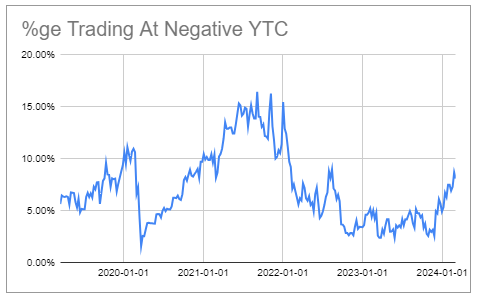

The rally over the last few months has pushed an increasing number of preferreds into negative yield-to-call territory, requiring some caution on the part of investors holding stocks trading above "par". The eventual yield of these stocks could easily be below their stripped or headline yield in case of a redemption.

Systematic Income

Many students of financial markets are familiar with the CAPM model which posits a tight relationship between beta and return - the higher the beta of a security, the higher should be its return. In practice, however, there is no relationship between beta and returns and in some cases it actually goes the other way - a so-called "beta anomaly" that has been documented repeatedly.

In a CAPM world, there are two ways to generate higher returns - to use leverage or to hold higher-beta securities. However because many investors are leverage-constrained, holding higher-beta securities is their only option. This pushes up the valuation of higher-beta securities, making them overly expensive, which, naturally, depresses their longer-term returns and causes the "beta anomaly".

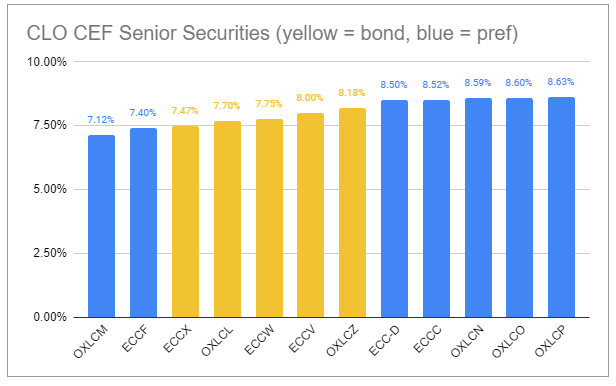

A similar dynamic exists in fixed-income. Specifically, it happens when securities lower in the capital structure trade at a yield that is not much higher than securities higher in the capital structure of the same issuer. We have often commented on this dynamic in the context of the CLO CEF sub-sector which has both bonds and preferreds.

We show this dynamic below across CLO CEF issuers with both bonds and preferreds such as ECC and OXLC. We see that not only are there preferreds with lower yields than bonds of the same issuer but that bond yields are not all that much lower than many of the preferreds.

Systematic Income

Clearly this is a qualitative description as a fair-value differential between bonds and preferreds would require making assumptions about likely loan defaults and CEF portfolio losses. However, for context, preferreds often get a rating a full grade lower (i.e. BB vs. BBB) relative to unsecured debt. In this context, bonds should trade at a spread of roughly 1.5% below that of the preferreds versus 0.4% on average now.

The intuition here seems to be that if investors like a given issuer, then it makes sense to go for their higher-yielding one, since all securities within the capital stack are money good. Although this does raise the question of why CLO CEF preferred investors are not instead in common shares, it does suggest why the yield differential between bonds and preferreds could be too tight.

The takeaway here is that bonds of the same issuer often offer more attractive risk-adjusted yield or risk/reward than the preferreds. More tactical investors can track the yield differential between the two types of securities (which often increases during market sell-offs and falls during rallies) to generate additional alpha by rotating between the two. This suggests sticking with bonds in the current environment of expensive credit valuations and rotate into preferreds when valuations readjust.

This week we added a couple of new senior securities to the respective Investor Tools. First up is the homebuilder Hovnanian preferred (HOVNP), rated CCC-, as well as a bond from mortgage REIT MITT (MITN) which also has 3 preferreds.

As far as the latter, in line with the discussion above, the differential between the bond and the preferreds yields looks fairly tight. For example, MITN trades at a 9.6% yield while 2 of the 3 MITT preferreds trade at a 10.5-6% yields which is roughly where the third preferred is expected to end up once short-term rates move to the medium-term consensus level. A roughly 10% relative yield pickup (9.5% to 10.6%) doesn’t feel like enough to go from a deeply subordinated preferred stock to senior unsecured.

True, in a worst-case scenario both types of securities are going to be goose-eggs, however in a more reasonable scenario the bonds should behave much better. MITT economic leverage is low at 1.5x and non-recourse leverage is very low, which puts the bonds in a decent place.

As suggested above, we see significant value in bonds in diversified income portfolios given the general compression of yields between securities across the capital structure as well as the ability of bonds to be more resilient during market sell-offs.

We currently hold bonds issued by various investment companies such as CEFs, BDCs and REITs with yields of 7-9%. These include the BDC WhiteHorse 2028 bond (WHFCL) at a 7.8% yield and a CEF OXLC 2031 bond (OXLCL) at a 7.7% yield.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.