Maksim Safaniuk

Maksim Safaniuk

Ovintiv Inc. (NYSE:OVV) finished 2023 strongly with 2H 2023 production around 8% above expectations. It appears to have provided relatively conservative guidance for 2024, with average oil and condensate production expected to decline 10% from 2H 2023 levels at the midpoint of its guidance. This is still 2% to 3% higher than its previous outlook for 2024 oil and condensate production, but it doesn't appear that Ovintiv is factoring in a large carryover into 2024 from its 2H 2023 production momentum.

Despite its strong recent production, I have downgraded Ovintiv to neutral now. Ovintiv's share price has gone up 7% since I looked at it in September 2023, while the weaker commodity prices (particularly for natural gas) means that its projected 2024 free cash flow has gone down several hundred million even if it hits the high end of its 2024 production guidance.

I now estimate Ovintiv's value at $50 to $51 per share at long-term (after 2024) $75 WTI oil and $3.75 NYMEX gas, which is pretty close to its current share price.

Ovintiv expects to average (at guidance midpoint) approximately 560,000 BOEPD in 2024 production, with 205,000 barrels per day of oil and condensate production. This is a significant -5% decrease in total production and -10% decrease in oil and condensate production compared to Ovintiv's 2H 2023 production levels.

However, Ovintiv's 2H 2023 production was also much better than expected (around 8% higher than expectations from July 2023) so Ovintiv may be being relatively conservative with its 2024 guidance and only factoring in a relatively modest amount of carryover in outperformance from 2H 2023. Ovintiv did boost its oil and condensate production expectations by 5,000 barrels per day compared to its preliminary outlook for 2024.

Ovintiv expects to achieve its 2024 production targets with approximately $2.3 billion in capital expenditures, reduced by approximately 16% from 2023 levels.

I am currently modeling Ovintiv's 2024 results based on the midpoint of its guidance, although as noted above, its recent production performance has been very strong compared to guidance.

At 560,000 BOEPD in 2024 production, including 205,000 barrels per day in oil and condensate production, Ovintiv is projected to generate $7.839 billion in revenues after hedges.

Ovintiv's Hedges (ovintiv.com (Q4 2023 Earnings Presentation))

This includes $201 million in positive hedge value and is also based on current strip prices of roughly $79 WTI oil and $2.35 NYMEX gas. Ovintiv has close to 50% of its 2024 natural gas production hedged, with those hedges having a neutral value at $3.50 gas.

| Type | Barrels/Mcf | $ Per Barrel/Mcf (Realized) | $ Million |

| Oil & Condensate | 74,825,000 | $76.75 | $5,743 |

| NGLs | 31,937,500 | $20.00 | $639 |

| Natural Gas | 584,000,000 | $2.15 | $1,256 |

| Hedge Value | $201 | ||

| Total Revenue | $7,839 |

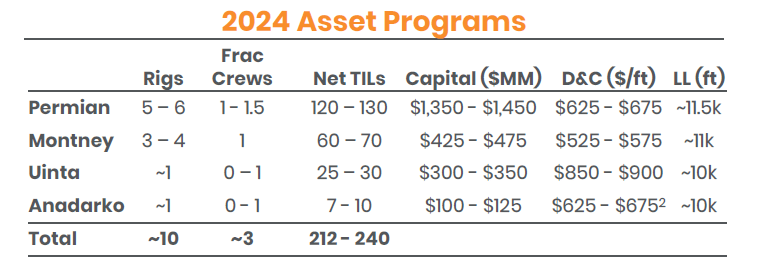

Ovintiv is devoting approximately 60% of its 2024 capex budget to its Permian assets, with another 20% going towards its Montney assets. Roughly 15% of its capex budget is for its Uinta assets and the remaining 5% is for its Anadarko assets.

Ovintiv's Capital Allocation (ovintiv.com (Q4 2023 Earnings Presentation))

Ovintiv is now projected to generate roughly $1.796 billion in 2024 free cash flow at current strip prices. This is based on the midpoint of its production guidance.

If Ovintiv ends up around delivering the high end of its full year production guidance instead, it would end up with approximately $1.9 billion in 2024 free cash flow.

| $ Million | |

| Production, Mineral and Other Taxes | $344 |

| Transportation and Processing | $1,584 |

| Operating Expenses | $920 |

| Net G&A And Market Optimization | $275 |

| Cash Interest | $420 |

| Cash Taxes | $200 |

| Capital Expenditures | $2,300 |

| Total Expenses | $6,043 |

Ovintiv's base quarterly dividend is $0.30 per share, which adds up to $323 million in annual dividend payments based on its 269.5 million outstanding shares as of February 16, 2024.

Ovintiv plans to split its remaining free cash flow equally between debt reduction (and bolt-on acquisitions) and share repurchases (plus variable dividends).

This would leave roughly $737 million (based on guidance midpoint production) that can be allocated towards debt reduction and bolt-on acquisitions and another $737 million that can be allocated towards share repurchases and variable dividends. Ovintiv has been choosing to focus on share repurchases between those latter two options.

Ovintiv is now projected to end up with around 260 million outstanding shares at the end of 2024 if it puts $737 million towards share repurchases. This factors in the expected share-based compensation during 2024 as well.

Ovintiv ended 2023 with $5.757 billion in net debt and thus would end 2024 with approximately $5.02 billion in net debt if it puts $737 million towards debt reduction during 2024. This doesn't include acquisitions though and Ovintiv has spent around $190 million on Permian acquisitions so far in 2024. This would put its year-end 2024 net debt at around $5.21 billion before further acquisitions.

I've adjusted my estimate of Ovintiv's value to around $50 to $51 per share at long-term (after 2024) prices of $75 WTI oil and $3.75 NYMEX gas. This also is based on production levels around the high end of its 2024 guidance.

Ovintiv's value has gone down a bit since I looked at it last September due to lowered 2024 free cash flow expectations. Natural gas accounts for around 48% of Ovintiv's total production, and Ovintiv's expected 2024 natural gas revenues have been reduced by around $600 million. This is partially offset by Ovintiv's hedges, but there is still a negative impact on Ovintiv's free cash flow of several hundred million dollars from the lowered prices.

Ovintiv ended up with excellent 2H 2023 production, although its guidance for 2024 has been more conservative. At the current strip, I project Ovintiv to generate approximately $1.8 billion in free cash flow at the midpoint of its production guidance, and around $1.9 billion in free cash flow at the high end of its production guidance.

I believe there is a good chance that Ovintiv can reach the high end of its 2024 production guidance, but that would still leave it with around $300 million lower free cash flow than I had projected for it in September 2023 (when 2024 natural gas prices were approximately $1 higher).

I now estimate Ovintiv's value to be $50 to $51 per share at long-term $75 WTI oil and $3.75 NYMEX gas.