Art Wager

Art Wager

Hoya Capital

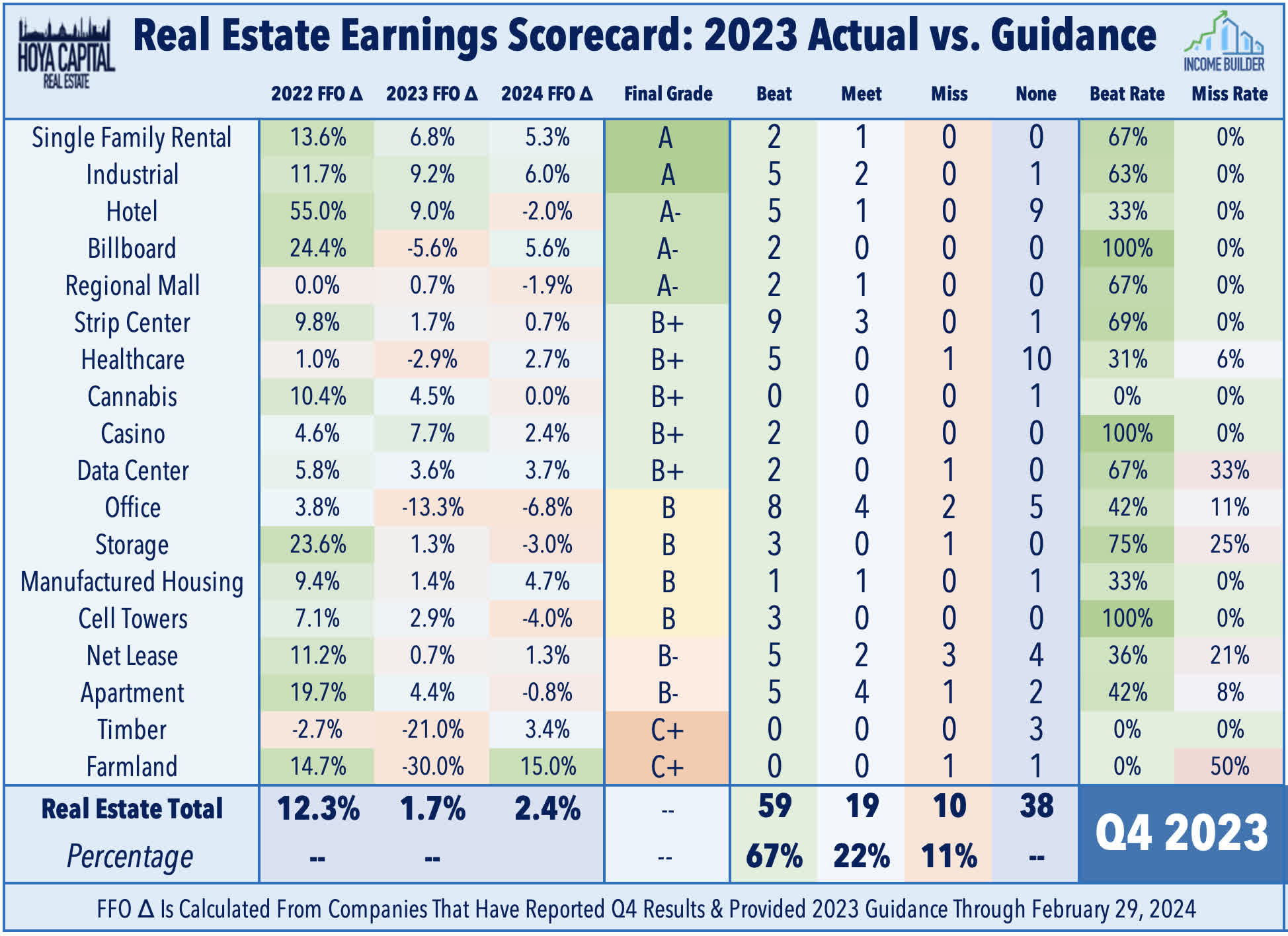

Over 200 U.S. REITs and homebuilders have reported fourth-quarter earnings results over the past six weeks, providing critical information on the state of the commercial and residential real estate industry. Beneath the reignited interest rate headwinds that have pressured the sector, REITs delivered one of their strongest earnings seasons since early in the pandemic recovery, and the back-half of the earnings season was actually a bit stronger than the first-half. Of the 88 equity REITs that provide full-year Funds From Operations ("FFO") guidance, 59 REITs (67%) beat the midpoint of their forecast, 19 REITs (22%) matched, while just 11 REITs (10%) missed estimates. This 67% FFO "beat rate" finished ahead of the historical REIT sector average in Q4 of roughly 65%, and ahead of the 55% "beat rate" in Q4 of 2022. Consistent with the "Tale of Two Economies" trends that we've discussed, upside surprises this earnings season came largely from the service-oriented pro-cyclical property sectors - retail, hotel, and specialty REITs - and from the still-supply-constrained single-family housing and logistics markets.

Hoya Capital

Pockets of weakness were seen in the interest-rate-sensitive property sectors - net lease and office - along with goods-oriented sectors - farmland, timber, and cold storage. "Rates Up, REITs Down" remained the overriding driver of REIT stock-price performance throughout earnings season, however, as the benchmark 10-Year Treasury Yield retraced about half of its late-2023 decline through the first two months of 2024 on the heels of several strong employment reports and lukewarm inflation data. At the start of earnings season in mid-January, markets were pricing in the first Federal Reserve rate cut in March, with six total rate cuts expected in 2024. At the end of earnings seasons, markets see just three rate cuts this year, with the first cut not expected until June. These relatively buoyant economic conditions have been most consistent with the so-called "No Landing" scenario of 2-4% inflation and economic growth - an outcome that is certainly better than the "Hard Landing" recession scenario, but clearly not as favorable as the ideal "Soft Landing" scenario of 0-2% inflation and economic growth.

Hoya Capital

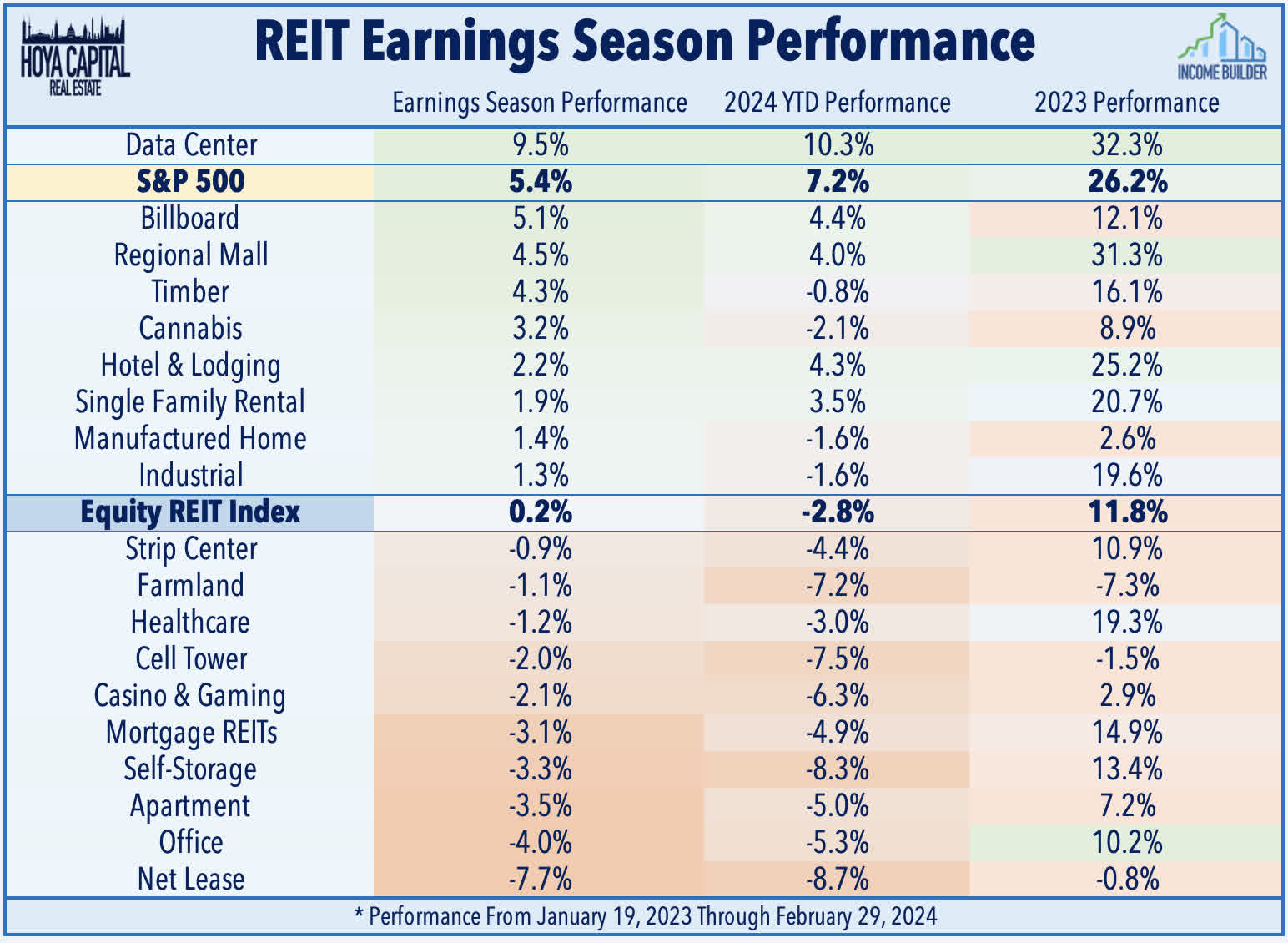

Real estate equities - the sector with perhaps the most to gain from a moderation in inflation and normalization in Fed monetary policy - had entered earnings season with wind in their sails after a rather dismal eighteen-month-long stretch where any sense of forward headway seemed illusive. That sense of stagnation returned over the past six weeks as, despite the relatively strong slate of earnings reports, the Equity REIT Index (VNQ) has gone nowhere this earnings season, underperforming the 5% gains from the S&P 500 (SPY). Fittingly in the "AI-generated" earnings season in which technology stocks have bifurcated from the rest of the market, the lone property sector that has outperformed the broader equity benchmark this earnings season - Data Center REITs - is the physical hub of Artificial Intelligence computing, and has jumped nearly 10% despite an earnings slate that, on a fundamental basis, was otherwise in the bottom-half of the REIT sector this earnings season. Net lease REITs - the most "bond-like" property sector - were the downside laggards.

Hoya Capital

At the property level, we've seen a supply-induced moderation in pricing power across some segments of the REIT sector - notably apartments, self-storage, and office - while other consumer-focused segments reported relatively resilient pricing power trends - notably retail and logistics. An easing of expense pressures - especially on the labor front - helped to drive strong performance in the senior housing and hotel sectors, and helped to ease some rent collection issues for skilled nursing and hospital REITs. Results from office REITs were surprisingly decent relative to the dire narrative, but a modest rebound in leasing activity might not be enough to change the trajectory after a dismal year of double-digit FFO declines and lingering interest rate headwinds. We saw mixed results from residential REITs, with a sharp cooldown in rent growth on the multifamily side, but stronger trends on the single-family side. There were no real "bombshells" this earnings season, and the handful of downside surprises were driven almost exclusively by elevated debt servicing expenses, underscoring the continued challenges facing more highly leveraged real estate portfolios from the higher rate environment.

Hoya Capital

With real estate earnings season now essentially complete - sans a handful of stragglers that report results over the next week - we compiled the critical metrics across each real estate property sector, which we've split into a two-part report: Winners of REIT Earnings Season & Losers of Earnings Season.

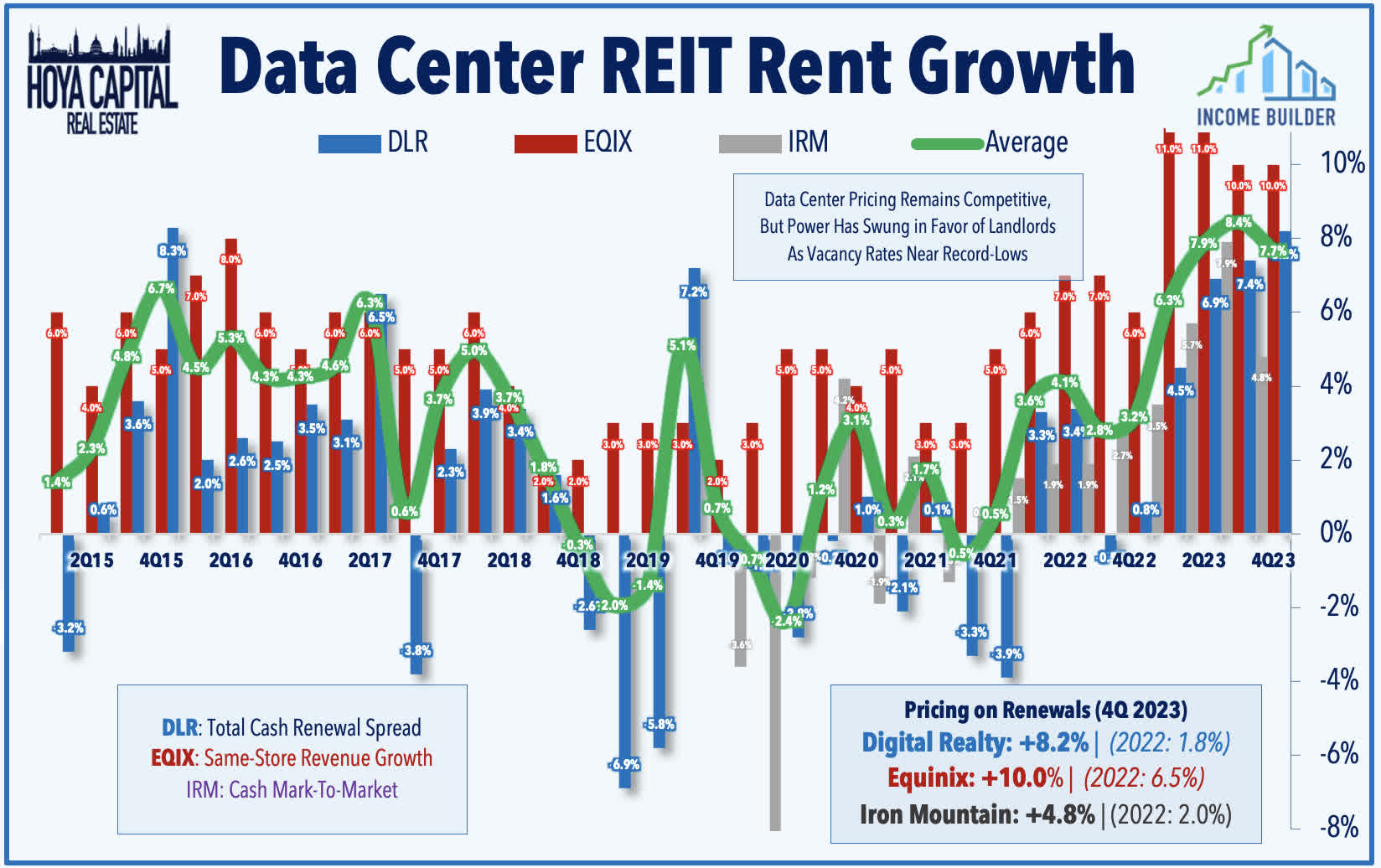

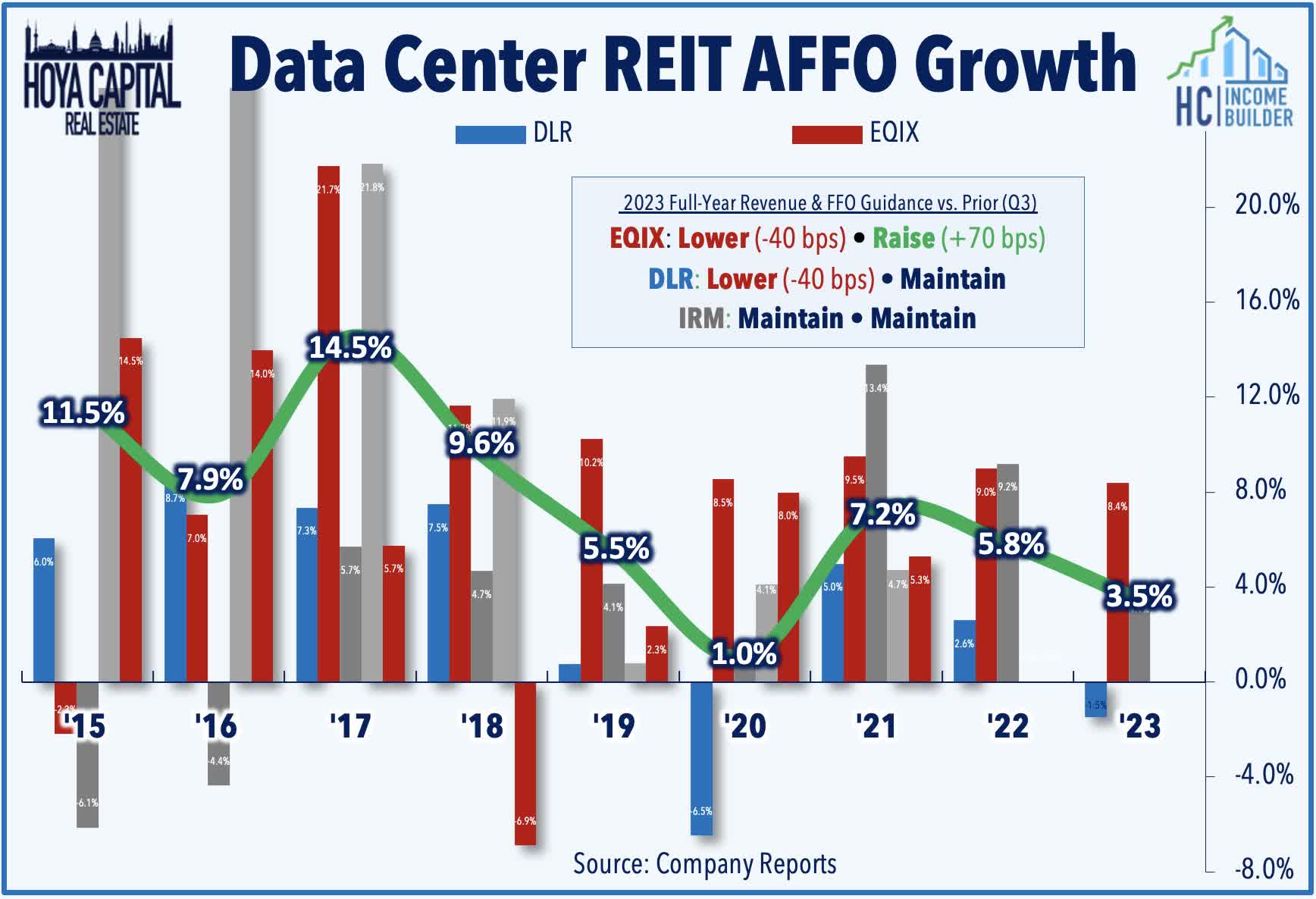

Data Center: Fittingly in the "AI-generated" earnings season in which technology stocks bifurcated from the rest of the market, Data Center REITs - the physical hub of Artificial Intelligence - delivered the strongest returns despite a mixed slate of results. Pricing power remained the upside highlight for data center REITs as incremental AI-related demand has clashed with a confluence of development bottlenecks - power shortages, higher cost of capital, supply chain constraints, ecopolitics, and NIMBYism - to create a more favorable dynamic and swung the pendulum of pricing power towards existing property owners. Equinix (EQIX) was the clear upside standout after reporting very strong results, citing "accelerating AI demand, robust pricing dynamics, and continued momentum" across its data center and digital services portfolios. EQIX reported full-year FFO growth of 8.7% in 2023 - above its prior guidance of 8.4% - and expects growth to accelerate to 8.8% in 2024. Pricing power remained impressive, with EQIX recording same-store revenue growth of 10.0% - its fourth-straight quarter of double-digit revenue growth.

Hoya Capital

Obscured a bit by the AI-driven optimism, results from the other major data center REIT - Digital Realty (DLR) - were less impressive. DLR reported that its full-year FFO declined -1.6% in 2023 as otherwise impressive revenue growth of 17% and record-high "same capital" NOI growth of 7.5% was fully negated by a combination of higher interest expense and deleveraging through asset sales and stock issuance. Disappointingly, the outlook for 2024 calls for FFO growth of just 1.3% as further deleveraging activities are expected to again offset an otherwise very strong year of property-level performance. Outside of the disappointing corporate-level FFO figures, property-level performance did remain impressive in Q4, highlighted by renewal spreads of 8.2% - the strongest since 2015. Iron Mountain (IRM) - which has grown its data center business into a viable player by cross-selling to its existing business storage customers - has been among the top-performers this after reporting solid full-year FFO growth of 4% in 2023 and providing an upbeat outlook for 2024 with expectations of 8% FFO growth. Data center leasing activity was disappointing in Q4 with just 4MW of activity, however, and is expected to decline 25% in 2024 at the midpoint of its initial outlook.

Hoya Capital

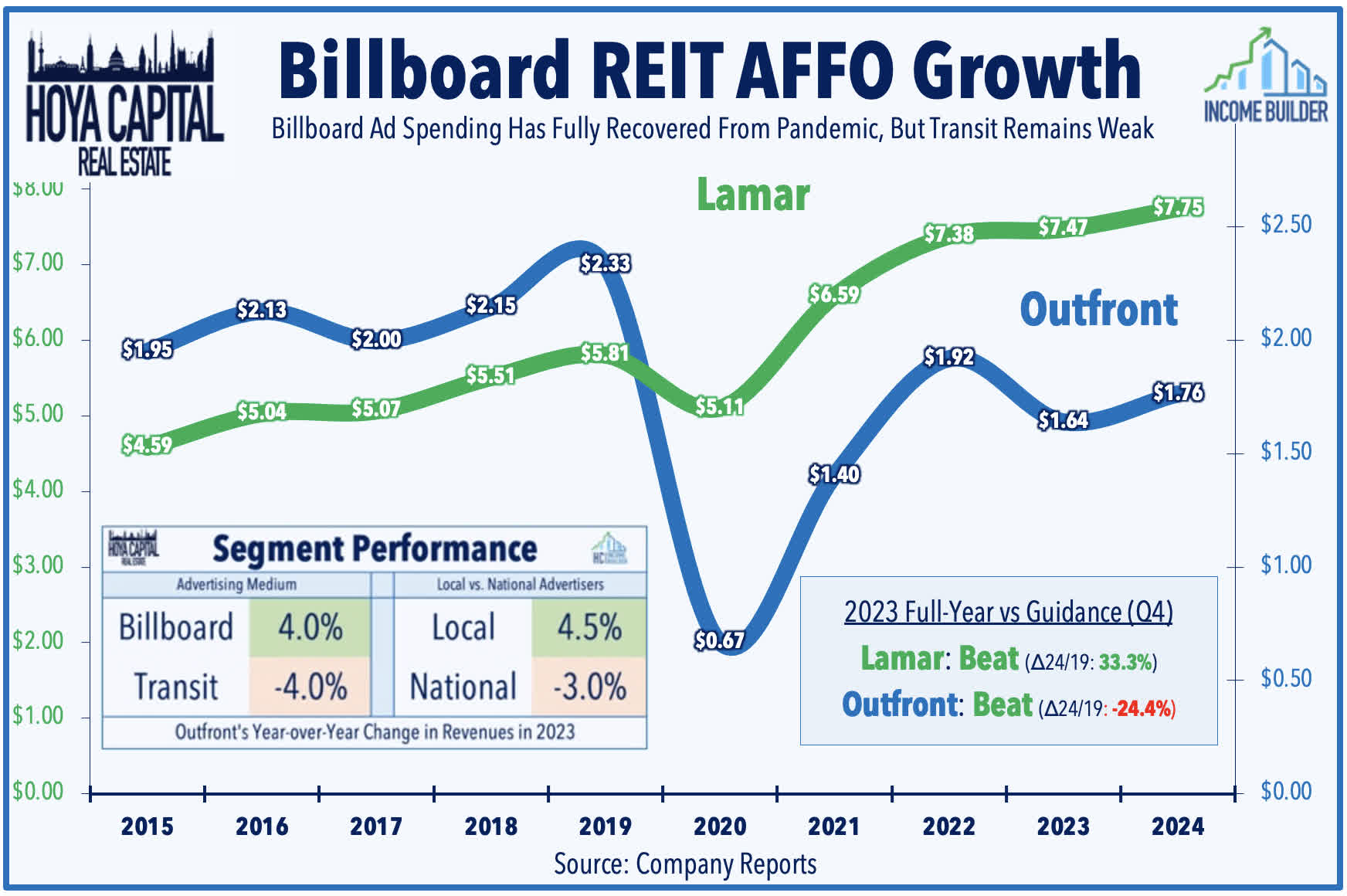

Billboard: (Final Grade: B+) The single most economically sensitive property sector, billboard REITs have been beneficiaries of the so-called "No Landing" scenario of 3-4% inflation and economic growth. Both billboard REITs posted strong gains this earnings season after results showed healthy "Out of Home" advertising spending trends in late 2023 and into early 2024, particularly among regional and local businesses. Outfront Media (OUT) - which endured a punishing sell-off of 70% between mid-2022 and late 2023 - soared after reporting continued strength from its core billboard segment, which offset lingering headwinds on its pandemic-disrupted transit segment and concerns about its debt-heavy balance sheet. Billboard revenues rose 4% for the year, "driven by higher rates resulting from robust demand," while revenues in its transit segment - which includes its MTA franchise - remain 35% below 2019 levels. Solid property-level fundamentals helped to partially offset a surge in interest expense, as OUT recorded a -14.5% dip in its full-year FFO in 2023, but sees a return to growth in 2024, projecting FFO growth in the "high single-digits." Lamar (LAMR) - which has benefited from its limited transit exposure and its stronger balance sheet - reported similarly solid results, recording full-year FFO growth of 1.2% in 2023 and projecting growth of 3.7% in 2024, which would be an impressive 33% above its 2019-level. Both REITs reported stronger local-based advertising spending, which grew roughly 4% year-over-year, while national brand spending declined by 3%.

Hoya Capital

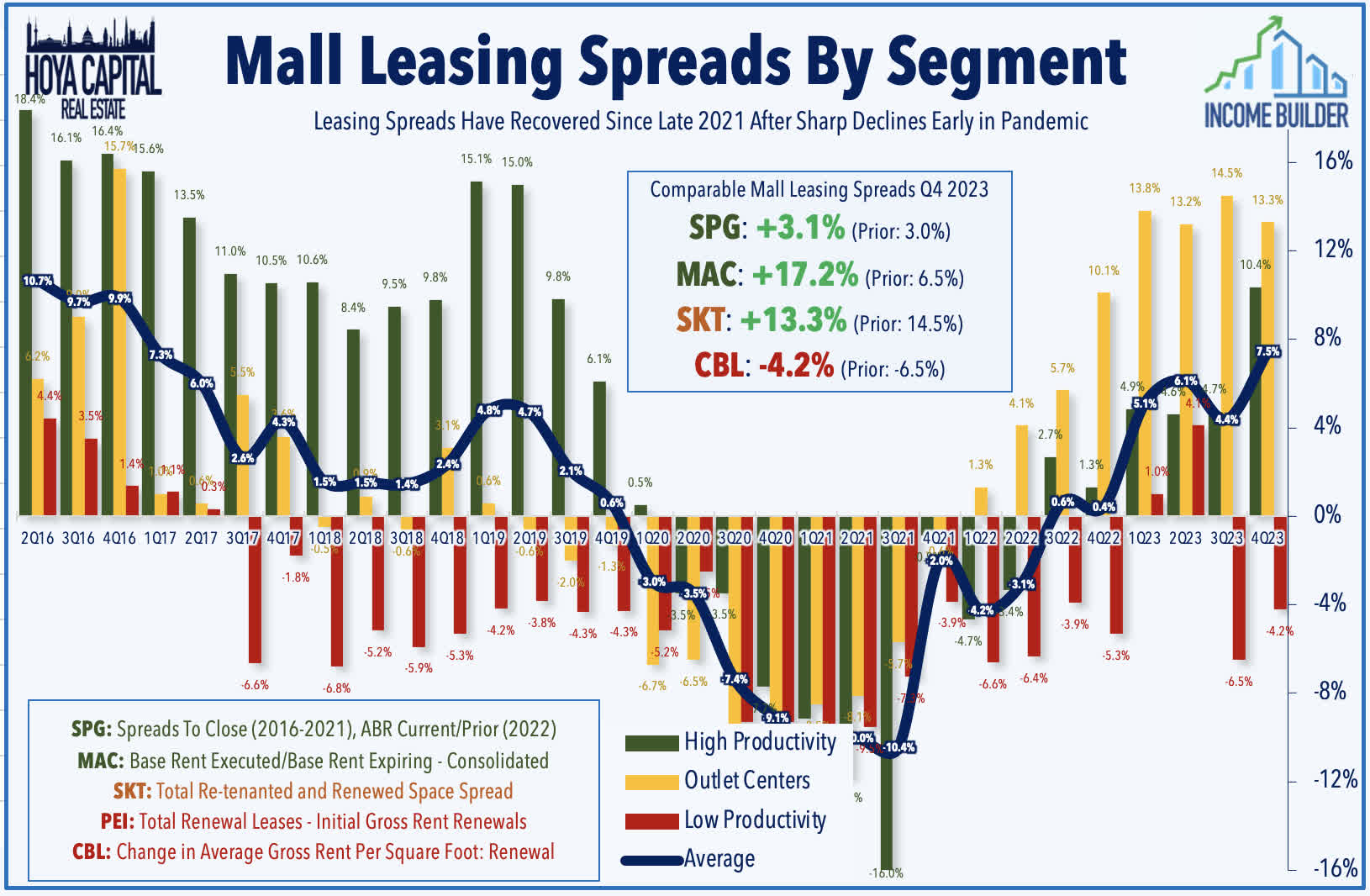

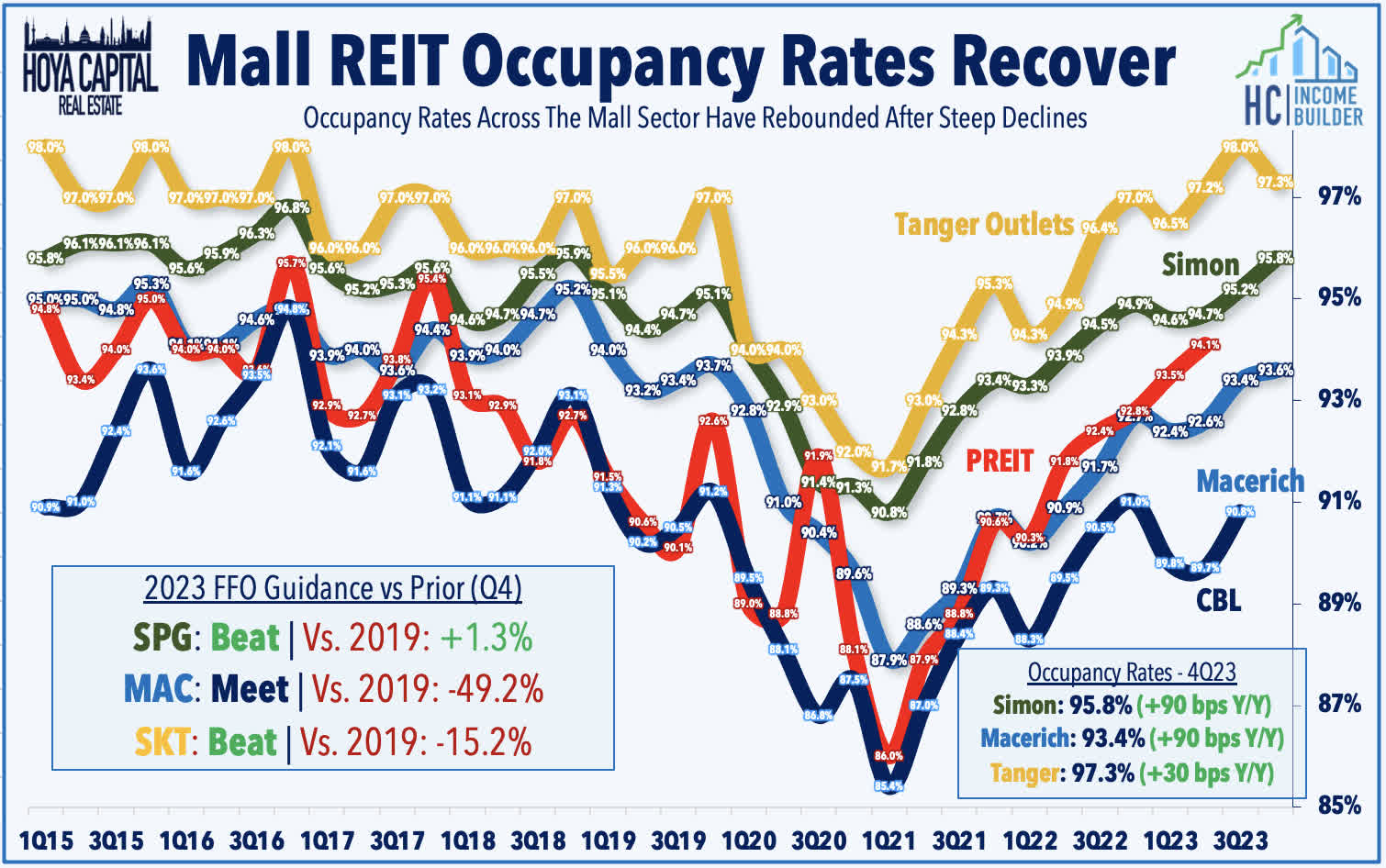

Malls: (Final Grade: A-) The retail apocalypse is officially over. As with the strip center peers, results from mall REITs showed that retail real estate fundamentals are as solid as they've been in at least a decade. Simon Property (SPG) reported solid results alongside another 3% dividend hike - its ninth since early 2021 - and a $2B stock buyback program. SPG reported that its full-year FFO rose 5.4% in 2023 - topping its pre-pandemic FFO - including the effects of gains from the partial sale of its interest in ABG. Occupancy increased to 95.8% - up 90 basis points from last year - to the highest level since Q4 2018. SPG's guidance for 2024 calls for FFO growth of roughly 1% after adjusting for investment gains, with higher interest expense offsetting solid NOI growth of "at least 3%." Average base rent shows a positive inflection in recent quarters, rising 3.1% year-over-year, and while SPG no longer discloses leasing spreads, it noted that it is "signing new leases at $74/foot and renewals at $65/foot," implying leasing spreads in the 20% range. Macerich (MAC) reported that its occupancy climbed to 93.4% at the end of 2023, up 90 basis points from last year to the highest level since Q1 2019. Leasing volumes and pricing were similarly impressive, with MAC signing 4.2 million SF of space during the year - its highest since the firm went public in 1994 - at rents that were 17.2% higher than a year earlier. Notably, MAC sees a return to growth for the first time in eight years, expecting full-year FFO growth of 0.6% and NOI growth of 2.75%.

Hoya Capital

Elsewhere, Tanger (SKT) has also rallied after it reported strong results highlighted by double-digit leasing spreads and provided an upbeat outlook for 2024. Tanger recorded full-year FFO growth of 7.0% in 2023 - well above its prior guidance of 4.9% - and expects growth of another 5.1% at the midpoint of its initial range. Positively, blended leasing spreads jumped 13.3% in Q4 - its eighth-straight month of positive spreads following a rough stretch of rent declines in 11 straight quarters from mid-2019 through late 2021. Leasing volumes were also impressive throughout 2023, with SKT signing over 2.3M SF of leases during the year - a record for the company - which lifted its occupancy rate to 97.3% - higher by 30 basis points from a year earlier to levels that are above the pre-pandemic 2015-2019 average of 96.5%. There were some reasons for caution, however, as the company noted that it has renewed only 24% of the space set to expire this year - down from 41% at this time last year - and stated that it "expects a higher re-tenanting rate in 2024 as it focuses on portfolio enhancement."

Hoya Capital

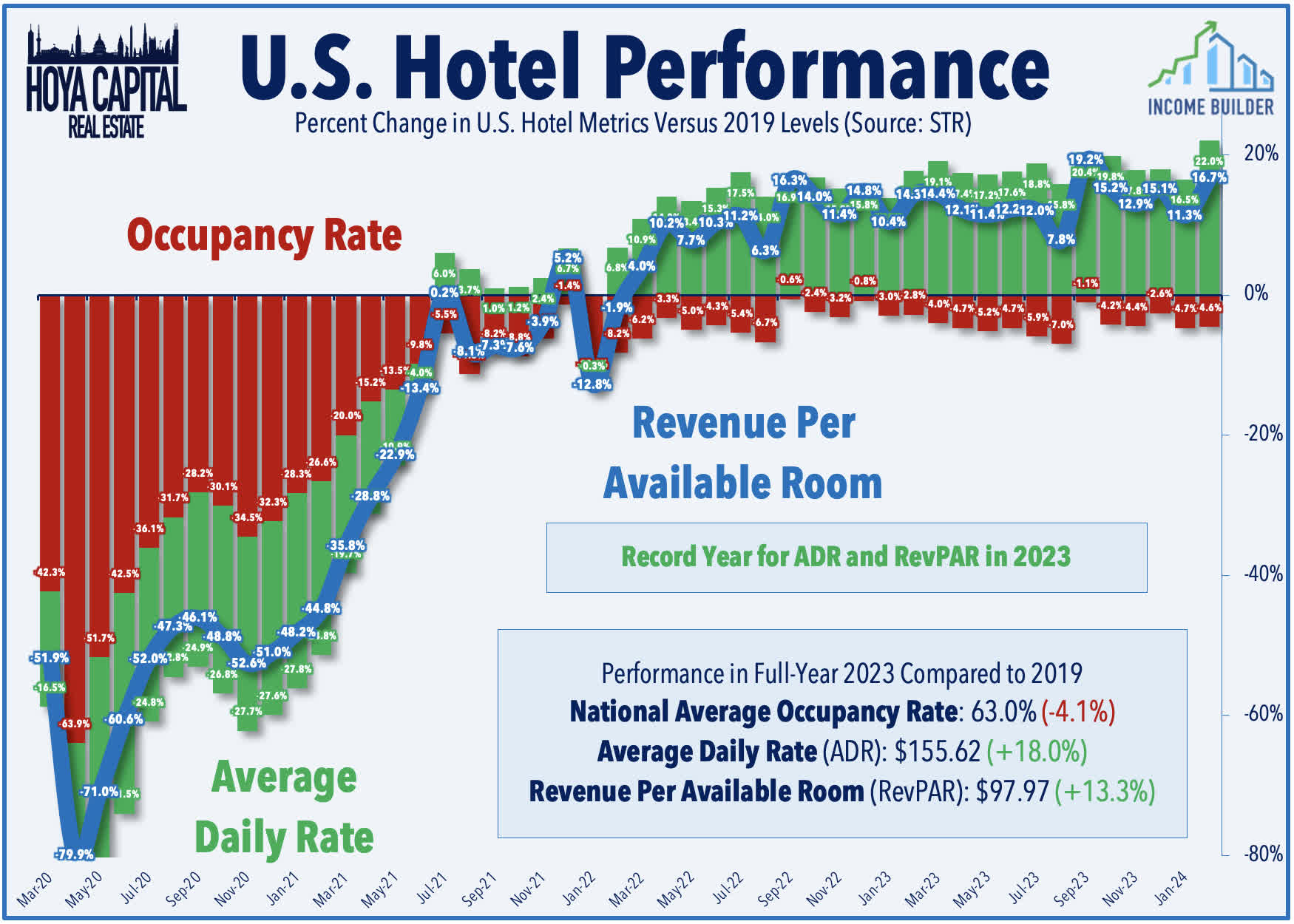

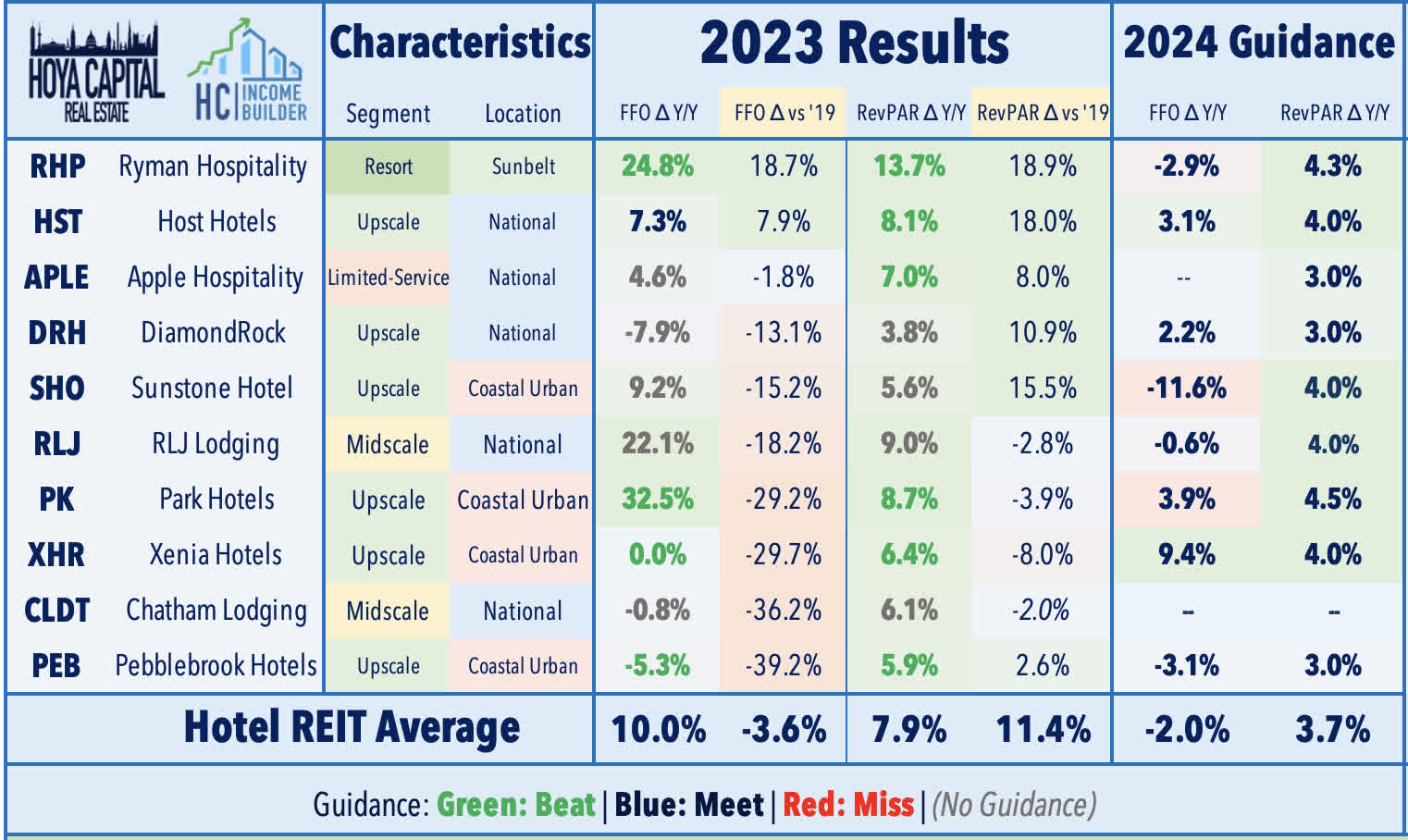

Hotel: (Final Grade: A-) At the peak of the pandemic downturn in April 2020, there were serious doubts about whether there would even be a hotel REIT sector when the dust settled. The past four years weren't pretty, but as we enter 2024, the hotel REIT sector is healthier now than it was in 2019. These REITs delivered another impressive earnings season with all five hotel REITs that provide full-year FFO guidance beating their full-year earnings, with commentary indicating that leisure demand has moderated only slightly in recent months, while business and group travel has continued its gradual recovery. TSA Checkpoint data shows that throughput has remained at around 110% of 2019 levels in early 2024, while hotel data provider STR reports that industry-wide Revenue Per Available Room ("RevPAR") was 13% above 2019 levels for full-year 2023, as a roughly 18% relative increase in Average Daily Room Rates ("ADR") offset a roughly 4% drag in average occupancy rates. Positive trends continued into early 2024, with RevPAR averaging about 14% above 2019 levels thus far. Hotel REIT guidance indicated that 2024 is shaping up to be the first "normal" year since 2019, with a tight forecast range of 3-5% RevPAR after double-digit swings in each year since 2020.

Hoya Capital

At the individual REIT level, Host Hotels (HST) - the largest hotel REIT - has been an upside standout after reporting that its RevPAR rose 8.1% during the year, which was 18% above 2019 levels. Host sees a "stable operating environment" in 2024 with forecasted RevPAR growth of 4%, resulting from "continued improvement in group business, a gradual recovery in business transient, and steady leisure demand." HST recorded full-year FFO growth of 7.3% in 2023 - roughly matching its prior outlook - and sees FFO growth of 3.1% in 2024. Xenia Hotels (XHR) - which focuses on luxury brands in West Coast and Southeast markets - has been the top-performer this earnings season after it reported better-than-expected FFO and RevPAR metrics in Q4 and provided an upbeat outlook for 2024, with expectations for sector-leading FFO growth of 9.4%. Sunbelt-focused Ryman Hospitality (RHP) - which has posted the strongest operating trends throughout the pandemic - has also been an upside standout after it posted double-digit FFO and RevPAR growth in 2023, each to levels that are roughly 20% above the 2019 comparable. Apple Hospitality (APLE) has also been a pandemic-era outperformer, posting another solid quarter, showing steady trends in the limited-service segment. Pebblebrook (PEB) has been a laggard after its results showed that the post-pandemic recovery remains incomplete in the business-travel-dependent coastal urban segments. PEB reported that its FFO remained nearly 40% below 2019 levels in 2023, while its RevPAR finally recovered to pre-pandemic levels - far below the 12% average increase from the balance of the sector.

Hoya Capital

Cannabis: (Final Grade: B+) We've only seen results from one of the four cannabis REITs, but so far, so good. Innovative Industrial (IIPR) has rebounded this earnings season after it reported stronger-than-expected results showing an improvement in rent collection in late 2023 and into early 2024. IIPR - which was the best-performing REIT from 2017-2021 before stumbling hard over the past two years amid industry-wide headwinds - reported that it collected 100% of owed rents in Q4 and year-to-date through February, up from the lows of around 90% in mid-2023. While certainly an improvement, the 100% collection rate in Q4 did include roughly 3.5% in previously delinquent rents and/or security deposits, including a $800k security deposit from 4Front related to a development property that faced delays in completion, and roughly $2M in legal settlements related to lease defaults from Kings Garden and Parallel. For Cannabis REITs - which have concentrated leasing and lending efforts on larger multi-state operators ("MSOs") and publicly-traded firms in recent years - tenant default issues have remained limited to a handful of smaller single-state operators. Despite the industry-wide headwinds throughout the year, IIPR reported that its full-year adjusted FFO rose 7.4% in 2023 to $9.08, which easily covered its $7.22/share dividend, representing a dividend yield of above 8%.

Hoya Capital

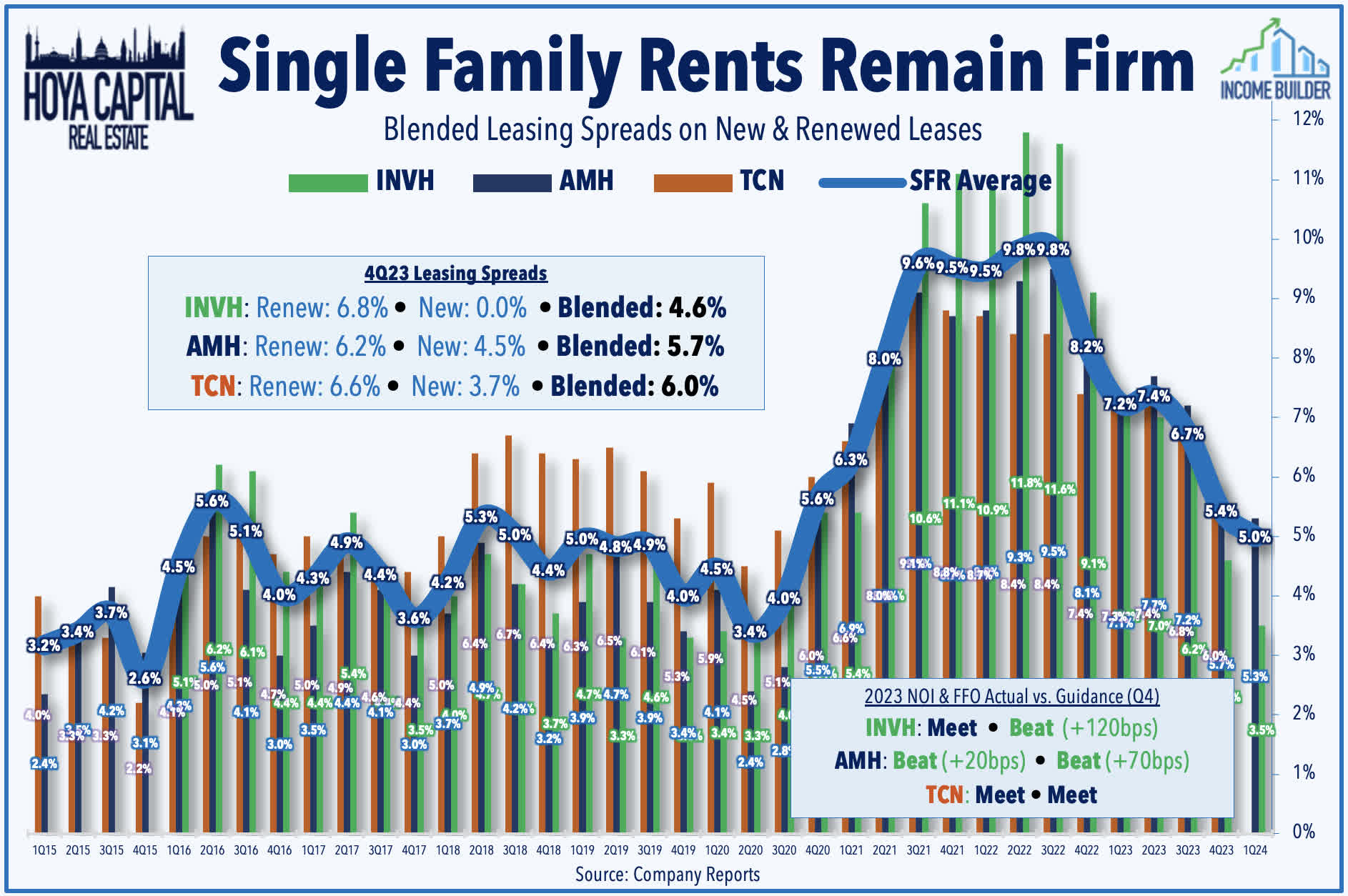

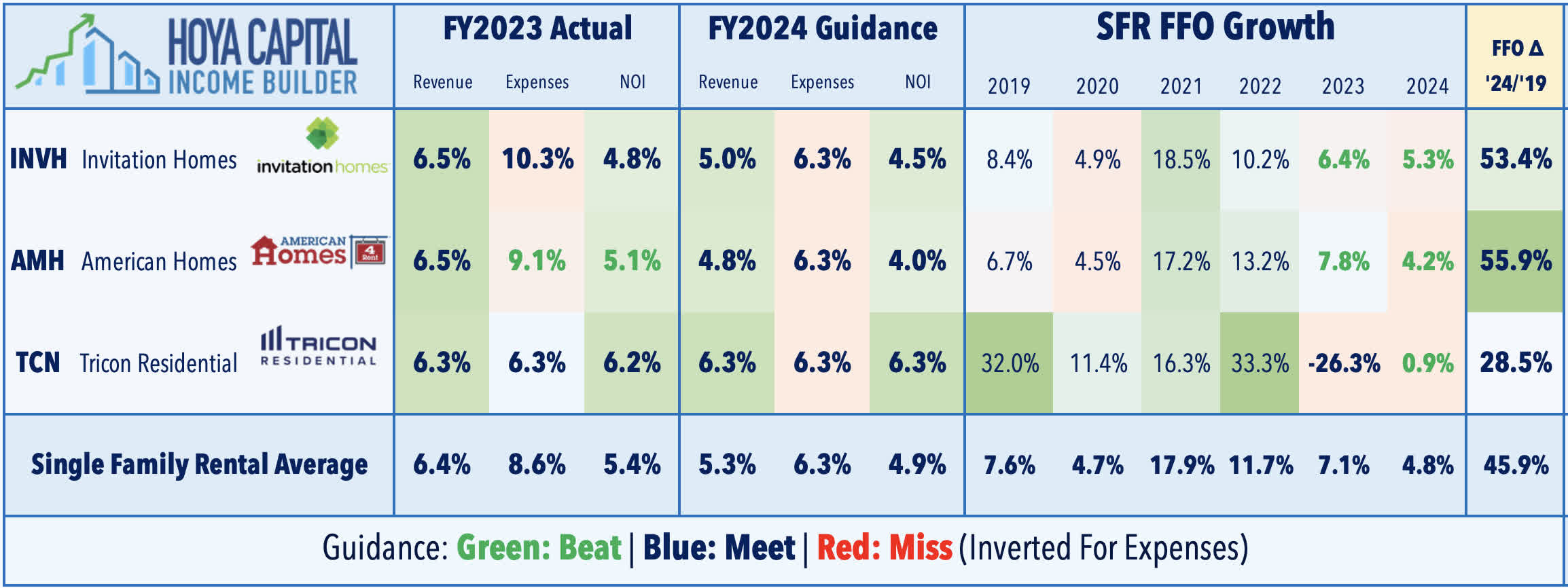

Single-Family Rental: (Final Grade: A) While results from multifamily REITs were less-than-impressive this earnings season amid a surge in apartment completions, reports from SFR and manufactured housing REITs showed that rent growth trends have remained buoyant on the single-family side, where inventory levels remain tight. American Homes (AMH) was the upside standout among the SFR REITs, reporting impressive full-year FFO growth of 7.8% in 2023 - above its prior forecast - and projecting FFO growth of 4.2% in 2024. Rent growth trends were particularly impressive, with blended spreads of 5.7% in Q4 (+6.2% renew, 4.5% new), while blended spreads held firm into January at 5.3% (+5.7% renew, 4.3% new). The earnings call was focused largely on macro SFR fundamentals and AMH's outlook on external growth. AMH conceded that "acquisition and capital market environments are not conducive to accretive growth" via traditional acquisition channels, but it continues to lean heavily into its internal Build To Rent ("BTR") program, which was responsible for the vast majority of its total portfolio growth in 2023.

Hoya Capital

AMH's macro outlook on SFR fundamentals remained very upbeat, pushing back on concern over an uptick in SFR supply in several markets (Vegas and Phoenix), and providing guidance calling for 96% occupancy rate and 4.0% same-store NOI growth in 2024. Invitation Homes (INVH) reported decent results as well, highlighted by blended rent growth of 4.6% in Q4 (+6.8% renew, 0.0% new) and FFO growth of 6.4% in 2023 - well above its prior guidance of 5.0%. INVH expects NOI growth of 4.5% in 2024 at the midpoint, with a 5% increase in revenues and a more modest 6.3% increase in expenses. INVH notes this guidance incorporated expectations of 8-10% property tax increases and insurance expense growth in the "mid- to high teens." Meanwhile, Tricon Residential (TCN) - which agreed to be taken private by Blackstone (BX) earlier this year - reported in-line results as sector-leading property-level NOI growth of 6.2% was offset by the effects of sharply higher interest expense, resulting in a 26% decline in full-year FFO. Underscoring the challenges faced by smaller private players with even higher leverage, TCN's interest expense increased by over $100M in 2023 to $316.5 on a portfolio that generates $795M in total revenue.

Hoya Capital

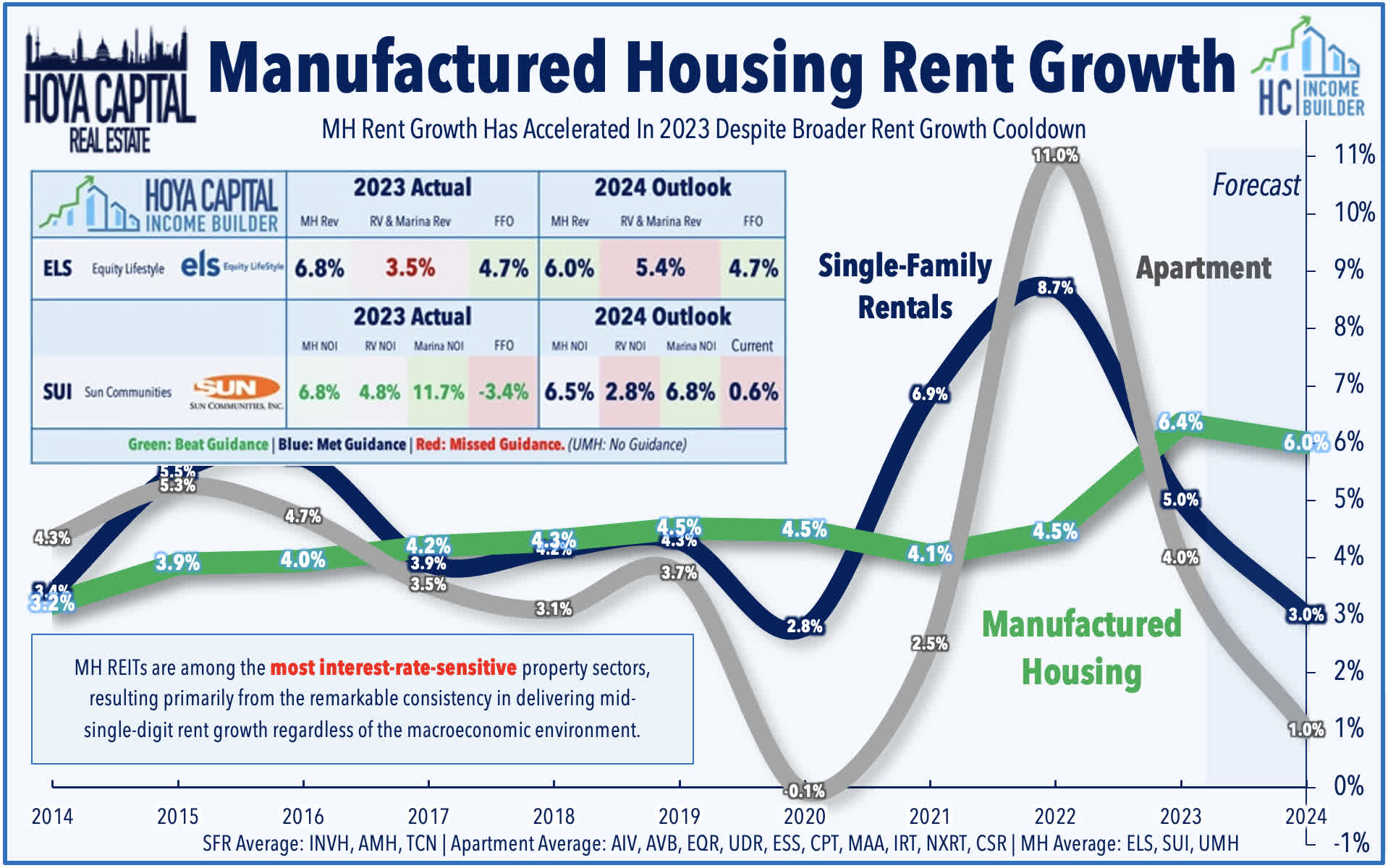

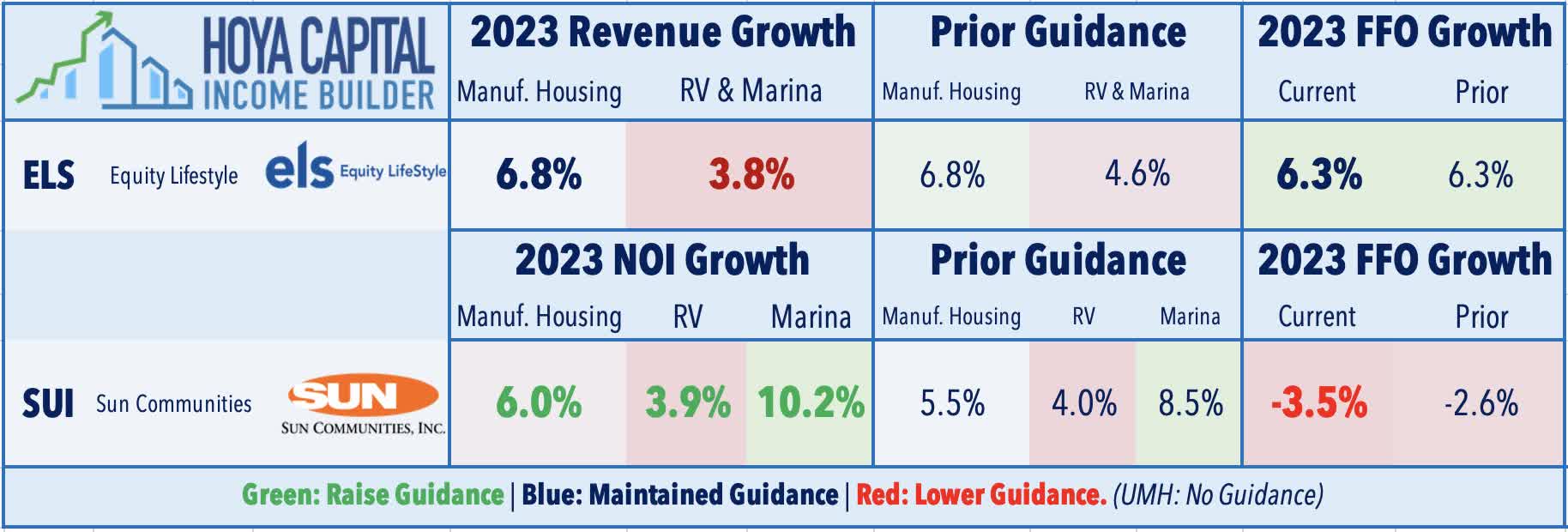

Manufactured Housing: (Final Grade: B) Sticking in the residential sector, manufactured housing REITs appear to be regaining their footing after an 18-month stretch of uncharacteristic stumbles. Sun Communities (SUI) reported very strong U.S. property-level performance in Q4 and provided guidance showing a return to FFO growth in 2024 alongside a 1% dividend hike, which helped to offset continued weakness in its struggling UK segment. SUI reported that its full-year Core FFO declined -3.4% in 2023 - slightly better than its prior guidance - and sees a return to growth in 2024 with expected FFO growth of 0.6%. Property-level performance in the U.S. was very strong in the final months of 2023, as headwinds from its sluggish transient RV segment finally began to moderate. For full-year 2023, SUI reported segment-level NOI growth of 6.8% for Manufactured Housing, 4.8% growth for RVs, and 11.7% growth for Marina - all of which exceeded its prior guidance. Its ill-timed international expansion into the UK in 2022 continues to present headaches for the company, however, as SUI wrote off another $370M in its Park Holidays investment and noted that its collateral backing a separate £337M loan was valued below principal. Ultimately, its UK division recorded a total NOI that was 55% below SUI's initial outlook for the year.

Hoya Capital

Results from Equity LifeStyle (ELS) were decent, highlighted by a healthy 7% dividend increase. ELS recorded full-year FFO growth of 4.7% in 2023 - roughly consistent with its recently revised guidance - and sees growth of 4.7% again in 2024. Despite an -11% decline in transient RV revenues, core revenues still rose 5.8% in 2023, but expenses came in hot at 7.0% for the year, driven primarily by higher real estate taxes in Florida and the effects of the nearly 60% jump in insurance premiums for the policy year beginning last April. ELS will provide an update on its 2024 renewals' next earnings call but noted a muted level of claims this year given the weak storm season. UMH Properties (UMH) has been a top-performer after reporting strong results showing steady demand and mid-single-digit rent growth across its portfolio. UMH reported full-year normalized FFO growth of 1.2% in 2023, which was 36% above the pre-pandemic 2019 level. Unlike its two larger MH peers which typically only own the land under the owner-occupied homes and RVs, UMH owns and rents over 10,000 physical homes. UMH credited strong leasing activity in this rental portfolio - which is now 94% occupied - and had success in selling these homes as well. These newly occupied rental and sales units resulted in a 9% same-property income growth and 13% NOI growth.

Hoya Capital

Industrial: (Final Grade: B+) While not reflected in the relatively muted stock price performance during earnings season, industrial REITs reported an impressive slate of earnings results, which collectively pushed back on concerns of softening logistics fundamentals. Seven of the eight REITs reported FFO growth that exceeded their prior FFO guidance - averaging over 9% in full-year 2023 - and provided guidance that projects solid growth averaging 6% in 2024. After a modest softening in rent spreads in Q3 from the record-setting pace in early 2023, we saw a reacceleration in spreads in Q4 to nearly 40% despite supply headwinds. Logistics stalwart Prologis (PLD) noted that while market rents have turned negative on a year-over-year basis following three years of record-setting growth, the "embedded" growth within the portfolio remains substantial as leases (typically signed with 3-6 year terms) get reset at market rates. PLD recorded net effective rent growth over the quarter of 74%, bringing the full year to a record of 77%. At the property level, Prologis achieved same-store NOI growth of 10.0% in 2023 - fractionally above its prior guidance - and sees same-store growth of 8.5% in 2024.

Hoya Capital

Results from the mid-cap REITs were quite strong as well. EastGroup (EGP) has been among the upside standouts after it reported full-year FFO growth of 11.3% in 2023 - above its prior guidance of 10.7% - and sees FFO growth of 6.2% in 2024. First Industrial (FR) reported similarly strong results and hiked its dividend by 16%. Both FR and EGP recorded a reacceleration in leading spreads in Q4 after a modest cooldown in mid-2023. Terreno (TRNO), meanwhile, posted sector-leading NOI growth of 13.3% in 2023 and pushed back on concerns over supply growth in its urban infill markets. Rexford (REXR) has been a laggard, however, after providing soft guidance reflecting an ongoing regional cooldown in its previously red-hot Southern California markets. While blended leasing spreads remained impressive at 45.6%, this was the lowest increase since Q4 2021. REXR noted a recent recovery in West Coast port traffic resulting from Red Sea disruptions, which follows a period of notable weakness and a major shift in volumes towards the East Coast. Volumes in LA and Long Beach rose 22% in Q4 compared to a -3% decline on the East Coast.

Hoya Capital

Cold storage operator Americold (COLD) has also been a laggard after its results showed surprising weakness in consumer spending on refrigerated food products in late 2023 and into early 2024 - especially in its European markets - and flagging a "big swing in the economy" which led to a 7.6 percentage-point drop in throughput volumes in Q4 versus the prior year. Underscoring the more services-oriented nature of cold storage operations compared to traditional industrial real estate, the disappointment in Q4 was entirely attributable to its weakness in its lower-margin warehouse services segment. While COLD's real estate segment posted an impressive 15.4% increase in total NOI for 2023 driven by record-high occupancy rates and strong pricing power, COLD's service segment ("global warehouse services") posted a 33% dip in total NOI in 2023. COLD's outlook indicated that these mixed trends will continue this year, cautioning that the services segment will see weaker performance in the first half of 2024 compared to the already-soft Q4 "given the continued declining throughput volume assumptions."

Hoya Capital

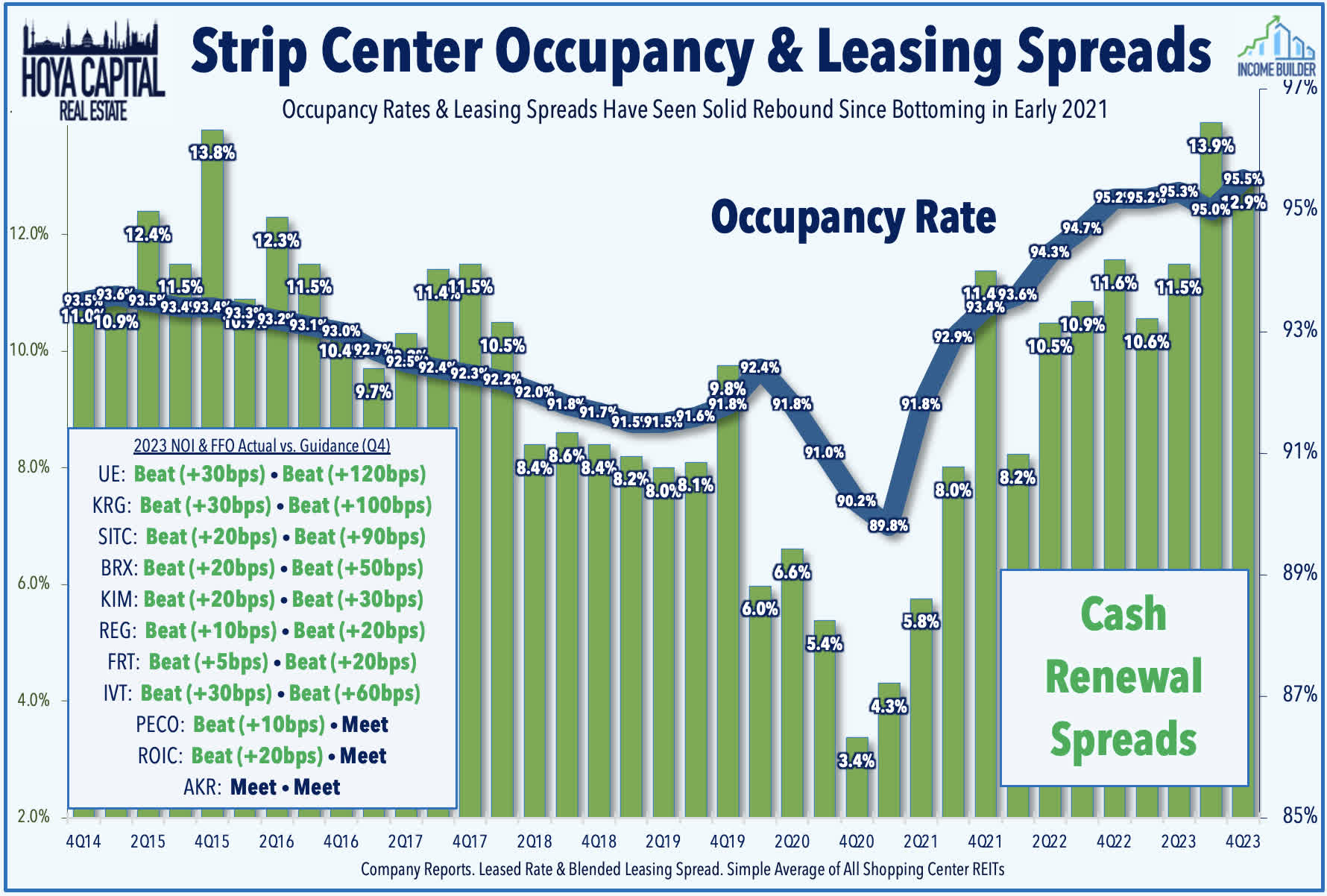

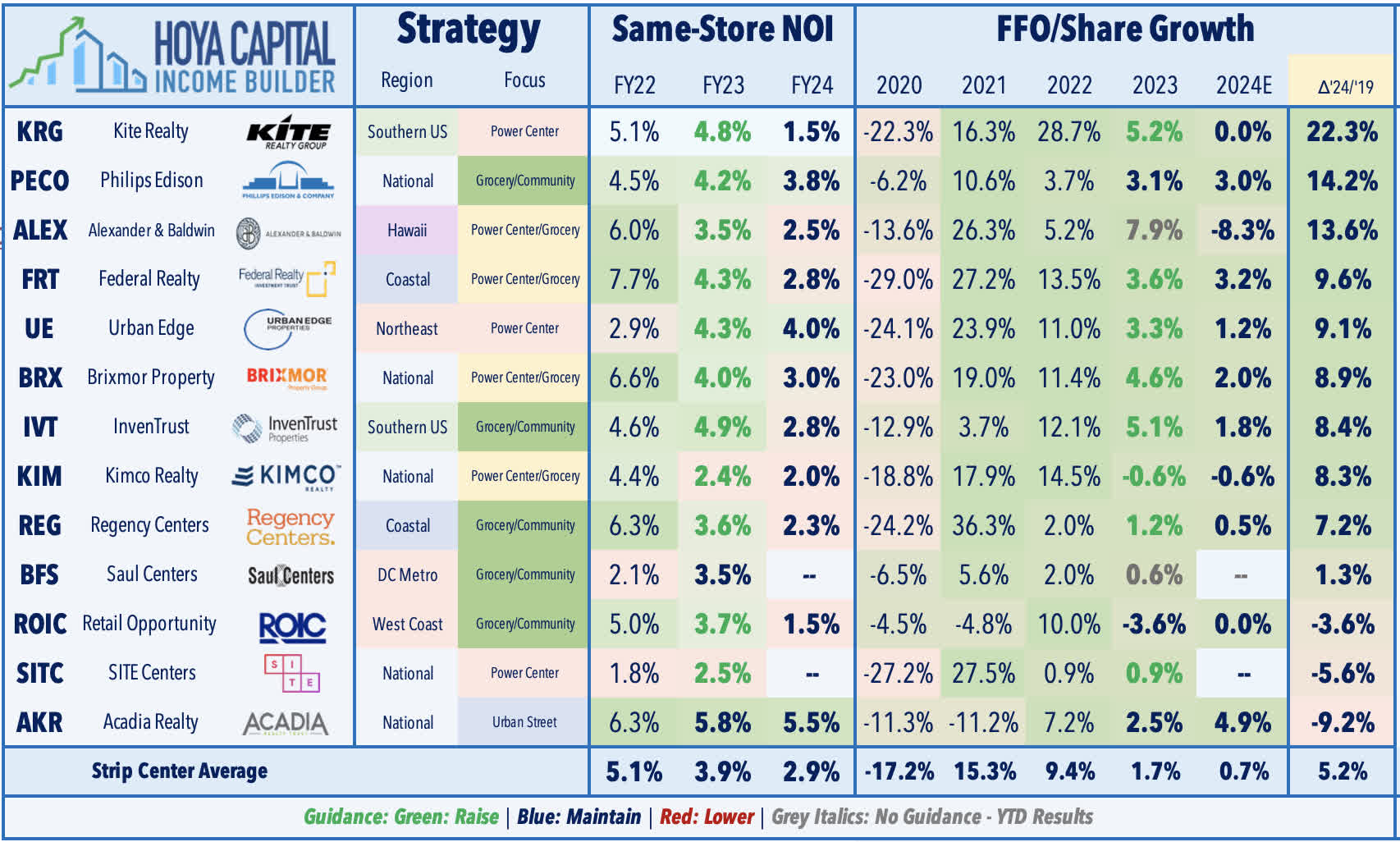

Strip Center: (Final Grade: A) As with the aforementioned mall REITs, results from strip center REITs this earnings season showed that retail landlords have the upper hand in rent negotiations for the first time in a decade, as store openings have outpaced store closings in each of the past three years. Strip center REITs delivered the highest total quantity of earnings beats: nine of the twelve strip center REITs beat their FFO estimate, while eleven of the twelve topped their NOI estimate. A number of REITs reported record-setting leasing volumes and rent spreads this earnings season, but the outlook for 2024 was surprisingly soft in light of this impressive leasing performance. Strip Center REITs expect FFO growth of 0.7% in 2023 after delivering growth of around 2% in 2024. That said, the initial guidance provided by strip center REITs at this time last year ultimately proved to be especially conservative, setting the stage for a year full of "beat and raise" quarters.

Hoya Capital

Kimco (KIM) the largest strip center REIT reported solid results as higher interest expense and the impacts of the Bed Bath and Party City turnover offset an otherwise record year of leasing performance. Kimco noted that it signed 1.0 million square feet of new leases in Q4 - the highest quarterly level in over 10 years - and generated pro rata cash rent spreads for new leases of 24.0%. Notably, this included four former Bed Bath spaces in which KIM achieved rent increases of 57%. Given these record leasing performance, the outlook for 2024 was disappointing, with KIM projecting a -0.6% decline in FFO this year which incorporates plans to "recycle lower growth centers" following its acquisition of RPT Realty. Kite Realty (KRG) has been an outperformer after reporting sector-leading full-year FFO growth of 5.2% in 2023 and noting that it signed a record 380k SF of new leases in Q4, achieving blended spreads of 14.5%. Brixmor (BRX) has also been a standout after reporting that leasing volumes totaled 1.7 million SF in Q4 - a record for the company - with rent spreads on comparable space of +19.6%. SITE Centers (SITC) has been a leader this earnings season as well after providing further specifics on its planned spin-off of its net lease properties into a new REIT named Curbline Properties that were well-received.

Hoya Capital

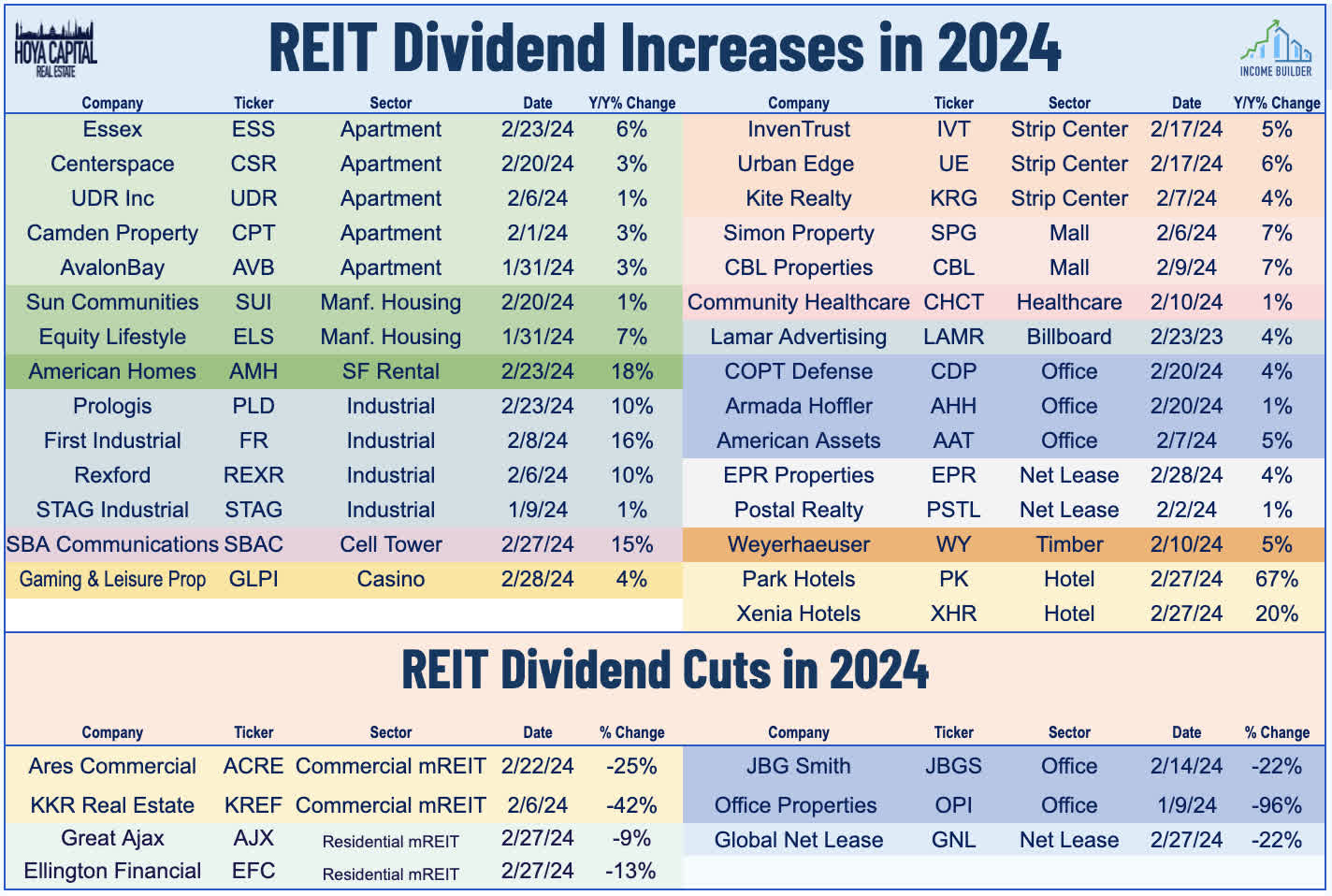

Upside surprises this earnings season came largely from the service-oriented pro-cyclical property sectors - retail, hotel, and specialty REITs - and from the still-supply-constrained single-family housing and logistics markets. As we'll discuss in the Losers of REIT Earnings Season report later this week, while there were no major "bombshells" this earnings season, the pockets of relative weakness were seen in the interest-rate-sensitive property sectors - net lease and office - along with goods-oriented sectors. Dividend sustainability is always a focus during earnings season, and we've been scouring through earnings calls to glean insights into the outlook for dividend hikes - and in some cases, dividend cuts - this year. Positively, we've seen roughly two dozen REITs raise their dividends this earnings season - lifting the full-year total to 29 - while seven REITs have lowered their dividend this year, nearly all of which are linked to office-related headwinds.

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Mortgage, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital