koiguo/Moment via Getty Images

koiguo/Moment via Getty Images

The investment thesis for Otis Worldwide (NYSE:OTIS) revolves around the substantial moat they possess in servicing and maintaining their extensive portfolio of elevators. Picture a scenario where a company not only records revenue from equipment sales but, as the equipment depreciates and faces malfunctions, is consistently re-engaged for maintenance services. This creates a reliable and predictable stream of income that doesn't rely on consumer demand but more on the quality and usage of their products. OTIS embody this model, and it is the service aspect that is the cornerstone of their business strength. That is why I am initiating Buy recommendation on the company.

OTIS stands as the largest global enterprise in the manufacturing, installation, and service of elevators and escalators. Facilitating the movement of 2.3 billion people daily, the company manages an extensive portfolio of approximately 2.3 million customer units worldwide, representing the largest such portfolio globally. Otis elevators and escalators are integral components of some of the world's most iconic structures, transportation hubs, and vibrant retail centers.

Around the world, Otis elevators are installed in buildings of all heights and styles. Some examples include:

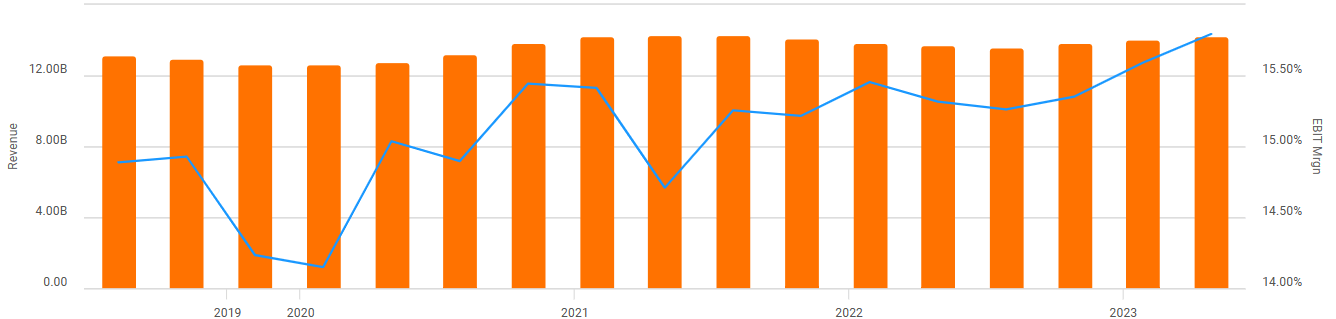

Beginning with the income statement, revenues aren't robust here, 5-year CAGR sales are 1.9% which is below the industry median of 5.12%, hampered by slower New Equipment growth. That being said, probability is better, OTIS sport 15% EBIT Margins after a 150bps move up since 2020, this is 59% higher than the sector median driven by robust operating leverage in the Service segment. OTIS also boast reasonable Net Margins of 9%, which is 67% higher the sector median. This alongside well managed working capital helps drive strong FCF Margins that are above 10%.

Seeking Alpha

In my view, the balance sheet is adequate. Net Debt to Sales stands at 41% with the next major maturity of $1.3 billion due 2025. The current cash balance sits at $1.27 billion, but with average operating cash flows of $1.64 billion over the last 3 years, the company is currently in a fine position to service the principals.

The Service segment, constituting 60% of sales with margins north of 23% stands out as a particularly compelling aspect. With a global portfolio of over 2 million elevators and escalators, the service segment appears very profitable. A well-maintained elevator will typically experience 4 breakdowns a year and the golden rule to increase the life of an elevator is regular maintenance and inspections, which can cost up to $2000 per year.

Some common elevator failures include power failures, damaged sheaves, and motor failure, which highlights the importance of proactive maintenance. Notably, when things do go wrong the financial dynamics come into focus, a full refurbishment can cost between $150,000 to $1,000,000 depending on the size of unit. OTIS, being the manufacturer of these elevators, strategically positions itself as a dominant player by handling repairs of their own malfunctioning elevators. This integrated approach consolidates OTIS' dominance in this crucial sector of business.

In contrast, their Equipment Segment demonstrates less impressive performance with Operating Margins of 6% and flat growth. Similar to conventional retailers, this segment finds itself susceptible to fluctuations in macroeconomic climate, particularly in relation to construction spending.

Initially, I had worries about the valuation and potential multiple contraction, Seeking alpha rank the overall valuation an "F" and top-line numbers don't compare particularly well to the Sector. However, it's worth noting that their very profitable Service segment is aligning well with sector median growth rates and boasts nearly double the EBIT margins.

Full year revenues grew above the 10-year CAGR, sales climbed a robust 5.6% organically driven by Service segment growth of 7.6% constant currency (CC) and New Equipment sales growth of 1.2% CC. After subtracting costs, Adjusted Operating Margin increased 30bps to 16%, driven by a 50bps expansion in the Service segment for a second consecutive year.

In terms of outlook, the company expects a global softening in new equipment unit growth, but with prices expected to climb, sales are forecast to remain flat organically. More encouragingly is the Service segment, that is forecast to grow volumes as well as price, driving mid to high single digit organic revenues. Their strong market position allows good pricing power, and the ability to feed through higher operating overheads to clients, leading to an expected 40-50bps increase in Adjusted Operating Margins in 2024.

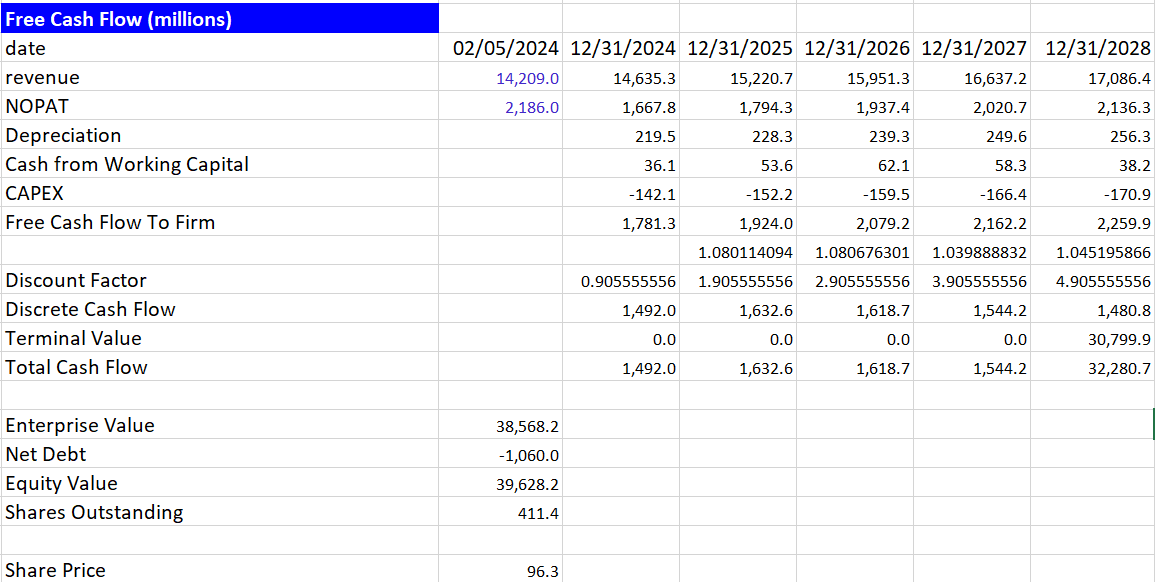

DCF (author own math)

To value OTIS, there are two approaches, the perpetuity approach and the multiple approach. Given the predictable nature of the Service segment, I began by using the perpetuity approach. Given a terminal growth rate of 4%, I get to a share price target of $96 and an upside of 6%. When using the multiple approach, I have been conservative in using the 5-year P/FCF ratio of 25x to get a share price target of $111 and an upside of 17%.

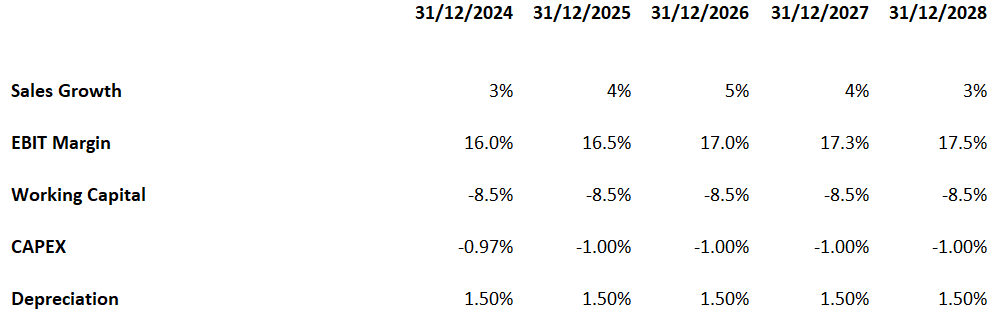

Assumptions for DCF (author own math)

OTIS are well positioned entering 2024, backlogs continue to grow, with strong demand across geographic regions. New Equipment sales stand to benefit in China due to the work going on with the nation's metro providers in helping expand urban transport and city development. In North America, OTIS has been awarded with the modernization of 16 elevator units in 560 Mission Street, as well as a maintenance contract for the 31 story commercial office building. In Hong Kong, they have been awarded a contract for 18 elevator units, which will be maintained by OTIS upon completion. In Dubai, a large project of 42 elevators has been granted in the world's tallest building, the Burj Khalifa. Finally, they are delivering on a multi-year modernization of the two duo lifts in the Eiffel Tower.

This strong backlog of work also produces good amounts of Deferred Revenue that helps free up cash flows that they use to return money back to shareholders. The dividend yield is 1.44% and I believe this will climb to over 2% in the coming years as the Service segment is a reliable underlying growth driver less affected by macroeconomic variabilities.

The main risk to my thesis is hybrid working. With the growing trend of corporations to utilize a hybrid and remote model of work, we could see less traffic across their office building network. Obviously, if the elevators are used less, they depreciate less, and the need for maintenance reduces, which is half their business model. Although, I don't see this as a critical issue because the company is well diversified across other industries such as leisure, where traffic has picked up again post COVID.

The quality of business here is strong, leaving the opportunity for further multiple expansion, given the underlying growth drivers. The valuation doesn't feel stretched, and I believe a higher multiple might be warranted, which could leave room for further upside. The lack of risk to earnings here is also compelling, which could increase the dividend yield, I believe this stock will become a big dividend player in the years ahead, so I am recommending a Buy on the company.