standret/iStock via Getty Images

standret/iStock via Getty Images

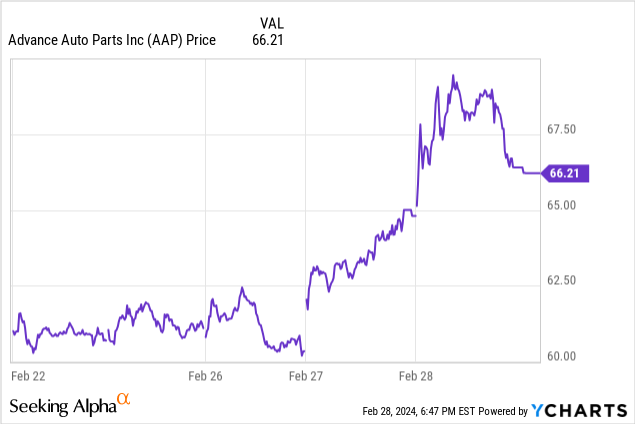

Advance Auto Parts, Inc. (NYSE:AAP) reported its Q4 earnings on Wednesday, February 28th. They were nothing special, with the company announcing a loss for the quarter. Meanwhile, sales fell once again.

Despite that, the stock rallied sharply on Wednesday morning as traders latched onto the firm's stronger guidance for 2024. While AAP shares pared their gains in afternoon trading, it was still a favorable reaction to a mixed earnings release:

This leads to a broader question: is Advance Auto Parts finally reaching an inflection point thanks to moves from its new management team? Or is this simply going to be another sell-the-news event for this struggling auto retailer?

The company's Q4 earnings release had two stories. One was the past results, which were unfavorable. Advance Auto Parts lost money for the quarter and witnessed declining revenues year-over-year. Furthermore, EPS came up far short of expectations for the quarter.

On the other hand, the company guided its earnings per share outlook higher for the upcoming year. Let's give management the benefit of the doubt that they will turn things around in 2024 and return to robust profitability.

Even if that is the case, however, I'm far from convinced that Advance Auto Parts would make a great long-term investment.

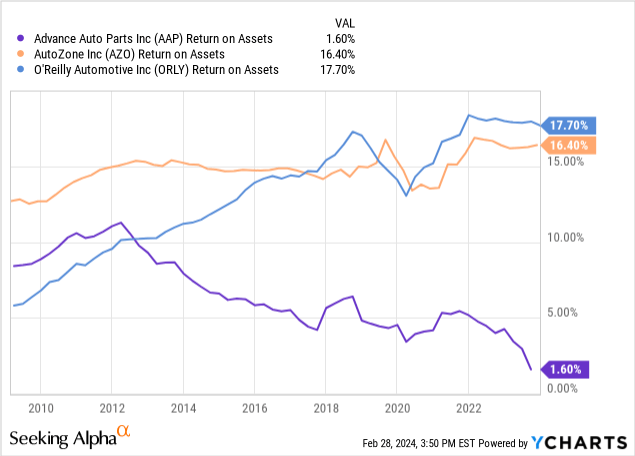

I can back up that assertion with one chart. Here is a comparison of Advance Auto Parts' return on assets "ROA" over the past 15 years compared to O'Reilly Automotive (ORLY) and AutoZone (AZO):

Coming out of the 2008 financial crisis, AutoZone was earning a roughly 13% ROA, with Advance Auto Parts at 9% and O'Reilly Automotive around 6%.

Since that point, things have entirely changed. O'Reilly went from last to worst, with its ROA rising to 17.7% now. AutoZone's metrics also significantly improved, with its ROA rising to 16.4%. Advance Auto Parts' ROA, by contrast, collapsed to just 1.6%.

If you look at Advance Auto Parts' trajectory, you can see that its ROA has been in steady, unrelenting decline since around 2013. However, the decline markedly accelerated over the past year. I'd totally buy the argument that the 1.6% ROA is too low and that 2023 was an unusually bad year for the company.

That said, if the ROA bounces back to 5% and flattens out there, how big of an achievement is that? It would still leave the company at just one-third of the profitability of its major rivals. It's one thing to say that Advance Auto Part will bounce back to 2022-level profitability. In fact, it's quite likely.

But what's the bigger structural change that would get Advance Auto Parts back to where its peers are at? 2023 was such a terrible year that some recovery seems likely. But unless there are large successful changes in the company's core operations, it is hard to see how the company would match either of its top rivals.

On Wednesday's conference call, there was an interesting tidbit about the firm's thoughts on industry composition. Here are CEO Shane O'Kelly's comments (emphasis added):

"But the industry fundamentals are very good. This is a disciplined industry. By the way, it's an industry that even with the big players, there's still room and runway to grow. By the way, there is just growth that occurs naturally. And so we won't be a share taker, but we're -- first step is to be a shareholder, and I mean that in terms of market share. So that's what we're looking to do."

Over the years, Advance Auto Parts has grown its store base less quickly than the competition, which isn't surprising given its lower returns on invested capital over the past decade. However, it's notable that the prior management team at the company was focused on marketing and it still struggled to grow the brand's footprint or revenues in a profitable manner.

The new team, led by O'Kelly, has more experience with supply chains and logistics. Given Advance Auto Parts' low profitability compared to rivals, this seems like a most useful skill set to have. If the core problem is simply inefficiencies in the firm's operations, a skilled team of logistics and supply chain experts might be able to solve things.

So far, the new management team has already put in place moves which will strip $150 million out of the firm's annual operating costs. Management also signaled that it is targeting another $50 million in reductions going forward.

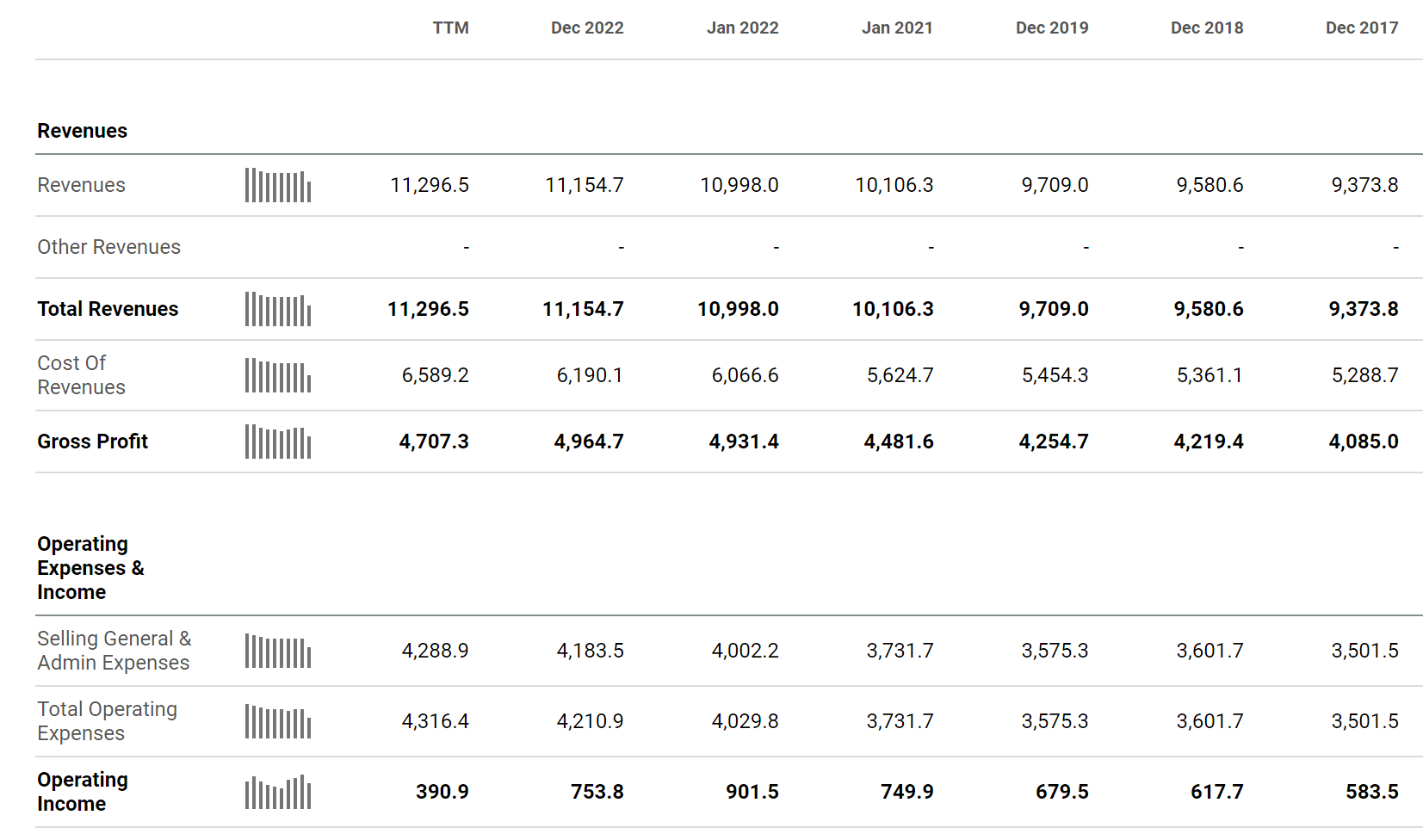

Looking at the firm's income statement, however, this does not appear to be that large of a reduction compared to the firm's total operations:

AAP Income Statement (Seeking Alpha)

The company was generating roughly between $600 million and $900 million in operating income annually prior to the significant downturn witnessed in 2023. Adding $150 million or even $200 million to operating income would be nice, but it doesn't appear to be a complete game changer for the company.

Interestingly, much of the $150 million in already realized spending cuts came from the marketing budget. Here is Mr. O'Kelly explaining this on the conference call:

"I think notably, marketing was an area where there were more significant cuts than in the other areas because we invested in marketing programs that didn't have a yield. And so we view that cost takedown not only as necessary, but one that didn't dampen our sales, if anything, I think we've got the opposite going out as we cleared out some bureaucracy."

No one wants to waste marketing money, of course. But I wonder if these reductions will be beneficial to the company over the longer term. O'Kelly states that the marketing reductions didn't dampen sales. However, in Q4 of 2023, Advance Auto Parts saw its revenues fall year-over-year as comparable store sales declined slightly. Meanwhile, on the same day that Advance Auto Parts announced its soft quarter, AutoZone reported its revenues grew 4.6% year-over-year as its comparable same-store sales rose 1.5%. In other words, Advance Auto Parts still has work to do to stop losing market share to rivals, and marketing budget cuts could further weaken its competitive position.

As you may have noticed, I'm at a hold rating rather than a sell on AAP shares. Given the tone of the article so far, what would lead me to a neutral outlook for the firm?

Simply put, I can see the argument for an Advance Auto Parts, Inc. turnaround here. O'Kelly has only been the CEO since September 2023, and new management should get more than six months to deliver results. Cutting marketing is an easy move to make, and perhaps there was some obvious fat left in that department from the prior leadership team.

What has excited investors is that O'Kelly can use his operations skills honed at Home Depot (HD) to turn Advance Auto Parts into a leaner and meaner retailing machine. That sort of deeper structural reimagining of the company, however, is likely to take longer than six months to play out.

O'Kelly is not trying to rapidly grow the company back to prosperity. Rather, he has set a goal to maintain a stable market share while improving profitability significantly. Advance Auto Parts has a large enough store and revenue base that it should be a viable player in the U.S. market with more efficient operations. Perhaps it will take O'Kelly a year or two to get the logistics and operations up to speed, but when he does, there could be considerable upside.

I've seen bulls suggesting that the company has the potential to do $10/share in annual earnings at its turned around end state; needless to say, the stock would be a steal at today's price if the company can deliver on that aim. Advance Auto Parts routinely earned more than $6 per share annually in the mid-2010s, and that was on a smaller revenue base and with more shares outstanding. If Advance Auto Parts, Inc. can get back to the sorts of profit margins and ROA figures that it was running a decade ago, there is a path to $8-10/share in annual EPS and a sharply higher stock price.

I can make an argument for the theoretical bull case for the company. And I wouldn't be short shares of the company here, given the significant upside potential if things go right and the seemingly discounted starting valuation today.

That said, for now, I must judge the stock based off of the actual results that the company is reporting. And the firm's Q4 in particular and 2023 more broadly offer little reason for optimism.

I'm willing to give O'Kelly more time to try to turn things around. But I wouldn't be in a rush to put my own capital to work here until the firm stabilizes its market share and we see signs that the company can straighten out its structural issues. I do think 2024 will be better than 2023 was for Advance Auto Parts, and shares could rally in the short-run on the more favorable guidance.

For long-term investors, however, I'd wait for signs that Advance Auto Parts is finally holding its own against O'Reilly Automotive and AutoZone before I got too excited.