Nick_Pandevonium/iStock via Getty Images

Nick_Pandevonium/iStock via Getty Images

I continue my focus on renewables energy by analyzing Ormat Technologies (NYSE:NYSE:ORA), one of the leading global companies in geothermal power generation. Here are links to my recent articles on renewable-related companies: Northland Power (TSX:NPI:CA), TransAlta (TAC), Sunnova (NOVA), Innergex (INE:CA) and Enlight Renewable Energy (ENLT). ORA has an installed capacity of 1215 MW, including 110MW of solar, out of a total of 16.3 GW of geothermal installed globally. Starting in 2020, the company implemented an investment campaign with the aim of generating new growth, finding a significant increase in revenues and a moderate improvement in operating margins and profitability. In January 2024, ORA finalized the acquisition of the geothermal segment of Enel Green Power North America for $271m, resorting to $200m in debt and securing an EBITDA of about $38m for an EV/EBITDA ratio of 7.13x. Although I have a very good impression of the company in terms of quality and business management, I think it is quite expensive at the moment, a fact confirmed by my DCF model. For this reason I currently rate the stock as a Hold. In the following sections, I will look at ORA’s business, main risks and opportunities, and financial performance, to provide an insightful justification for my outlook on the stock.

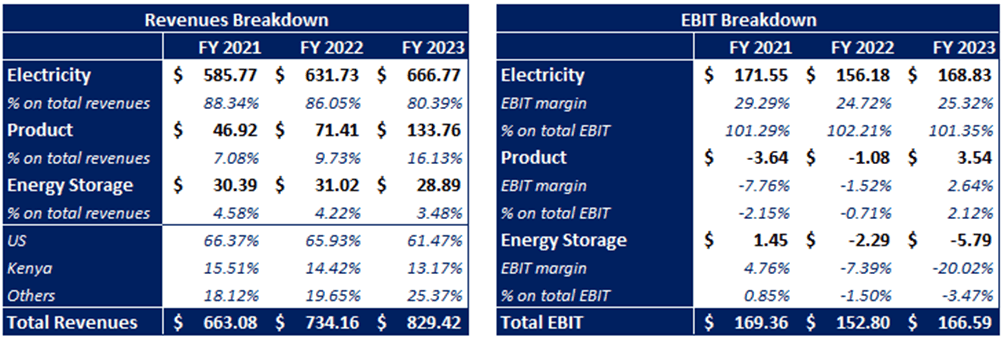

Ormat business is structured around three business segments: Electricity, Product and Energy Storage.

ORA SEC Filings and Author's Analysis

Electricity: within the segment it develops, builds, and operates geothermal, and to a small extent solar energy plants, selling the electricity produced through PPA contracts, with a weighted average term of 15 years as of December 2023. This is the main source of total revenues with a share of 80.4% in FY23, down from 88.3% in FY22; such decrease is mainly due to increased revenues in the Product segment and, to a lesser extent, a decline in electricity production due to maintenance of some geothermal plants resulting in a performance below the potential capacity.

The segment is even more essential in terms of EBIT, as the other two segments have been performing negatively or close to parity in recent years. In FY23, it posted an EBIT margin of 25.3%, up from 24.7% in FY22.

Asset portfolio: ORA owns 1215MW of installed capacity including 110MW of photovoltaic plants, 53MW of REG (Recovered Energy Generation) plants, and 1042MW of geothermal plants, accounting for 6.4% of installed geothermal capacity globally.

Assets under construction: the construction of 11 geothermal plants with a total capacity of 131MW is planned between 2024 and 2026, of which 26MW expected in 2024 as well as the installation of 72MW of photovoltaic plants, including 16MW in 2024. Moreover, Ormat finalized the acquisition of some assets of ENEL Green Power North America in January 2024, increasing their capacity by 100MW, 40MW of geothermal plants and 60MW of photovoltaic plants. The acquisition has already been included in the asset portfolio capacity previously discussed but has not been reflected on the balance sheet yet. Based on statements released by Enel, the plant is expected to achieve $38m in EBITDA, which added to further $15m generated by the plants projects that will be finalized in 2024, should result in an overall increase of around $50m in EBITDA, all other things being equal.

Product: within the segment ORA operates as an EPC for the construction of geothermal plants for third parties.

Backlog: as of December 2023, the backlog was worth $152m, 76% of which was in New Zealand. The segment appears to be improving after the big drop due to the pandemic; between FY21 and FY23, the segment was characterized by steadily increasing revenues, albeit with a backlog below FY17 and FY18 levels.

EBIT margin reached 2.6% in FY23, improving the negative results experienced between FY20 and FY22. It appears that the segment's breakeven is located around $100m in revenues, below which it fails to generate operating profits.

Figures in $ Million (Investor Presentation March 2024)

Outlook: growing demand for renewable energy is expected to boost new installations of geothermal power plants. However, I believe Product will hardly pair Electricity marginality, thus it will continue to have a dilutive effect on the company's margins.

Energy Storage: the segment deals with the construction and operation of storage systems, with a current storage capacity of 170MW (298MWh). As of December 2023, most of its revenues are derived from merchant prices, causing greater volatility in the segment's results than in the Electricity one. This volatility is heavily affecting marginality, with a slight dilutive effect on ORA 's total results though, due to the segment's low incidence in terms of revenues. The management has expressed a willingness to increase the share obtained through fixed contracts. This would allow a stabilization of economic results, while retaining the ability to obtain higher remuneration in the event of electricity prices growth.

Assets under construction: although the business unit is quite small, it is at the center of Ormat expansion plans, which aims to install 355MW between 2024 and 2025, requiring a significant financial commitment.

Geothermal plants require significant upfront financing relative to their production capacity, as it is not possible to scale up by extending the size of the plant. Moreover, geothermal plants currently developed cannot by nature reach capacities above 50 MW, reducing the possibility of implementing such technology on a large scale. These two problems, on the other hand, are negligible for both photovoltaic and win power plants.

ORA, like most companies in the industry, is highly affected by the interest rate environment. That is because high interest rates, in addition to rising interest expenses, also increase the discount rates of cash flows. The latter, although contractually settled, are received over a considerable period and in some cases are not indexed to inflation.

The Product segment has highly dilutive effects on the company's operating margins and is characterized by high turnover volatility by operating on a commission basis.

Ora is exposed to developing economies. In particular, about 38.5% of revenues were achieved in Kenya, Indonesia, Guatemala, Honduras, and New Zealand.

Ormat is one of the world's leading producers of electricity through geothermal plants and has strong verticalization in the industry, particularly in binary cycle plants.

Future developments of Enhanced Geothermal Systems, a new type of geothermal plant still in the experimental stage, would allow the construction of plants up to 100MW, increasing the affordability of geothermal plants.

Finally, Geothermal is a renewable energy source with a very constant output that can guarantee the production of baseload power, thus being able to provide continuous service to the power grid. This is also possible through batteries and nuclear energy, whereas solar and wind are too volatile sources to ensure continuous service at all times.

seekingalpha.com and Author's Analysis

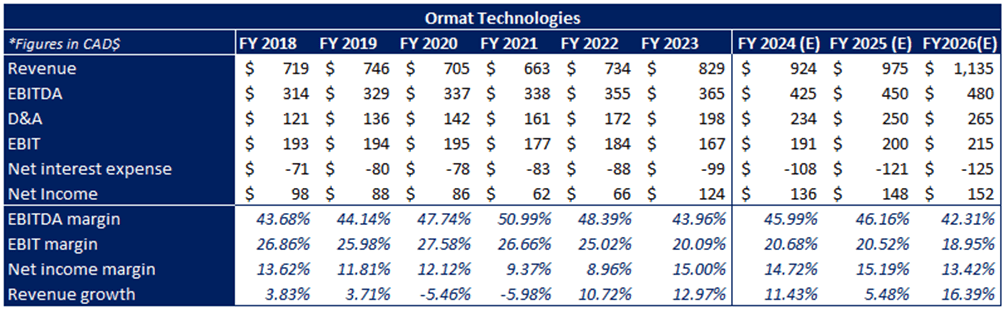

Ormat revenues increased 13% YoY to $829m in FY23, mainly because of new installations and the end of maintenance work at some plants. Such investments have been financed through debt for $1B, stock issuance for $682m and operating cash flows, which was equal to $309m in FY23. They also enabled the reduction of operating costs, with EBITDA and Net Income margin reaching 44% and 15% respectively. I expect further revenue growth in the next 3 years, thanks to the acquisition of ENEL's assets, the installation of new plants as well as increased revenues in the Product segment. Moreover, I believe margins will be in line with FY23, positively impacted by improving marginality in both Products and Energy Storage.

seekingalpha.com and Author's Analysis

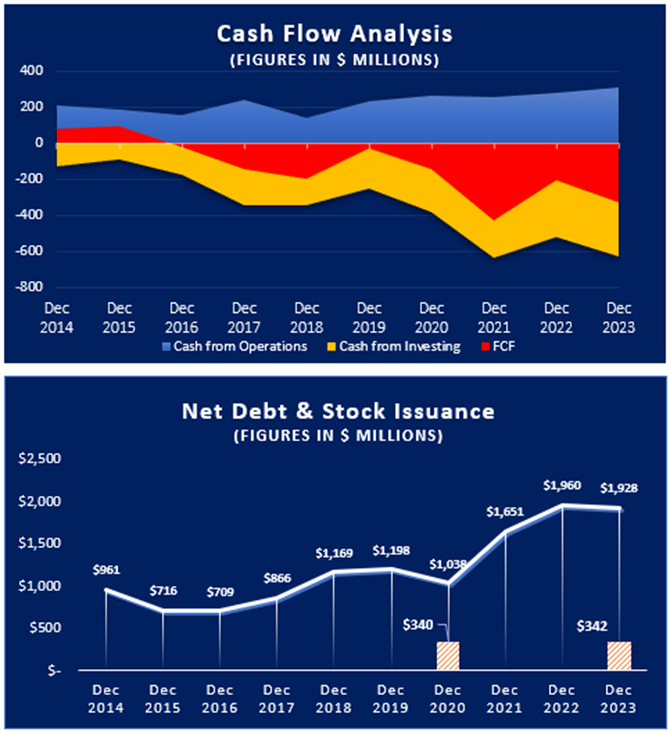

As can be seen in the above charts, ORA had always achieved negative Free Cash Flow between FY16 and FY23, especially since FY20 when the new plant construction campaign intensified. The data highlights how Ormat was not able to produce positive FCF even in years of lower growth and investment.

High capital requirements have almost doubled net debt, $1.9B on Dec 23 vs $1.0B on Dec 20, with a Net Debt/EBITDA ratio reaching 4.5x, further covered by $3.8B in PP&E. Between 2024 and 2026, the implementation of the business plan will still require a significant amount of capital, which will be added partly through additional debt as was the case with the ENEL acquisition, and partly through future possible capital increases, which have been employed several times in past years.

The Inflation Reduction Act provides an excellent opportunity to finance some of the needed liquidity through tax equity financing as geothermal power plants generate tax credits in the form of PTCs and storage systems in the form of ITCs. The company expects indeed to raise $145m from tax equity partners in FY24. Tax credits will be a key factor that will allow ORA to achieve higher margins in the coming years than the historical average, leading to lower cost of financing and easier capital raising.

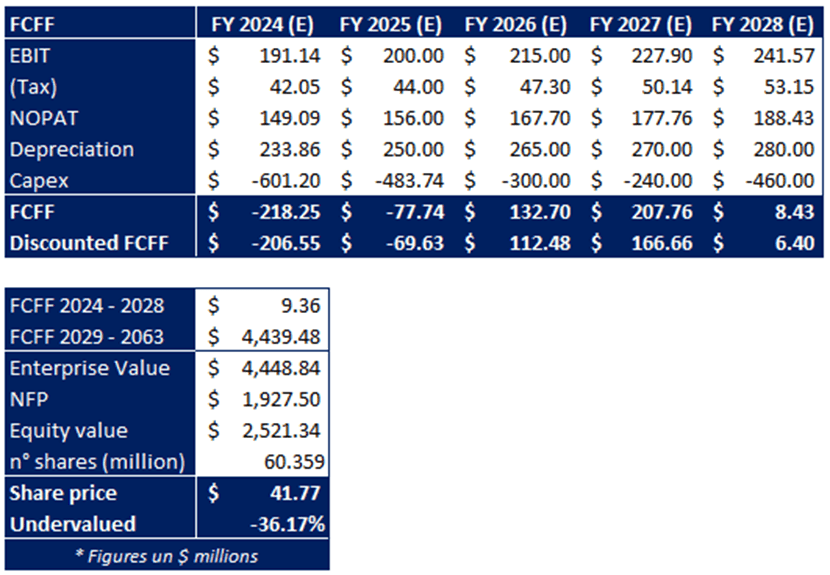

To have a further view of the valuation of the company, I carried out a Discounted Cash Flow analysis using the following assumptions:

The model is a two-stage DCF, with the first stage being composed of expected FCF up to FY28, whereas the second one accounts for the discounted cash flows going from FY29 and FY63. Please note that the second stage is 10 years longer than the one I used in my previous analyses, to consider the greater residual life of geothermal plants compared with solar and wind plants.

Beta equal to 0.47x, sourced from Yahoo Finance.

MRP (7.47%) and Risk-Free rate (5.94%) were obtained using Fernandez's FY23 data, weighted by the geographic breakdown of the company's revenues. The cost of equity obtained is 6.66%. ORA has higher numbers than the competitors analyzed in previous articles because of its greater exposure in developing countries such as Kenya and Indonesia.

Cost of debt (4.66%) was obtained from the ratio of interest expenditure to Ormat's total debt as of December 2023.

WACC = 5.67%.

The model returns a value of $41.77 a share, about 38% lower than the current market price. This is consistent with my bear expectations, as FY24E EV/EBITDA of 13.8x and FY24E P/E of 29x are multiples too high compared with the companies analyzed in the sector in previous articles.

Author's analysis and expectations

Overall, I currently rate Ormat Technologies as a Hold. I am pleasantly impressed by the company's well vertically integrated organization, a factor that could be a great asset in the future, especially if geothermal technologies would evolve further. ORA seems to have, at least for the time being, debt under control, largely covered by tangible assets, despite the heavy expansion investments initiated by the company in FY20. The improvement in financial performance during FY23 is expected to continue, boosted by the tax credits introduced by the IRA. However, I believe the stock is currently too expensive, about 30-40% above fair price. In addition, the dividend of 0.79% appears far more modest than that returned by other IPPs, underscoring concerns about the company's operating cash generation.