The best photo for all/iStock via Getty Images

The best photo for all/iStock via Getty Images

OptimizeRx Corporation (NASDAQ:OPRX) is on a path of exponential topline growth which is driving the valuation multiples to the lowest levels in the company's history. However, the market is not reacting much to the recently announced stellar guidance and we believe there is an opportunity to capitalize on a possible valuation re-rate in 2024. Based on peers' valuations and the software sector median multiples, OPRX may be undervalued by some 30%.

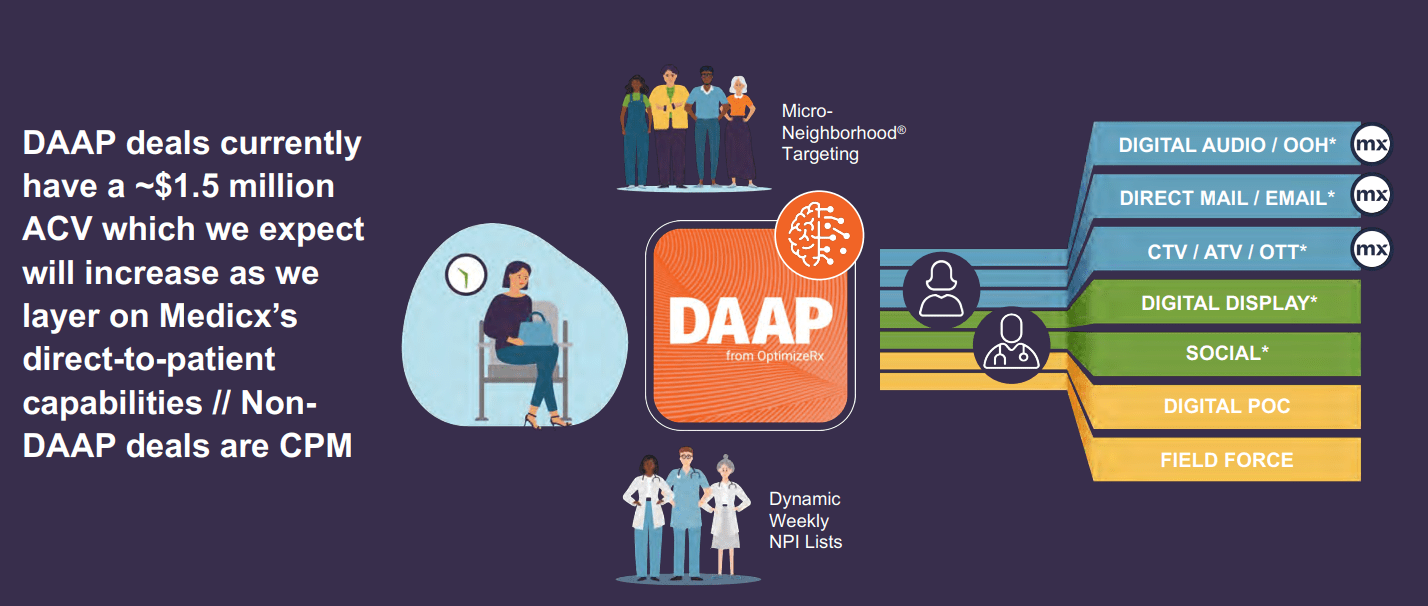

OptimizeRx, as the name suggests, provides a platform to improve the reach of drug distributors to reach the largest number of physicians (and patients) as possible. To do so, they employ advanced AI-based and direct messaging technologies that are merged with highly efficient targeting strategies. All their offerings are integrated into a single suite called Dynamic Audience Activation Platform, or DAAP. Their two main services are (1) patient discovery, and (2) script optimization and improvement. Basically OPRX sources customers and then focuses on driving script growth organically by increasing the awareness of specific brands over others.

DAAP Overview (Latest Corporate Presentation)

The strength of their suite is the integration of various channels and services, which provide valuable synergies in data collection and distribution. Right now, the average contract value for their deals is around $1.5 million, which is expected to increase as a result of cross-selling to existing customers as they appreciate the results of the DAAP platform.

KPIs (Latest Corporate Presentation)

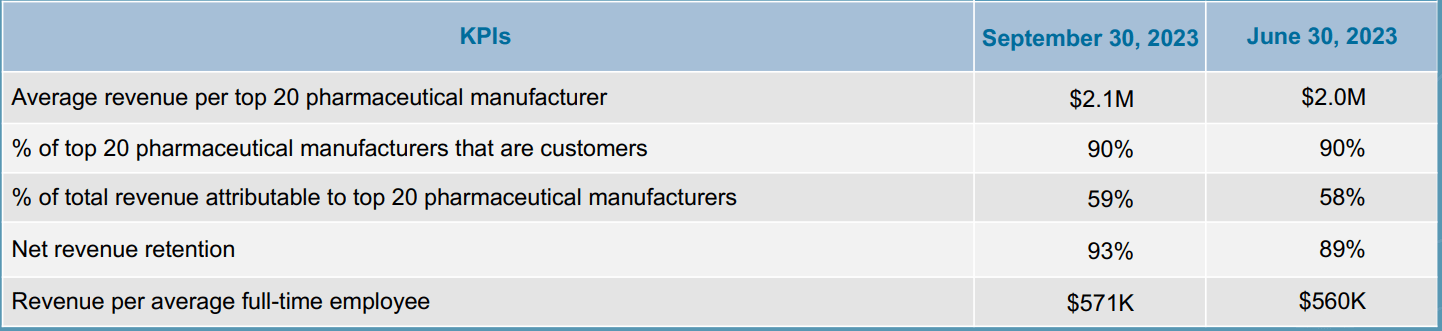

The KPIs also provide some useful insights. OPRX has been able to capture a 90% coverage of top pharma manufacturers, and 60% of its revenue is coming from these clients. We believe this is a strong signal of confidence, and shows that the largest players in the industry are appreciating the high ROI offered by this software. Another important point is revenue retention, which stands at 93% and growing QoQ.

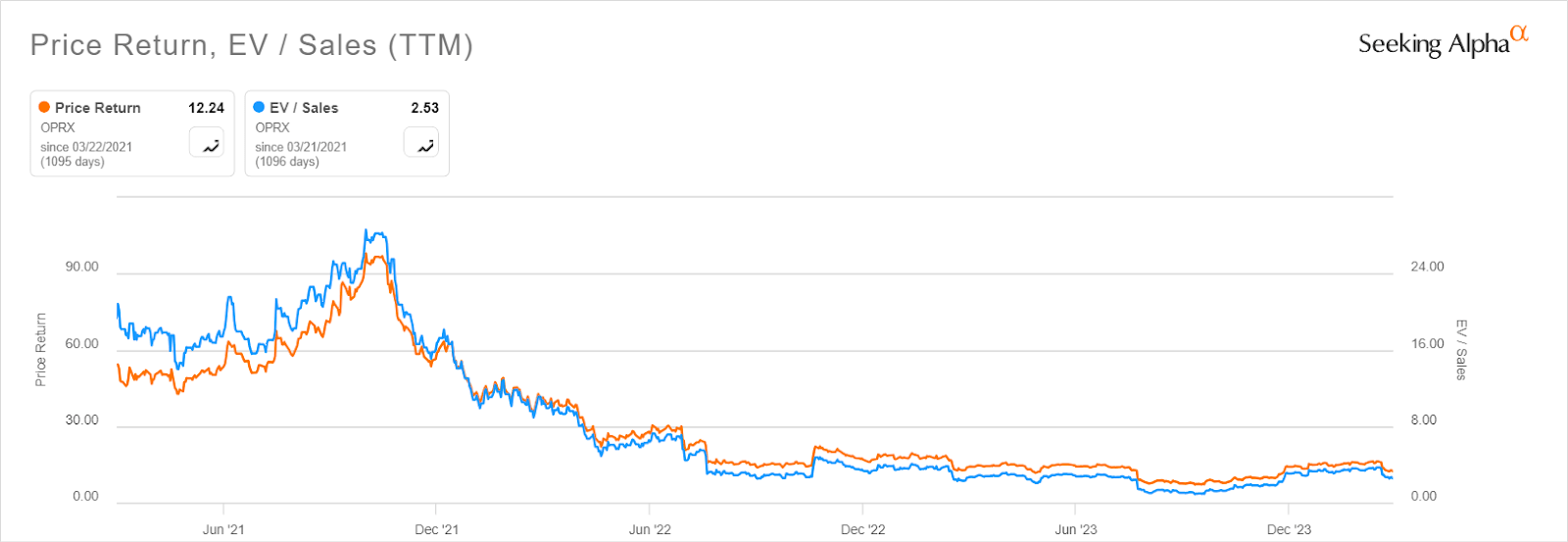

OptimizeRx's past performance is very similar to many other software companies. They had stellar valuations in the 2020-2021 period, trading well above 20x times revenues. However, revenue growth has been relatively steady between 2021 and 2022, which later contributed to the aggressive valuation re-rate post 2021.

Price Return and Valuation (Seeking Alpha)

After trading as high as $90 per share and 25 times revenues, the stock is now at $12 and EV/Sales at 2.5, practically decimated. But all this happened while financials were actually improving, and the company is now starting to deliver on its previous forecasts.

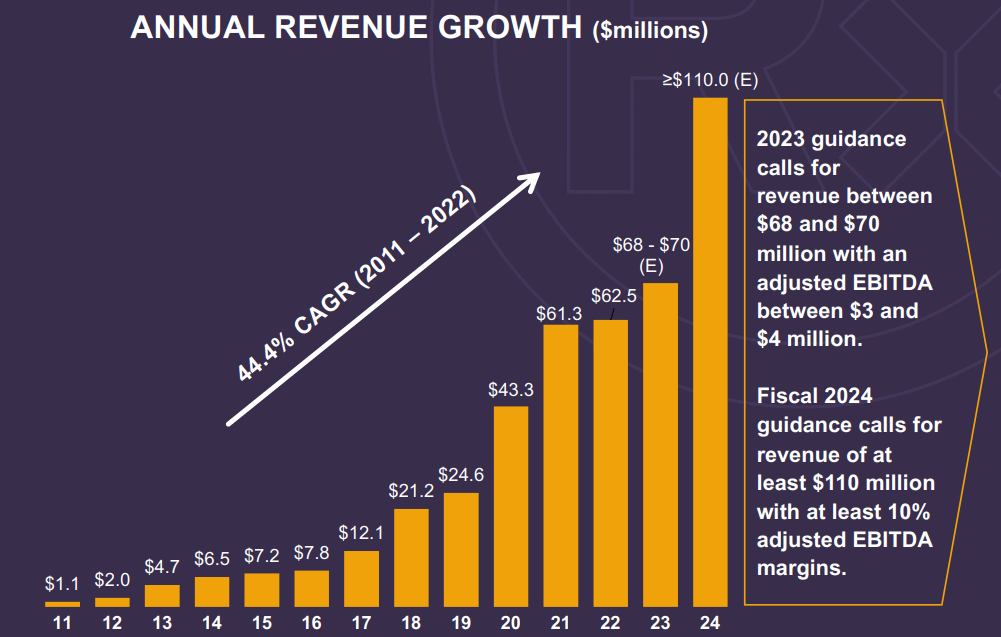

Annual Growth (Latest Corporate Presentation)

This is revenue growth over the last 13 years, including the guidance for 2024. Notice that the growth is not linear, but is concentrated in some years where new contracts are signed or existing customers increase the size of existing agreements. However, for 2024 it is different. The large revenue jump is expected as a result of the $95 million acquisition of Medicx, which closed in Q4 2023. Medicx is an omnichannel marketing and analytics provider focused on the customer side. For this reason, we believe there are likely several data-related synergies to be implemented which could boost topline growth and improve the offerings (and marketing ROI) to existing customers. Assuming a $75 million contribution from standalone OPRX, it means that Medicx is being acquired at around 3x times revenues, which is below the sector median of 3.6x. The acquisition is being funded by a $40 million credit line and existing cash. The Pro-forma entity should have around $12 million in cash per the company communications.

When a company makes an acquisition of roughly half of its own size, many things can go wrong. While we are not discussing Bayer and Monsanto here, there are still potentially harmful integration risks to watch out for in this acquisition. Additionally, the former president of the acquired company took the role of Chief Commercial Officer at the new pro-forma company. Differences in views and strategies could likely generate conflicts within the C-suite which would be negative for shareholders. However, we expect the overall outcome to be positive. Both teams have plenty of professional experience and so are expected to deliver efficiency on this deal.

Another source of risk is competition. This is a fast-growing sector that is undergoing fast development, and new competitors may arise with disruptive technologies that steal market share from companies like OPRX. The good news is that like many other software companies, customer loyalty is usually very high given high transition costs.

We believe that the pro-forma company arising from this acquisition will be severely undervalued in the current market environment. There are indeed several opportunities to grow the topline organically which arise from the quality of the data set that OPRX will have after this deal.

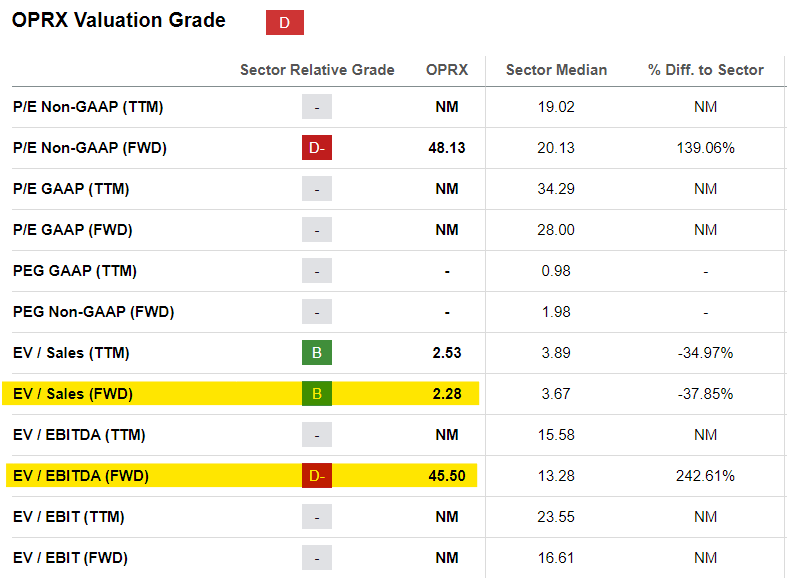

Valuation - Sector (Seeking Alpha)

Right now after a first look, OPRX might seem expensive relative to the sector. The forward EV/EBITDA stands at around 45x times, much greater than the 13x times of its sector. However, this number fails to take into account the new guidance, and the new capital structure post-acquisition.

Management is expecting "at least 10%" Adjusted EBITDA margin on at least $110 million in revenues. This means a baseline EBITDA of $11 million, along with some room for upside potential. The pro-forma net debt would be around $30 million - $40 million credit line less the $12 million in cash. Overall, this translates into a forward EV/EBITDA of 22x, which is less than half of the initial first figure. However, it is still looking expensive on a sector-wise basis.

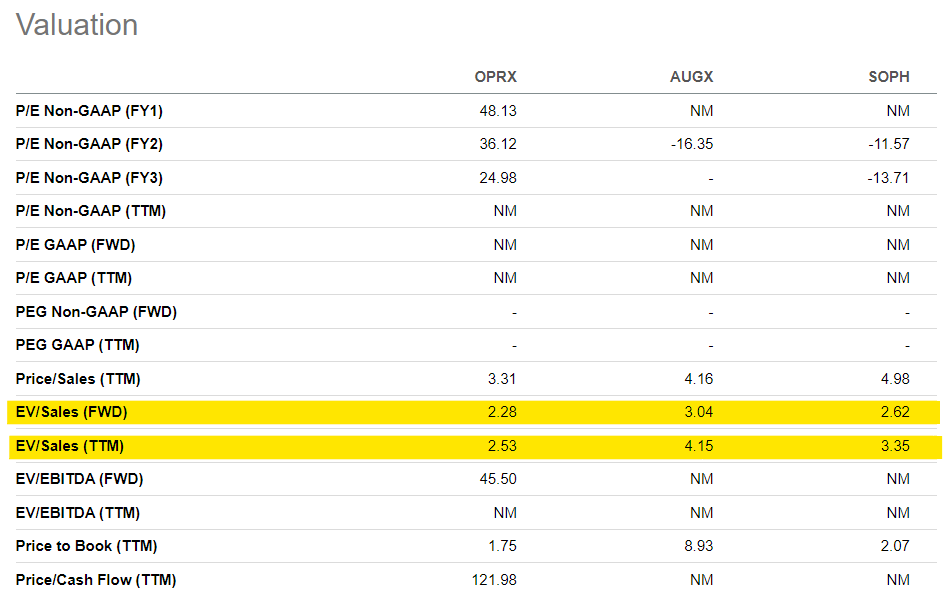

However, this comparison is misleading for one main reason: the sector as a whole has not been growing at a 27% CAGR for the past 5 years like OPRX did. So we need to adjust for this superior performance, and we will do so by running a closer comparison with 2 similar companies. However, we do so using an EV/Sales multiple as the majority of these companies have still negative EBITDA.

Valuation - Peers (Seeking Alpha)

We immediately see that in this group OPRX is an outlier in terms of its cheapness, and the closest competitor - Augmedix, Inc. (AUGX) - is at around 50% higher valuation while achieving more or less the same growth rate. For this reason, we believe that a re-rate towards the average between the two competitors - 2.8x EV/Sales - is possible throughout 2024. At that multiple, the stock would trade at around $16, implying an upside potential of 30% from the current price.

OptimizeRx is a fast-growing industry disruptor that is bringing cutting-edge technologies to the forefront of patient targeting in the healthcare business. They have built a strong product, proved by revenue retention KPIs and topline growth. After their latest acquisition, the market failed to properly value the pro-forma company, and we expect an upside potential of around 30% from a valuation re-rate in 2024.