urbazon/E+ via Getty Images

urbazon/E+ via Getty Images

OppFi (NYSE:OPFI) is a company developing a digital finance platform enabling banks to provide better access to credits for the underbanked segments in the US.

Share performance has been relatively weak since going public in November 2020 at the price of $9.9 per share. It was trading sideways the following year, before trending lower to a $2 price level for most of 2022. Despite seeing a 1-year high of $5, the stock is now trading at $2.6 upon a correction.

I initiate my coverage with a neutral rating. My 1-year price target of $2.6 presents an 8% upside from $2.4 today.

YCharts

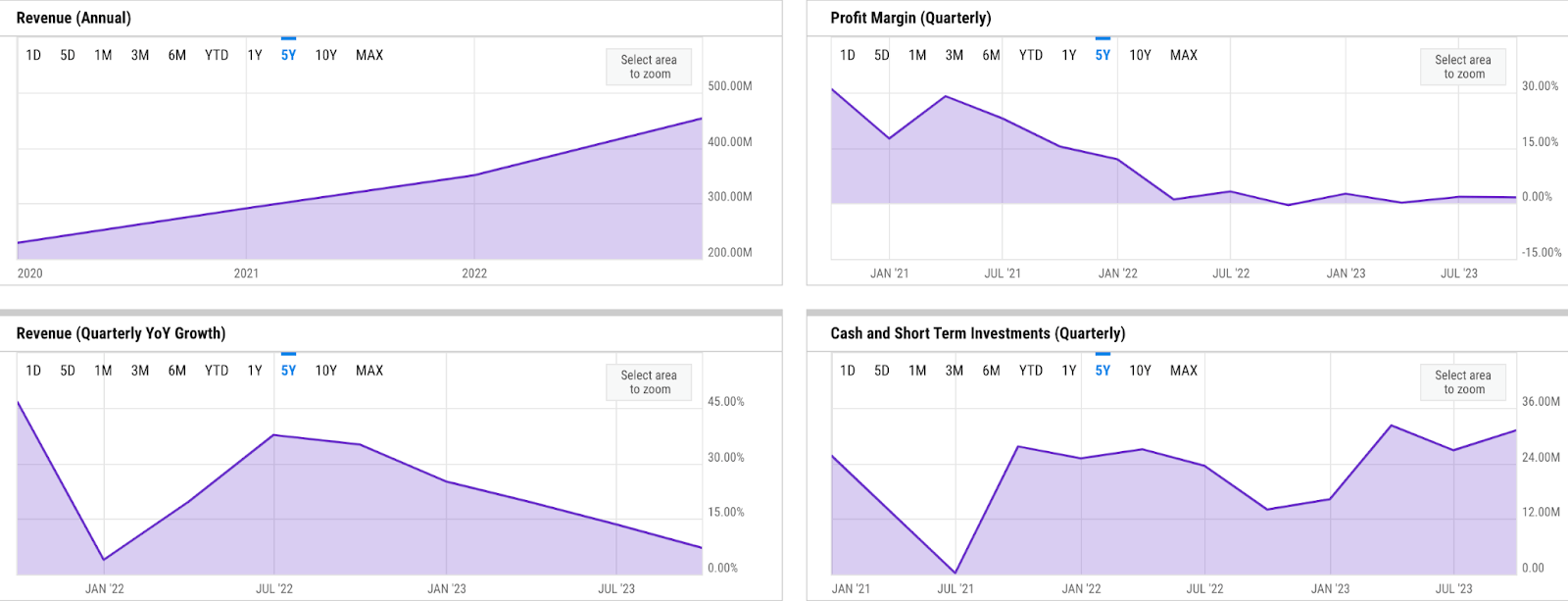

OPFI's fundamentals are relatively decent. Annual growth has declined from 20% level to around 10% as of FY 2023. In FY 2023, OPFI finished the year with $509 million of revenue, a 12% YoY growth. However, the slowdown in growth is compensated with stronger bottom-line performance. Though still far away from the double-digit level during pre-pandemic, net margin saw a considerable improvement in FY 2023. In FY 2023, OPFI saw net margin expanding from 2% in the last FY to around 7.6%, which is a similar outlook to 2021.

The profitability improvement seems to also translate to better adjusted EBITDA/aEBITDA, which has made a positive impact on liquidity. aEBITDA more than doubled to $114.7 million in FY 2023. Cash and short-term investments, which have been mostly situated around $25 million - $30 million as of late, saw an increase to $73.9 million in FY 2023, about 48% YoY growth.

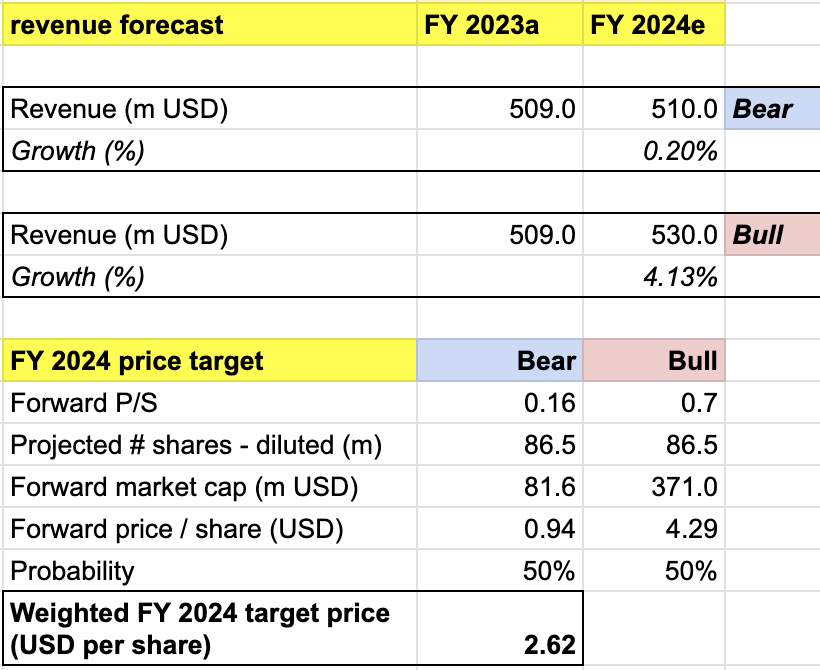

In FY 2024, OPFI expects to maintain its bottom-line strength while seeing slower growth. As per its guidance, OPFI will aim to deliver $510 million - $530 million of revenues. At such a level, OPFI will expect a 0.2% - 4.1% YoY growth, meaning that growth should further slowdown YoY or even be flat in the worst-case scenario. Nonetheless, OPFI would expect to see $46 million - $49 million of adjusted net income, which is a 10% growth on average.

As commented by the management in the Q4 earnings call, the main culprit for the potential slowdown is the expectation of persisting macro challenges into 2024. In light of that, I think that the management's focus on profitable growth is a decision that would make sense at this time. Though a rebound appears unlikely, I see some positive initiatives that could serve as potential catalysts for OPFI to deliver within the context of profitable growth in 2024.

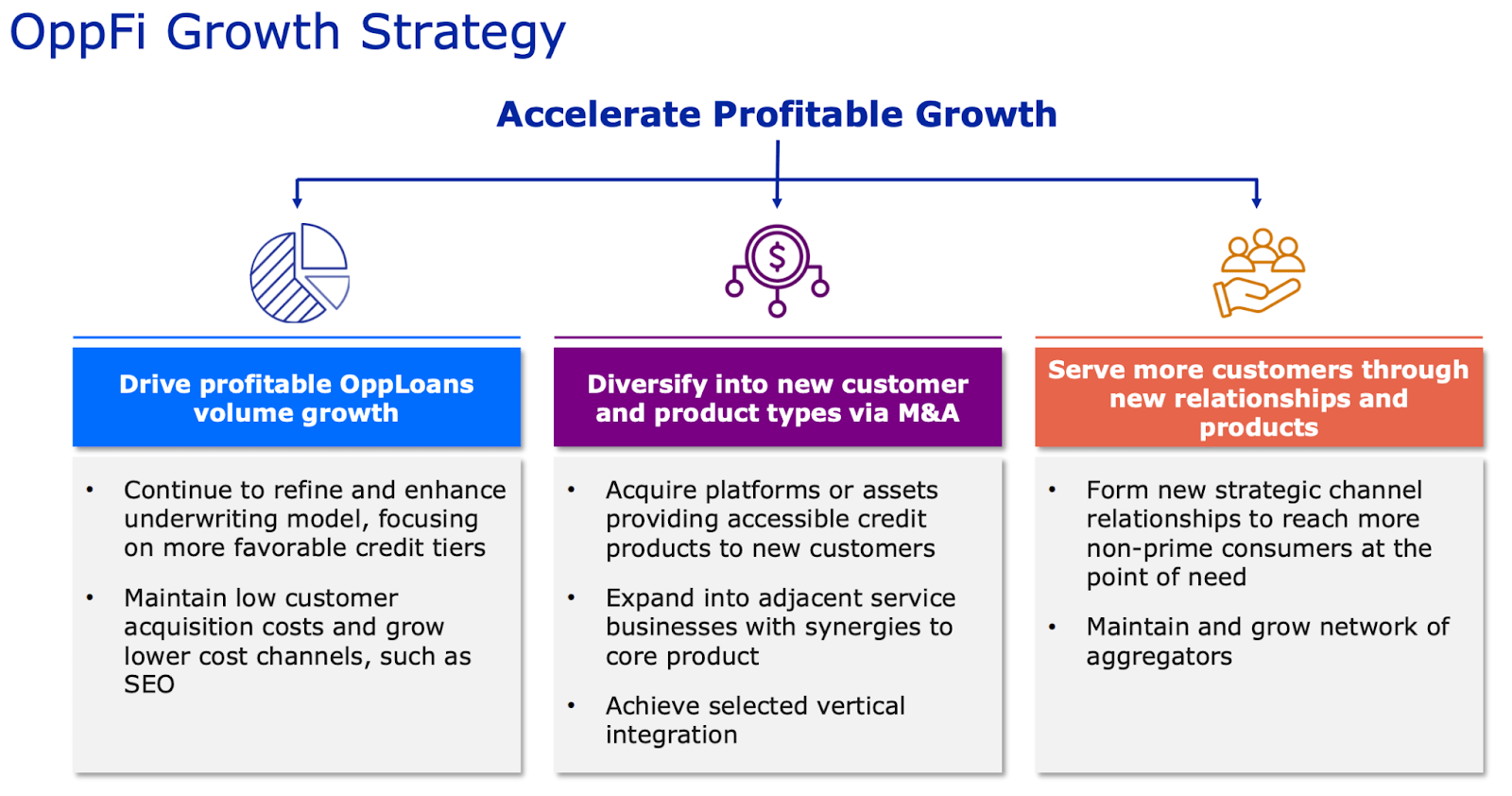

First off, I believe the geographic expansion of bank partners into new states could more or less serve as medium to long-term catalysts for OPFI. Bank partnership has been a key go-to-market strategy for OPFI. Under such a model, OPFI leverages its technology to assess the creditworthiness of borrowers before referring them to its banking partners, who would then originate loans. I believe that there is room for upside here for state expansions since OPFI's loan portfolio generation still seems to be concentrated within most Florida and Texas as of late.

OPFI presentation

Today, bank partners are playing an even more important role in driving revenue growth. Since going public, the share of net originations by banking partners has increased considerably from merely 90% in 2021 to 100% as of Q4 2023. In my opinion, this means that OPFI is now pretty much operating as a tech-enabled referral channel for traditional banks.

Furthermore, I also believe that the launch of new credit-scoring algorithm in Q2 2024 should help support OPFI's recent shift towards 100% bank partnership model:

In conjunction with the banks that partner with us, a new credit model is expected to be launched in Q2 that will incorporate an updated dynamic risk model intended to drive lower risk origination volume and reduce credit losses.

Source: Q3 earnings call.

OPFI presentation

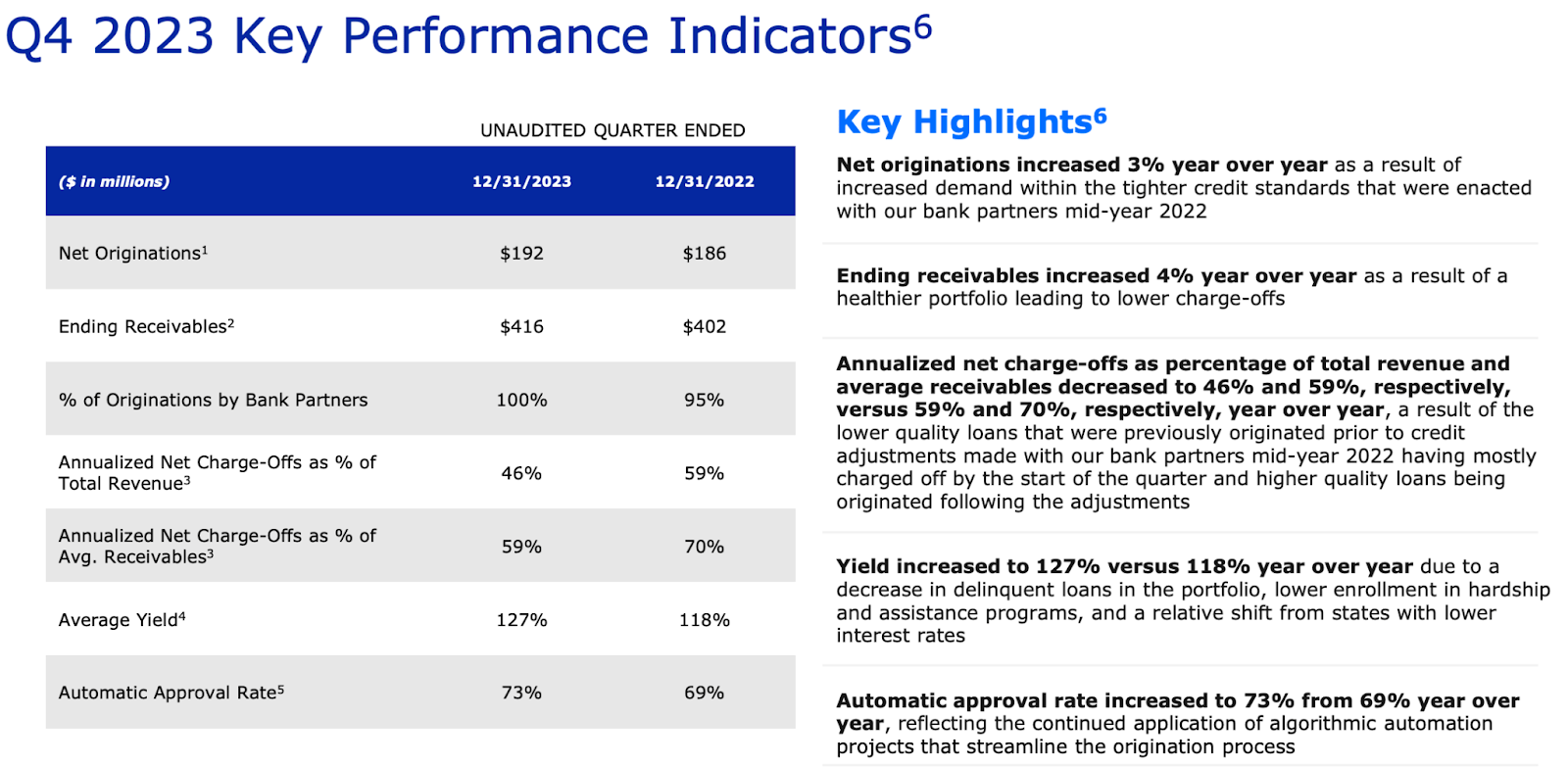

I believe the launch of a new credit model here is also aligned with OPFI's overall profitable growth strategy, especially as it relates to the focus on higher-quality credits. The new credit model should eventually help profitable growth by enhancing OPFI's loan economics. As of the latest quarter alone, I have noticed how loan economics have already improved across the board even with the current technology. For instance, the automatic approval rate significantly increased to 73% from 69%, while the average yield also increased to 127%, already demonstrating the promise of the current technology.

Overall, I believe risk remains moderate to high. Aside from the persisting macro challenges, I view a relatively high partnership concentration as a key risk to my thesis.

As of today, inflation remains high in the US, which could prompt the Fed to reconsider rate cuts in 2024. While the high-interest rate assumption seems to have been baked into OPFI's forecast, I am not entirely sure to what extent it has:

We expect the economy in 2024 to be similar to how it was in 2023, with sticky inflation and interest rates higher than historic norms. As we have communicated during the past couple of years, persistent above normal inflation hurts customers more than recessions do, because they have more difficulty budgeting for everyday expenses, especially when living paycheck to paycheck with limited to no savings.

Source: Q4 earnings call.

Furthermore, I think that the high interest rate environment today may also pressure the market's interest in OPFI's stock. This means that OPFI may be unlikely to see upward price action in the near term during the temporary headwinds at present.

OPFI website

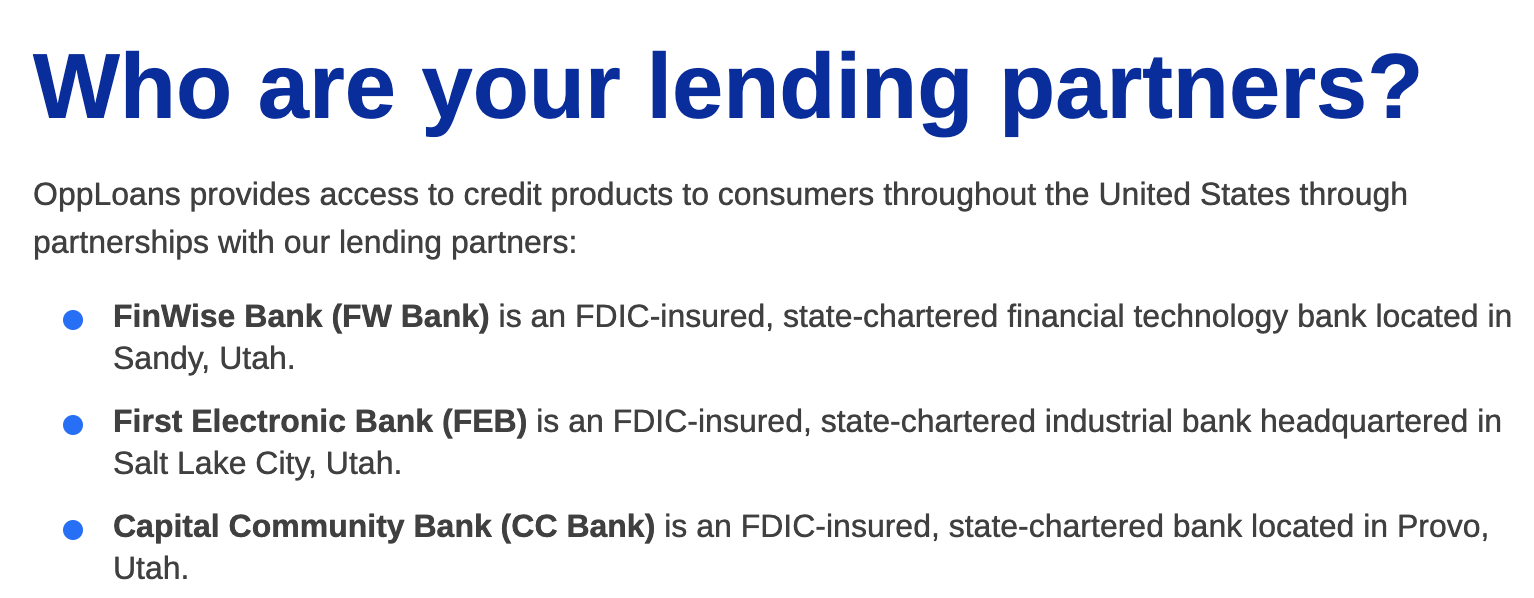

On the other hand, I believe the high bank partnership concentration should be a major risk factor today. As OPFI continues to shift into a 100% bank partnership model, its exposure to this risk factor is even higher. OPFI's bank partners are concentrated only within 3 state banks, which means that any potential shock to any of these banks, or agreement termination could meaningfully impact OPFI's revenue growth. For instance, even though OPFI has not yet disclosed its latest net origination contributions from these banks as of Q4 2023, its 2022 filing revealed that FinWise made up over 60% of net originations that FY.

My target price for OPFI is driven by the following assumptions for the bull vs bear scenarios of the FY 2024 projection:

Bull scenario (50% probability) assumptions - OPFI to achieve its FY 2024 revenue of $530 million, a 4.13% growth, at the high end of OPFI's guidance. I assign OPFI a forward P/S of 0.7x, which implies a share appreciation to $4.3, where the stock was trading towards the start of the year. Furthermore, the 0.7x also suggests a higher valuation premium as OPFI sees higher quality originations.

Bear scenario (50% probability) assumptions - OPFI to deliver FY 2024 revenue of $510 million, a 0.2% growth YoY. OPFI would finish the FY at the low-end range of its guidance. In this scenario, I would expect OPFI's P/S to remain at 0.16x, where it is trading today.

price target (own analysis)

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of $2.6 per share, presenting a potential upside of 8% from the current level. At this point, I would give the stock a neutral rating.

The challenging macro situation has impacted OPFI's business in recent times. This could continue in 2024, with the stock potentially experiencing sideways price action in the worst-case scenario. I consider the bank partner's geographic expansions and the launch of new credit-scoring technology, as potential medium to long-term catalysts. The fact that OPFI has shifted into a 100% bank partner origination model as per the most recent quarter may further solidify these catalysts, though there's also a downside to it. I rate the stock neutral.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.