Oleg Breslavtsev/Moment via Getty Images

Oleg Breslavtsev/Moment via Getty Images

On Holding AG (NYSE:ONON) is successfully expanding into new categories and experiencing robust growth in its core markets. The company operates in an attractive industry with significant barriers to entry and ample room for growth with its move of expansion into running. The company is still in an early period of its growth phase, and from here on, can continue to grow. The company’s robust new-product pipeline and greater economies of scale are key to driving market-share gains, while maximizing margin. The company is trading at a lower end of its valuation multiple over the past two years, and I believe as On continues to gain market share, the multiple will re-rate upwards from current levels. I assign a buy rating to the stock.

As On ventures into new sports, running will continue to be a primary driver of growth due to its dominant position in the athletic footwear market and its increasing popularity worldwide. While major sneaker brands like Nike, Adidas, and Puma compete to develop the fastest shoe for elite marathon runners and broaden their appeal in the running community, they have faced challenges in building lasting loyalty among everyday runners. In contrast, On has achieved significant success as one of the top three running brands in most of its core markets and with key retail partners over the past five years. With the imminent launch of two new speed-performance technologies and expansion into comprehensive athletic apparel offerings, On is well-positioned to capture additional market share.

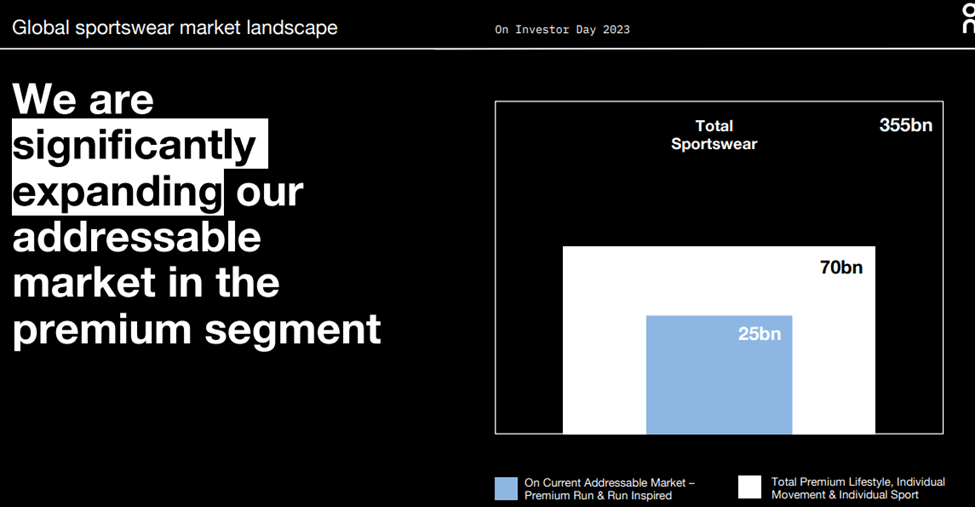

Despite its less than 1% of the global sportswear market share, and compared to competitors, lower brand awareness, the company has the potential to increase its visibility and market presence through initiatives such as event-driven engagement, wholesale partnerships, and collaboration with athletes. The company is expanding from running into tennis, outdoor & lifestyle with an increased focused on newer apparel offering which will further help expand its addressable market size. Even In the early stages of development, On is making significant progress in the global sports footwear market.

Company Presentation

China is a highly promising opportunity for geographic expansion for ONON. Many athleisure brands are looking to expand into China due to the growing middle class of the country, growing interest in sports, and the increased purchasing power of Chinese consumers. On can tap into a wider customer base if it invests to expand its presence in mainland China by opening their new stores along with larger retail formats. If the company enhances its omnichannel approach through leading digital platforms, it can increase its market share. Since On opened its first store in 2019, it has seen impressive triple-digit growth in China.

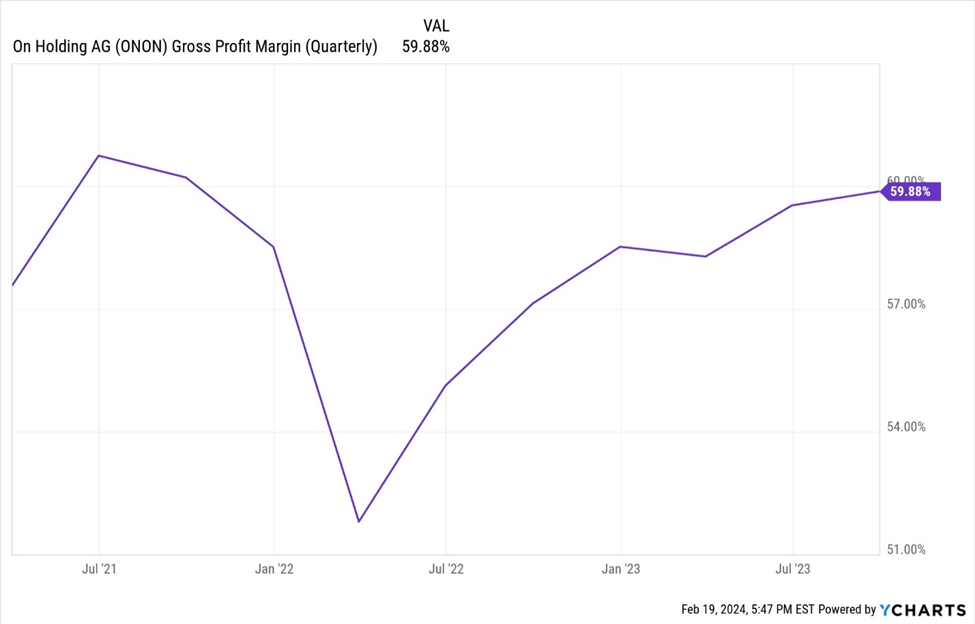

With just 1.6% share in the global sports-footwear market and even less in overall sportswear, On could increase sales at a high double digit compound annual growth rate over the next three years and achieve its goal to double the pace by 2026. Gains will be driven by direct-to-consumer expansion, scaling up in underpenetrated markets, such as China, and continued product innovations. On's gross margin of 59% could expand past the company’s goal of more than 60%, fueled by increased direct-to-consumer penetration and continued high full-price sell-through. Rising DTC penetration, bringing sourcing in-house and changes to free-trade agreements, has driven 580 bps of gross-margin expansion since 2019. With the latter two catalysts now complete, I believe that a rising DTC mix can help push toward its goal faster. Meanwhile, On’s premium positioning in performance footwear offers a layer of margin protection, as more innovative and high-priced products have strong full-price sell-through, limiting the need for discounting.

Ycharts

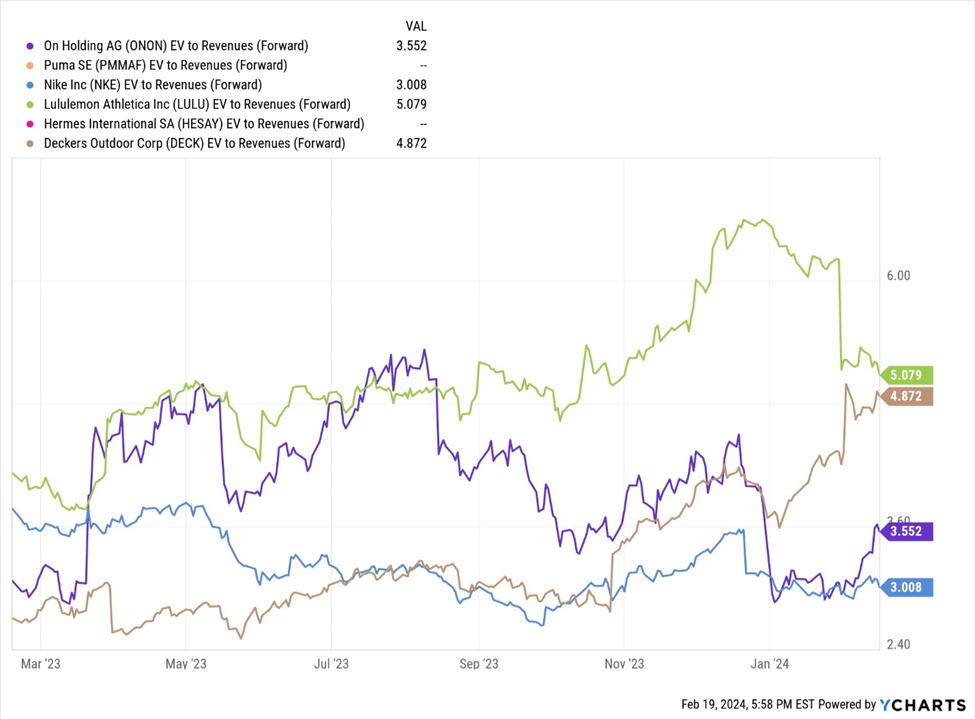

Compared to historical valuation multiples for future projections, current levels are approaching the lowest points observed over the past year. ONON's valuation multiple has been more or less around the premier global athletic brands, which I believe is justified given ONON's significantly stronger growth in both top and bottom lines. The current trading multiples for the shares stand at 3.5x EV/Sales, which is significantly lower than the company’s two-year average multiple of 6.2x as per Capital IQ. The company is positioned to grow at a high ~30% rate & as market share gains accelerate I think the multiple can re-rate upwards from current levels. I am bullish and assign a buy rating to the stock.

Ycharts

On faces some serious competition in the sportswear market as it is going head-to-head with big names like Nike, Adidas, Hoka, and Brooks. Employing a multi-channel distribution strategy, the company has 62% of sales coming from wholesale and the remaining 38% from retail. This setup brings in some complexities and risks that might limit upside in the stock. On's product line also carries a fashion risk. Its shoes, with many sharing a similar aesthetic, may find themselves vulnerable to shifts in fashion trends.

On Holding is in the initial phase of growth across a majority of its markets and product categories within the athletic footwear and apparel industry. The company operates in an attractive industry characterized by significant barriers to entry and promising growth opportunities fueled by trends in health and casualization. With upcoming launches of speed-performance technologies and expansion into athletic apparel, On is poised for further growth. The company is trading at a low multiple compared to its own multiple over the past two years, and I believe as the company continues to gain market share, the multiple will re-rate upwards from current levels. I assign a buy rating to the stock.