SweetBunFactory

SweetBunFactory

I discussed my ‘Strong Buy’ thesis for ON Semiconductor (NASDAQ:ON) in my previous coverage in June 2023, emphasizing their key strengths in carbide and electrification in the auto and industrial end-markets. I forecast the company will deliver double-digit revenue growth and explosive FCF growth over the next few years. I reiterate a ‘Strong Buy’ rating with a one-year target price of $150 per share.

In Q3 FY23, ON Semiconductor stock price took a hit when they revised down the full year guidance for silicon carbide (SiC) revenue from $1 billion to $800 million. One of their key Tier 1 customers was reducing their inventory levels caused by high-interest rate and softness in end-market demand. In Q4 FY23, ON Semiconductor finished the year with $800 million in revenue. The company is committed to growing their silicon carbide business at twice the rate of the market growth in FY24. I think the company's 2x market growth projection is quite realistic as the outperformance is aligned with their historical growth rate, and ON Semiconductor has the leading advantage in their 200 mm SiC wafer technology.

During the earnings call, their management projected the silicon carbide market to grow by 20%-30% in FY24, which is slower than the growth rate experienced in the past two years. While there is some softness in the EV market expected in FY24, I remain optimistic about ON Semiconductor’s long-term growth prospects for the following reasons.

In October 2023, ON Semiconductor announced that they completed the expansion of the world-largest silicon carbide fabrication facility in Bucheon, South Korea. The manufacturing facility is capable of producing more than 1 million 200 mm SiC wafers per year at full capacity. The wafer manufacturing facility enables ON Semiconductor to supply their advanced SiC chips over the next few years, offering tremendous competitive advantages over their major competitors. ON Semiconductor believes they own 25% of the global market share in SiC.

Infineon Technologies (OTCQX:IFNNY), one of the key competitors of ON Semiconductor, achieved €500 million in SiC revenue, as communicated in their earnings call. Infineon has signed a contract with SK siltron to produce 150 mm SiC wafers. Wolfspeed (WOLF) is ramping up their 200 mm productions for SiC, and they are quite confident in the robust demand for SiC during their latest earnings call. STMicroelectronics (STM) achieved €1.14 billion in SiC revenue in FY23, marking 60% YoY. All these SiC vendors have demonstrated strong growth momentum in the SiC businesses.

As highlighted in my previous coverage, ON Semiconductor possesses the competitive advantage with its diverse portfolio in both IGBT and SiC. The broad portfolios are suitable for auto OEMs to choose between traditional silicon materials, and the new silicon carbide. Moreover, it would be easier for auto OEMs to switch from one design to another with minimum switching costs.

In short, if ON Semiconductor achieves growth at 2x the rate of the market, I project their SiC revenue could potentially reach $1.2 billion in FY24, representing above 13% of group revenue as per my estimates.

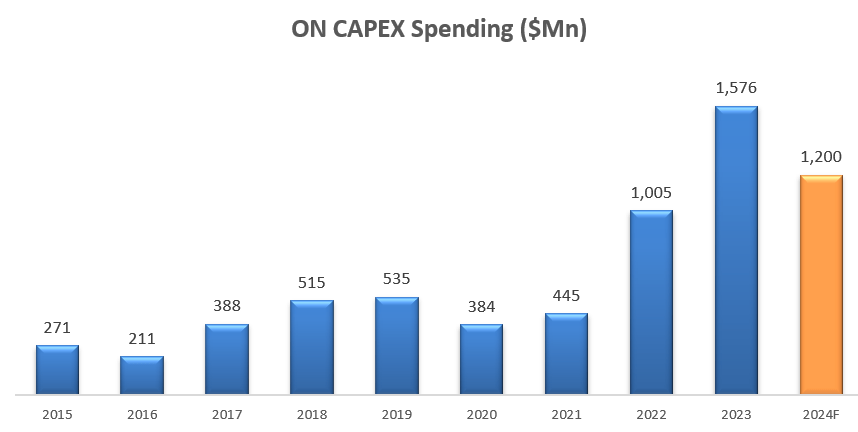

As ON Semiconductor has been building their SiC manufacturing and wafer facilities over the past two years, their CAPEX spending has surged from $445 million in FY21 to $1.57 billion in FY23, as depicted in the chart below.

ON Semiconductor 10Ks; Author's Estimate

During the earnings call, their management expressed that their heavy investment in SiC wafer manufacturing was nearing completion, and anticipated CAPEX to be in the low-teens percentage of total revenue in FY24. According to my calculation, their CAPEX spending will be around $1.2 billion in FY24, representing 13% of revenue.

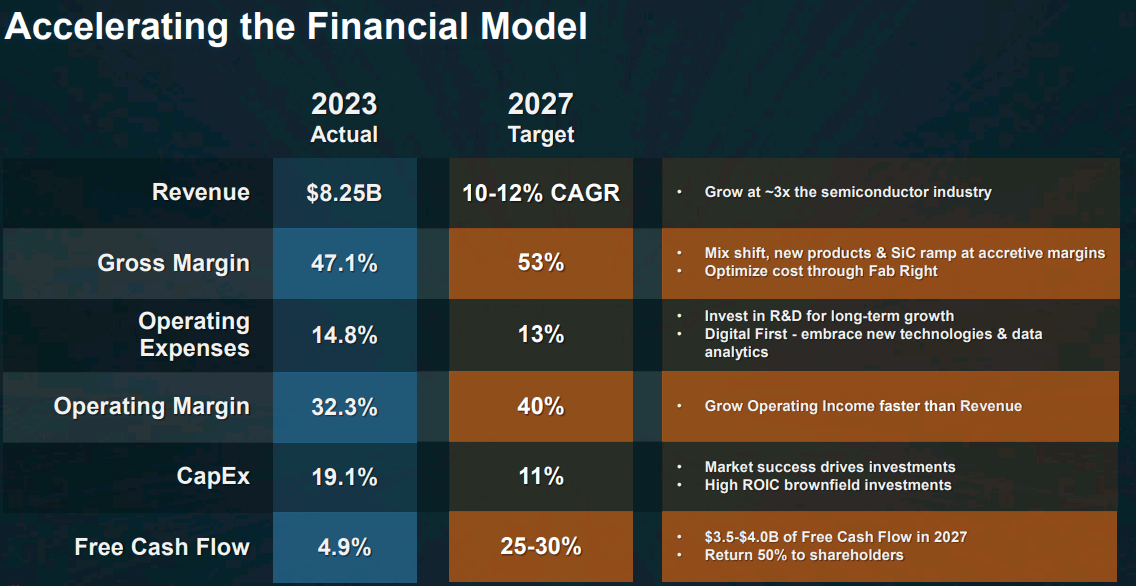

Furthermore, ON Semiconductor anticipates reducing their CAPEX to 11% of total revenue by FY27, alongside an expected increase in FCF margin to reach 25-30%. If the company can deliver on their long-term guidance, I expect significant FCF growth from $406 million in FY23 to more than $3 billion in FY27.

ON Semiconductor Investor Presentation

In Q4 FY23, ON Semiconductor delivered -4% revenue growth and -11.3% adj. operating profit growth. Automotive business grew by 13% year-over-year and Industrial was down 10% year-over-year.

ON Semiconductor Quarterly Results

It is quite understandable that industrial business experienced negative growth. The overall industrial production has been quite weak as consumers have reduced their consumption of physical goods in the post-pandemic era. In order to address the weak end-market demands, the overall manufacturing industry has been reducing their high inventory levels in 2023, resulting in a softening of manufacturing production.

For the full year, ON Semiconductor generated only $402 million in FCF, caused by high CAPEX spending and elevated inventory levels. They repurchased $564 million of own shares, an increase in amount from $260 million in FY22. I will discuss the inventory issue in the risk section. They ended with $2.5 billion in cash and $3.3 billion in debts, reflecting a robust balance sheet.

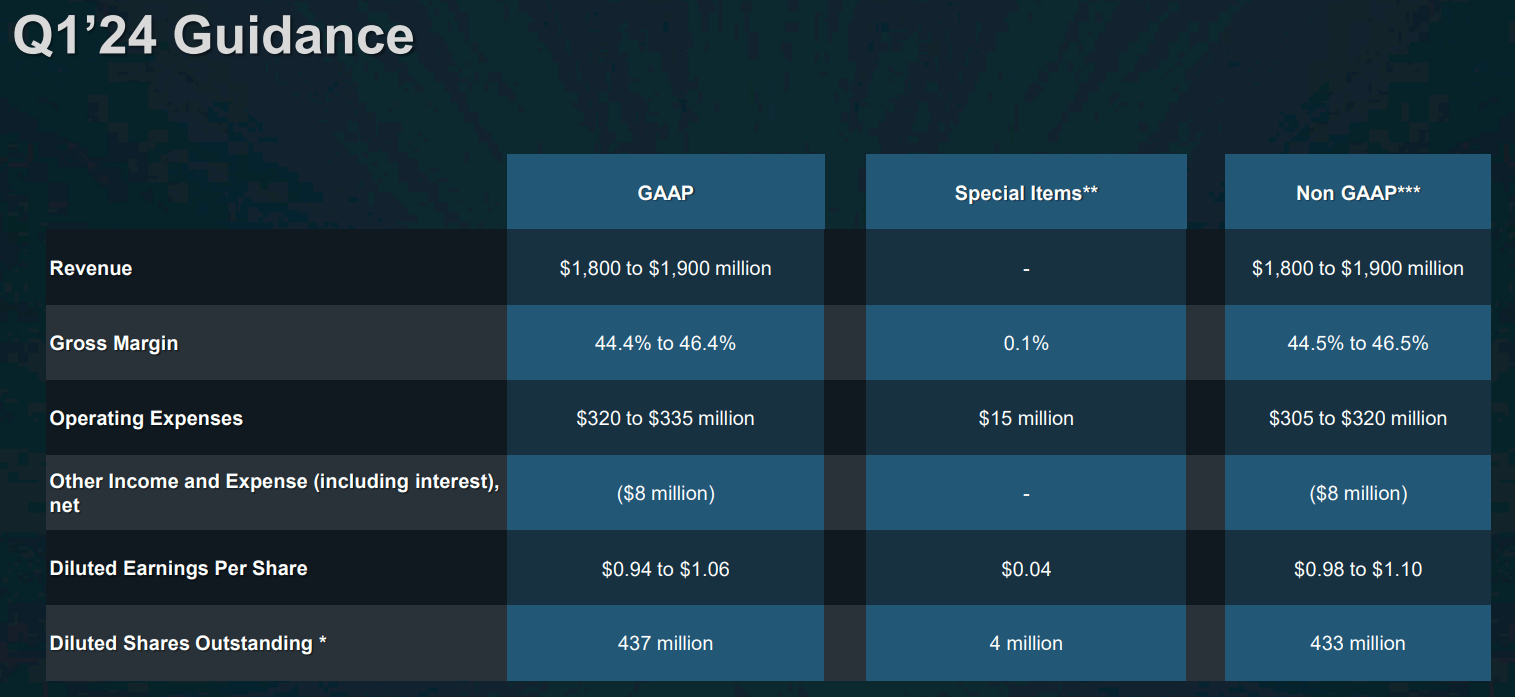

For Q1 FY24, ON Semiconductor is guiding approximately MSD decline in revenue, as shown in the slide below. The revenue guidance reflects the ongoing pressure from the weak Industrial market and the softness of automotive OEM demands.

ON Semiconductor Investor Presentation

For FY24, I am considering the following moving pieces for their business growth.

Adding together, I expect ON Semiconductor will deliver 7%-8% revenue growth in FY24, and it is highly likely that FY23 marked the bottom of the cycle for the company.

My model assumes 7% revenue growth for FY24, suggesting 4.8% growth contribution from SiC, 3.6% from Image Sensor, and some growth headwinds from remaining industrial businesses. For the normalized growth, I assume 10% topline growth, aligning with their historical average throughout cycles. As SiC is growing rapidly, it would represent around 15% of group revenue soon. Assuming SiC maintains its growth momentum, it could contribute 5%-7% to the group topline growth. If the rest portfolios only grow at MSD, ON Semiconductor could achieve at least 10% year-over-year growth. It is worth nothing that, to be conservative, my estimation is at the lower end of their midterm guidance of 10%-12%.

ON's gross margin expansion is primarily influenced by the utilization rate. As disclosed in the latest conference, their gross margin was only 30% when the company was running at 65% utilization rate in FY20. Now they are standing at around 40% gross margin, with an anticipated long-term target of 53% gross margin. It is understandable that it would take several quarters for a new fab to ramp up its production, and ON Semiconductor has built several wafer facilities over the past few years, which has affected their utilization rate. As discussed previously, ON Semiconductor’s heavy investment cycle appears to have peaked in FY23; therefore, I anticipate their utilization rate starts to improve in FY24.

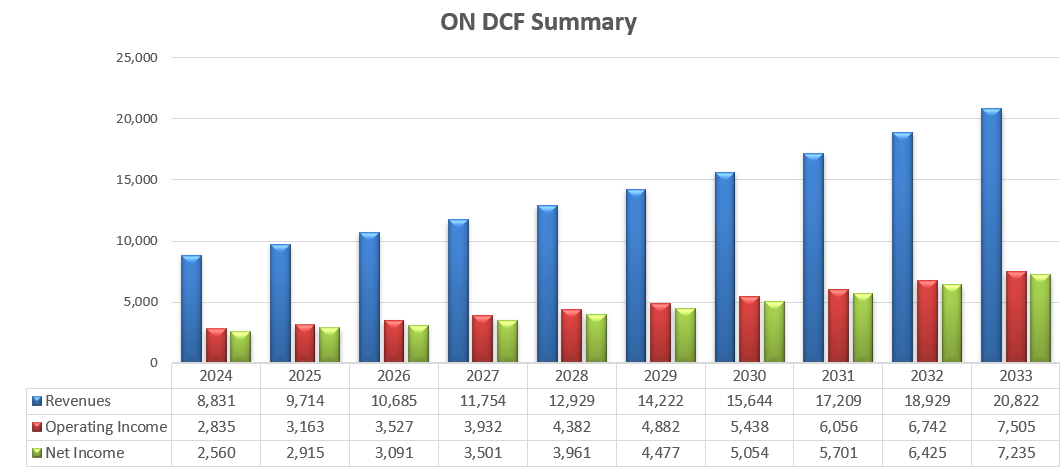

In terms of margin, another factor to consider is their low-margin business exits. They divested $180 million of non-core/low-margin businesses in FY23. These business exits could create margin tailwinds for the near future. Considering all these factors, I calculate their operating expenses will grow by 9.3% annually, leading to 40-50bps margin expansion. The chart below exhibits the projected revenue, operating income and profits over the next 10 years.

ON Semiconductor DCF - Author's Calculations

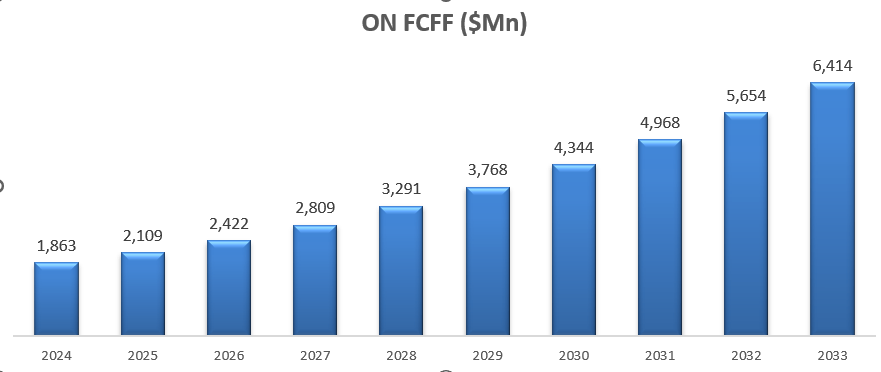

The second step is to calculate the total enterprise value: the present value of all the future free cash flow of the firm (FCFF) as shown in the chart below. I estimate a fair EV of $63.6 billion, and a one-year target price is calculated to be $150 per share after adjusting for net cash position of $1.1 billion. The current stock price is only trading at 16x forward FCF, a quite cheap multiple in my view.

ON Semiconductor DCF - Author's Calculations

ON Semiconductor experienced $495 million of cash outflow from inventory in FY23, causing -$863 million change in working capital for their operating cash flow. The current elevated inventory level was caused by their 74 days of bridge inventory to support their fab transition in the SiC ramp up process, as communicated during the earnings call. Their management estimated that their base inventory decreased by $52 million sequentially, excluding the SiC ramp up inventories.

Additionally, ON Semiconductor is operating in a quite volatile market environment, with their key end-markets such as auto and industrials being highly cyclical. Their growth is subject to the business cycles of these key-end markets. Therefore, investors should have a higher risk tolerance to withstand the volatility of their earnings, as well as stock price.

For SiC, STMicroelectronics has a big ambition to grow the business towards $2 billion in revenue by FY25. In FY23, according to their management, they won 160 projects spread across 100 customers, which serves as a strong indication for their future SiC growth. It is quite important to monitor ON Semiconductor’s key competitors, such as STMicroelectronics and Infineon Technologies. Investors should monitor these companies' 200mm and 150mm wafer capacity and utilization rate, customer wins, as well as their SiC revenue growth rates, as these factors could assess ON Semiconductor’s competitive advantages in SiC market.

I anticipate their SiC revenue will cross $1 billion mark in FY24, and with the completion of the wafer facilities build-up, their FCF is expected to experience explosive growth over the next few years. The stock price is significantly undervalued in my view, and I reiterate ‘Strong Buy’ rating with a one-year target price of $150 per share.