swissmediavision/E+ via Getty Images

swissmediavision/E+ via Getty Images

It's no overstatement to say that I have written bunches of articles on Omeros (NASDAQ:OMER) since 03/2018's "Omeros: Beauty And The Beast". The year 2023 was a rare exception, with no Omeros article. I am setting things right for 2024 dusting off my keyboard to report Omeros' current investment merits.

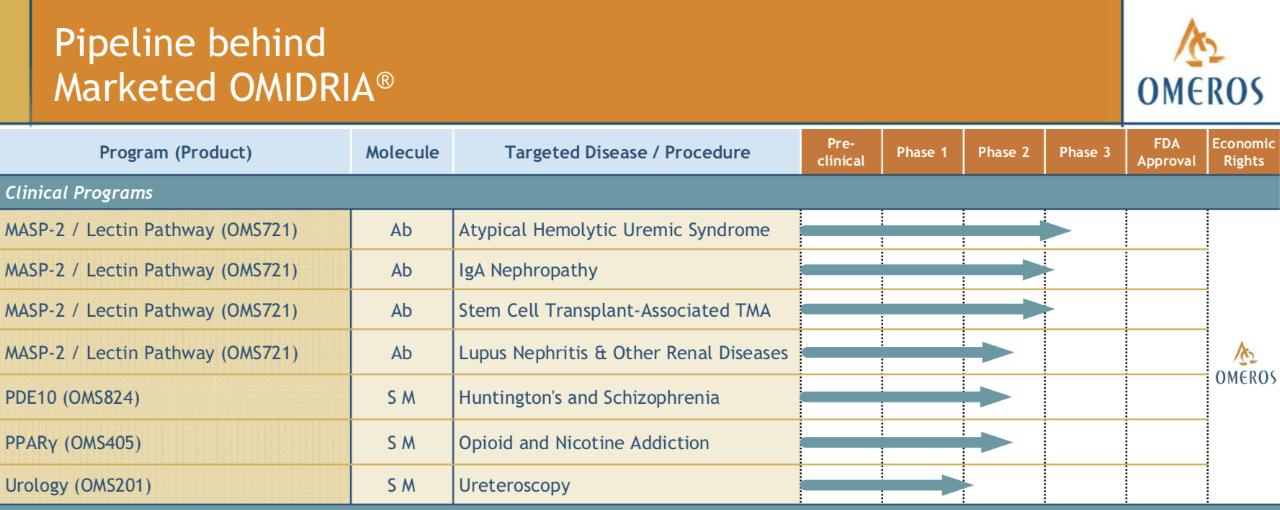

Back in 2018 Omeros' pipeline graphic boasted three narsoplimab (OMS721) clinical trials either in or nearing phase 3 status as set out below:

seekingalpha.com

These therapies had also received various designations including breakthrough therapy, orphan drug, and fast track. It also had a fourth, in a phase 2 trial for lupus nephritis and other kidney disorders.

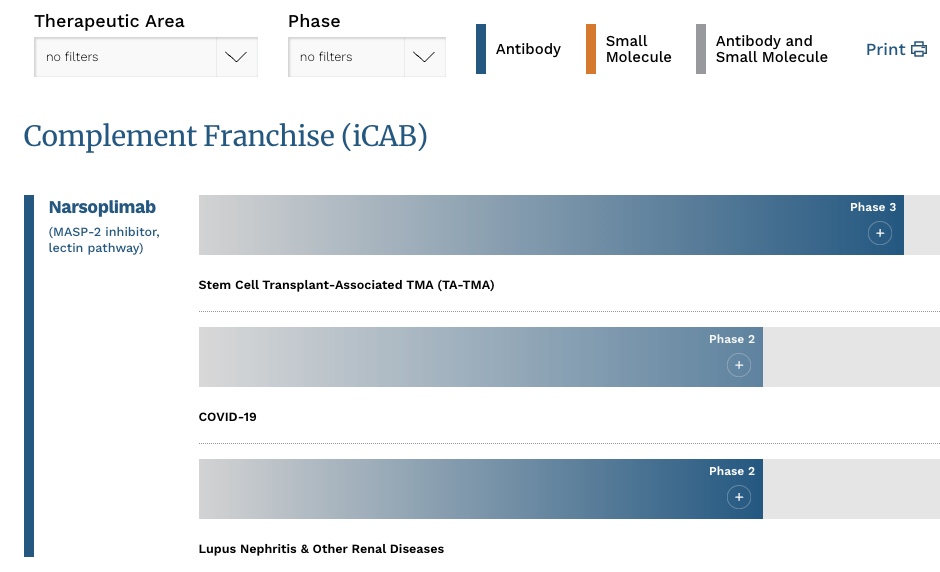

Moving ahead six years to 02/2024. Omeros website currently shows a vastly different narsoplimab pipeline as set out below:

omeros.com

Narsoplimab most advanced trial back in 2018 for atypical hemolytic uremic syndrome just seemed to drop in emphasis over the years. Now it is totally gone from its pipeline. This is not a new development. The reasons for its failure are unclear.

It removed IgA nephropathy (IgAN) from Narsoplimab's pipeline more recently, painfully, and publicly. In a 10/2023 release, Omeros stock got hit with a quick ~48% haircut when it announced topline results from its phase 3 IgAN trial. The release advised:

Topline results show that narsoplimab did not achieve statistically significant improvement over placebo. The UPE reduction in the placebo group was markedly greater than that reported in trials of other agents in IgA nephropathy. Based on the absence of statistical significance and as previously agreed with FDA, Omeros will not submit an application for approval of narsoplimab in this indication and will discontinue the ARTEMIS-IGAN clinical trial.

Kaput, finito. Management tried to save face with lame protestations about surprisingly high proteinuria reduction in the placebo comparison group. Two of narsoplimab's phase 3 candidates have hit the dust.

What about the third? Stem cell transplant-associated TMA (TA-TMA) has been an indication for which I have long held high hopes. Unfortunately it has been on life support since the FDA issued its 10/2021 CRL. I have held out hope that Omeros would be able to work out an arrangement with the FDA to refile its BLA.

As time has passed I am unsure if it is reasonable to expect anything for narsoplimab in this indication. During its most recent earnings call (the "Call") CEO Demopulos was enthusiastic about its forward path. I was concerned about its timeline and the two conditions still to be satisfied.

In terms of timeline, any new BLA filing will not be until mid-2024. Further, it is conditioned on:

In other words, there is no assurance that narsoplimab can ever make it to a TA-TMA BLA filing. How would one handicap such an event and even assuming it once files an acceptable BLA what are the chances of FDA approval? Those constitute known unknowns.

As for its lupus and kidney disorder trial, it seems to have been abandoned. Assuming it refers to NCT02682407, Omeros has not updated this since 04/2020 on clinicaltrials.gov. During the Call CEO Demopulos noted in the context of its IgAN disappointment:

...the evidence supporting the role of the lectin pathway and kidney disease and the therapeutic potential of MASP-2 inhibition remained strong. That said, any future development of lectin pathway inhibitor for IgA nephropathy or other indications that similarly require long-term chronic dosing are better suited for OMS1029, our next generation long acting MASP-2 inhibitor.

Wow that is strange. Should Omeros still be including lupus and kidney disorder on its pipeline as a phase 2 trial as shown in the excerpt above? In contrast, its OMS1029 is listed as a phase 1 trial:

omeros.com

I could find no trials on clinicaltrials.com in searching for "0MS1029" so I have no further details on that trial. Later in the Call, Demopulos cites the goal of advancing OMS1029 to phase 2 during the summer of 2024.

While narsoplimab has been a definite challenge for Omeros bulls, its OMIDRIA ocular irrigating solution has provided recent bright spots. I discuss its long-term revenue development and recent outlicensing deal (the "Deal") with Rayner Surgical's DRI Healthcare Trust in "Omeros: Taking It To The Max".

The Deal has provided Omeros with significant chunks of much-needed non-dilutive capital including:

In addition, Omeros retains the following rights in OMIDRIA:

...all royalties payable on any net sales of OMIDRIA outside the U.S., expanding after December 31, 2031 to Omeros receiving all royalties on global net sales of OMIDRIA.

During the Call CEO Demopulos and CFO Jacobsen reviewed its financial standing. In his opening review, Demopulos advised:

As of September 30, 2023, we had $310.3 million of cash and investments on hand. Omeros has $95 million of convertible debt maturing November 15 of this year, which we plan to retire. Even after retiring the 2023 notes, our current available cash and investments should enable us to fund our operations and continue advancing our multiple programs well into 2025. And as I noted just a few moments ago, we are evaluating options to extend that runway non-dilutively well into 2026 or beyond.

The 02/2024 OMIDRIA revision satisfied this last item, the $115 million will cover nearly a year of Omeros' $31 million quarterly cash burn. It is tricky to figure out any precise future cash burn; its historic quarterly revenues will be impacted by its OMIDRIA deal and its expenses will fluctuate as it revamps its development priorities to right size them to expected liquidity and to reflect IgAN miss.

I figure it had $310 million at the end of Q3 2023. If one deducts:

This balance of $175 million would be at the close of 2024. It should cover quarterly expenses well into 2026.

At the close of its Q3, 2023, Omeros had two outstanding notes. As stated in the Call it was paying its 2023 notes for $95 million. Omeros also has its 2026 notes for $210 million due 2/15/2026. It will likely refinance these over the next year + either with a loan or a share offering.

It seems to have fairly well picked its OMIDRIA goody tree clean, so I do not expect any more blockbuster cash infusions from that source. That is not to say that it won't be to generate some cash from its pipeline although I regard that as a long shot.

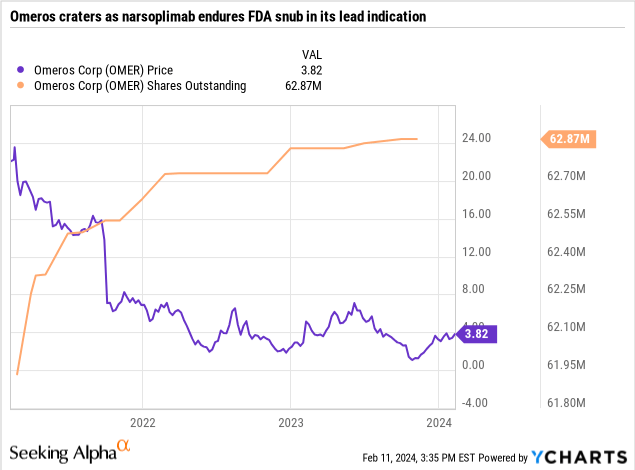

Its opportunities to raise capital via share offerings will depend to a great extent on its share price. This has varied greatly over the recent past as shown by the chart below:

In 07/2022 Omeros did enjoy a brief 69% surge, likely on takeover speculation. With that exception, its recent path has shown no sign of recovery.

I have long been a bull on Omeros. Unfortunately, it has not rewarded me for my constancy. As I write on 02/11/2024, I am disappointed at its near-term prospects. It has hollowed out and spent revenues from its sole approved therapy, OMIDRIA. Narsoplimab is struggling to work itself around so that it can file its BLA.

As discussed above it has ample near-term liquidity. However, it will need to generate additional liquidity to both pay its 2026 notes in two years and to pay its quarterly cash burn beginning at some point in 2026.

I continue to hold on to a modest stake in Omeros. I try to work my basis lower by trading around a core position. As I have tried to make clear in this article, it is easier to support a bear thesis for Omeros than it is to support a bull thesis.

That said I am holding on to my modest core position in Omeros. I am rating it as a hold.