zhihao/Moment via Getty Images

zhihao/Moment via Getty Images

Omnicell (NASDAQ:OMCL) has built a highly differentiated portfolio of products and services in the medication dispensing market that puts it, in my opinion, in a strongly advantageous position as the company is building a strong moat that will allow it to stay highly profitable and enjoy high and stable revenue streams in the long term, which should translate into significant (and hopefully steady) returns for investors once a more mature stage is reached. The M&A strategy and innovative efforts carried out in recent years have revolved around one specific goal: building a medication dispensing system as fully automated and comprehensive as possible to offer it to the different players in the healthcare industry, which would provide stable revenue streams for Omnicell thanks to the products and services offered around the system and improved outcomes and profit margins for its customers thanks to a unified, automated system with a lower margin of error.

Despite this, healthcare centers have significantly reduced their capital investments in recent quarters as a result of higher labor and operating costs, which has erased much of the optimism that investors built in recent years as the company has been recently reporting weaker revenues and margins. As a consequence of these headwinds, the management is currently taking some time to review the business while reducing its workforce and will now prioritize debt over growth as it holds $569 million in convertible senior notes due in September 2025 while financing conditions have worsened significantly since these were issued in September 2020.

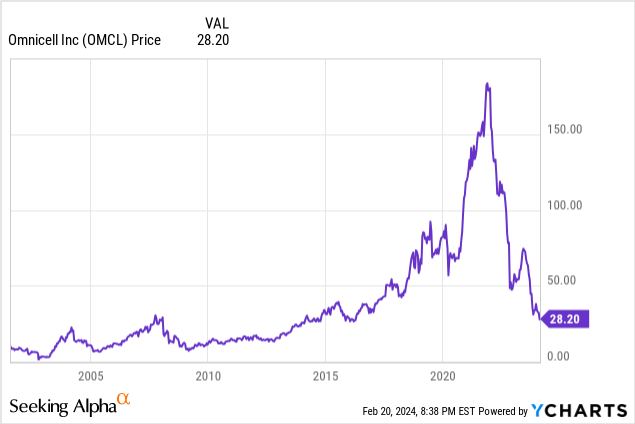

Operational weakness and short-term risks caused an 85% drop in the share price from all-time highs reached in November 2021 and a 65% decline since the end of 2019, the last year before the coronavirus pandemic crisis, which I consider a good opportunity for those medium and long-term investors with enough patience to wait for the healthcare industry to stabilize and for operations to improve again. In my opinion, it is normal for sales to suffer a material decline in the current macroeconomic context marked by increased operating costs for most industries, including healthcare, as the company's products represent capital investments for its customers, and investors should not forget the remarkable growth experienced before the recent setback and the strong moat the company is building. Furthermore, the balance sheet is very robust thanks to high cash and equivalents, and high total receivables should release some more cash in the coming quarters, mitigating much of the potential impact of the upcoming convertible senior notes' expiry date.

Omnicell is a manufacturer of medication management systems for pharmacies, specialty pharmacies, central pharmacies, IV pharmacies, and hospitals, including operating rooms, whose recent efforts are focused on achieving a zero-error, fully automated medication management infrastructure to, on the one hand, improve the outcome for patients and, on the other, optimize the operations of the different players in the healthcare system. The company was founded in 1992 and its market cap currently stands at ~$1.28 billion as it employs almost 4,000 workers, which reflects that it is a relatively new company that has expanded very quickly.

Omnicell logo (Omnicell.com)

The company's products seek to automate and optimize the medication dispensing process in both hospitals and pharmacies, as well as provide inventory management solutions, which seek to optimize their operations by automating processes and reducing human errors, as well as avoiding waste caused by medication expiration thanks to inventory optimization services. Using 2023 as a reference, approximately 62% of revenues are provided by product-related operations, whereas the rest are provided by service-related operations. Geographically, around 90% of revenues take place within the United States, so its geographical diversification is still very limited, which represents both a risk and a (growth) opportunity at the same time.

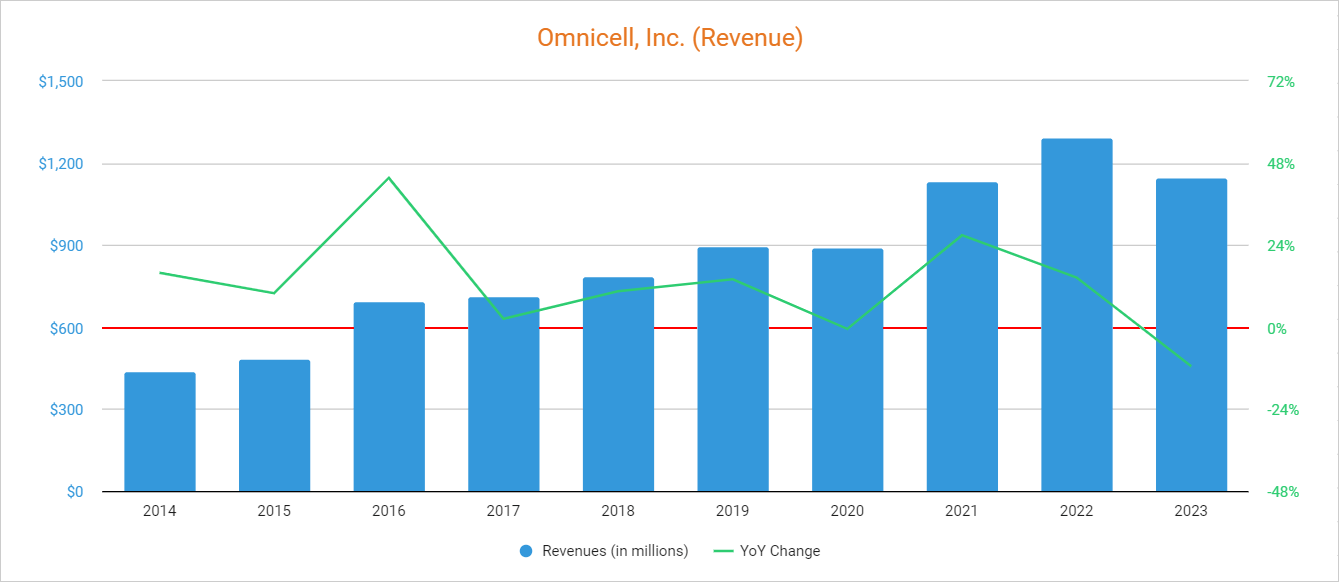

Despite the strong demand experienced in 2021 and 2022, the company is poised to significantly disappoint shareholders in its goal of achieving revenues in the $1.45 billion to $1.55 billion range by 2024 as 2023 closed with revenues of just $1.15 billion, which is sowing frustration in the market and caused a collapse in the share price.

Currently, shares are trading at $28.20, which represents an 84.94% decline from all-time highs of $187.29 in November 2021, and a 65.49% decline from the $81.72 at which shares closed on December 31, 2019, the year before the outbreak of the coronavirus pandemic. The situation has changed drastically in recent quarters, as a significant decrease in capital investments in the healthcare industry due to the recent increase in operating and labor costs is hindering Omnicell's sales. Furthermore, this comes at a time when the company is facing the upcoming expiration of very advantageous convertible senior notes in September 2025, so shareholders are expecting rising interest expenses or some share dilution in the foreseeable future.

To understand how Omnicell has come to offer such a comprehensive service in the medication dispensing and management process, it is very important to review the M&A strategy carried out in recent years. As these acquisitions are focused on creating a comprehensive service for customers, they are, in my opinion, highly scalable, which should not only provide a high margin profile but also significant revenue growth over the years.

In January 2016, the company acquired Aesynt, a provider of IV, Central Pharmacy, Point of Care, and Enterprise software solutions for healthcare players generating annual revenues of $190 million and annual EBITDA of $23 million at the time of the purchase, for $271.5 million. Later, in December 2016, it also acquired Ateb, a leading provider of pharmacy-based patient care and medication synchronization solutions to independent and chain pharmacies, for $40.7 million. Finally, a few months later, the company acquired InPharmics, a provider of advanced pharmacy informatics solutions to hospital pharmacies serving over 150 hospitals at the time of the purchase, for $5 million to expand the portfolio of services offered by the company.

After all these acquisitions, the company entered a deleveraging phase and successfully paid down all its debt, which opened the doors to a new expansion stage in 2020. In this regard, in October 2020, the company acquired Pharmaceutical Strategies Group's 340B Link business, which provides software-enabled services and solutions for hospitals, health systems, clinics, and entities to capture cost savings under the federal 340B Drug Pricing Program to expand Omnicell's reach in centers serving the most vulnerable communities. The acquired business reported trailing twelve months' revenues of $35 million at the time of the purchase and the company paid $225 million for the purchase.

The M&A activity continued in September 2021 when the company acquired FDS Amplicare, a healthcare financial and analytics solutions provider focused on managing, forecasting, and mitigating retail pharmacies' direct and indirect remuneration fees with annual revenues of $29 million at the time of the purchase, for $177 million. Later, in December 2021, the company also acquired ReCept, a leading provider of specialty pharmacy management services for health systems, clinics, and physicians, for $100 million. The acquisition spree continued in the same month when Omnicell acquired MarkeTouch Media, a pharmacy software solutions provider generating annual revenues of ~$14 million at the time of the purchase, for $82 million to enhance the company's advanced services portfolio, and it also acquired Hub and Spoke Innovations a month later to offer patients 24/7 access to their medications and reduce the workload in UK pharmacies.

The company has managed to increase its sales steadily in recent years, boosted by acquisitions and innovation efforts as it keeps updating its products and services to cover an increasing range of needs in medication dispensing, a trend that the reopening of the economy after the outbreak of the coronavirus accelerated in 2021 as revenues increased by 26.88% in 2021 and by $14.48% in 2022. Still, lower demand caused by strong cost pressures in the healthcare system has caused an 11.48% revenue decline in 2023, especially in the current strict financing environment.

Omnicell Revenue (Seeking Alpha)

More specifically, revenues decreased by 8.84% year over year in Q1 2023, by 9.78% year over year in Q2, by 14.19% year over year in Q3, and by 13.04% year over year in Q4 (and 13.36% quarter over quarter), and are expected decline by a further ~7% in 2024 as bookings decreased by 19% year over year in full 2023 due to delayed capital projects in the industry as customers are trying to keep as much cash as possible in their balance sheets. Still, this upcoming decline is expected to mark the bottom, and revenue growth is projected at ~5.6% in 2025 as the management expects some Point of Care booking increases throughout 2024. A fact worth mentioning is that services revenue increased by 12% year over year in Q4 2023 thanks to an increased installed base and pricing actions. Also, the company has gained significant market share at the Point of Care level in the last 3 years, and innovation efforts remain in force as it recently launched a new XT console upgrade to improve nursing efficiency and user experience. Now, the management plans to keep improving the platform in 2024 to retain earned customers in the long run and expand the company's total addressable market.

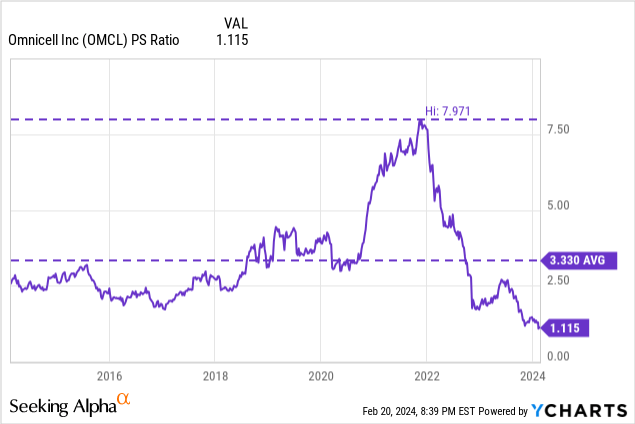

Along with this, the management is making great efforts to capitalize on the demand growth expected for cloud-based infrastructures in the coming years as it opened a software development center in India in September 2021. But despite Omnicell's growth experienced in recent years and the efforts to continue expanding the possibilities offered by its products and services, the recent drop in the share price caused by operational weakness has sunk the P/S ratio to the lowest levels seen in recent years at 1.115, which means that the company generates annual revenues of $0.90 for each dollar held in shares by investors.

This ratio is 66.52% below the average of the past 10 years and represents an 86.01% decline from the 10-year peak of 7.971 reached at the end of 2021, which essentially means that investors are giving less value to the company's revenues not only because of very pessimistic growth expectations but also because lower volumes and inflationary pressures have caused a contraction in profit margins.

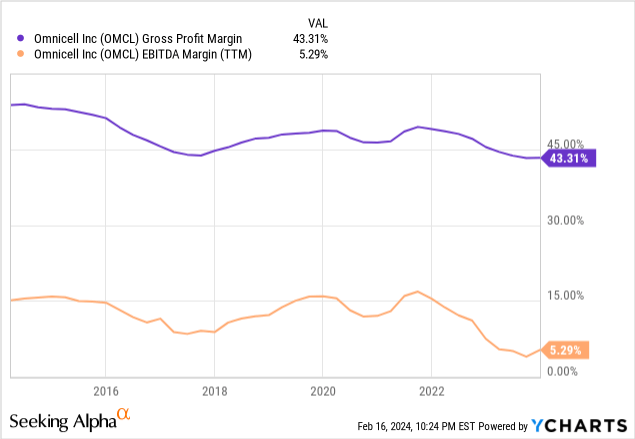

The company's products and services provide significant added value to its customers as the breadth of services offered is ample, significantly improving the optimization of its operations and reducing the need to rely on various service providers to manage their medication management systems. This has allowed Omnicell to report high gross profit and EBITDA margins over the years, although these have recently been negatively impacted by inflationary pressures and decreasing volumes as the trailing twelve months' gross profit margin currently stands at 43.31%, whereas the EBITDA margin is at 5.29%.

Furthermore, the gross profit margin decreased to 40.72% in Q4 2023 and the EBITDA margin almost entered negative territory as it was as low as 0.14%. During the quarter, non-GAAP EBITDA was $24 million compared to $41 million in Q3 2023 and $26 million in the same quarter of 2022, which reflects that the impact of the recent revenue and margin decline is greater than the savings achieved through recent cost-control initiatives, and the company reported negative EPS -$0.32 in the quarter. Despite this, normalized EPS was $0.33 as the company is suffering one-time losses for its current restructuring process, and the management forecasts a flat normalized EPS of $0.90 to $1.40 in 2024 and a very acceptable improvement to ~$1.48 in 2025, which is still significantly lower compared to the $3 EPS reported in full-year 2022 and the $1.91 reported in full year 2023.

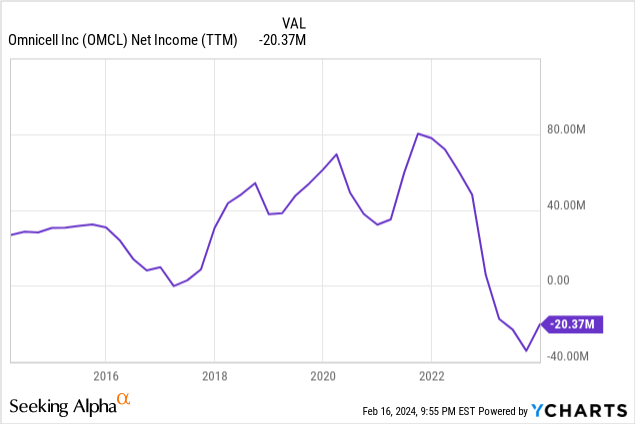

The company is currently enduring strong cost-control initiatives with the help of an external consultant and is currently reducing its workforce by 7% in a process that will extend until the end of Q2 2024, which caused $10 million of severance-related expenses in Q4 2023 that added to the current headwinds as the company reported a negative net income of -$20.4 million in full 2023 compared to a positive $5.6 million in 2022. Still, the measure is expected to bring $50 million of annual savings once finished, from which around 75% are operating expenses. Most (but not all) of these savings are expected to be achieved at the beginning of Q1 2024, so some margin stabilization should be noticeable in the coming quarters. A workforce reduction of the same magnitude was announced in November 2022, but recent weakness has forced the management to make further reductions.

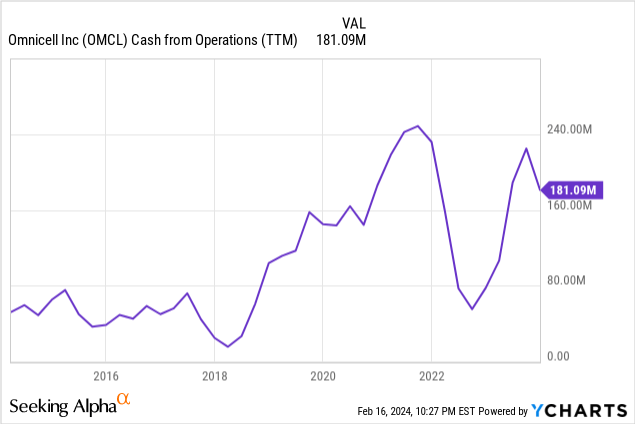

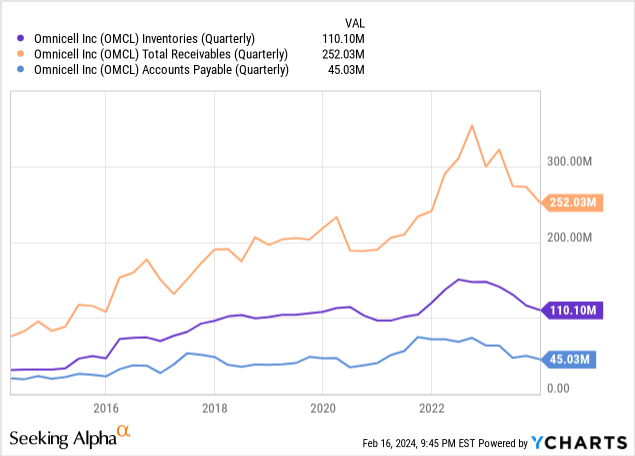

Still, cash from operations has remained robust at $181.09 million over the last 12 months thanks to inventory and accounts receivable reductions, something the company has continued to do until now as it reported positive cash from operations of $38.4 million in Q4 2023. Still, this cash generation is unsustainable over time as, during the quarter, inventories decreased by $6 million and accounts receivable by $32.2 million while accounts payable decreased by only $4.9 million.

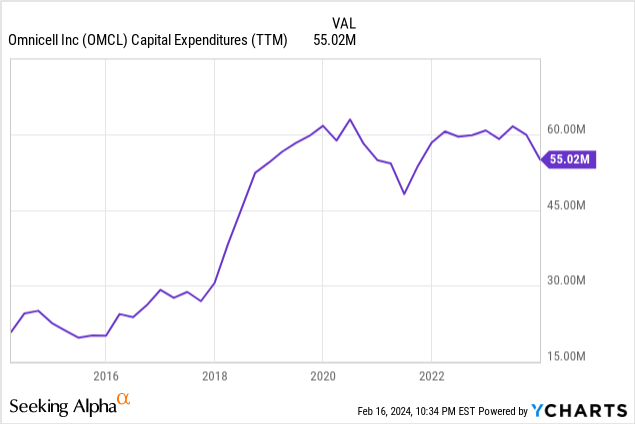

In this regard, the company is making extensive use of the resources available on the balance sheet to avoid reporting negative cash from operations as it needs to build as much cash as possible before September 2025, at which time the current convertible notes of $569 million expire. In addition, the company also needs to make extensive use of cash to continue covering capital expenditures that currently stand at over $50 million per year as it is in the midst of an expansion stage.

Luckily, capital expenditures have moderated slightly in recent quarters as the company reported capital expenditures of $9.1 million in Q4 2023 compared to $10.6 million in Q3 2023 and $13.7 million during the same quarter of 2022, and at this rate, annual capital expenditures would drop to below $40 million. Additionally, I would expect more reductions in the coming quarters as expansionary efforts are currently on hold. Still, higher-than-usual inflation will continue to negatively impact profit margins in 2024 and the management expects some negative product mix for the year, which will reduce the benefits of the ongoing labor cuts.

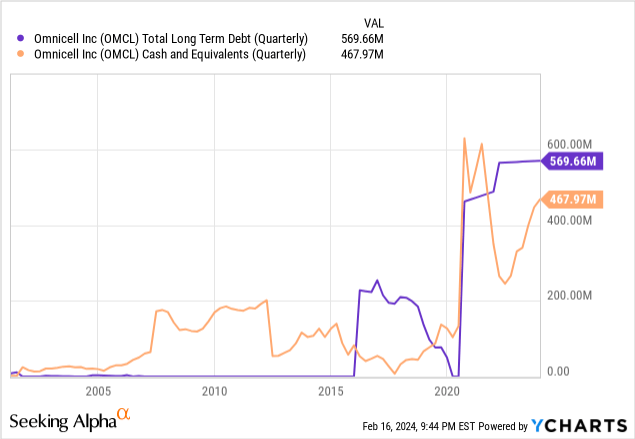

The company currently holds $569.66 million in long-term debt and cash and equivalents of $467.97 million. This high cash and equivalents has been possible thanks to the recent conversion of inventories and receivables into actual cash as cash and equivalents increased by $223 million since Q2 2022 to $468 million despite current headwinds.

Additionally, the balance sheet still has $252.03 million of accounts receivable and inventories at healthy levels of $110.10 million, while accounts payable have been reduced in recent quarters to $45.03 million, so I expect cash from operations to remain strong throughout 2024 as the company should be able to continue converting accounts receivable into actual cash and is not expected to need to build higher inventories to continue operating normally. Furthermore, we should not forget that a large part of the ongoing workforce reductions will be reflected in results starting in Q1 2024.

In this sense, such high cash and equivalents, as well as very high accounts receivable, should make possible a significant reduction of the impact that the expiration of the senior notes will have on the balance sheet in 2025, although investors should expect that either interest expenses will increase once these highly advantageous notes expire, or the shares will suffer some share dilution.

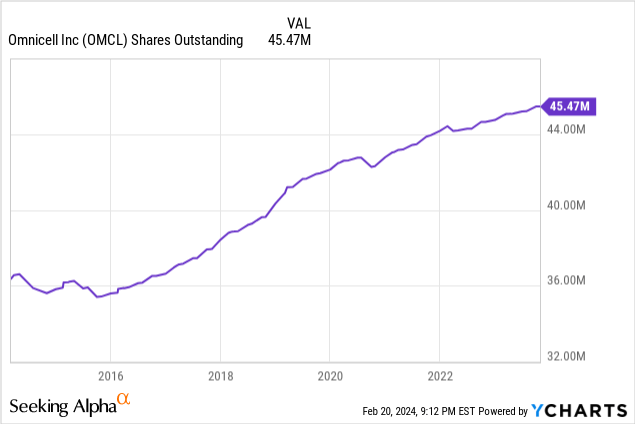

Given that the company is still in an expansion phase marked by aggressive acquisitions and innovation efforts, it has needed financing not only through the use of debt but also through the issuance of shares as cash provided by share issuances was $435.1 million in the 2014-2023 period, whereas cash used to repurchase shares was $258.5 million, which has caused a ~25% increase in the total number of shares outstanding during this period.

This trend has been maintained over time since the company's foundation, which means that as it has grown, it has been divided among more shares, meaning that each share represents an increasingly smaller portion of an increasingly bigger company. Investors can expect this to continue happening in the coming years, especially in the short term because the management needs cash to pay down its debt, although this trend should stop as soon as the company reaches a sufficient level of maturity.

All Omnicell shareholders, as well as potential investors interested in initiating a position in the short term, should be aware of a series of risks that Omnicell shares present. Below I am going to highlight what, in my opinion, are the most significant risks that investors should take into account and monitor, especially for the short and medium term.

In my opinion, the company's products and services are creating a need in those places where they are installed as such a comprehensive platform provides a lot of simplicity for the workers of the different centers that make up the healthcare system, something that should provide reliable revenue streams for Omnicell in the long term as changing the company's platform for other suppliers would mean the need to retrain workers and, often, lower their productivity. As an investor, this is the most important aspect to keep in mind, as having a product that essentially provides benefits and conveniences to your customers is one of the main ingredients for long-term success.

Regarding the company's current situation, higher labor and operating costs in the healthcare industry are delaying capital projects as customers are trying to reduce their investments until current headwinds subside, especially taking current disadvantageous financing conditions into account. This has caused a reduction in volumes and, therefore, profit margins, which were also directly impacted by inflationary pressures. To all this, we must add that the $569 million convertible notes will expire in September 2025, so I would expect rising interest expenses and some share dilution in the short term.

Even so, I consider that the headwinds experienced in recent quarters represent a good opportunity for medium and long-term investors given that the share price is highly influenced by investors' pessimism as it declined by as much as 85% from all-time highs reached in November 2021. The current high cash and equivalents and accounts receivable suggest that the company will be able to cushion much of this impact, so I believe that the potential share dilution and increase in interest expenses will be limited. Furthermore, recent labor cuts are expected to provide $50 million in annual savings and current headwinds are, in my opinion, temporary as they are directly linked to the macroeconomic and financing landscape, while services revenue should keep growing over the years as the installed base keeps increasing. In the long term, I believe that it will be increasingly difficult to compete with Omnicell as it is building a highly specialized portfolio as complete and automated as possible. For all these reasons, I consider that the share price can reach the $81.72 with which 2019 closed once the current headwinds clear up and optimism reigns again among investors, which will surely require a lot of patience (and reviews of the situation) as the recovery could take a few years but is, in my opinion, worth it as this would represent a ~190% return from current prices.