Analysts Have Been Trimming Their Omnicell, Inc. (NASDAQ:OMCL) Price Target After Its Latest Report

It's been a sad week for Omnicell, Inc. (NASDAQ:OMCL), who've watched their investment drop 14% to US$27.41 in the week since the company reported its yearly result. The results overall were pretty much dead in line with analyst forecasts; revenues were US$1.1b and statutory losses were US$0.45 per share. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Omnicell after the latest results.

Check out our latest analysis for Omnicell

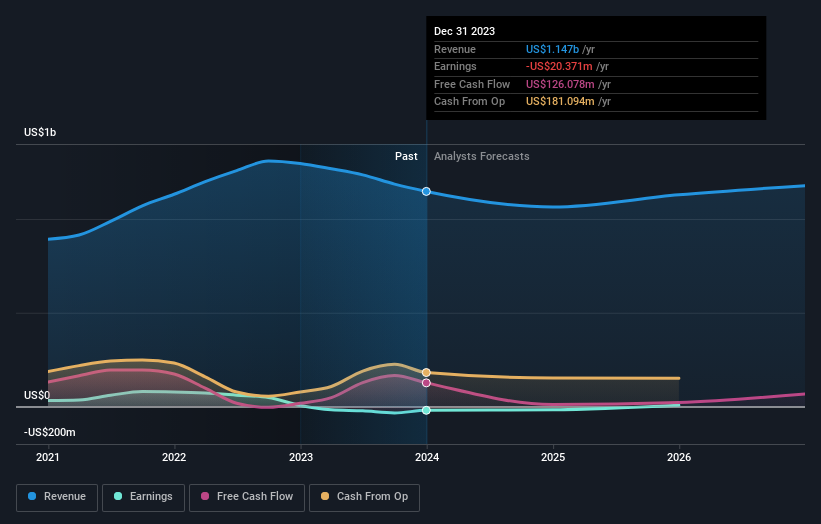

After the latest results, the consensus from Omnicell's eight analysts is for revenues of US$1.06b in 2024, which would reflect a measurable 7.2% decline in revenue compared to the last year of performance. Losses are expected to be contained, narrowing 15% from last year to US$0.38. Before this earnings announcement, the analysts had been modelling revenues of US$1.08b and losses of US$0.05 per share in 2024. While this year's revenue estimates held steady, there was also a sizeable expansion in loss per share expectations, suggesting the consensus has a bit of a mixed view on the stock.

With the increase in forecast losses for next year, it's perhaps no surprise to see that the average price target dipped 10% to US$33.57, with the analysts signalling that growing losses would be a definite concern. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Omnicell, with the most bullish analyst valuing it at US$40.00 and the most bearish at US$26.00 per share. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We would highlight that revenue is expected to reverse, with a forecast 7.2% annualised decline to the end of 2024. That is a notable change from historical growth of 10% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 7.9% annually for the foreseeable future. It's pretty clear that Omnicell's revenues are expected to perform substantially worse than the wider industry.