koosen

koosen

Shares of Olin (NYSE:OLN) have been a meaningful underperforming over the past year, losing about 20% of their value. Since rating shares a hold in October, they have largely tread water, rising just 3% vs a 13% gain in the S&P 500. At the company’s 2024 guidance, it does have a forward free cash flow yield of nearly 9%, which is certainly not expensive. That said, my caution on OLN has been driven in part by a lack of confidence in management, and these significant concerns persist, which leave me on the sidelines.

Seeking Alpha

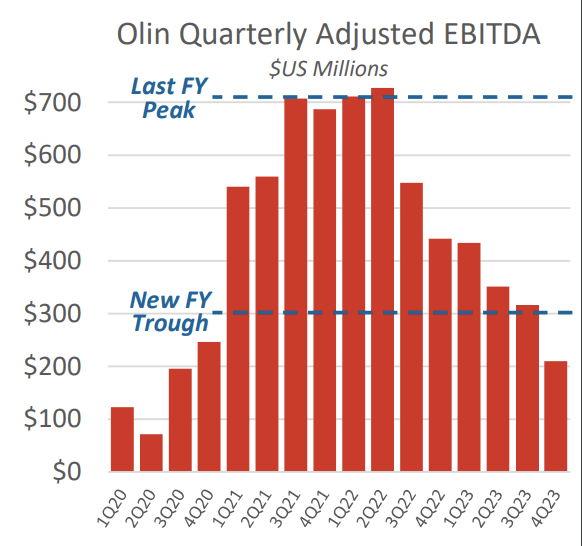

In the company’s fourth quarter, Olin earned $0.43 on $1.6 billion of revenue. This was about $0.15 ahead of consensus. Revenue fell by about $362 million, but cost of goods sold fell by a narrower $164 million as it lost operating leverage in the face of weaker volumes and prices. During the quarter, Olin generated $210 million in adjusted EBITDA down from $442 million a year ago. This is an important figure because it is substantially below what Olin has argued it would earn in a “trough” environment.

As I wrote about in October, Olin has historically had a highly cyclical business, given its exposure to commodity (rather than value-add) chemical markets with a significant dependence on Chinese construction activity. Through stated efforts to better manage volumes and diversify, Olin management has argued it has somewhat reduced cyclicality. Last quarter, it showed $350 million in quarterly EBITDA or $1.4 billion/year as trough levels. Interestingly, the same chart this quarter was adjusted down to $300 million or $1.2 billion per year.

Olin

I argued that the $1.4 billion level was not credible based on actual results, so it is a positive that management has moved off of this number, even if belatedly. For the year, Olin generated $1.3 billion in EBITDA, a level it expects to modestly surpass in 2024. Based on prior guidance, that would mark 2 years of below-trough results. At that point, it is clear that what you are communicating as a “trough” is not really a trough, particularly considering the US and global economy have continued to expand throughout. Now, these results will be about $100 million brough trough levels.

Of course, while this number is lower, I am still not sure it represents a genuine trough level for the business. After all, Q4 EBITDA was $210 million or $840 million annualized. In Q1, it expects to generate about $230-235 million in EBITDA, or about $920 million annualized. This is why I continue to view guidance as ambitious and view management as having a credibility problem. We cannot be sure they do not revise down trough guidance further. Its full year guidance of at least $1.3 billion in EBITDA also implies a significant second-half acceleration which may or may not materialize.

Further on the topic of management, it is important to remember that Olin is essentially being led by a caretaker. As discussed in October, CEO Scott Sutton announced he will be stepping down, though no replacement had been named. That speaks to an unorderly succession process and potential friction between management and the board. To regain credibility, new leadership is needed. Additionally, it is simply important to know who will be running the company going forward. Disappointingly, on the conference call, outgoing CEO Sutton said that to his knowledge no offer has been made to a potential new CEO. While Sutton may be able to run the company well on a day-to-day basis, a new permanent leader is needed to be empowered to make strategic decisions. The duration of this search is troubling. I also suspect a new leader may want to abandon or significantly alter trough guidance, just given the gap between that and current operating results. Until a new leader is announced and either guidance changes or results improve, there is likely to be skepticism toward Olin management.

Looking closer at results, its primary unit, Chlor Alkali Products & Vinyls, reported a 7% sequential decline in sales to $906 million and a 39% drop in EBITDA to $171 million. For the full year, sales were down 21% and EBITDA down 34%. During the quarter, it reduced volumes to help support pricing and margins and it expects to limit sales activity at least through February in an effort to preserve pricing.

Its Epoxy business remains deeply challenged but saw some improvement. Sales fell by 3% to $313 million, but its net loss narrowed by $4 million to $10 million as it reduced inventory and benefited from lower raw material costs. Epoxy drove $472 million in EBITDA in 2022; in 2023, that declined 94% to $26 million as sales fell by half. This segment has been hit by both weak demand and increased supply. On the supply front, Chinese epoxy supply is set to continue to rise as new plants come online. Given weak domestic demand, Chinese exports will likely rise over the next two years, weighing on global prices.

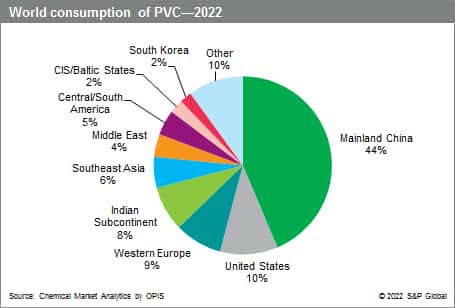

Olin’s products are closely tied to PVC demand. While I have been more optimistic on US construction activity given federal infrastructure spending, China is the primary consumer of PVC, accounting for nearly half of the market. At best, the path forward for the Chinese real estate market can be described as uncertain. Major developers like Evergrande are being liquidated, and meaningful policy support has not been forthcoming. Ultimately, if this market rebounds, Olin will benefit, but if it stays weak, Olin results will remain weak. Given the number of investment opportunities, I prefer to focus on companies with less exposure to Chinese construction, unless valuation is incredibly compelling.

S&P Global

Finally, its Winchester unit saw sales rise 4% to $395 million and EBITDA 3% to $74 million aided by higher commercial pricing and offset by weaker military demand. With the war in Ukraine requiring tremendous amounts of ammunition, this is a potential tailwind. However, it is unclear how much more funding for the war effort the US government will authorize. As such, I am unsure how much growth will materialize. Still, this segment is better positioned than PVC-tied segments; it is simply just not large enough to carry the company.

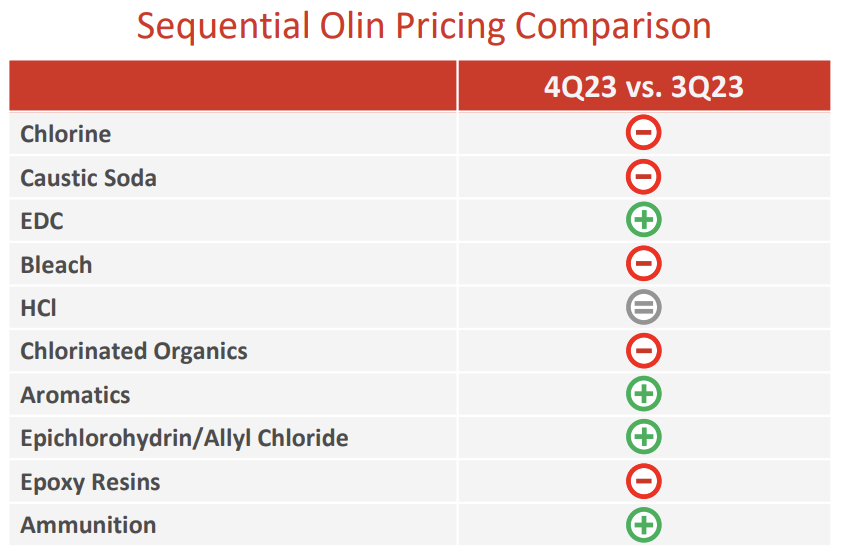

On the bright side, management is seeing increased customer demand in some segments. Additionally, while prices had been falling across the board earlier this year, the outlook is now more mixed, though on a volume-weighted basis, prices did fall for Olin’s overall product portfolio in Q4. In Q1, it expects to push a sequential increase in chlorine prices, which will be a positive. Of course, its guidance for a 10% rise in Q1 EBITDA and over $1.3 billion in 2024 EBITDA assumes gradual improvement in the market.

Olin

Olin does remain cash flow generative even with results weak on a relative basis. It repurchased $711 million of stock in 2023, though the pace slowed to $116 million of buybacks in Q4. As a result, it reduced its share count by 10.3% in 2023. It also has a solid balance sheet with $170 million of cash and $2.5 billion of debt for net leverage of 1.9x.

For the full year, it expects to grow adjusted EBITDA to at least $1.3 billion while investing about $238 million in cap-ex. That should leave it with $545 million in free cash flow. Its dividend costs about $100 million, which would allow about a 7% share count reduction at the current share price. Ultimately, to achieve $1.3+ billion in EBITDA, it will need to get back to $350-400 million in quarterly EBITDA in H2 2024, which will be difficult with increasing Chinese supply and weak construction activity there.

I do continue to expect OLN to generate ~$500 to $550 million in free cash flow and about $4 in earnings, but there is some downside risk if Chinese activity worsens further, or if a new CEO significantly alters guidance to “lower the bar.” Until we see new management, I expect shares to remain stuck in the $45-50 range or a 9-10% free cash flow yield, and I see Olin as dead money. It remains more of a value trap than a value opportunity.