J. Michael Jones

J. Michael Jones

Ollie’s Bargain Outlet (NASDAQ:OLLI) retails brand name merchandise in the United States, focusing on low outlet pricing. The company operates under many brands, including Ollie’s, Good Stuff Cheap, Real Brands Real Cheap!, and Sarasota Breeze. Under the brands, the company sells a very wide variety of products.

Since the company’s IPO in 2015, Ollie’s stock has appreciated greatly with the company’s store growth strategy – since the IPO, the stock’s appreciation currently stands at a CAGR of 17.5%. As capital is mostly spent on growth and share repurchases, the company doesn’t currently pay out a dividend.

Stock Chart From IPO (Seeking Alpha)

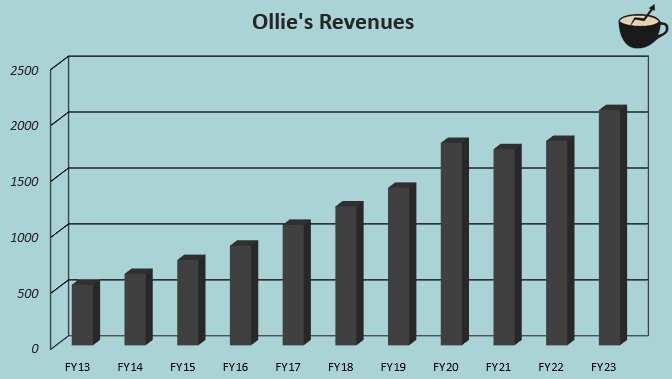

Ollie’s has had great growth through constant new store openings – the company has grown revenues organically at a CAGR of 14.5% from FY2013 to FY2023. The company now operates in 30 states, and still sees good room for more store count growth in the long-term future. Ollie’s current return on equity stands at a fairly good figure of 11.46%.

Author's Calculation Using TIKR Data

The company has a great amount of capital to finance future growth. Currently, Ollie’s holds $266.3 million in cash as well as $87.0 million in short-term investments on the company’s balance sheet. While the store expansion does take up a good amount of capital with $124.4 million spent in FY2023, Ollie’s has historically been able to allocate some capital towards share buybacks in addition to growth investments.

Ollie’s reported the company’s Q4/FY2023 results on the 20th of March. The company boasted revenues of $648.9 million in line with expectations, representing a great year-over-year growth of 18.0%. Excluding the effect of an extra week in the reported period, the achieved growth was 11.9% year-over-year, slightly lower than prior quarters in FY2023. The quarter showed a normalized EPS of $1.23 compared to analysts’ expectations of $1.16; overall, the quarter went as expected.

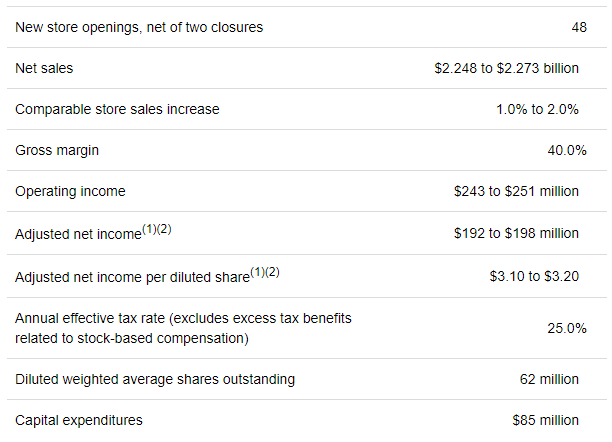

I believe that the FY2024 guidance was the more important piece of information in the longer-term investment case. Ollie’s also gave a FY2024 outlook with the Q4 report. The company expects net sales of $2248 million to $2273 million, with the middle point representing a growth of 7.5%. The outlook came in somewhat below expectations, as analysts expected revenues of around $2295 million for the year. Analysts were expecting an EPS of $3.21 in FY2024 compared to Ollie’s given guidance of $3.10 to $3.20 – the given EPS is roughly in line with expectations. While both revenues and the EPS were guided below expectations, the guidance miss was very minimal, and doesn’t in my opinion worsen the investment.

Ollie's FY2024 Outlook (Ollie's Q4 Press Release)

On the other hand, the company’s long-term ambition is growing – Ollie’s updated the long-term target of total store count from 1050 into 1300 with the Q4 report. At the end of Q4, Ollie’s has a total of 512 open stores; the new target aims at a significant runway in future growth, and in my opinion signals that Ollie’s strategy is proceeding well. In FY2024, the company is looking to add 48 net new stores compared to 44 in FY2023.

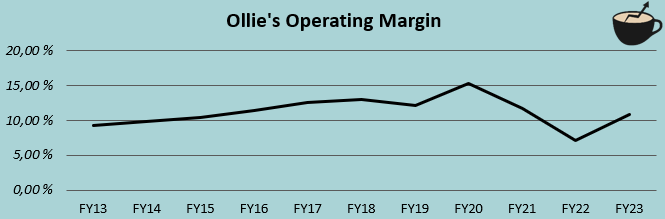

In prior years, Ollie’s has been able to drive up profitability with constant operating margin increases. The company has had quite a widely worse performance in the past three years, though, as profitability has suffered from FY2021 to FY2022.

Author's Calculation Using TIKR Data

In my opinion the future margin level is quite important, and any future margin improvement could be highly valuable. The achieved FY2023 operating margin of 10.8% is still below the FY2020 high and prior years’ performance, and Ollie’s guides for quite minimal margin expansion in FY2024 with an operating margin of 10.9% with the middle point of sales and operating income – currently, it doesn’t seem like profitability is going to grow back into the prior years’ high. Ollie’s targets a long-term gross margin level of 40% as told in the Q4 earnings call, signaling a very similar level to the achieved FY2023 gross margin of 39.6%.

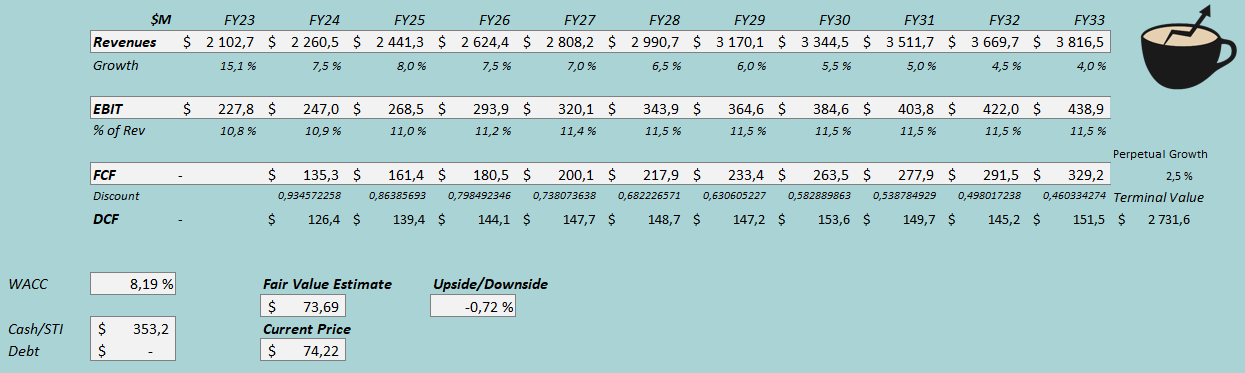

The stock seems to be priced for a continued growth story with a financial performance that I expect. To estimate a rough fair value for the stock and to demonstrate the valuation, I constructed a discounted cash flow model. In the DCF model, I estimate revenues to grow with Ollie’s FY2024 guidance middle point of 7.5% for the year. Afterwards I estimate a growth of 8% for FY2025 that slows down gradually into a perpetual growth rate of 2.5%, representing a CAGR of 6.1% from FY2023 to FY2033.

For the EBIT margin, I estimate some bounce back closer to Ollie’s previous margin highs with very slight gross margin improvement and operating leverage. After the FY2023 performance of 10.8%, I model a gradual improvement into an EBIT margin of 11.5% from FY2028 forward. The company guides for capital expenditures of $85 million for FY2024, well above D&A, making the cash flow conversion somewhat poor. I estimate the conversion to improve as the growth slows down.

With the mentioned estimates along with a cost of capital of 8.19%, the DCF model estimates Ollie’s fair value at $73.69, very near the stock price at the time of writing. While the valuation is by no means too high, I don’t see any immediate upside for the stock.

DCF Model (Author's Calculation)

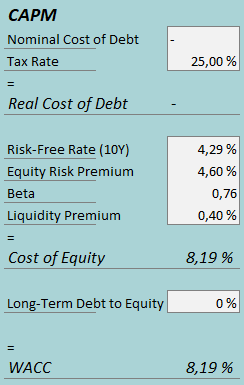

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

Ollie’s doesn’t currently hold any interest-bearing debt, and I estimate the financing decision to stay the same with a long-term debt-to-equity ratio of 0%. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.29%. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. Yahoo Finance estimates Ollie’s beta at a figure of 0.76. Finally, I add a small liquidity premium of 0.4%, creating a cost of equity and WACC of 8.19%.

Ollie’s long-term growth story is progressing well. The company reported Q4 results mostly in line with expectations. While the FY2024 revenue guidance was slightly below expectations, the long-term store target was raised, signaling confidence in the growth runway ahead. The company’s operating margin is below previous years’ highs, though, and Ollie’s doesn’t seem too ambitious to achieve the previous highs. The stock currently seems priced fairly as my DCF model estimates a value very near the stock price; for the time being, I have a hold rating for the stock.