Sundry Photography

Sundry Photography

Here’s a good “note to self” to remember: the headline risk from negative events, particularly surrounding data breaches, often wears out as fundamental stories regain momentum. This is exactly what happened with Okta (NASDAQ:OKTA), the single sign-on and identity management software platform that reported a data breach in October. The stock dipped sharply after the breach and Q3 results reported in December cited a much larger-than-anticipated impact from the event.

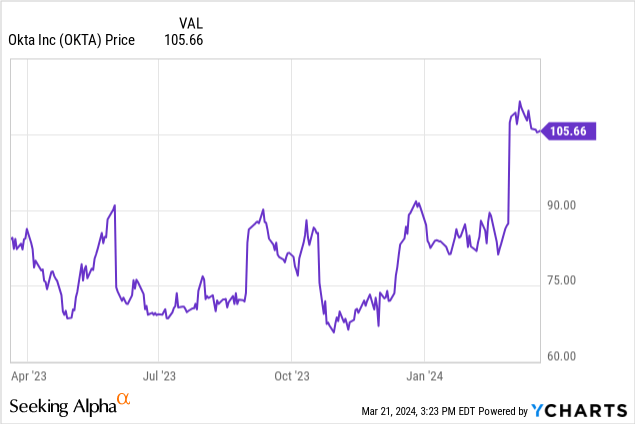

Since then, however, Okta has rallied in tandem - if not even better than - its tech peers. Up ~20% year to date, investors cheered the company's Q4 earnings release and its slightly boosted outlook for the remainder of the current year FY25.

I last wrote a note on Okta in December, when the stock dipped to $70 in the wake of Q3 earnings and the impact of the data breach. Since then, my position has rallied more than 50% - and I'm heading for the exit. Now cognizant of a number of fundamental slowdowns that appeared in Okta's Q4 results plus the overhang of a richer valuation, I'm downgrading my viewpoint on Okta to neutral.

Price, of course, is the main consideration here. At current levels near $106, Okta trades at a market cap of $17.72 billion. After we net off the $2.20 billion of cash and $1.15 billion of debt on Okta's most recent balance sheet, the company's resulting enterprise value is $16.77 billion.

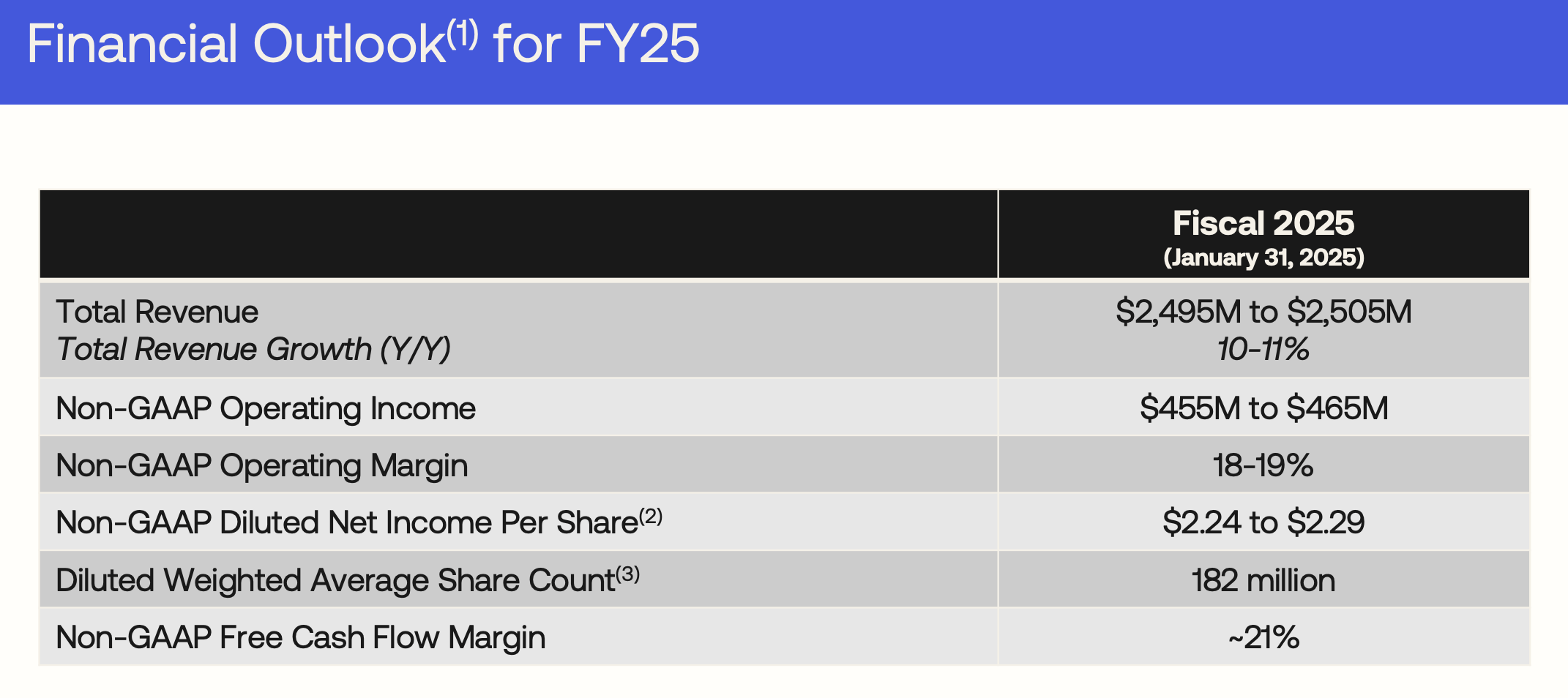

Meanwhile, for the current fiscal year, Okta has guided to 10-11% y/y revenue growth, up from a prior view of ~10% growth:

Okta outlook (Okta Q4 investor deck)

And if we apply the company's 21% FCF margin expectation against the $2.50 billion revenue midpoint of this guidance range, we arrive at $525 million of FCF, up 7% y/y (FY24 margin was 22%).

Taken together, Okta's valuation multiples are currently sitting at:

At current levels, I'm concerned about a number of trends that have materialized in Okta's results: both slowing customer growth and weaker net expansion trends, which have simultaneously slowed down revenue growth.

There are still a number of positives in Okta to consider, including its large $80 billion TAM, its good balance of growth-versus-margin, and its nearly pure recurring revenue base. But all considered, given the sharpness of Okta's rally since December, plus the fact that the company expects growth to decelerate to the low teens very soon, I think it's more than appropriate to lock in gains here and invest elsewhere.

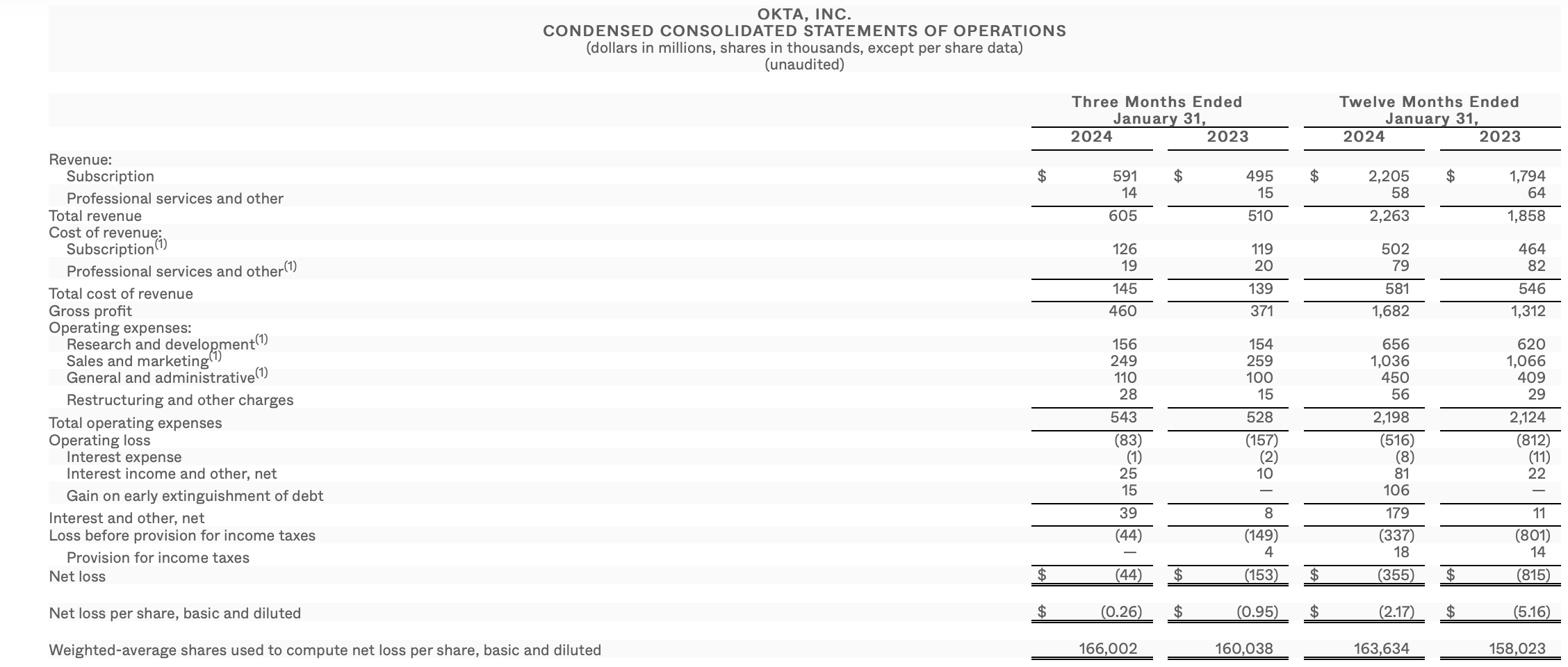

Let's now go through Okta's latest quarterly results in greater detail. The Q4 earnings summary is shown below:

Okta Q4 results (Okta Q4 investor deck)

Okta's revenue grew 19% y/y to $605 million, ahead of Wall Street's expectations of $588 million (+15% y/y). While it was a strong beat, we do note that revenue decelerated three points versus 22% y/y growth in Q3. Note as well that Okta continues to cite lingering (though inestimable) impact from the October data breach, and that this will be an overhang on FY25 revenue as well.

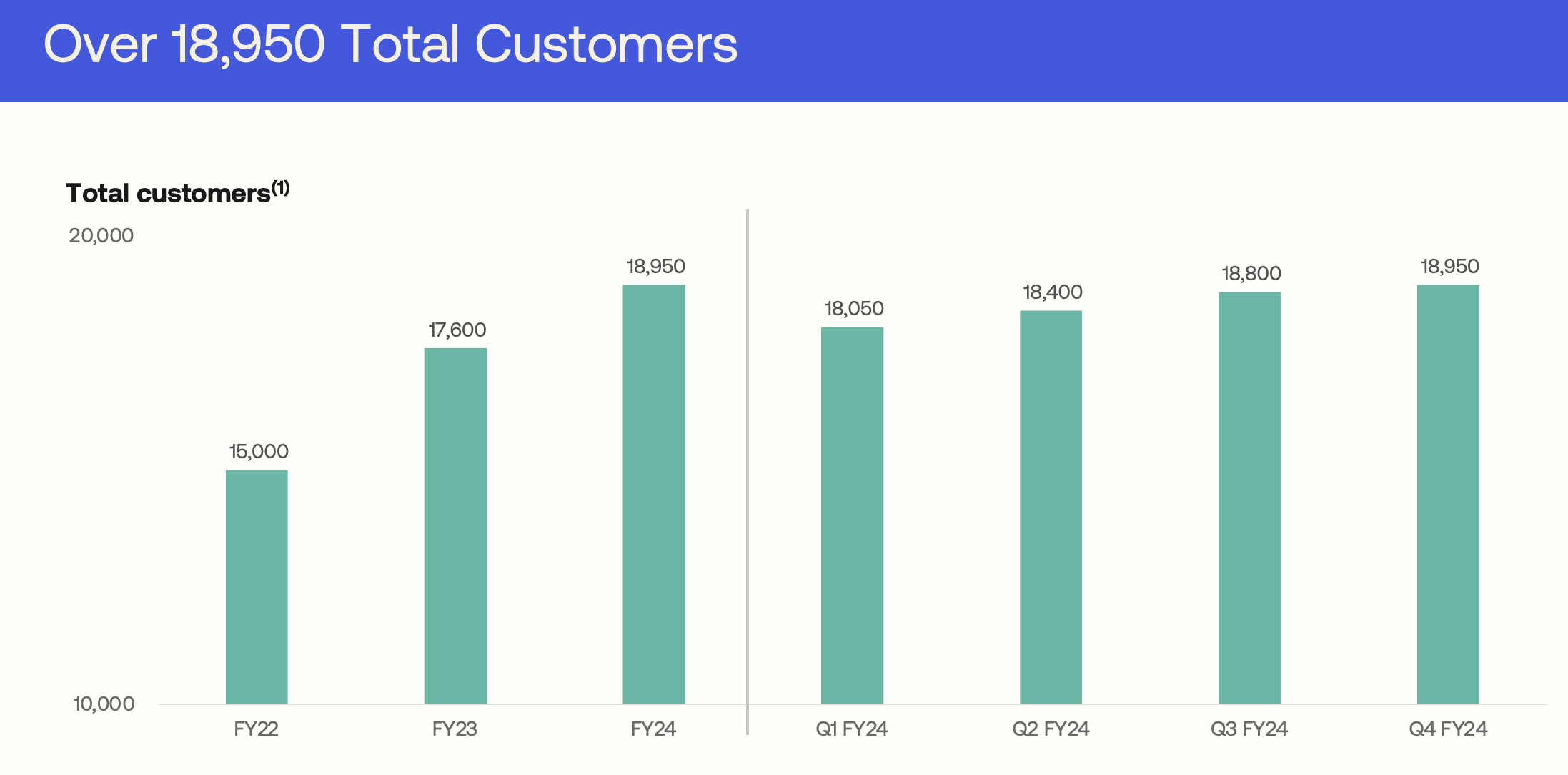

In addition to this, there are a number of other concerning metrics to call out. As shown in the chart below, Okta ended Q4 with just shy of 19k customers, but it only added 150 net-new customers in Q4: versus an average of ~400 customers over the prior two quarters.

Okta customer trends (Okta Q4 investor deck)

Historically, the fourth quarter tends to be a big quarter for new deal signings, given that many IT departments try to exhaust their budget allocations before the end of a calendar year.

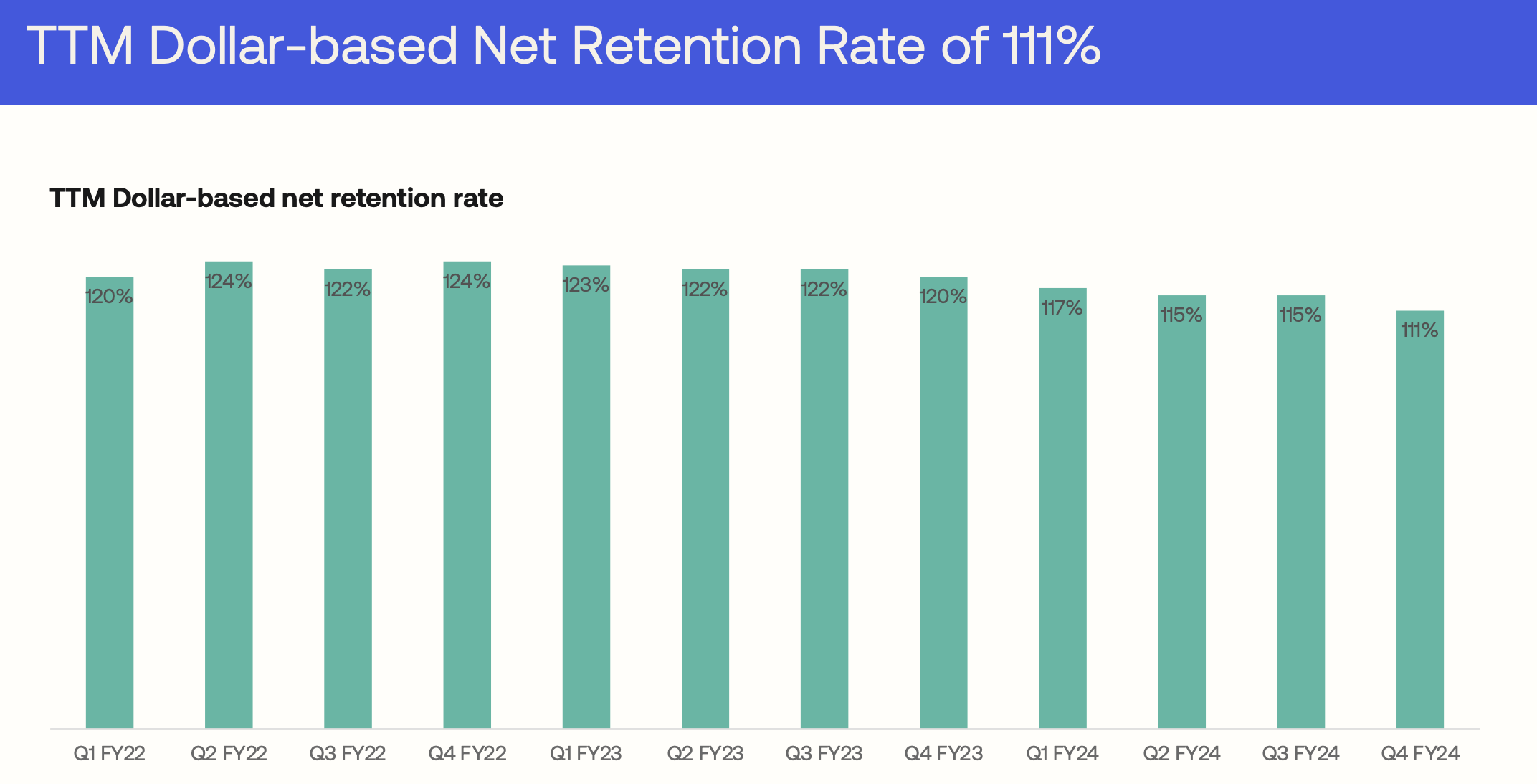

Not only that, but existing customers are also expanding at a slower pace. Dollar-based net retention dipped to an all-time low of 111%, reflecting both macro headwinds that are curbing seat expansion (as companies continue to lay off staff and slow down hiring, Okta's seat-based pricing products will suffer) as well as product upsells.

Okta retention rates (Okta Q4 investor deck)

Management believes that the overall environment remains "challenging." Here's further commentary from CFO Brett Tighe's remarks on the Q4 earnings call, detailing the company's latest go-to-market trends and its planned sales actions for the current year:

When analyzing our key metrics, we couldn't attribute a quantifiable impact from the security incident on our Q4 results. While not quantifiable, the event likely had some level of impact. We'll continue to monitor this as we move through FY '25. All things considered, our solid Q4 financial performance suggests minimal impact on our financial results stemming from the security incident. The macro environment during Q4 was relatively consistent with what we experienced in Q2 and Q3 of FY '24. In short, it's stable, but still challenging [...]

Now I'm going to address one of the actions we're taking to drive new business and reignite new customer acquisition. Starting at the beginning of this quarter, we shifted our direct sales team that focuses on the SMB market in the Americas to what's commonly referred to as a hunter-farmer model. That means we now have a team of account executives focused on driving new customer acquisition and a separate team of account executives focused on upsells within our installed base. We believe that we're still very underpenetrated within our existing base of nearly 19,000 customers. This natural evolution will enable us to drive better results with both new and existing customers."

We hope that these focused sales teams will be able to reverse the recent trend of both slowing customer adds and lower net retention rates, but this remains to be seen as we move through FY25.

Profitability was the main bright spot amid weaker customer metrics. Pro forma operating margins jumped 12 points y/y to 21%, up from 9% in the year-ago quarter. Note as well that the company announced layoffs covering 400 heads, or roughly 7% of its workforce, in early February, which should help boost margins over the long haul.

To me, there's more risk than reward in Okta when it's trading above $100. With observed slowdowns across revenue and all of Okta's customer metrics, I'd rather de-risk here and invest elsewhere.