A shot of a pipeline at sunset.

bjdlzx

A shot of a pipeline at sunset. bjdlzx

When I invest in businesses, the outlook for both the company and the industry are two factors that I don't take lightly. Of course, exceptional businesses in declining industries can still create wealth for shareholders. However, those are the exceptions to the rule in my view.

Statista

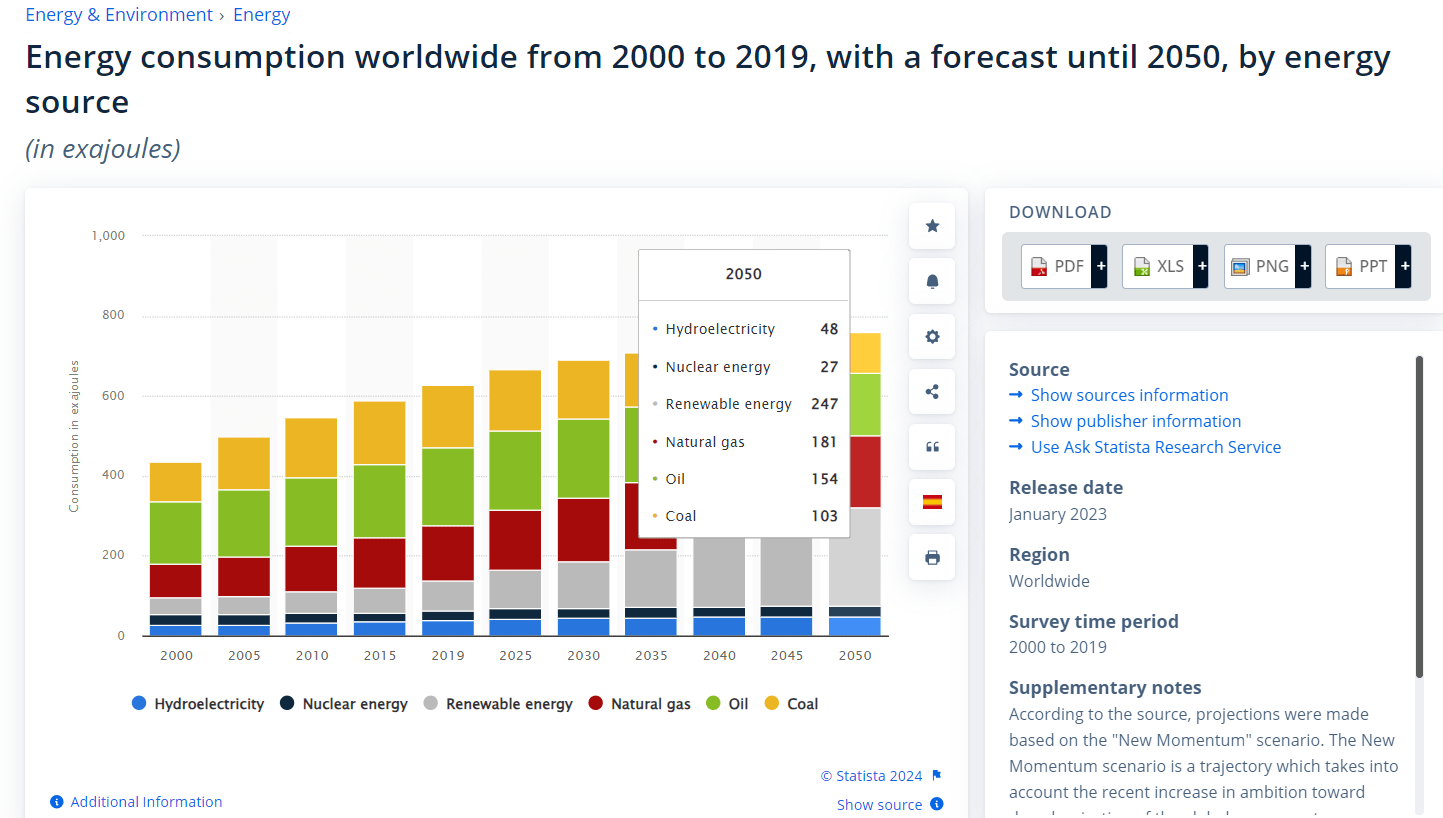

One industry toward which I am reasonably bullish is midstream operators, most especially natural gas-oriented midstream. The underlying basis for my optimism is simple math. As illustrated above, global energy consumption in 2019 was 628 exajoules. Of that, 140 exajoules, or 22.3% of global energy consumption, was made possible by natural gas according to Statista.

Global economic development is one element that will push energy demand higher over time. As more people ascend into the global middle class, they will have the modern amenities that many of us in economically developed nations take for granted.

Another catalyst for greater energy demand is that it's estimated the world will add approximately two billion people over that time frame, per the United Nations. Thus, total global energy demand is anticipated to rise to 760 exajoules by 2050. Thanks to the reliability, affordability, and abundance of natural gas, global consumption will rise to 181 exajoules or 23.8% of global energy consumption by that time, according to Statista.

One of the leading natural gas-focused midstream operators is ONEOK (NYSE:OKE), which comprises 2.3% of my portfolio, making it my fourth-biggest holding. A lot has happened since I initiated a buy rating in November.

For one, ONEOK upped its quarterly dividend per share by 3.7% to $0.99. Last week, the company also shared encouraging financial results for the fourth quarter ended Dec. 31, 2023.

The only event that has transpired in recent months to negatively impact my buy rating is the recent rally. Since my buy article, shares of ONEOK have produced a total return of 16%. This is ahead of the 13% total returns that the S&P 500 (SP500) generated in that time.

Today, I will be unpacking ONEOK's recent operating results and the valuation to explain why I am downgrading to a hold for now.

Dividend Kings Zen Research Terminal

ONEOK's 5.3% dividend yield is above the industry median of 3.8%, earning it a B- grade on dividend yield from Seeking Alpha's Quant System. Yet, this dividend appears to be built on a sound foundation, with a B+ safety rating from the Quant System.

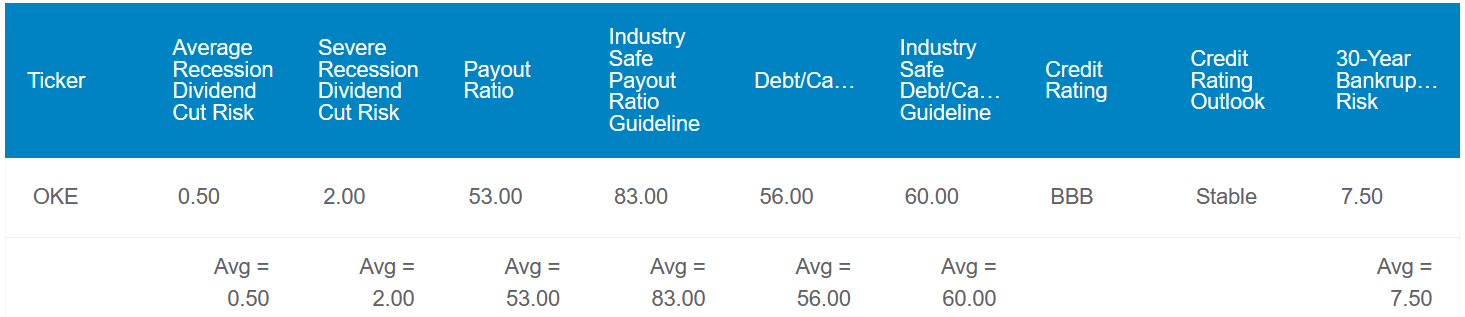

That is because the company's DCF payout ratio is 53%, which is far better than the 83% that rating agencies have set as the industry-safe figure. ONEOK's 56% debt-to-capital ratio is also just below the 60% that rating agencies prefer. Due to these reasons, the company's balance sheet is rated BBB on a stable outlook by S&P. That suggests the probability of ONEOK going bankrupt in the next 30 years is 7.5%.

According to Dividend Kings, the chance of a dividend cut in the next average recession is 0.5%. Even in a severe recession, the chance rises to just 2%. For context, these are both the lowest risks possible in the Zen Research Terminal.

Dividend Kings Zen Research Terminal

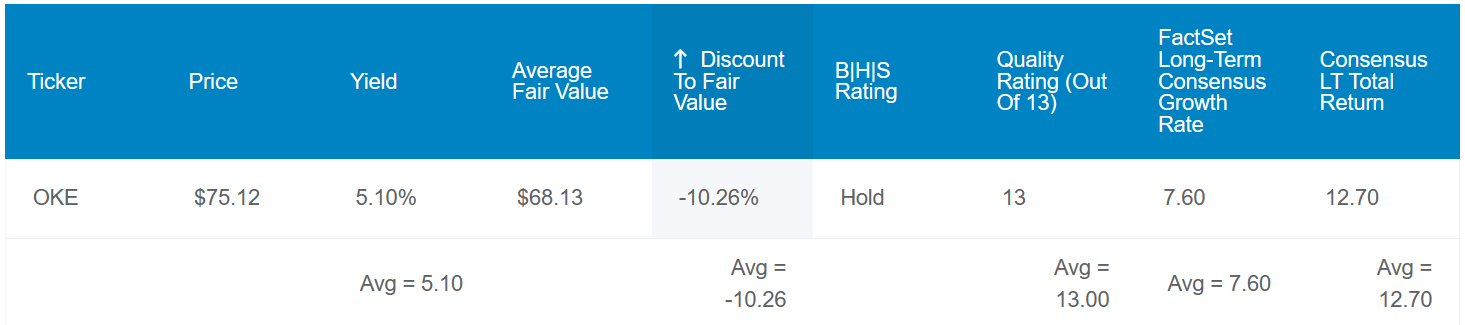

As I alluded to above, ONEOK's valuation is the one thing preventing me from maintaining my buy rating now. Using the five-year average dividend yield of 6.2% per Dividend Kings' Automated Investment Decision Score Tool, shares could be worth $64 each. The normal price-to-operating cash flow ratio in recent years suggests that ONOKE's shares could be fairly valued at $71 apiece. Relative to the current $77 share price (as of March 4, 2024), this means the midstream operator could be 13% overvalued against the average $68 fair value estimate.

If OKE returns to fair value and can put up the growth expected, these are the total returns that it may post in the coming 10 years:

ONEOK Q4 2023 Earnings Press Release

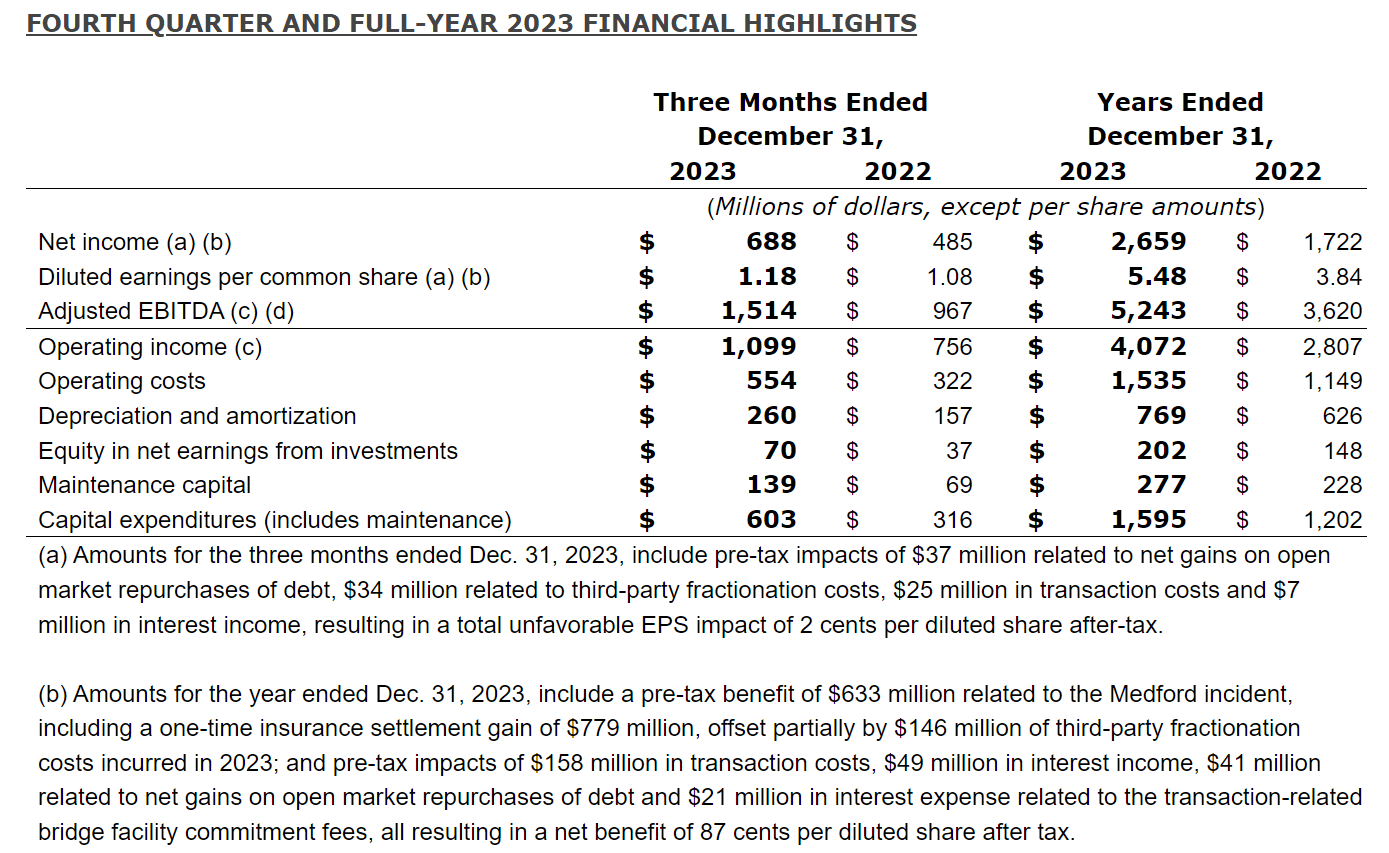

From my perspective, ONEOK's operating results for the fourth quarter were impressive. The company's net income surged 41.9% higher year-over-year to $688 million in the quarter. ONEOK's adjusted EBITDA soared 56.5% higher over the year-ago period to $1.5 billion during the quarter.

Even digging into more detail, the midstream operator's results were still solid. Adjusting for the higher share count tied to the acquisition of Magellan Midstream Partners last September, diluted EPS climbed 9% higher year-over-year to $1.18 for the fourth quarter. Speaking of the acquisition, a new segment was added due to it: The Refined Products and Crude segment.

Backing out the $424 million boost to adjusted EBITDA from the segment, adjusted EBITDA would have grown by 12.7% over the year-ago period in the quarter.

How did ONEOK's legacy business deliver such respectable results in the fourth quarter? Well, it was a multi-faceted effort to deliver such results to shareholders.

One of the things that stuck out to me during the Q4 2023 Earnings Call was the remarkable growth that has continued in the Rocky Mountain region. ONEOK's NGL raw feed throughput volumes rose by 20% year-over-year during the fourth quarter. The promising overall demand for natural gas that I cited earlier is being met by increased production in the region.

Over the years, ONEOK has expanded its total pipeline network from 30,000 miles in 2013 to 50,000+ in 2023 per CEO Pierce Norton's opening remarks. That is how NGL volumes have compounded by 20%+ annually in the past five years, and natural gas processing volumes have grown by 10% annually.

The Gulf Coast/Permian region also benefited from 17% NGL raw feed throughput volume growth for the fourth quarter. Lastly, natural gas volumes processed rose just as much in the period.

Moving forward, the company believes that its operating momentum to close out 2023 will carry into 2024. ONEOK thinks that adjusted EBITDA will climb by around 16% in 2024 to a midpoint of $6.1 billion.

A couple of tailwinds cited by management have me convinced that this is a reasonable estimate for the year. For one, volume growth was robust to conclude 2023. Including the Magellan acquisition, well connects were up 54% in 2023 versus 2022. This means that as producers keep growing production, more volume will flow through ONEOK's infrastructure.

ONEOK Q4 2023 Earnings Presentation

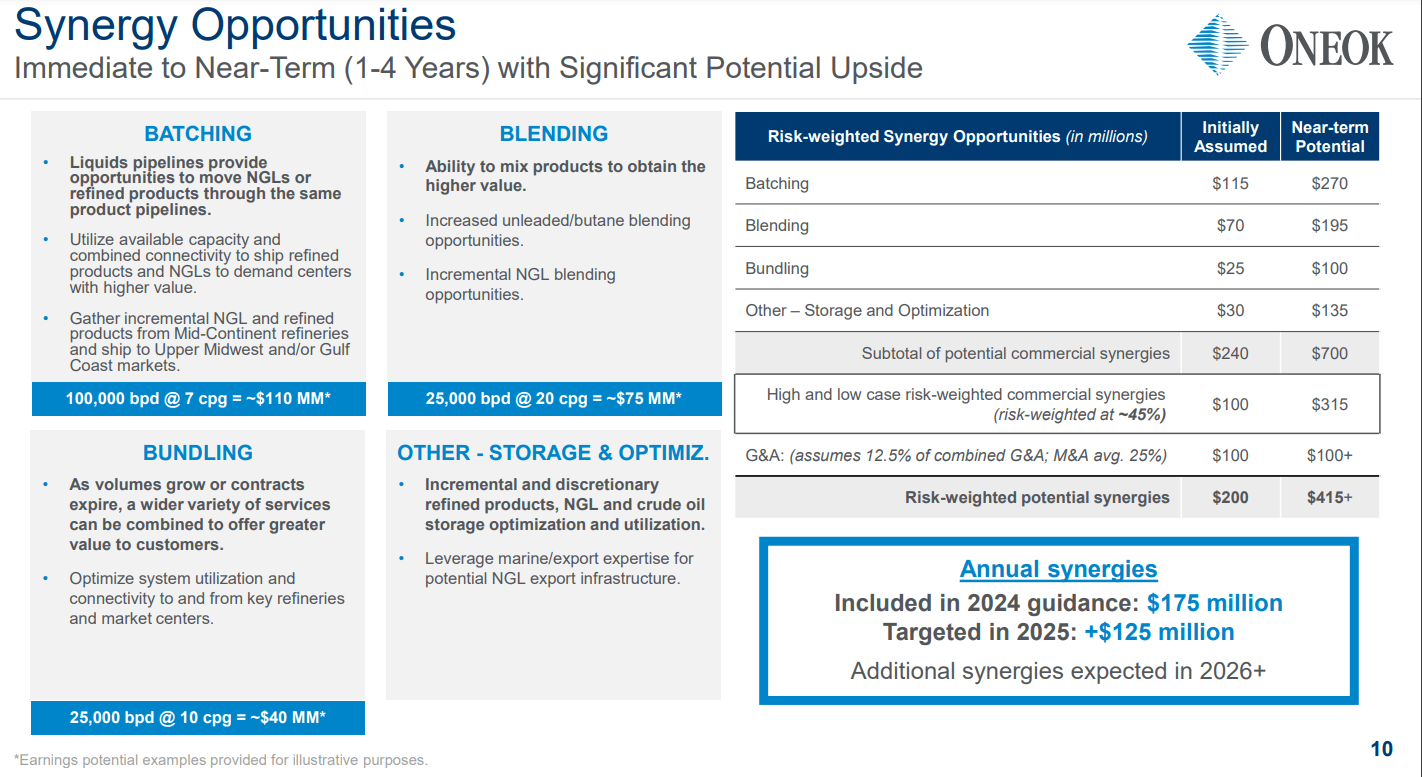

According to Executive Vice President Kevin Burdick's remarks during the earnings call, the completion of the Magellan merger also eliminated public company costs. As the company also cross-sells products to offer more value to customers, that is another synergy that could be achieved. This is why ONEOK thinks that $175 million in synergies can be realized in 2024, with another $125 million in 2025, and more to follow in 2026 and beyond.

Combined with investment opportunities and volume growth, that's why the future appears to be bright for ONEOK. That includes the Elk Creek Pipeline expansion to 435,000 barrels per day, which the company anticipates will come into service in Q1 2025.

ONEOK's debt load also looks to be under control. As of the fourth quarter, the annualized net debt-to-EBITDA ratio was just under the long-term target of 3.5, at 3.46. The company also had no borrowings on its $2.5 billion credit agreement and a $338 million cash balance, which should provide it with ample liquidity (unless otherwise noted or hyperlinked, all details were sourced from ONEOK's Q4 2023 Earnings Press Release and ONEOK's Q4 2023 Earnings Presentation).

ONEOK's 3.7% dividend increase indicates that dividend growth is ramping back up. For additional perspective, this was the biggest dividend raise since a 3.8% bump in the quarterly dividend per share to $0.825 in 2018.

ONEOK Q4 2023 Earnings Presentation

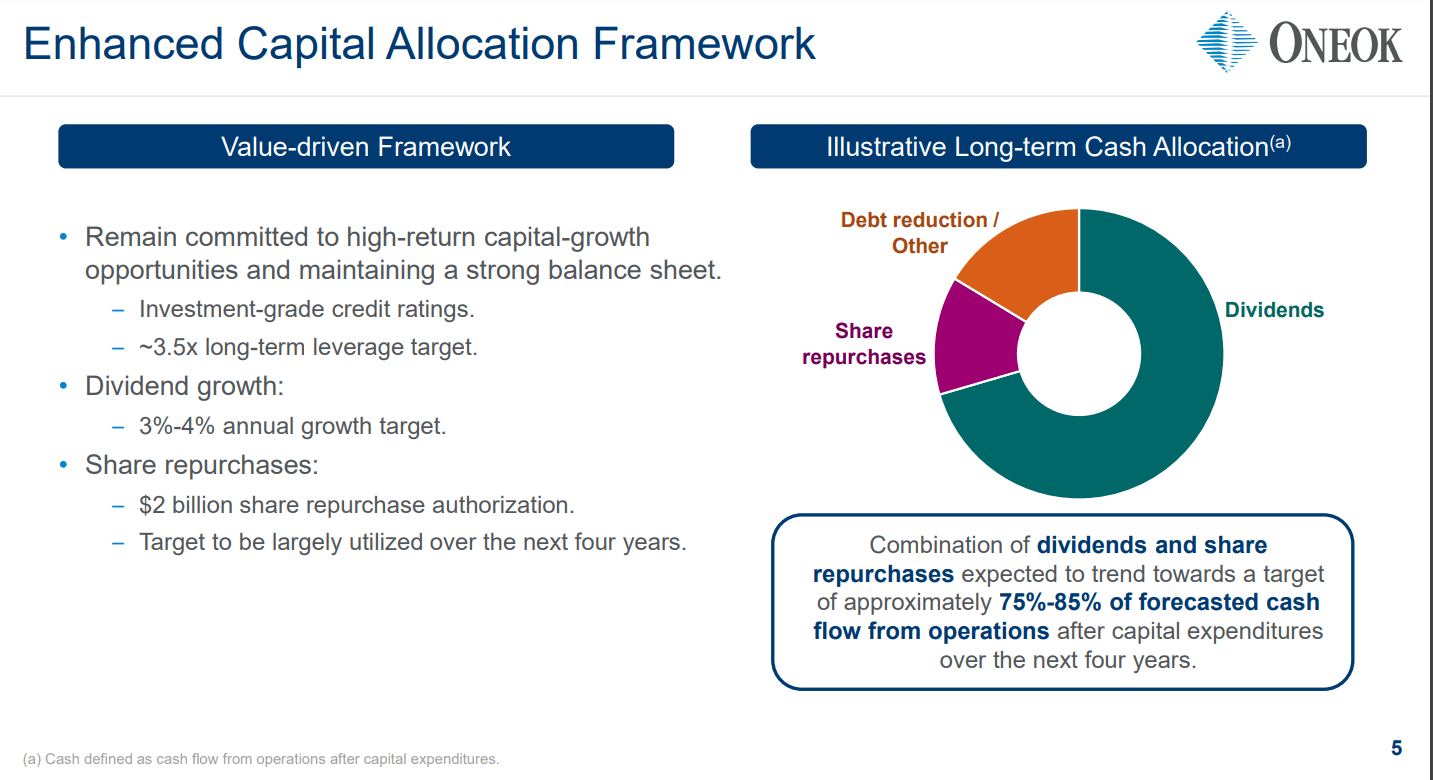

This should continue in the years to come. That's because the company is targeting 3% to 4% annual dividend growth for the foreseeable future. ONEOK is forecasting that between 75% and 85% of anticipated operating cash flow after capex will be committed to the dividend and share repurchases.

As a result of this ample operating cash flow, ONEOK projects that it will complete its $2 billion share repurchase authorization in the coming four years (info according to ONEOK's Q4 2023 Earnings Presentation). For a company with a roughly $45 billion market cap, that's not an insignificant buyback program.

ONEOK's recent results and outlook both convey that the company is doing quite well, but there are still risks to the investment thesis.

One risk has to do with the potential for regulatory and legal setbacks with ongoing growth projects. If any of the company's major projects run over budget or hit legal snags amid environmentalist opposition, that could hurt growth prospects.

As I noted in my previous article, another concern to watch is counterparty risk. According to slide 16 of 25 of the Q4 2023 Earnings Presentation, the company estimates that 85% of its anticipated earnings will be fee-based in 2024. That builds stability into its results, with one caveat. If the operating environment for its customers is unfavorable (e.g., a natural gas/crude oil industry downturn), some may not meet their financial obligations to ONEOK. That could weigh on the company's operating results.

ONEOK is a leading operator in an industry that won't be going anywhere anytime soon. The company's latest operating results prove this to be the case, in my opinion. Finally, I appreciate the investment-grade balance sheet and adequate liquidity.

But until shares of ONEOK come back down closer to fair value, I will be merely hanging onto my shares and not adding. If a selloff happened, shares became more valuable based on fundamentals, or some combination of those two happened, I would be open to buying a bit more. In the meantime, that's why I am downgrading ONEOK to a hold now.