nevarpp/iStock via Getty Images

nevarpp/iStock via Getty Images

Happy New Year! I hope that you are doing well. Last year was a challenging year for the partnership with respect to performance. I am not going to make any excuses or blame any external forces for these results. I accept full responsibility for my decisions and the outcome. I am writing this letter from a place of humility, because frankly there was a lot to be humble about.

Despite these humbling results, I remain highly confident that the partnership faces a bright long- term future. Humility is not the opposite of confidence - arrogance is. One of the greatest challenges in investing is to balance humility with confidence.

What gives me this confidence? I strongly believe that my investment process, which has had many years of success prior to the last couple of years, is as relevant as ever. If anything, I have improved it, and myself as the investor implementing it, from recent experience in ways that I will share with you later in this letter.

I also don't think that the markets have fundamentally changed in a way that skillfully applied value investing no longer works. The rapidly changing human psychology which drives the wild gyrations in market prices is the same as it has been for many decades. And while I do think some things have changed and require appropriate adjustments as I will elaborate shortly, the core tenet that prices can and do disconnect from fundamental business value in ways that can allow a thoughtful investor to generate excess returns through hard work has not.

Allow me to end this introduction with some thoughts on my own psychology and mental state. Faced with such challenging results, many investors would go on tilt. They would deviate from their process in one of two ways. Either, they would swing wildly for the fences trying to desperately "catch up," perhaps cynically figuring that if the last Hail Mary pass doesn't work it won't matter anyway. Or, they would become shell-shocked and fearful of taking any risk, no matter how well- considered, for fear of making a mistake.

Let me assure you that I am in neither of these mental states. I am going to continue to focus on my "true north" - the investment process that I outlined to you in the Owner's Manual. At the same time, I will be, and have been, learning from my experience to improve it further from first principles. I have been, and will continue to make new investments, as I will describe to you momentarily, taking well-calculated risk when warranted, but staying disciplined to not stray from the process.

The last couple of years have been challenging. I have always told you that I view my temperament as one of my biggest sources of competitive advantage in investing. My hope is that the rest of this letter and my actions over time during a tough period will demonstrate that. Onwards, to what I strongly believe will be a better and more profitable future for the partnership.

| Light Gray: thesis is tracking roughly in-line with my base case Orange: thesis is tracking somewhat below my base case Red: thesis is tracking significantly below my base case Dull Green: thesis is tracking somewhat better than my base case Bright Green: thesis is tracking significantly better than my base case White: No data |

| The portfolio was priced at 85% of Base Case value and at 69% excluding cash at the end of Q4 Option-adjusted net exposure was at -3%, reflecting option-based hedges Cash and equivalents were 52% at the end of the quarter, and weren't a reflection of market timing, but rather a temporary residual of the bottom-up investment process |

"Knowing" things isn't always enough. Sometimes you must experience them personally to viscerally understand them. When that happens, your mind truly internalizes the knowledge that was already there.

As the saying goes, fools learn from their own mistakes while smart people learn from those of others. With that in mind, here are my sometimes-painful lessons that I relearned during 2023:

I always paid attention to management quality. My criteria of competence and alignment haven't changed. What has changed is how much emphasis I put on management.

The typical management team has the following attributes:

Slightly above-average is just not good enough. It's hard to think of material long-term wealth created by management teams that fit the above characterization, or even by ones that are one notch above. I challenge you to find multiple counterexamples over 20+ year periods.

Of course, one can bet on a reversion to the mean of a deeply undervalued stock that doesn't require long-term company greatness for attractive returns. The problem with that is that mediocre management can mess that up as well. What you end up with then is just a cheap stock with no reason for that situation to change, and little-to-no direct capital return to allow shareholders to benefit without the market's re-rating. In short, a classic "value trap."

Expensive stocks can stay expensive for a long time. Or they can get even more expensive. Usually there is some story that people psychologically buy into, and it is very hard to know when the herd will decide to change its mind.

You might think that fundamental developments might do it. However, think about a stock that is trading at 50x earnings. It usually trades at those levels because the current growth rate is high and people extrapolate it into the distant future. That might be right, or it might be wrong. However, investors can choose to believe the story for as long as they wish, regardless of any logic to the contrary or any current results.

On the other hand, betting that the price is too crazy to be sustainable simply on excessive valuation is a bet where time is against you. The worst part is that you can eventually be proven right, but still lose money. I concluded, after painful experience, that it is just too hard for me.

I was researching, and getting close to investing in, a company with a good business and impressive owner-oriented management with a track record of success. Then one day I woke up to see that the Board had just fired the CEO.

In the public back-and-forth that followed between the CEO, the Board and various shareholders, all kinds of things came out that I had no idea were happening. Apparently according to the Board the CEO was under-delivering on organic growth. Supposedly he pushed the Board to make large acquisitions outside of the core competency of the company. And so on.

I am not sure if we will ever know the truth, but what was shocking is how none of this was known to the shareholders despite it, supposedly, having been going on for multiple years. The next time you listen to management on an earnings call or read some bland statement from a Board, think about that. And wonder how much what they are saying publicly reflects what is really going on.

When learning how to interview, I was taught that data suggests that hypothetical questions are useless, and the only thing that has predictive power is what people had done in the past. In other words, you shouldn't be asking "How would you…?" but rather "How did you…?"

In the absence of a track record of accomplishment, you should take a CEO's plans as hopeful intent. That doesn't mean they are lying, just that we really don't necessarily know what they can or cannot do. There is a particular danger if they use language that resonates with you. More than once in my investment career I fell for someone who said all the right things, except that they hadn't done them - in the past, nor as it turned out, would they - in the future.

Psychological pain tolerance isn't something that you can assess about yourself until you experience the pain. Nor can you know how others will behave during periods of adversity - either theirs or your own.

The good news is that sometimes others will positively surprise you. They will be generous and supportive during tough times, perhaps more so than can be reasonably expected. Others will act predictably as fair-weather friends.

The biggest learning isn't about others - after all, you can choose whether to keep associating with them. It's about yourself. If what you learn surprises you to the upside, then you can be proud of having weathered tough times with grace and resilience and use that as a source of well-deserved strength in future endeavors.

The tribe of value investors is small and dwindling. Some think it is or it should be on its way towards extinction. Others are seeking to redefine its identity.

It has an unofficial chieftain, Warren Buffett, its most famous and successful member. I have lost count of how many times someone has blindly quoted him in an argument, or implied that an investing action is correct because it is similar to ones taken by him.

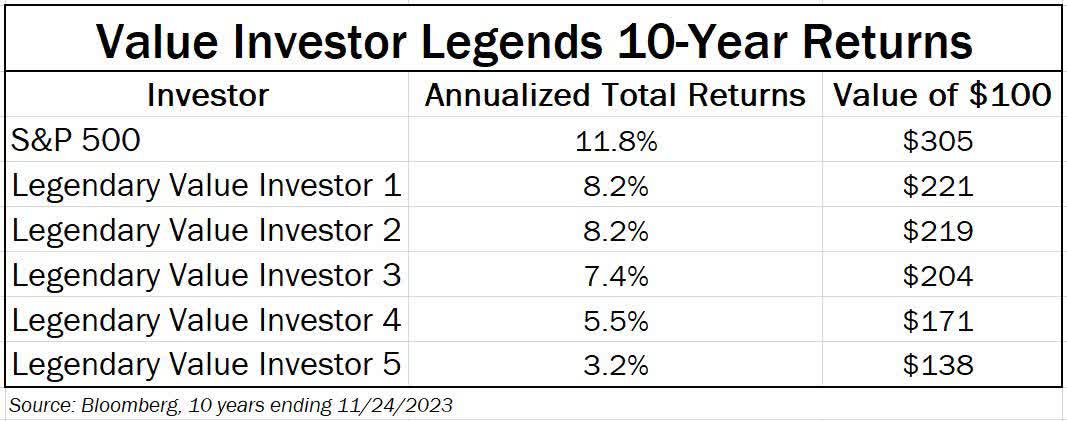

Members of the value investor tribe are facing a difficult choice. On the one hand, a core tenet of value investing is discipline and sticking to a well-defined process. On the other hand, the last decade or so hasn't showered value investors with much success. Certainly not compared to decades prior when successful practitioners had handily beaten the markets.

Let me paint a picture of how bad things are.

The table below presents the results of 5 value investing legends over the last decade. These are people managing billions of dollars. Some have written books. Others have made frequent TV appearances. You would know all their names if you were a member of the value investor tribe.

What's more, at the beginning of this decade these people had something that most other tribe members did not have: a clearly-articulated value investing process with 10+ years of successfully implementing it to beat the stock market at scale.

And yet, as you can see from the table, not one of them has come close to beating or even matching the market.

You might think that I cherry-picked these investors to make a point. I did not. I am sure there are some value investors who did fine during the last decade but, let me assure you, that to the best of my knowledge the list above is fairly representative of the value investor experience managing meaningful pools of capital.

You might also think that maybe they all had a lot of overlap in their holdings, and it just happened that their group of stocks did poorly. Nope. These investors had different portfolios, had very different degrees of portfolio concentration and varied in the size of companies that they focused on.

So, what's going on?

The tempting explanation for someone looking to defend the tribe is that the last decade has been defined by a small group of large companies generating a disproportionately high percentage of the market's returns. That's true. However, if instead of using the S&P 500 index we were to use the S&P Midcap 400 index, it would still beat all of the value investor legends on the list. The S&P 500 Equal Weighted index would trounce the legends by an even greater margin, not that far off from the results of the S&P 500.

So no, we can't lay most of the blame on the Magnificent Seven, Amazing Five, Terrific Nine or whatever moniker du jour market watchers come up for the hot stock group of the moment.

Another theory is that a lack of a real recession in the last decade has deprived value investors of their time to shine. Value investors' focus on protecting against things going wrong typically allows them to do better during a recession and the accompanying market downturn. Furthermore, the fear that accompanies this part of the cycle allows us to plant seeds for the future by buying bargains not readily available during other times.

We had a blip of a recession during the COVID pandemic in 2020, which was quickly snuffed out by massive amounts of government intervention. That, in turn, inflated a market bubble in both stocks and bonds, driving risk appetites through the roof. As a result, we are ending the period in an environment where investment attributes valued by value investors are being underappreciated by the market, while the stocks of companies most in favor now are ones that don't fit the process of most value investors.

There is merit to this theory that a combination of not having a real downcycle in the sample combined with end-point bias of ending on a particularly challenging market environment for the value investing approach is creating a 10-year period that is not representative of most future decades in the market. However, it's hard to know how much of the underperformance is due to this versus more permanent causes.

What are some more troubling possibilities, at least if you are a member of the value investor tribe?

One theory is that the increasing dominance of passive investing is exacerbating stock market momentum and hurting value investors. Since most indices are market capitalization-weighted, once a stock goes up some, there is now a much greater pool of capital that is forced to buy it as new money is added to the funds than there was 10 or 20 years ago. This creates a reflexive spiral where the stock market winners keep going up because… they had gone up.

I think there is truth to this theory, but it's hard to know how much of an impact it has had. Besides, I am not ready to believe that the most efficient capital market in the world has become massively inefficient to the degree that there is a large and permanent disconnect between market prices and business values.

What other causes could there be for the challenges facing value investors?

Some years ago, Warren Buffett pointed out that the pace of business disruption has increased. That has two implications:

Let's examine each implication. The classic, Benjamin Graham-style circa 1940s, investing approach relies on finding companies whose securities would produce a high rate of return if their companies' future financial performance even approximately resembles that of the past. Analysis is performed to make sure that there are qualitative reasons for the stability of past financial results, and the future is looked at as a threat rather than an opportunity for extra profit.

Graham always stressed that cheapness of the security alone, or even cheapness compared with long-term historical profitability are not enough. However, Buffett's insight suggests a much higher rate of false positives for an investor applying the classical value investing approach. What would that look like?

You encounter a stock that is trading at a low multiple of the average profits over the past economic cycle. Not seeing any specific threat on the horizon, you, as a card-carrying member of the value investor tribe, purchase this stock. You believe the margin of safety lies in the fact that even if the future profitability is somewhat below the historical average, your returns will still be satisfactory given your low purchase price.

So, what's the problem?

If businesses can be disrupted much faster than before, then a much higher percentage of situations of the type described above can turn out to be bad investments. Their history no longer acts as a prologue to the future, and their future profitability may be drastically below that of the past. The low price relative to historical profits alone is insufficient to prevent permanent capital loss that value investors work so hard to avoid.

Conversely, if disruptors are likely to be more often successful than they had been in the past, and perhaps successful to a much greater extent, then the conclusion might be that you want to search for investment ideas among potentially successful disruptors rather than among cheap securities. Disruptors, by their very nature, rarely have a long history of financial success. When they do, their securities rarely trade at a low price relative to those historical profits given market expectations, perhaps justified, for much better financial performance in the future.

This approach is not in itself new. It has been successfully practiced by Philip Fisher in the 1940s and the 1950s, the same time period during which Graham successfully practiced his approach. The process for implementing it has also been known for a long time, laid out masterfully by Fisher in his Common Stocks and Uncommon Profits.

What is different is that the odds of success appear to have shifted from companies defending historical competitive advantages and profit streams to those attacking them with new business models.

So, the doomsday scenario for the value investor tribe can be summarized as follows:

However, all is not lost.

Proponents of the above theory reach the conclusion that analytical efforts should be spent on finding successful disruptors. That's not the only possible logical conclusion. If value investors can adapt by using better qualitative analysis techniques to find the smaller set of companies that have both defensible business models and cheap securities, that provides another path to success.

Let's not forget - the Philip Fisher style of investing is going to lead to many false positives and large losses as well. The winners are not normally distributed, but rather follow the same kind of power-law probability distribution seen in Venture Capital and movies. And what do we know about the distribution of returns in Venture Capital? There is a huge dispersion of returns between the best investors and the rest, and the median return isn't all that great.

In plain English - for every self-styled successful "compounder bro" publicly pounding their chest about their amazing business analysis skills and doing a victory lap, there might be many using a similar process with similar skill but with far inferior results. Except that those investors don't advertise their lack of success, so the selection bias makes you think that the overall approach is far more likely to lead to investing success than it really is. It also might lead you to falsely believe that the person doing the public victory lap can replicate their success for many years to come.

The value investor tribe has a choice to make. The way I see it, it is to:

I clearly favor the third choice. My conclusion, informed by the greater pace of business disruption, is that successful value investors should adapt by:

Incidentally, that's what it looks like the Tribal Chief, Warren Buffett is doing. Not that it makes it right or wrong. However, it's certainly interesting to note that the man who was early in recognizing this paradigm shift of greater business disruption has had his cash hoard growing in recent years. People all too often quote the well-worn quote of Buffett's that "it's better to buy a wonderful business at a fair price than a fair business at a wonderful price." The only problem is that that's not what the great investor actually does. He might say it to make the people selling their businesses to him feel better, but in reality he isn't looking to pay a fair price for anything. He is looking for one thing only: to pay a price for a predictable business highly likely to result in attractive returns.

Don't you think he knows plenty of large, wonderful businesses? You don't think that he believes that Visa (V) or Microsoft (MSFT) or pick any one of a number of successful blue chips that are widely owned these days are excellent businesses with good management? Of course he does. Why does he not own them? He doesn't think their price offers him an attractive enough rate of return relative to that of likely future opportunities. That's the only explanation for his growing cash hoard consistent with the facts.

We humans like simple answers. Good vs. bad. Hero vs. villain. The problems are all temporary and thus no change is required, or they are all structural and we are doomed.

The truth about the threats facing the value investor tribe is more complicated than that. Some factors depressing results are clearly temporary - we haven't had a real recession and downturn in a while, and the current endpoint strongly favors other approaches. However, other threats are real and require us to adapt to be successful. Not everyone is going to adapt, and of those who do, not everyone will choose to do it in the same way. However, ignoring the changed environment is not likely to be a successful option, for the environment is certainly more difficult to navigate than in prior decades, and thus requires not blind adherence to old rules, but thoughtful implementation of classic ideas in new ways.

I remain very cautious about the investment environment. Predicting what the economy will do or how markets will behave in the short-term is folly. However, being aware of the environment that we are investing in is wise. The frothier the markets and the economy the more cautious we should be, and conversely when a lot of fear is reflected in market prices, we should be excited to search for opportunities.

Many things in the markets oscillate from one extreme to the other. While we can't assume that historical ranges and averages represent some kind of immutable law from which there can be no deviation, often where things stand relative to long-term history can be quite informative. Lest you come away with the impression that my caution is based on some sort of "gut feel," here are some factors that combined make me believe that this is a very challenging time to find attractive opportunities:

All of the above notwithstanding, I don't make my investing decisions in a top-down way. Rather, I focus on bottom-up, micro-economic driven investing. One of you asked a follow-up question after last Fall's Annual Partnership Meeting: given how much cheaper I showed the U.S. small-cap stocks to be vs. large-caps right now, shouldn't I be able to find some good ideas among them?

I spent a serious amount of time going through ~ 1,700 U.S. small-cap stocks one at a time, using the same quality and price criteria I always do. The result was that a meagre 15 stocks, or less than 1%, made it into the top of my idea-generation funnel. That is a very small percentage, and all on a bottom-up basis.

None of this implies that an immediate market crash is in order. It does suggest to me that it's prudent to be very cautious and to maintain an appropriately high bar for new investments.

Babcock is a UK-based defense services company that is three years into its turnaround. Prior management pursued an aggressive acquisition strategy, which, when combined with misleading accounting has resulted in massive problems. The new management arrived in late 2020 and began the long journey to recovery.

I typically avoid early-stage turnarounds. While the upside usually appears large, what is less obvious but true on average is that the probability of achieving the turnaround is fairly low. The ideal time to invest in a turnaround is when substantial progress has already been made in key performance measures, but before all of the benefits have dropped to the bottom line and become obvious to the market. While the upside is somewhat less at this point than at the beginning of the turnaround process, that is more than compensated by the much higher probability of success and the shorter wait to achieve it.

Management is also crucial in any turnaround effort. In this case we have a CEO/CFO team whose prior role was successfully turning around another UK defense company. While that is no guarantee of success, having management which has done it before is a major plus.

So far, the management team has cleaned up the balance sheet, divested non-core assets, identified the issues that were depressing margins in the core business and outlined a plan for achieving long-term targets that appears reasonable. Additionally, I did a research call with a former employee who suggested a culture of competence and execution under the new leadership. None of this is a guarantee that the turnaround will happen, but these things tilt the odds in our favor.

I bought a small position in the stock at about 65% of my Base Case value estimate. The upside to the Best Case is a triple, while the downside to the Worst Case is under 30%. The stock is trading a high single digit P/E on my estimate of normalized EPS. The balance sheet is at a sustainable level of leverage with Debt/EBITDA below 2.5x, and management recently reinstated a dividend.

I judge this to be an above-average quality business due to the fact that in a good portion of revenue base it has unique capabilities and operates in a very concentrated oligopoly for services which are a must, especially in an increasingly dangerous world. My assessment is that management is also of above-average quality due to its prior track record, former employee feedback on the culture, and the transparency with which it communicates with investors.

Investing in Aimia was a mistake, and I take full responsibility for it. I incorrectly extrapolated management's prior track record of beating the market while running an investment management firm into an assessment of them being good stewards of capital in a different setting. Furthermore, I only had evidence of a moderate amount of excess return generation and none of high integrity that I should have required in choosing to invest in a company whose primary goal was to be a long- term investment vehicle.

Integrity is where the issues arose. Perceiving itself under attack by an activist investor trying to take over the company, management engaged in what they called a "strategic" transaction which meaningfully diluted other shareholders. The transaction could only be called strategic if the strategy was to entrench management at the expense of other shareholders. Otherwise it looks a lot like they were just giving away very cheap stock, based on their own recent assessment of intrinsic value, just to bring in some new investors with some perceived pedigree to the Board.

Presumably the goal was to get more stock in the hands of friendly investors who would vote for them given the prior, very close, shareholder vote which they almost lost.

I of course don't know all the details, but it looked a lot like self-dealing to me - using our funds to benefit management rather than all of us. Once I have reason to question management's integrity, nothing else matters. I exited our position gradually over the subsequent month at a small loss.

After our exit, the CEO and COO were forced out and new management took over. At this point I don't have any reason to get re-involved.

I have learned a painful but useful lesson which has caused me to upgrade my investment process to set a higher bar for management research and assessment before getting involved. That is especially true when the primary plan is for management to redeploy rather than return a lot of the company's cash flow.

Reducing a position from a large to a small size is no trivial decision, and I didn't take it lightly. OI became a large position after starting out as a medium position that appreciated following well- priced purchases in the depths of the COVID fears. Maintenance research is important, as is trying to debias myself as much as possible, especially on investments that I have owned for a long time.

With that in mind, I decided to do some additional digging and did a couple of research calls with former and current customers. What I learned was on the margin unfavorable relative to my prior thesis. What I thought would be a permanent increase in European margins, albeit not all the way to the current peak margins in that segment, appears to be wishful thinking on both my part and the management's. My conversations suggested that there was no structural improvement in that business, and the increase was due to cyclical dynamics surrounding the natural gas price spike and the subsequent price increases.

Furthermore, in the U.S. where margins are depressed, while there is a strong likelihood of margin increases, it's now less clear that they will return all the way to their historical levels. That is because the current weak margins are due to overcapacity driven by substitution in beer to aluminum cans, and even with that shift largely done it will take a number of years to use up the spare capacity.

In short, my assessment of both revenues and margins came down, resulting in a lower range of profits and values. It also became clear that far from being ready to step up and buy stock now that the company's balance sheet was in good shape, any buybacks would likely be small and delayed if the profits were to cyclically decline in the short-term, as seems likely to be the case.

With all of that in mind, I looked at OI through the lens of the same criteria that I would use to size a completely new position. As unpleasant as it was to see, that made it clear that objectively the investment merited a small, rather than a large, position size. Remaining disciplined to my investment process, I reduced the position.

I let our remaining call options expire in January, and have not replaced them. The company is now a turnaround that is dealing with a stretched balance sheet and a potential recession. I have not yet been able to discern material evidence that the turnaround is already succeeding. Meanwhile, if the cycle were to occur sooner and be deeper than currently expected, the equity would quickly become worthless.

It's tempting to double-down on one's bets especially when there is such a huge amount of upside if the company is able to turn itself around and avoid bankruptcy. After all, there is still the chance of the equity being worth $10+ vs. the under $1 share price. However, merely being lured by the large upside is a mistake - lottery tickets also have huge upside relative to the price paid, but they are known for their negative expected value. At this point I don't have any differentiated insights that would allow me to assign probabilities better than the market to the various scenarios, and so I am going to avoid gambling and pass.

I will keep monitoring the situation and if there are signs that the turnaround is succeeding, I would be happy to revisit my decision even at a much higher price. In turnarounds, the best expected return is usually obtained when the odds have shifted in the company's favor even if the upside has been reduced.

As I have committed to do in the Owner's Manual, I will use these letters to provide answers to questions that I receive when I believe the answers to be of interest to all of the partners. This quarter I received two questions that I wanted to answer for everyone's benefit. Please keep the questions coming; I will do my best to address them fully.

Since you showed U.S. small capitalization stocks to be much cheaper than large capitalization stocks and at a reasonable absolute P/E ratio in your Annual Meeting presentation, aren't there some good investments within that group that you can find?

I took this question seriously and as I summarized earlier in this letter did substantial work to check its premise on a bottom-up basis. I used the following criteria for adding a stock to the top of my idea generation funnel:

I believe that these criteria are appropriate and neither too tight nor too loose. I certainly expect that they will miss some investments that if one were to do a deep dive into would prove to be attractive. I also understand that a number of investments will pass the above checklist and will still not prove to be attractive enough upon deeper examination. However, for the purposes of screening through a large list of potential opportunities I believe these criteria to be approximately right.

I found only 15 companies that meet these criteria out of all U.S. small caps. That is less than 1% - a very low number. How do I reconcile that with a reasonable P/E ratio for the index as a whole? I believe it to be a combination of:

Do you intentionally aim to have all or mostly small capitalization stocks in your portfolio? Is that designed to make it appear different or help you market the fund?

First, one of the major premises behind starting Silver Ring Value Partners was to not do anything with respect to investing for marketing reasons. That is very different from most of the industry, with its "style boxes," portfolios filled with household names that managers won't be blamed too much for owning, over-diversification that nearly guarantees a mediocre outcome at best and so forth.

I understand the point of the question, however, as I have encountered managers who deliberately try to make their portfolios look exotic in the hopes of marketing themselves as totally different than anyone else. This seems to be particularly true of those trying to sell their services to institutional allocators who seem to have a special predilection for managers that come across as investing in a unique niche.

That is not what I am doing. My goal is to apply my process in a disciplined way, from first principles. The process has certain qualitative requirements for companies - these are more usually met among larger companies since these tend to be on average better businesses. It also has certain requirements for the degree of mispricing of each stock - this tends to be easier to find among lesser known companies, at least on average.

So the two factors above tend to pull in different directions with respect to what size companies eventually fit both my qualitative and quantitative criteria. Next, we need to consider that there are three to four times as many small cap stocks than large cap stocks, at least in the U.S. So if one is truly unbiased with respect to size and not constrained by too much in assets under management, then I believe that a portfolio constructed from first principles will frequently have a reasonable portion invested in smaller companies.

However, that is a byproduct of the process, not its goal. My high-quality company hunting ground that I described to you in earlier letters of about a thousand companies has a median market capitalization of about $5 billion. I have owned companies with a market capitalization as small as $50M and as large as $100B and expect to have a wide range of market capitalization companies in the portfolio over time with the mix determined by opportunity not by optics.

I encourage you to consider the results summarized below in conjunction with both the investment thesis tracker as well as the discussion of the individual companies in this letter. Any investment approach that is judged over less than a full economic and market cycle is liable to appear better than and worse than it really deserves at different points. Ultimately, it is the quality of the investment process and the discipline with which it is implemented that determines the long-term outcome. Therefore, I strongly encourage you to focus on process over outcome in the short-term.

I track a number of metrics for the portfolio to help me better understand it and manage risk. I track these both at a given point in time, and as a time series to analyze how the portfolio has changed over time to make sure that it is invested in the way that I intend for it to be. Below I share a number of these metrics, what each means, and what it can tell us about the portfolio. As time passes, you should be able to refer to these charts and graphs to help you gain deeper insight into how I am applying my process.

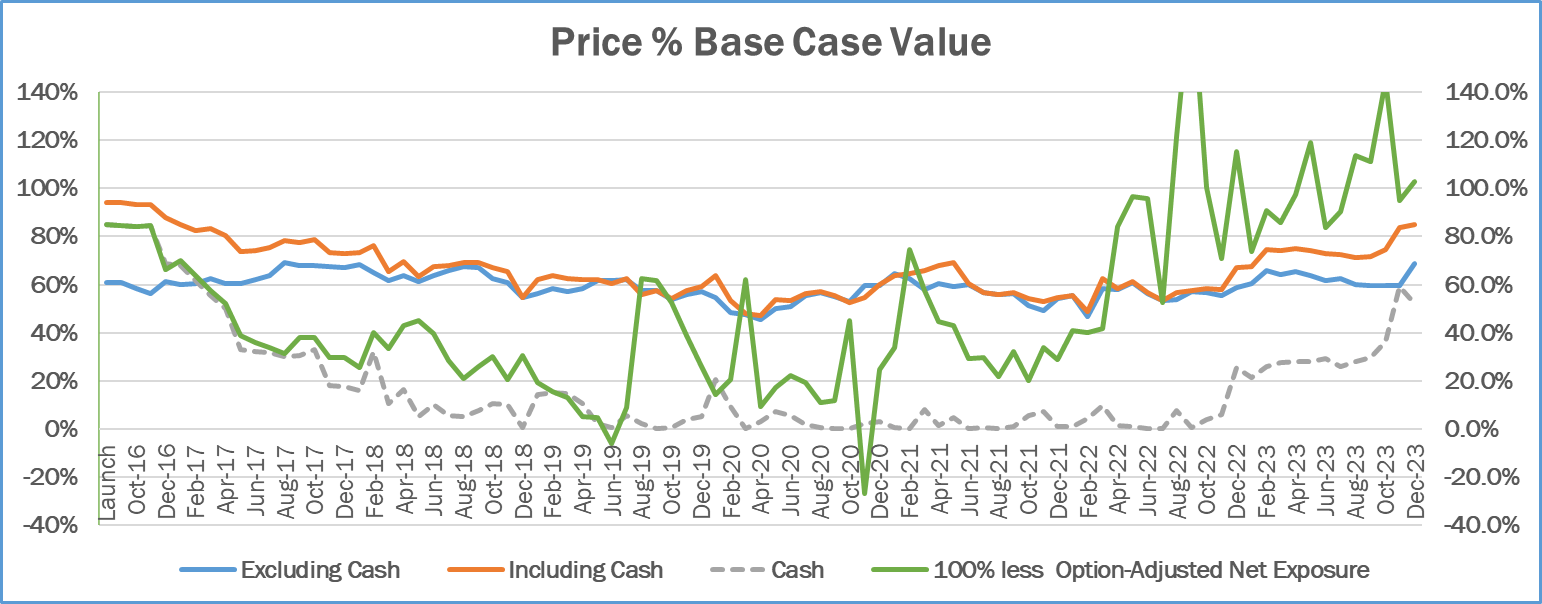

This metric tracks the portfolio's weighted average ratio between market price and my Base Case intrinsic value estimate of each security. This ratio is presented both including cash and equivalents, which are valued at a Price to Value of 100%, and excluding those. All else being equal, the lower these numbers are, the better. Excluding cash and equivalents, a level above 100% would be a red flag, indicating that the portfolio is trading above my estimate of intrinsic value. Levels between 90% and 100% I would characterize as a yellow flag, suggesting that the portfolio is very close to my estimate of value. Levels between 75% and 90% are lukewarm, while levels below 75% are attractive.

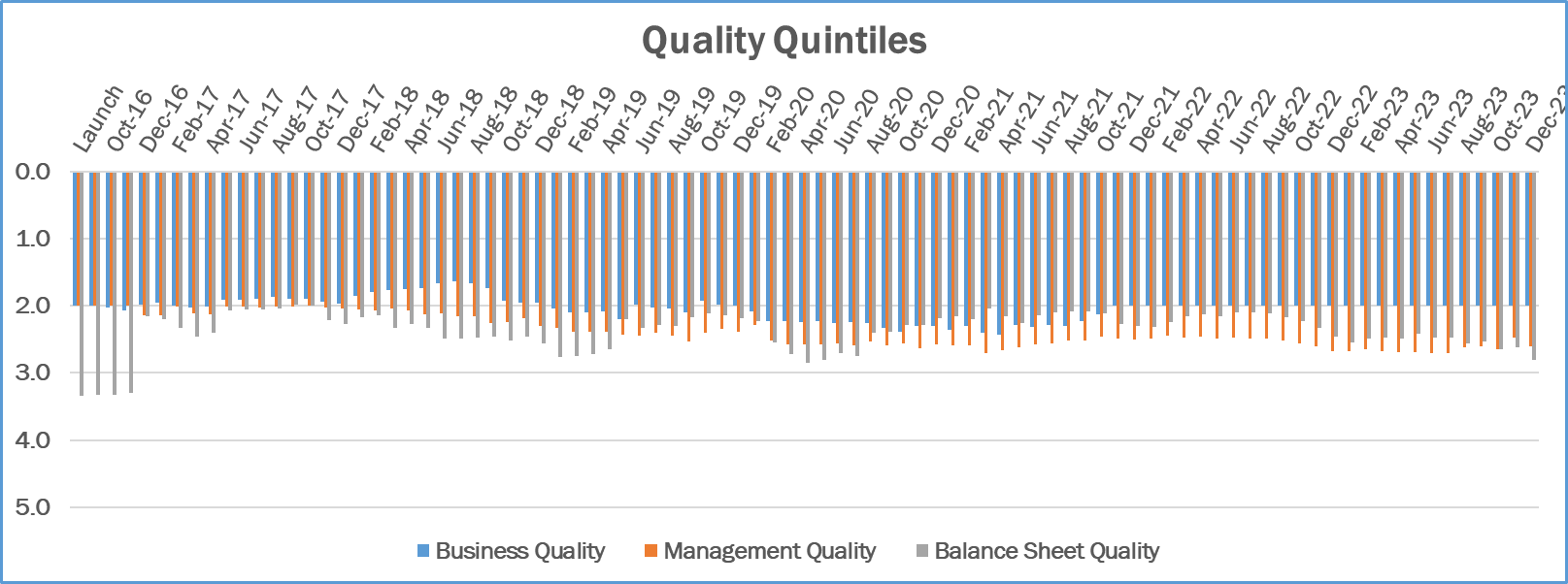

As outlined in the Owner's Manual, I evaluate the quality of the Business, the Management and the Balance Sheet as part of my assessment of each company. I grade each on a 5-point scale with 1 meaning Excellent, 2 Above Average, 3 Average, 4 Below Average and 5 Terrible. The chart that follows presents the weighted average for each of the three metrics for the securities in the portfolio.

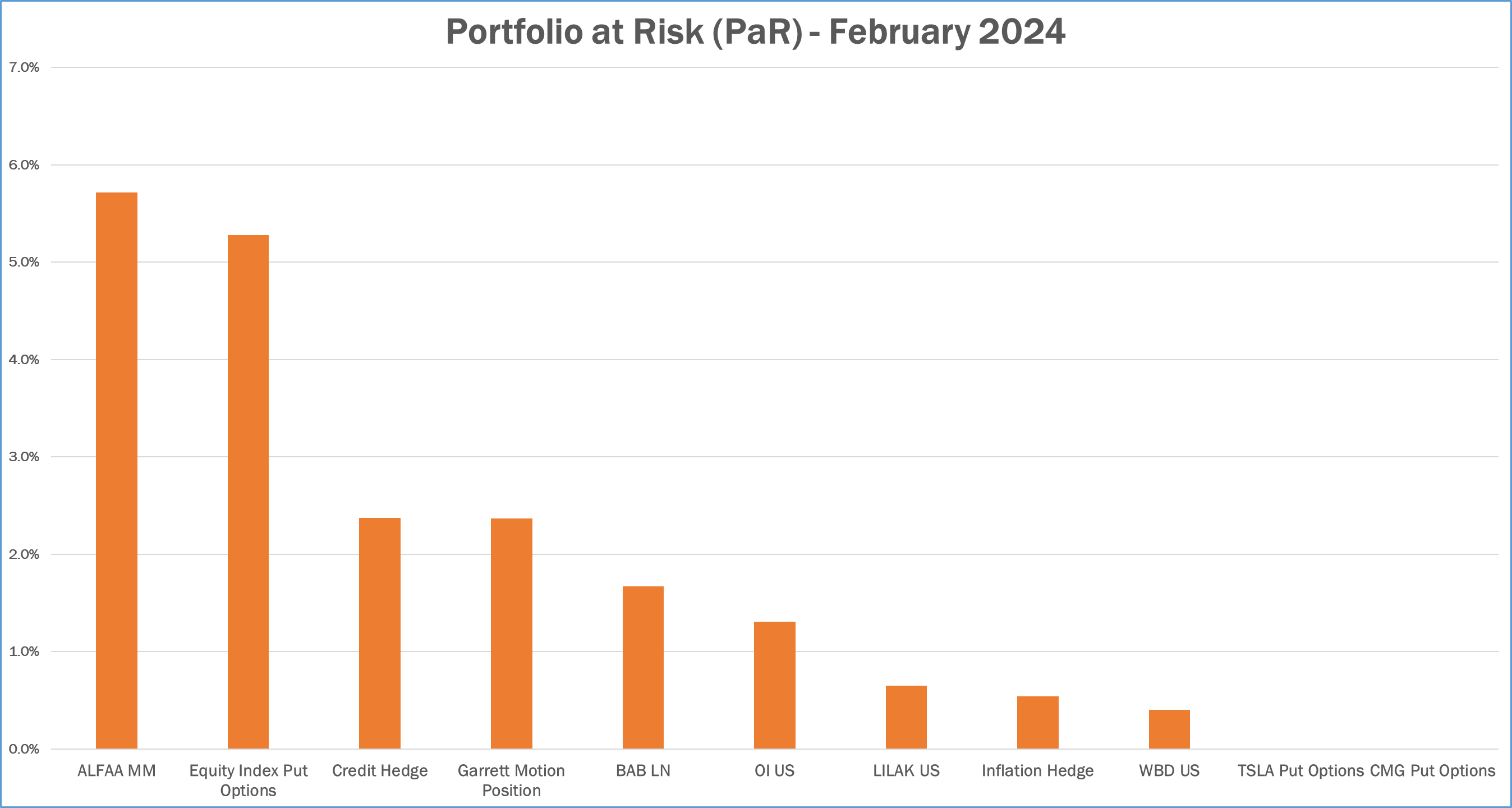

I estimate the Portfolio at Risk (PaR) of each position by multiplying the weight of each position in the portfolio by the percent downside from the current price to the Worst Case estimate of intrinsic value. This helps me manage the risk of permanent capital loss and size positions appropriately, so that no single security can cause such a material permanent capital loss that the rest of the portfolio, at reasonable rates of return, would not be able to overcome. I typically size positions at purchase to have PaR levels of 5% or lower, and a PaR value of 10% or more at any time would be a red flag. The chart below depicts the PaR values for the securities in the portfolio as of the end of the quarter. Positions are presented including options when applicable.

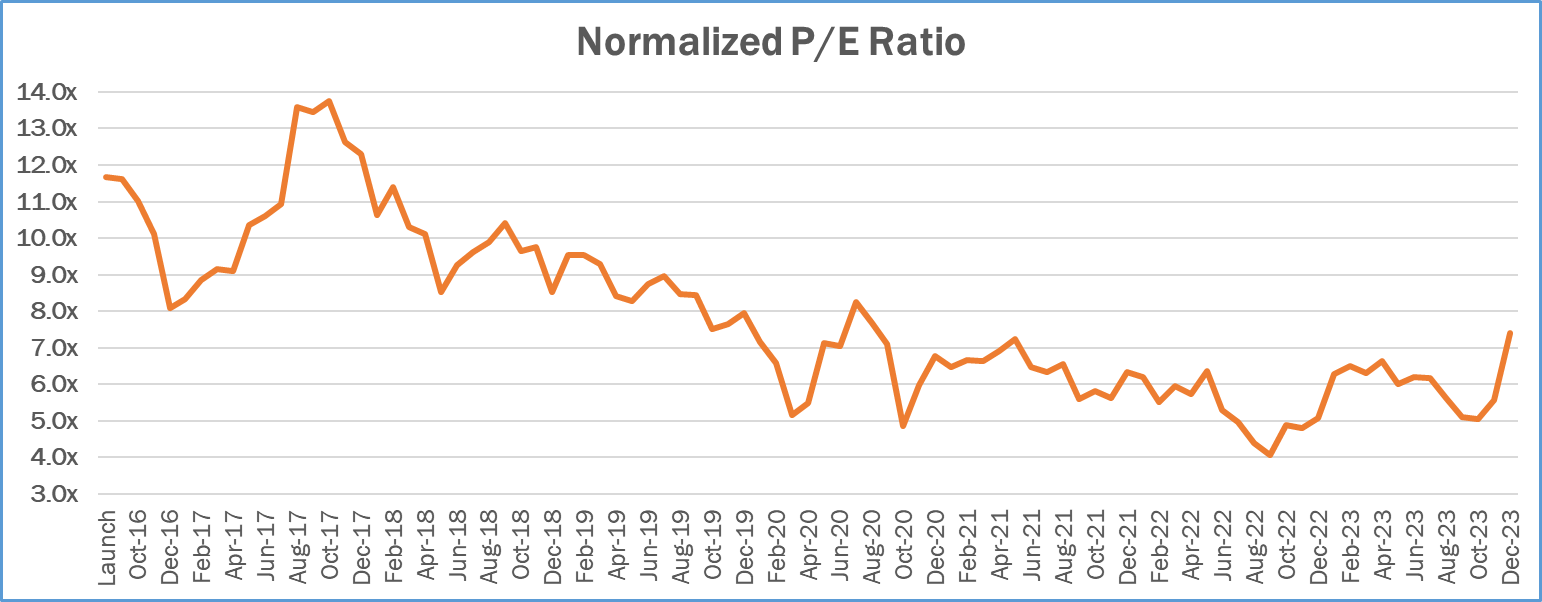

I supplement my intrinsic value estimates, which are based on Discounted Cash Flow ('DCF') analysis, with a number of other metrics that I use to make sure that my value estimates make sense. One of the more useful ones is the Normalized P/E ratio. The denominator is my estimate of earnings over the next 12 months, adjusted for any one-time/unsustainable factors, and if necessary adjusted for the cyclical nature of the business to reflect a mid-cycle economic environment. The numerator is adjusted for any excess assets (e.g. excess cash) not used to generate my estimate of normalized earnings. One way to interpret this number is that its inverse represents the rate of return we would receive on our purchase price if earnings remained permanently flat. So a normalized P/E of 10x would be consistent with an expectation of a 10% return. While the future is uncertain, it is typically my goal to invest in businesses whose value is increasing over time. If I am correct in my analysis, our return should exceed the inverse of the normalized P/E ratio over a long period of time. The graph below represents the weighted average normalized P/E for the equities in the portfolio.

This has been a humbling couple of years for me as an investor. Through experiencing these challenges and reflecting on them I have learned and improved my process. I have also re-proven to myself that I am able to stick to my process and stay rational during periods of prolonged adversity. I truly believe that these valuable lessons will contribute to a bright future for the partnership in the years ahead.

I appreciate your trust and support during this time. If I can answer any questions please don't hesitate to reach out.

Thank you in advance,

Gary Mishuris, CFA

| IMPORTANT DISCLOSURE AND DISCLAIMERS The information contained herein is confidential and is intended solely for the person to whom it has been delivered. It is not to be reproduced, used, distributed or disclosed, in whole or in part, to third parties without the prior written consent of Silver Ring Value Partners Limited Partnership ("SRVP"). The information contained herein is provided solely for informational and discussion purposes only and is not, and may not be relied on in any manner as legal, tax or investment advice or as an offer to sell or a solicitation of an offer to buy an interest in any fund or vehicle managed or advised by SRVP or its affiliates. The information contained herein is not investment advice or a recommendation to buy or sell any specific security. The views expressed herein are the opinions and projections of SRVP as of February 5th, 2024, and are subject to change based on market and other conditions. SRVP does not represent that any opinion or projection will be realized. The information presented herein, including, but not limited to, SRVP's investment views, returns or performance, investment strategies, market opportunity, portfolio construction, expectations and positions may involve SRVP's views, estimates, assumptions, facts and information from other sources that are believed to be accurate and reliable as of the date this information is presented-any of which may change without notice. SRVP has no obligation (express or implied) to update any or all of the information contained herein or to advise you of any changes; nor does SRVP make any express or implied warranties or representations as to the completeness or accuracy or accept responsibility for errors. The information presented is for illustrative purposes only and does not constitute an exhaustive explanation of the investment process, investment strategies or risk management. The analyses and conclusions of SRVP contained in this information include certain statements, assumptions, estimates and projections that reflect various assumptions by SRVP and anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies and have been included solely for illustrative purposes As with any investment strategy, there is potential for profit as well as the possibility of loss. SRVP does not guarantee any minimum level of investment performance or the success of any portfolio or investment strategy. All investments involve risk and investment recommendations will not always be profitable. Past performance is no guarantee of future results. Investment returns and principal values of an investment will fluctuate so that an investor's investment may be worth more or less than its original value. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.