imaginima

imaginima

OGE Energy Corp. (NYSE:OGE) generates, transmits, distributes, and sells –including at the retail level—electricity. It owns OG&E, the largest electric utility in Oklahoma. OGE Energy has streamlined and simplified its operations by jettisoning its interest in a midstream gas pipeline partnership.

It is in a good position for a number of reasons:

I recommend OGE Energy for its solid business, favorable prospects, and healthy dividend. I am considering buying shares.

In 2023, OGE Energy’s net income was $416.8 million or $2.07/share, compared to 2022 net income of $665.7 million or $3.32/share. However, the distance was almost entirely due to the fact that 2022’s results included $1.16/share for gas midstream operations, a business that OGE Energy fully exited in 2022.

Despite the lower earnings, in other years, OGE Energy had substantial losses due in part to its losses in the gas midstream business.

According to the company’s investor presentation, negative factors were:

Positive factors were:

OGE Energy expects 2024 earnings per share of $2.12.

According to OGE Energy’s CFO Bryan Buckler in the most recent investor call, load growth areas include manufacturing in western Arkansas. In Oklahoma, load growth is in the defense, food and beverage distribution sectors, and particularly new data center load driven by the increase in artificial intelligence.

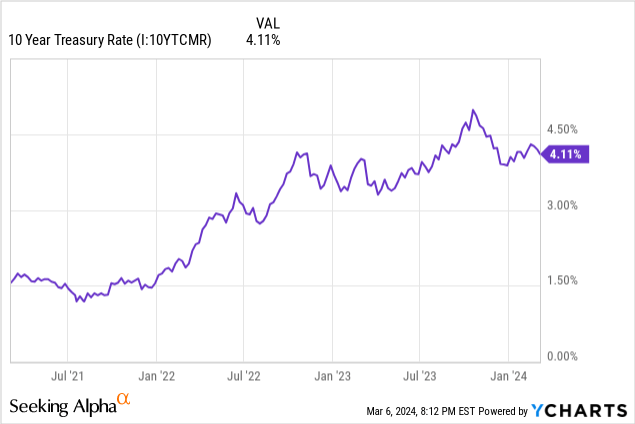

The Federal Reserve’s current rate is 5.25%-5.5%, and Fed Chairman Jerome Powell has not signaled near-term cuts in the next few months. High rates keep financing costs for debt-heavy sectors like utilities high. They also increase the competition for gaining and keeping equity investors.

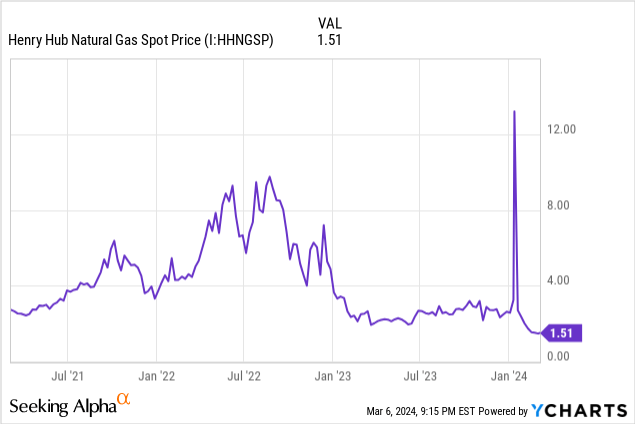

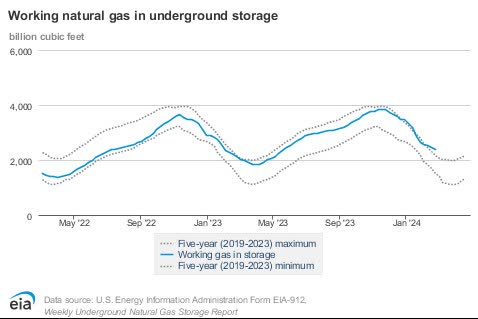

Gas production volumes are healthy. Natural gas prices have fallen dramatically, although they may now be in a slight recovery mode. Nonetheless, affordable natural gas is an advantage for OG&E because it relies on gas as a power generation fuel.

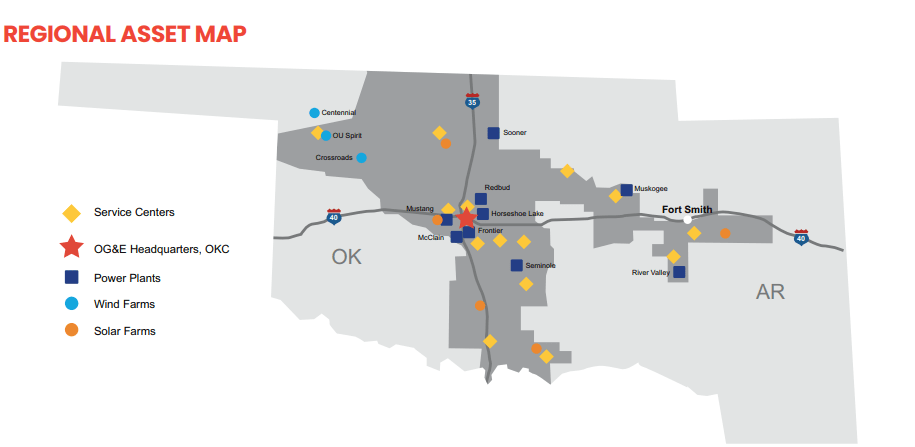

As shown below, OGE Energy, through its OG&E utility provides electric service to 896,000 customers in a 30,000-square-mile area of Oklahoma and western Arkansas. The vast majority of these, 762,000, were residential customers.

OGE Energy

According to the most recent 10-K:

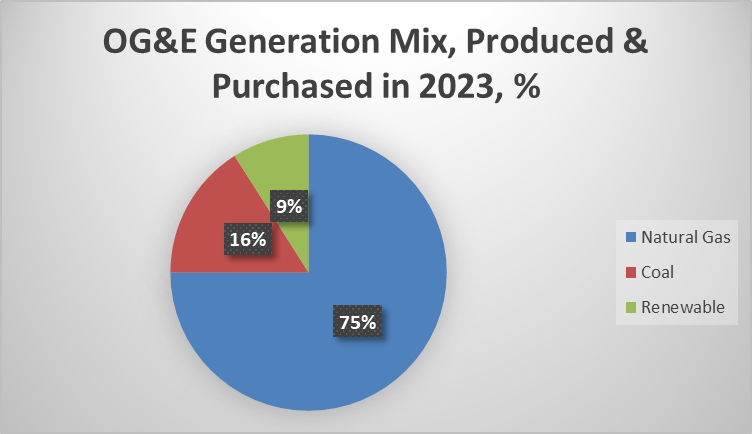

“Of OG&E's 7,116 total MWs of generation capability 4,754 MWs, or 66.8 percent, are from natural gas generation, 1,559 MWs, or 21.9 percent, are from coal generation, 321 MWs, or 4.5 percent, are from dual-fuel generation (coal/gas), 449 MWs, or 6.3 percent, are from wind generation and 33 MWs, or 0.5 percent, are from solar generation.”

This differs from the chart below, as the chart reflects OG&E's actual generation mix (not its capacity) and also includes OG&E’s purchased power.

OGE & Starks Energy Economics

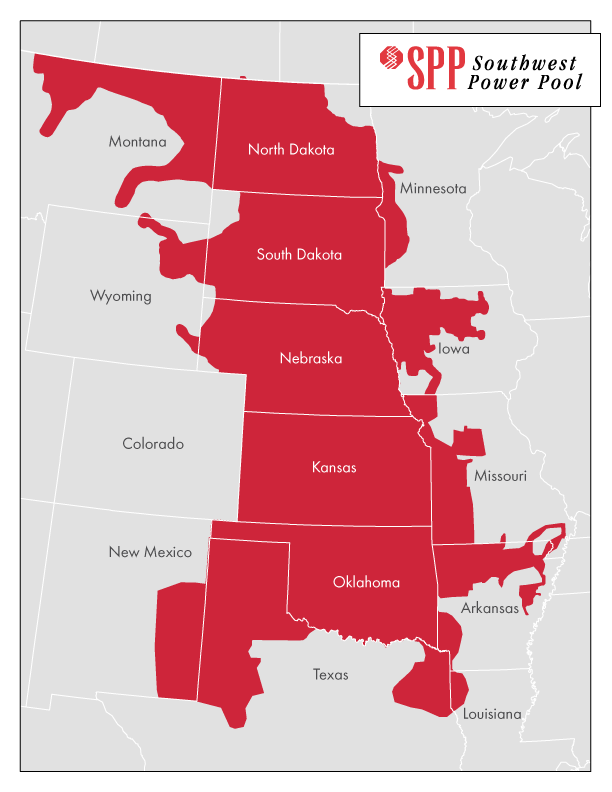

The OG&E utility is part of the Southwest Power Pool.

Also of interest is how much OG&E’s fuel cost has come down, from 6.83 cents/kilowatt-hour in 2021 (due partly to Uri storm effects) to 5.48 cents/kilowatt-hour in 2022 to 2.93 cents/kilowatt-hour in 2023 (due to lower gas prices).

OKEnergytoday.com

Several important crosscurrents are factors in current and future natural gas prices:

EIA Natural Gas Weekly

On March 6, 2024, the NYMEX Henry Hub natural gas futures price for delivery in April 2024 closed at $1.93/MMBTU.

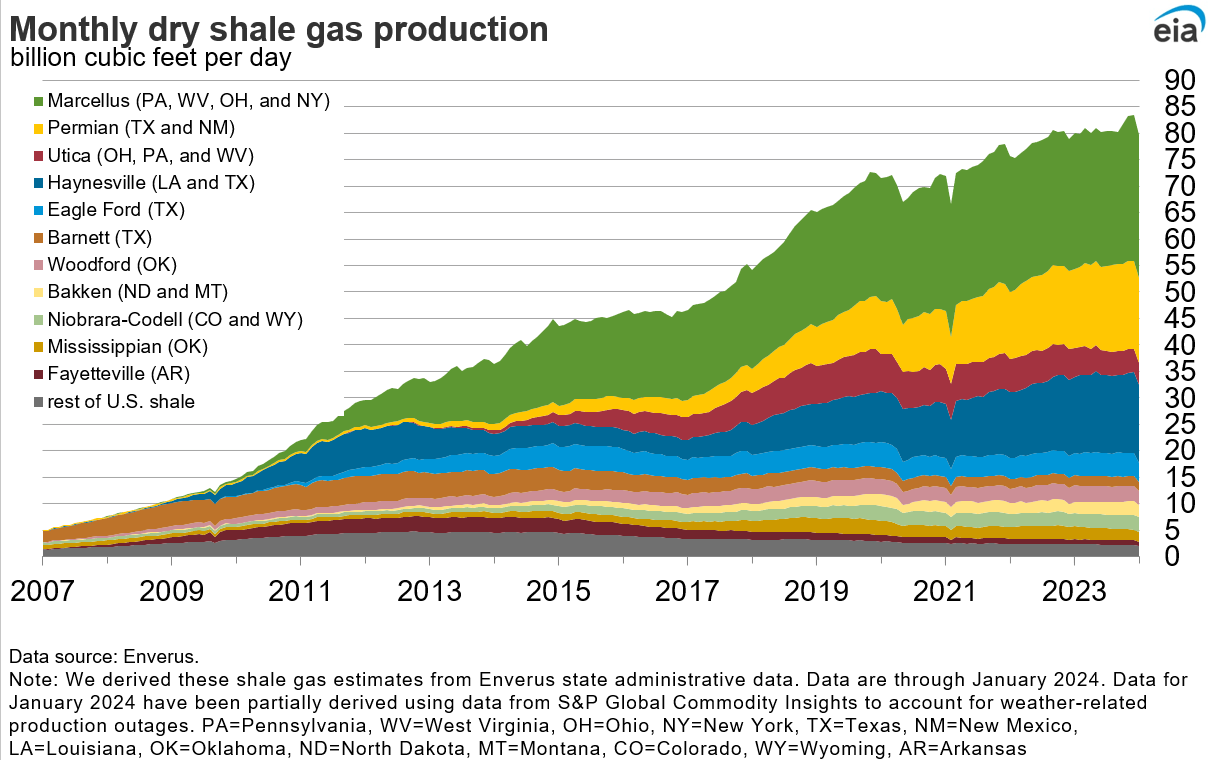

Not only can OGE Energy access the vast and growing gas production from west Texas, but Oklahoma is also a significant supplier of natural gas, at 8.2 BCF/D in 2021, for example.

EIA Natural Gas Weekly

Several exploration and production companies produce natural gas in Oklahoma, including Coterra (CTRA), Devon Energy (DVN), Gulfport (GPOR), Marathon Oil (MRO), Ovintiv (OVV), Exxon Mobil (XOM), and private Continental Resources.

OGE Energy is headquartered in Oklahoma City, Oklahoma.

Although regulated utilities have their own geographic territories and business lines (electricity, gas, water, steam, or a combination) and so don’t compete directly, they do compete for investment.

OGE Energy’s utility subsidiary, OG&E, does not have direct competitors. However, OG&E has oversight from and reporting responsibilities to public utility commissions in the states in which it operates—Oklahoma (Oklahoma Corporation Commission) and Arkansas (Arkansas Public Service Commission). In rate cases it answers to and is subject to input from a wide variety of customer-stakeholders. The company is also subject to normal market pressures for its fuel sources and changes in demand for its gas delivery and electricity production.

On March 1, 2024, Institutional Shareholder Services ranked OGE Energy’s overall governance as a 2, with sub-scores of audit (4), board (3), shareholder rights (3), and compensation (1). In this ranking a 1 indicates lower governance risk and a 10 indicates higher governance risk.

In September 2023, Sustainalytics ranked OGE Energy at 31.8 (75th percentile, or “high” risk) with sub-scores of 15.7-environmental, 10.6-social, and 5.5-governance. A factor in OGE Energy’s score is its thermal coal plants.

On February 15, 2024, short shares were 3.5% of floated shares. Insiders own a tiny 0.34% of outstanding stock.

OGE Energy’s beta is 0.71, meaning less volatility than the overall stock market, but more than some other utilities, like The Southern Company’s current 0.49.

On December 31, 2023, the two largest institutional stockholders, some of which represent index fund investments that match the overall market, were BlackRock (12.4%) and Vanguard (10.6%).

BlackRock is a signatory to the Net Zero Asset Managers initiative, a group that manages $57 trillion in assets worldwide and which limits hydrocarbon investment via its commitment to achieve net zero alignment by 2050 or sooner.

Although BlackRock is no longer using the term "ESG," its net zero goals appear the same as it does what it calls “transition investing.” And, although it has shifted its membership in Climate Action 100+ to its international affiliate, BlackRock has not withdrawn from the Net Zero Asset Managers initiative.

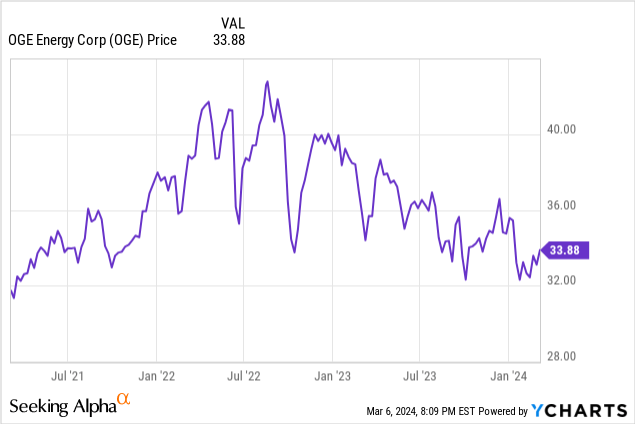

The company’s market capitalization is $6.8 billion at a March 6, 2024, stock closing price of $33.90/share.

The company’s enterprise value (EV) is $11.6 billion, and its EV/EBITDA ratio is 10.2, barely above the preferred ratio of 10 or less that would suggest a discount.

The 52-week price range is $31.25-$39.09 per share, so the March 6, 2024, closing price of $33.90 is 87% of its 52-week high. The company’s one-year target price is $34.63/share, putting its closing price at 98% of that level.

Trailing twelve months (TTM) EPS is $2.07 for a current price-earnings ratio of 16.4.EPS projections for 2024 and 2025 average $2.12 and $2.27, respectively, for a forward price-earnings ratio range of 14.9-16.0.

TTM return on assets is 3.2% and return on equity is 9.3%.

OGE Energy’s dividend of $1.67/share represents a 4.9% yield.

TTM operating cash flow was $1.23 billion while levered free cash flow was -$36 million.

On December 31, 2023, OGE Energy had $8.3 billion in liabilities including $4.3 billion of long-term debt and $12.8 billion in assets resulting in a standard-for-utilities liability-to-asset ratio of 65%.

Mean analyst rating is a 2.7, or near “hold,” from the seven analysts who follow it.

The company’s book value per share of $22.32 is two-thirds of the market price, indicating positive investor sentiment.

Potential investors should consider their expectations of regional economic growth in Oklahoma and western Arkansas, state regulatory environments, regional population growth, and the prospects generally for growth in electricity demand.

At a liability-to-asset ratio of 65%, OGE Energy and the utility sector are more exposed to interest rate changes (up AND down) than companies in other sectors. Higher rates eventually translate directly into higher debt costs for the substantial portion of the company’s capital structure that is debt. Higher rates also mean more inter-instrument competition for dividend-seeking equity investors. Conversely, lower rates mean the opposite and are a positive risk.

I recommend OGE Energy to dividend investors for its 4.9% dividend. I am considering buying shares.

Although the company has a high price/earnings ratio, what is appealing about it, like Black Hills, is its location in growing areas and business-forward states and its affordable generating fuels (wind, natural gas, coal). It has steady operations, which are now more streamlined and more focused (without the gas midstream).

A sector-wide benefit is the expected growth in electricity demand, particularly as artificial intelligence is increasingly applied.

While interest rates are still higher than in recent history, it appears likely they may come down somewhat in the second half of 2024, which benefits all utilities and interest-rate sensitive sectors.

oge.com