tumsasedgars

tumsasedgars

Recently, I have been selling my investments in Business Development Companies (BIZD), with recent sales including shares in:

Fortunately for me, each of these sales locked in significant total returns and freed up substantial capital to take advantage of other opportunities available at the time. In addition to my desire to free up capital to take advantage of other opportunities, my reduced exposure to the BDC sector was also motivated by the fact that I am growing increasingly bearish on the sector. This souring of sentiment is the result of three major factors:

One of the reasons why I am not attracted to the BDC sector right now is that there is growing competition in the direct lending and private credit sectors. In addition to the public trading vehicles, virtually all of the mega asset managers, such as Blackstone (BX), BlackRock (BLK), Brookfield (BAM)(BN), Ares (ARES), KKR (KKR), Carlyle (CG), Apollo (APO), and Blue Owl (OWL) are pouring tens of billions of dollars into the sector. Moreover, major banks like JPMorgan (JPM) and Goldman Sachs (GS) also invest billions of dollars into these loans.

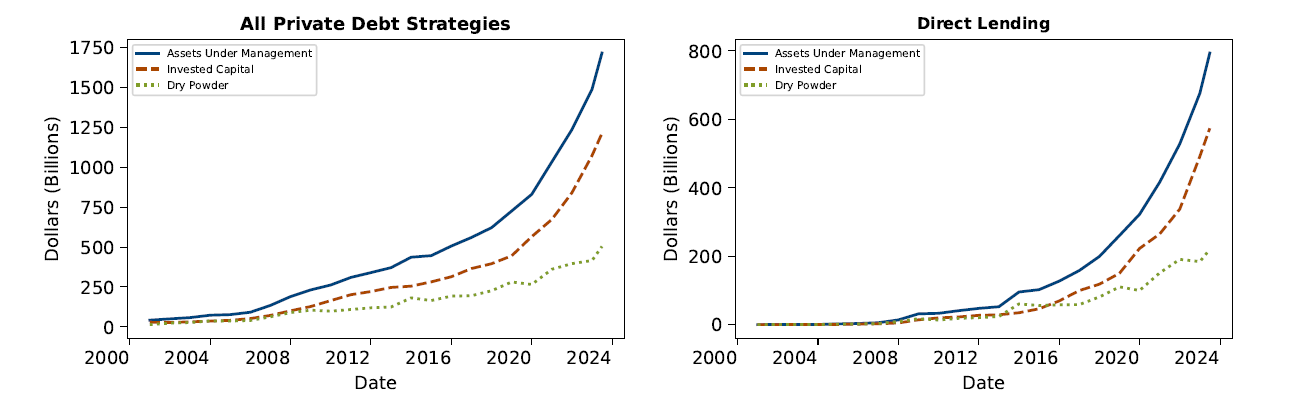

As a result, the sector has seen exploding growth, with all private debt strategies growing AUM by about $1.5 trillion over the past decade and a half and direct lending in particular roughly quadrupling in size over the past half-decade alone:

Growth in Private Debt Allocations (US Federal Reserve)

This exponential growth is leading to tighter spreads in the sector and - according to researchers at the Federal Reserve - potentially lower underwriting standards. Therefore, it is reasonable to conclude that the risk-reward profile of newly underwritten deals in the sector is declining on average and will likely continue doing so moving forward.

The loans that BDCs typically invest in are by nature on the risky end of the spectrum given the fact that they typically command yields that rival typical equity returns, despite the increased supply of willing lenders in the space. This means that they are generally quite sensitive to macroeconomic conditions.

Moreover, the vast majority of these loans are tied to short-term interest rates. Given that the Federal Reserve has raised short-term interest rates quite rapidly over the past two years and appears poised to keep them elevated for longer than many expected, this is starting to put significant pressure on many counterparties to these loans. Additionally, these companies are getting pinched even further by sticky inflation. As a result, their interest coverage ratios are declining and their balance sheets are getting tighter and tighter.

As ARCC's CEO recently cautioned:

we're likely to see defaults in the industry increase this year...you have some companies that are making interest payments but continue to live off revolver availability, cash, et cetera, but the liquidity is getting tighter and tighter. And so my expectation is that defaults will go up this year.

We have seen this manifest itself in several BDC's results recently as well. OCSL reported that its non-accruals on a fair value basis more than doubled from 1.8% at the end of Q3 to 4.2% at the end of Q4. Moreover, FSK just reported that its non-accruals on a fair value basis also more than doubled from 2.4% at the end of Q3 to 5.5% at the end of Q4. This is quite surprising coming from portfolios managed by leading asset managers like KKR and particularly Oaktree. This is likely a sign of things to come for the rest of the industry as well, as per ARCC's CEO's comments.

Moreover, with the Yield Curve Inversion model currently indicating that there is a "very high" risk of recession hitting the U.S. economy in the near future, and leading business figures like JPM's Jamie Dimon saying that there is a less than 50% chance of the U.S. economy achieving a soft landing, there could very possibly be further headwinds for the sector. Moreover, the Fed is much more likely to cut before they hike interest rates moving forward, so it is pretty safe to say that BDCs are at peak earnings right now. This is especially true when you factor in that many BDCs will have some of their own debt maturing in the coming months and years that they will likely have to refinance at much higher interest rates than they currently enjoy.

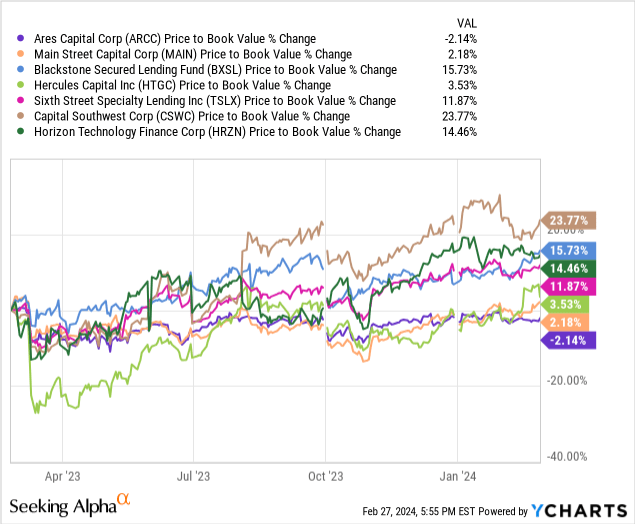

Last, but not least, the industry's valuations are not particularly compelling right now either. A clear indication of this is that the seven highest regarded blue chips in the BDC sector - ARCC, Main Street Capital (MAIN), BXSL, Hercules Capital (HTGC), Sixth Street Specialty Lending (TSLX), Capital Southwest (CSWC), and Horizon Technology Finance (HRZN) - are all trading at meaningful premiums to NAV and all but ARCC have seen their multiples expand over the past year, with some expanding their multiples significantly.

Moreover, even ARCC and MAIN - the two weakest performers over the past year in terms of P/NAV - are trading above their historical average P/NAV multiples.

Yes, it makes sense that investors are attracted to effectively floating rate securities that are delivering elevated earnings right now due to interest rates being high, but the aforementioned deteriorating fundamentals and growing competition in the space seem to make it a poor risk-adjusted place to allocate capital, especially at a premium valuation.

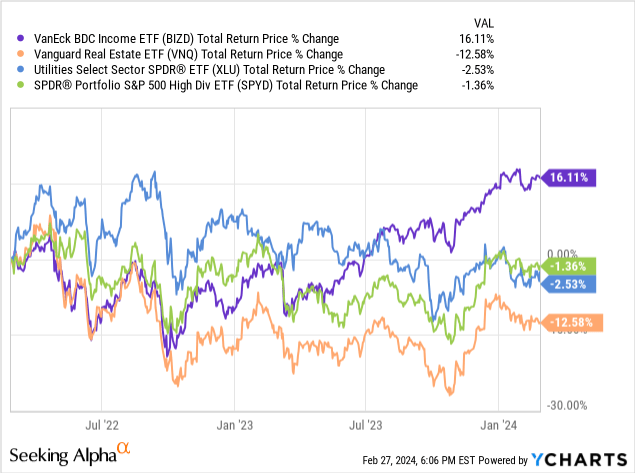

BDCs have been a great place for high-yield investors to be over the past two years as the rapid rise in interest rates and the remarkably resilient U.S. economy so far have created a Goldilocks scenario for the sector, with soaring net interest spreads and resilient - or even growing - NAVs per share. In contrast, REITs (VNQ) and utilities (XLU) have suffered from rising interest rates, leading to considerable outperformance for the BDC sector and underperformance for REITs and utilities relative to the broader high-yield dividend stock sector (SPYD):

We have successfully allocated capital into BDCs over much of this period, helping us to outperform as well. Moving forward, however, we expect BDCs to underperform and are growing increasingly bullish on REITs and utilities. As a result, we are selling our BDC positions opportunistically to lock in strong profits and recycle the capital into beaten-down high-quality infrastructure and REIT names.