ktsimage/iStock via Getty Images

ktsimage/iStock via Getty Images

Ocugen Inc. (NASDAQ:OCGN) is a clinical-stage biotechnology company based in Malvern, Pennsylvania. It is focused on gene and cell therapies and inhalable vaccine development. The OCU400 program, with indications for RP, adRP, and LCA, is progressing to phase 3 clinical trials in 1H 2024. NeoCart, a cell therapy for knee repair, has also advanced to phase 3 trials. Finally, OCGN's participation in the $5 billion NIAID-funded trial for OCU500 inhaled COVID-19 vaccine enhances the company's financial and strategic position. In my valuation analysis, I conclude that OCGN is a reasonably good speculative “buy” despite its inherent risks, as it holds significant upside potential if it delivers on its revenue projections.

Ocugen is a clinical-stage US biotechnology company founded in 2013. It specializes in discovering, developing, and distributing vaccines and gene and cell therapies for eye disorders. Its proprietary platform focuses on modifier gene therapy to treat retinal diseases. The company also researches infectious diseases and orthopedic illnesses. However, as of today, OCGN is mostly a bet on their star IP OCU400 and its successful research and eventual commercialization.

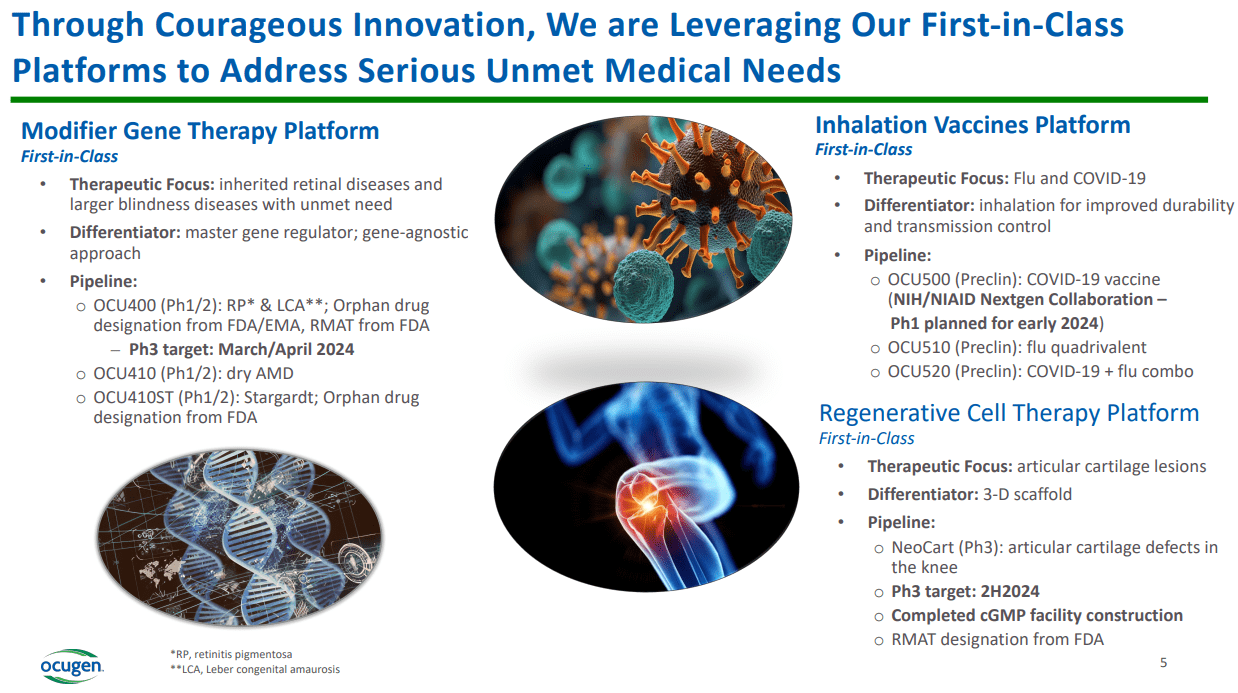

Source: Corporate Presentation, February 2024.

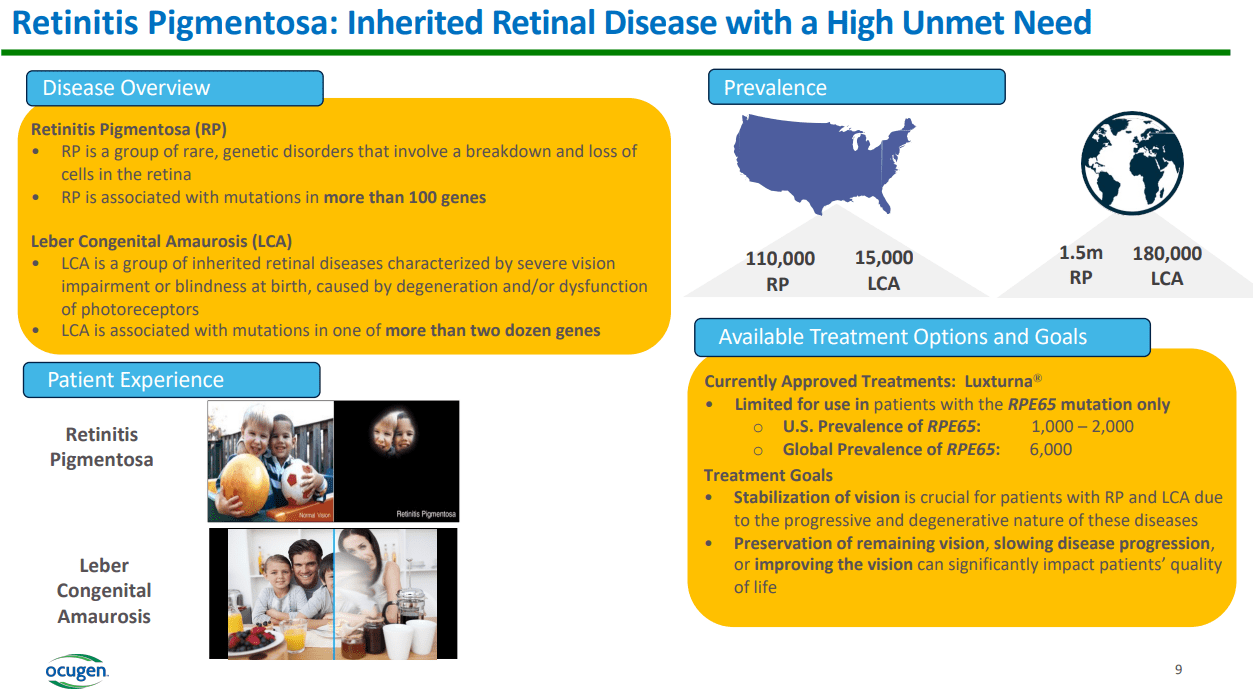

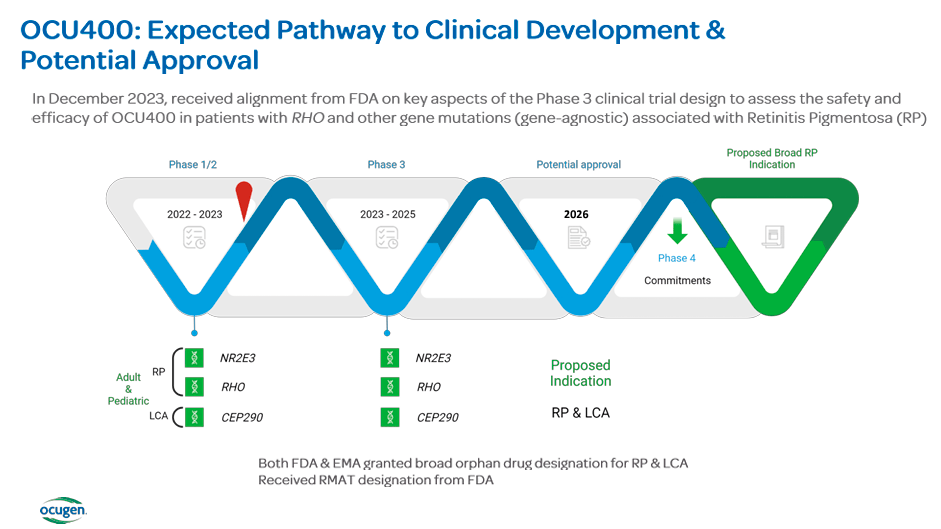

As previously noted, the gene therapies in OCGN’s pipeline include its main product candidate, OCU400, currently in phase 1/2, progressing to phase 3 with orphan drug designation. It is indicated for inherited eye diseases such as retinitis pigmentosa [RP], autosomal dominant retinitis pigmentosa [adRP], specifically related to NR2e3, and Leber congenital amaurosis [LCA]. RHO and CEP290 mutations are involved in retinal dystrophies characterized by loss of vision and eventual blindness. The NR2E3 mutation plays a crucial role in the differentiation of photoreceptor cells. Its mutation causes enhanced S-cone syndrome [ESCS], which provokes increased blue light sensitivity, night blindness, and loss of peripheral vision. This mutation sometimes leads to RP, which produces progressive peripheral vision loss, leading to night blindness and central vision loss.

Moreover, the RHO gene encodes rhodopsin, a protein that regulates retinal rods responsible for low-light vision. Mutations in this gene cause adRP, resulting in progressive vision loss. Finally, the CEP290 gene is involved in ciliogenesis for the formation and function of cilia in the retina. Its mutation can generate LCA, a retinal degeneration that produces congenital blindness. Also, it can provoke other forms of retinitis pigmentosa and other syndromic diseases that affect not only vision but other bodily systems due to the role of the CEP290 ciliary function.

Source: Corporate Presentation, February 2024.

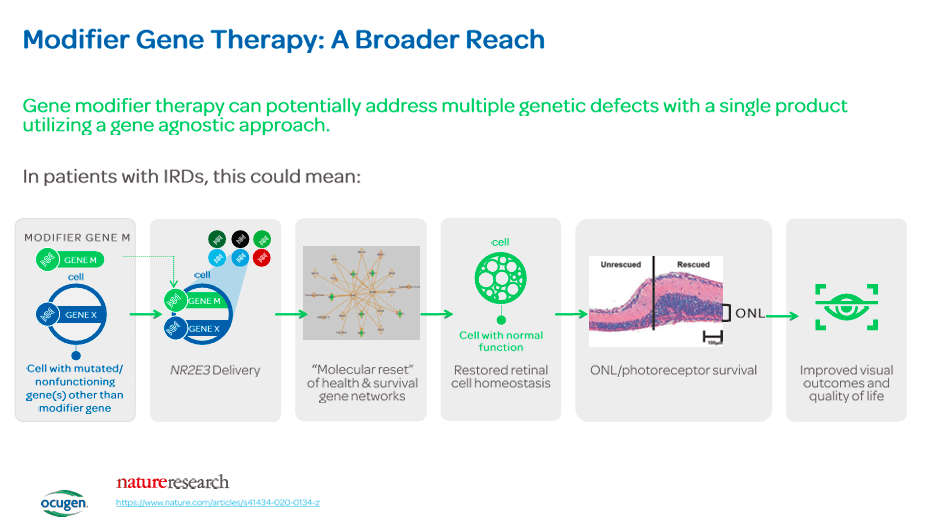

The most interesting part about OCU400 therapy is that it delivers a functional gene copy that can modify disease progression through a nuclear hormone receptor gene. This gene is related to multiple retinal biological pathways necessary for retinal health. The functional gene is delivered using an adeno-associated virus [AAV] vector that can control retinal cells. Once in the retinal cells, the gene produces its protein to mitigate the disease's progression or reverse its effects. On September 30, 2023, data from phase 1/2 further supported the drug's safety and potential benefits. The positive results represent an advancement in the drug's development and should enhance investors' confidence in future success. Then, in December 2023, OCU400 received a Regenerative Medicine Advanced Therapy [RMAT] designation from the FDA. It is a status granted to accelerated development and review of regenerative medicine therapies. Overall, OCU400 is now OCGN’s main value driver, and it should be the main focus for potential investors.

Still, OCGN also has OCU410 and OCU410ST, which are mong OCGN’s gene therapy pipeline. These are prescribed for dry age-related Macular Degeneration [dry AMD] and Stargardt disease, which is an orphan disease with no current treatment option and 44,000 patients in the US. These drugs are in Phase ½ as gene therapies that also use the AAV platform to supply a retinoic acid receptor-related, orphan receptor A [RORA] gene to the retina to address lipofuscin accumulation, oxidative stress, inflammation, and cell survival by modulating the nuclear hormone receptor [NHR] RORA pathway.

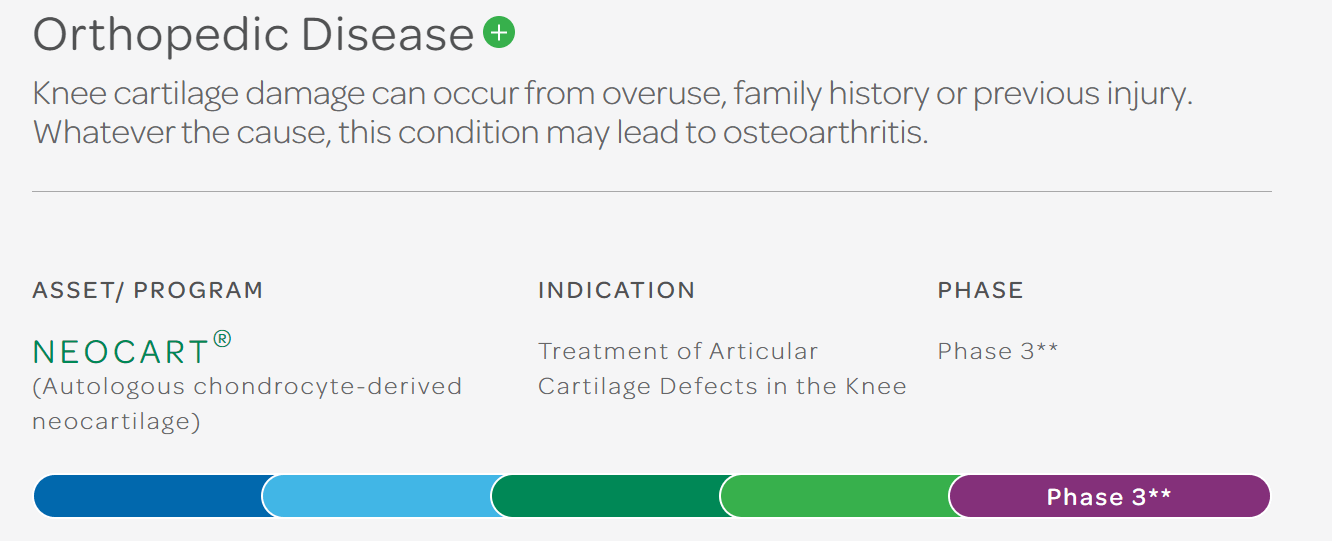

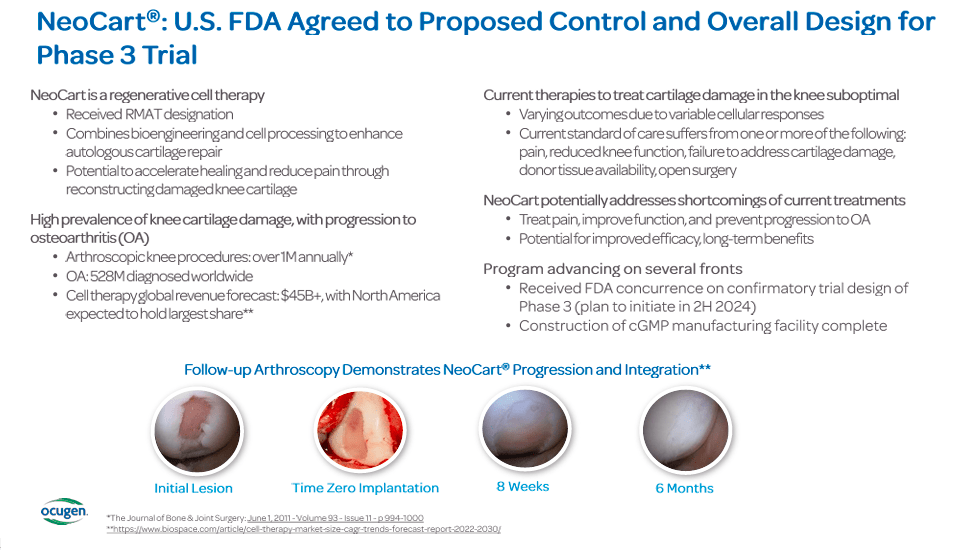

Another interesting OCGN cell therapy is NeoCart, an autologous chondrocyte-derived neocartilage used to treat articular cartilage defects in the knee. This therapy is in phase 3, clinical trials, the final stage before regulatory FDA approval for public use. Since it’s already in Phase 3, it could also be considered a potential value driver in the near future, yet note that most of the company’s investor-related presentations seem to be focused on OCU400. Nevertheless, articular cartilage defects on the knee cause pain and functional disability, affecting athletes and the general population, so NeoCart could also be potentially lucrative. Current treatments include palliative care, physical therapy, and microfracture or cartilage grafting surgery.

Source: Corporate Presentation, January 2024.

These treatments have limitations and are not always successful. NeoCart offers a potentially more effective, less invasive, and lasting solution leveraging the body's cells to reduce pain and restore function. This drug has also received an RMAT designation by the FDA. Interestingly, OCGN’s NeoCart progression to phase 3 diversifies its already promising IP into something unrelated to ophthalmology.

Source: OCGN’s website.

Moreover, OCGN’s inhaled vaccine program for COVID-19 and flu is in the Investigational New Drug [IND] stage, and we should get further updates on 1H2024 in collaboration with the National Institute of Allergy and Infectious Diseases [NIAID]. On October 10, 2023, the OCU500 bivalent inhaled COVID-19 vaccine was selected for the $5 billion government project NextGen to advance the vaccines for this disease. This additional funding could enhance OCGN's financial position.

Lastly, OCNG’s biological program OCU200 is in the IND submitted stage. It leverages a fusion protein combining Transferrin and Tumstatin to address the causes of Diabetic Macular Edema [DME], Diabetic Retinopathy [DR], and Wet Age-Related Macular Degeneration [Wet AMD]. Transferrin is a protein that transports iron, which could target and deliver Tumstatin to retinal cells. Tumstatin is a fragment of collagen that inhibits the growth of new blood vessels to reduce abnormal blood vessel growth and leakage. This biological addresses a significant need for more effective treatments for DME, DR, and Wet AMD, which are the leading causes of vision loss and blindness in adults.

In the last earnings call, OCGN's executives highlighted the clinical progress of its key programs. The OCU400 program will initiate phase 3 trials in 1H 2024 after the positive results obtained from its phase 1/2 study. The phase 3 clinical trial for OCU400 will initially concentrate on RP patients, with an LCA focus to be added later. The planned stage 3 will enroll around 100 patients and have a one-year follow-up period. In the ophthalmology area, OCU410 and OCU410ST for AMD and Stargardt disease are also advancing, marking milestones in developing therapies for a wide range of ocular diseases with gene therapy solutions.

Source: Corporate Presentation, January 2024.

NeoCart for knee repair is on the way, with a state-of-the-art facility nearing completion and fulfilling all current good manufacturing practices [cGMP]. The construction of this cGMP facility is crucial for regulatory compliance and will facilitate future product's entry into the market.

Source: Corporate Presentation, January 2024.

The NIAID-funded trial for the OCU500 vaccine and the development of NeoCart for knee restoration shows OCGN's commitment to a diversified approach to tackle broader health challenges outside ocular diseases, potentially widening the company’s impact and market opportunities. Overall, I see OCGN as mainly a bet on OCU400 at this stage, but it’s certainly a company with promising IP progression across different verticals.

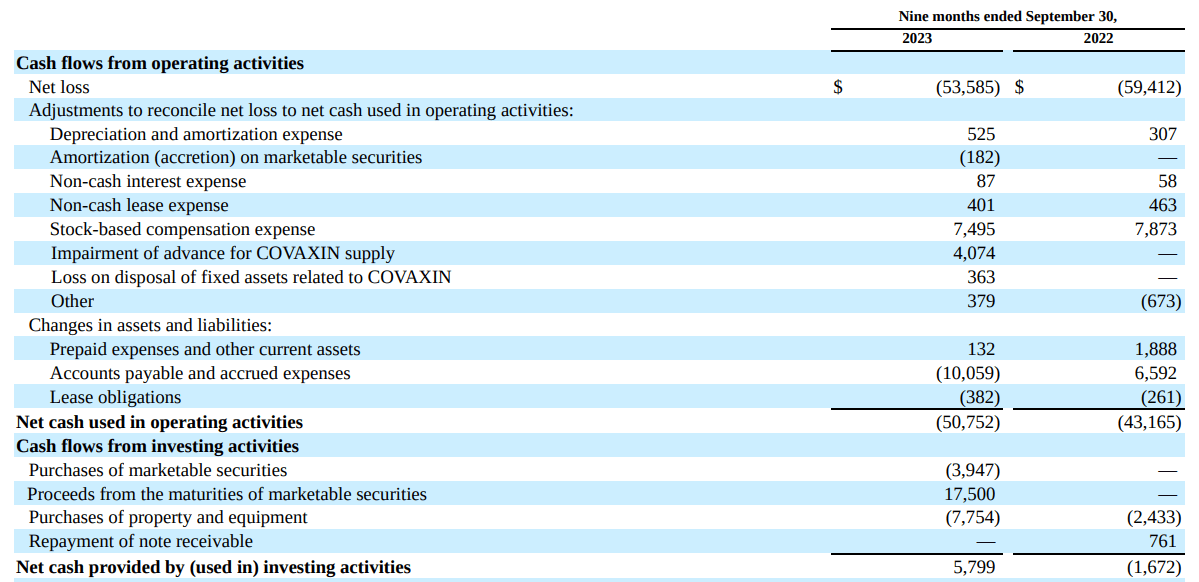

From an investment perspective, it’s worth noting that as of September 2023, the company had just $53.5 million in cash and equivalents against $1.5 million in long-term debt. Moreover, the company has accumulated losses for years and has no revenues. Using their CFOs and Net CAPEX from OCGN’s latest quarterly report, I estimate the cash burn figure at $58.6 million. This corresponds to the first nine months (3 quarters) of 2023. Thus, the corresponding annual figure is roughly $78.1 million if we annualize that cash burn. This is likely OCGN’s main issue, implying a dangerously low cash runway of just 0.7 years (counting from September 2023). Therefore, the reality is that the company needs additional funds to sustain its R&D efforts.

Source: Corporate Presentation, February 2024.

Nevertheless, funding is possible because it has 1) low debt and 2) an exceedingly promising product portfolio, especially through OCU400. For context, OCGN expects FDA approval for OCU400 by 2026, which quickly unlocks significant revenue potential. Both of these factors suggest that the company should be able to raise funds, though if it opts to do so through equity, there will be dilution for existing shareholders. Personally, I speculate that OCGN will likely fund future operations through a mix of equity and debt, likely supported by a partnership, assuming FDA approvals for OCU400 occur. With those out of the way, I foresee a realistic path toward commercialization efforts.

Still, the reality is that 0.7 years starting from September 2023 implies that they will run out of cash by June 2024. Thus, OCGN undoubtedly needs cash this year, and it will require a substantial amount to make it through to 2026 by the time it aims to start commercializing OCU400. That means it should raise enough cash for 2H2024, 2025, and 2026 (the year it commercializes OCU400). The current cash burn rate implies the equivalent of roughly 30 months' worth of cash burn, which I estimate is about $195.3 million. Since its current market capitalization is $277.0 million, this could be a substantial dilution if it’s all done through equity.

Source: OCGN’s latest 10-Q report.

The dilution impact is difficult to anticipate, but ideally, most of it would be financed through debt and equity early on to get OCGN through 2024 into 2025. By then, the odds of FDA approval should be higher, and the likelihood of signing a partnership that funds the rest (2026 commercialization funding needs) will increase. Yet, if that happens, revenue-sharing agreements would occur as well. Alternatively, more dilution and debt would be required if no partnerships happen. At that point, commercialization efforts could begin in 2026, assuming FDA approvals are obtained as expected, yet once again, funding that expansion will become an issue.

So, OCGN’s funding is my main issue today, but I’m exceedingly optimistic about OCU400 and its revenue potential. I see multiple reasonable pathways to raise funds and its potential dilutive effects. Still, the revenue potential likely outweighs those downsides significantly, which is why I rate OCGN a “buy” for investors who understand those caveats. After all, if OCGN delivers billions in revenue from OCU400 in 2026, it could all be worth it for investors today, even despite dilution risks in the short term.

As previously noted, the path from approval to generating billions in revenue will be fraught with hurdles ranging from market adoption, payer reimbursement, competition, and logistical or manufacturing challenges. These are significant issues that OCGN’s management will have to tackle, and today, it seems that it’s mostly just an R&D team composed of 61 employees. So scaling up operations efficiently and funding them will be difficult and a key risk to consider for investors.

Source: TradingView.

Moreover, my “buy” rating mostly hinges on OCGN actually delivering on its roadmap toward FDA approval and commercialization. If this is delayed, which is entirely possible due to biotech's inherent risks, investors could quickly face significant losses. Yet, overall, OCGN’s product pipeline is incredibly promising, and I believe a solid R&D foundation supports the notion of eventually getting the necessary FDA approvals. This will unlock billions in potential revenues down the line, and at the relatively low valuation of $277.0 million in market cap today, it seems like a reasonable speculative “buy,” all things considered.

Overall, OCGN is an exceedingly promising biotech company with pre-revenues, and its main product in the short term will likely be OCU400. This particular drug could unlock billions in revenues for shareholders by 2026, but getting there is fraught with several risks ranging from funding, dilution, and regulatory approvals, to name a few. Yet, OCGN trades at a relatively low valuation today after considering the potential upside it could achieve. Its R&D efforts and diversified IP portfolio suggest the company is on track to deliver substantial shareholder value. Thus, I think OCGN is a good speculative “buy” for investors who understand the risks present at this point.