Grace Cary/Moment via Getty Images

Grace Cary/Moment via Getty Images

Over the past several days now, a number of interesting developments have emerged regarding both Masonite International Corporation (NYSE:DOOR) and Owens Corning (NYSE:OC). On February 9th, news broke that Owens Corning struck a deal to acquire Masonite International in an all-cash transaction. And then, on February 14th, the management team at Owens Corning announced financial results covering the final quarter of its 2023 fiscal year. This was followed up on February 19th by the management team at Masonite International announcing financial results for its final quarter of the same fiscal year.

All of this data, combined, gives us a great deal to think about regarding both businesses. It just so happens that both of these companies are firms that I have been bullish about in the past. The last article that I published about Masonite International came out in February of 2023. In that article, I said that the enterprise had proven itself to be a quality operator. Growth had been impressive and, despite some weaknesses, shares looked attractive enough to rate the business a "buy." Since then, shares have seen upside of 40.1% compared to the 21.5% seen by the S&P 500 (SP500).

As for Owens Corning, I actually downgraded the company to a "buy" in November of last year. After seeing the share price skyrocket, I felt as though much of the easy money had been made, but that there was still some opportunity for investors. Since then, we have seen a roller coaster ride. Since announcing its purchase of Masonite International earlier this month, OC shares have dropped by 12.3%. Even with that, the stock is up 7.4% since I last wrote about the business. By comparison, the S&P 500 is up 11%. However, since I initially rated the firm a "strong buy" in July of 2022, shares are up 73.1% compared to the 26.6% seen by the S&P 500.

Given these recent developments, I would say that reevaluating the prospects, both individually and as a group, makes sense. At the end of the day, it is clear that Owens Corning’s purchase of Masonite International is really only fantastic if planned synergies can be achieved. But even without those, the purchase seems to be a solid one at an attractive price. If anything, I'm a little surprised at how cheap investors in Masonite International were willing to part with their shares. But for those who are still bullish that business and bullish about this space, transitioning over to Owens Corning might not be a bad idea.

According to a press release issued by Masonite International, the management team said that they were selling the business to Owens Corning at a price of $133 per share. This represents a 38% premium to what shares of the company were trading at the day before the announcement. The total equity value of the transaction is worth about $2.9 billion. Having said that, when you factor in net debt, this number is expected to rise to roughly $3.9 billion.

Owens Corning

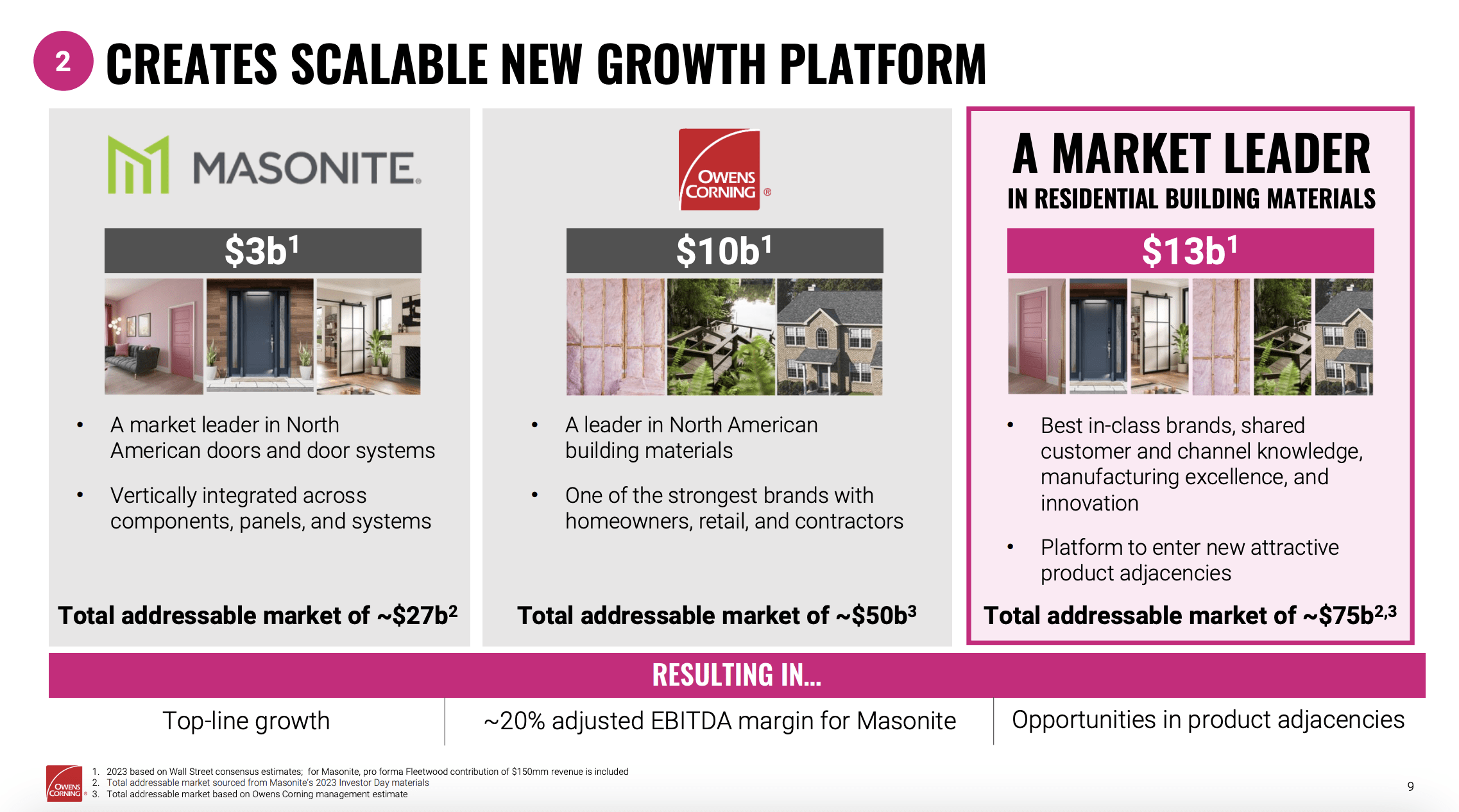

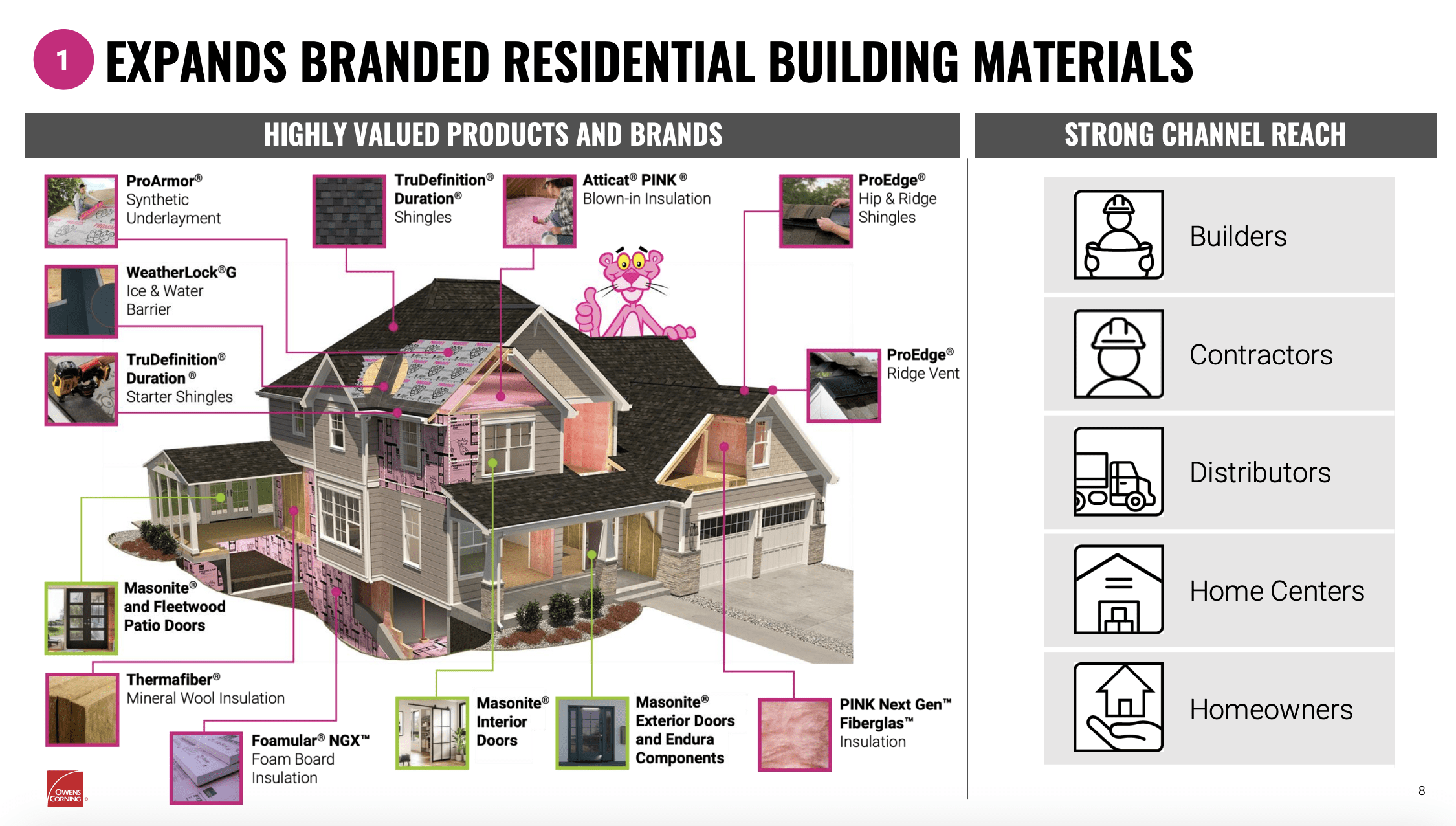

Based on my own review of the investor presentation that talks about the transaction, there are really two primary reasons why Owens Corning has decided to purchase Masonite International. The first and most obvious reason is for the purpose of expanding. The fact of the matter is that, with revenue of $2.83 billion, Masonite International is a rather large player in the $27 billion North American doors and door systems market. To be clear, this market opportunity also includes some of the other major products that the company engages in such as panels and other related components.

Historically, this is not an area that Owens Corning has focused on. Although it's also a player in the North American building materials market, its emphasis has largely been the sale of things like laminate and strip asphalt roofing shingles. It also sells other roofing components. The firm is also a major player in the insulation and composites markets. Using data from the 2023 fiscal year, Owens Corning generates around $9.68 billion in revenue annually. That makes it a massive player and what it sees as a $50 billion market.

Owens Corning

Combined, the companies should generate around $12.5 billion in revenue out of a roughly $75 billion market. By adding these different operations together, the first benefit that you get is supplier power. It's easier for many firms to source their goods or supplies through a single player. There can also be some cost savings on that front as well. If you're going to be buying 10s of millions of dollars worth of product, the supplier just might give you a good deal. But of course, there is another angle to this purchase. And that involves synergies.

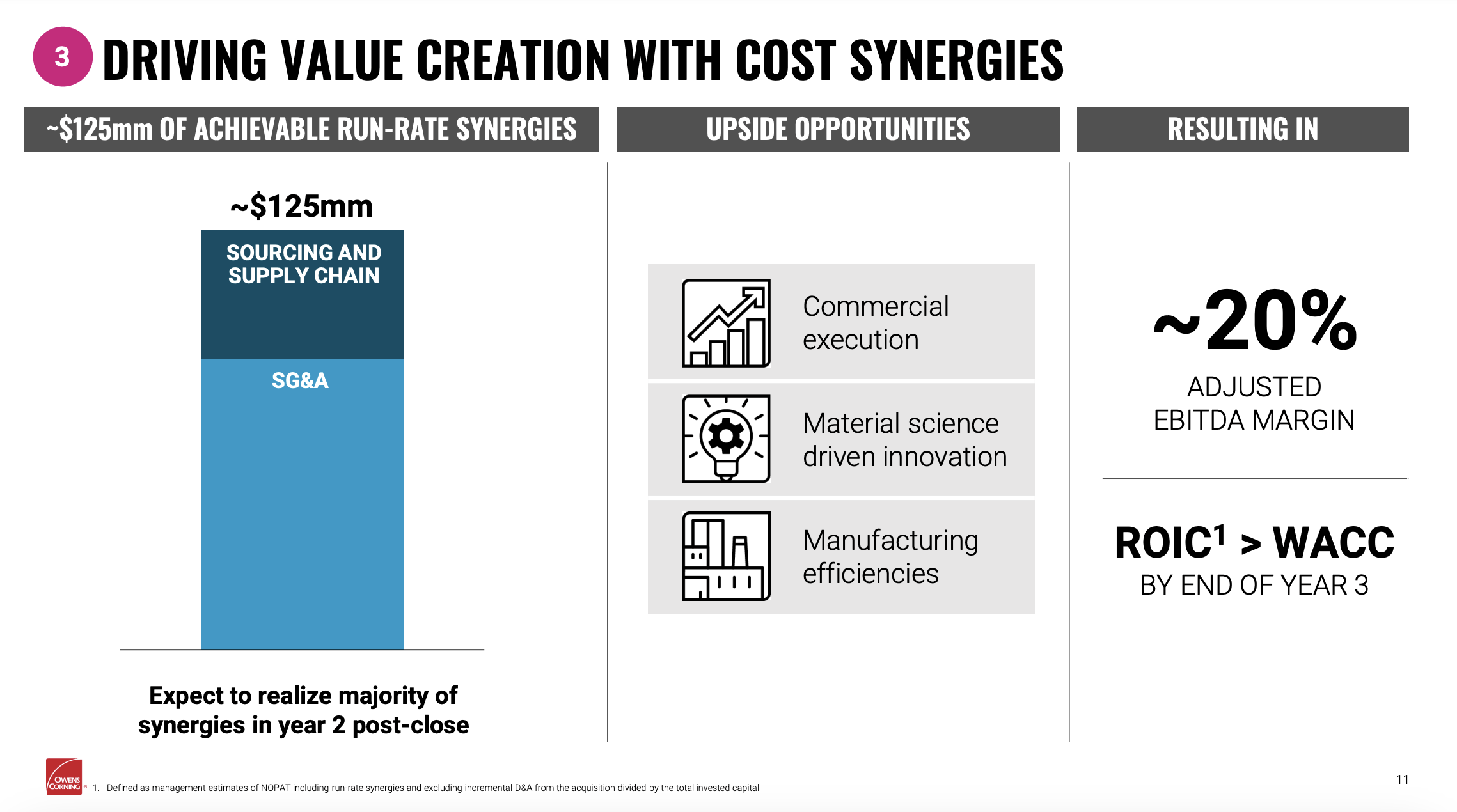

According to the management team at both companies, the combined firm should generate around $125 million in annual run rate synergies by the second year following the close of the transaction. A specific breakdown of these synergies has not been provided. But management did say that the majority of them will involve reductions in selling, general, and administrative costs.

This is not surprising to me in the least bit. You don't need two investor relations departments. You don't necessarily need two accounting departments. The list goes on. Basically, trimming certain parts of the corporate fat can help cut costs materially. However, some portion of this reduction and expense will involve sourcing and supply chain. This will likely be a combination of rationalizing assets and exercising buying power over the supply chain.

Owens Corning

Of course, this transaction does have one downside. And that is that Owens Corning will likely have to take on a good chunk of debt. The firm had net debt as of the end of the most recent quarter of $1.43 billion. On top of this, Masonite International has net debt of $937.5 million. Nobody knows at this time what the terms of any debt will be. But since neither business has a net cash position, some financing to cover the roughly $2.9 billion equity value of the transaction will be necessary. In fact, the firms expect that, upon closing in the middle of this year, the net leverage ratio of the firm will be between 2 and 3. They expect this to drop to around 2 by the end of the year.

One thing that might help is that, also recently, Owens Corning did announce a strategic review of its glass reinforcements business. This falls under the Composites segment of the firm, and it operates as one of the largest providers of glass reinforcements for the wind energy market, as well as other markets like transportation and consumer products, in North America. Specific details of this segment have not been provided. But management did say that revenue is around $1.3 billion and EBITDA should be somewhere around $235 million. It's hard to imagine a unit like this being valued by the market at less than between $1.8 billion and $2.2 billion. Selling that off would do you wonders for the company's balance sheet. But, of course, the terms have to be right.

Author - SEC EDGAR Data Author - SEC EDGAR Data

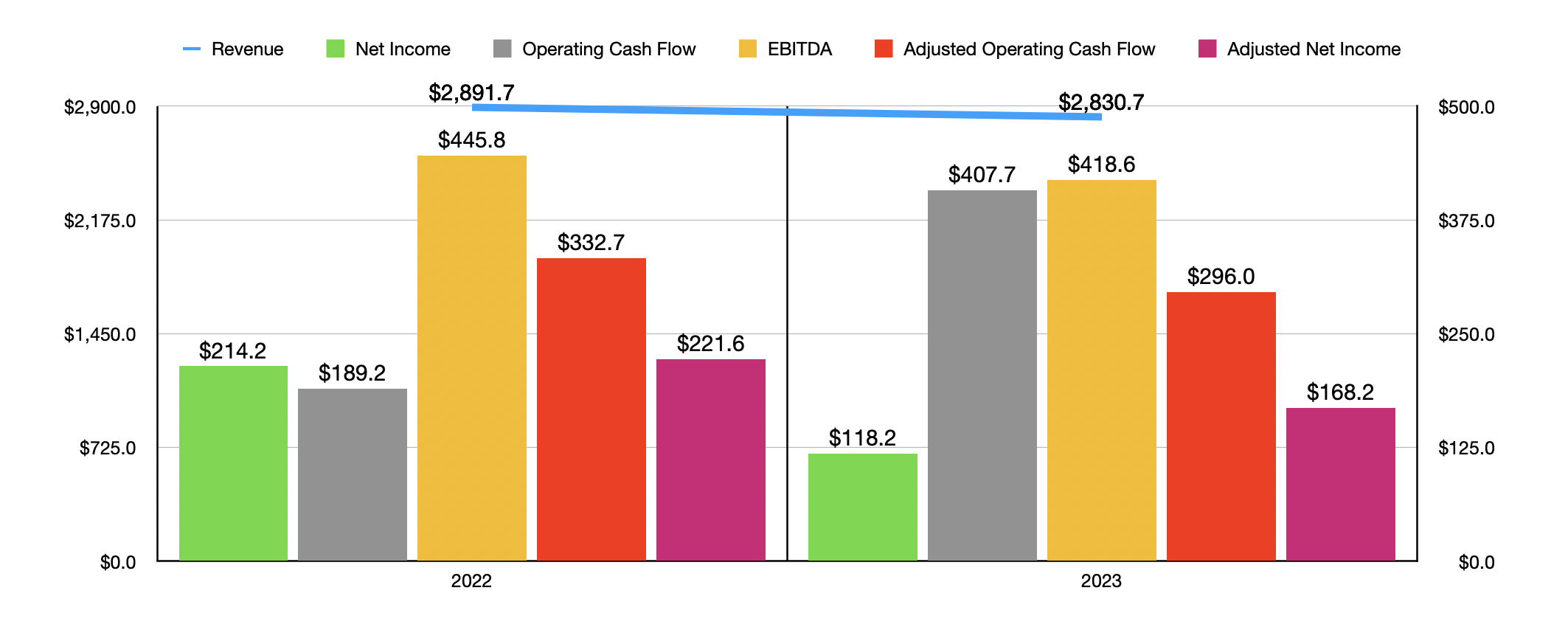

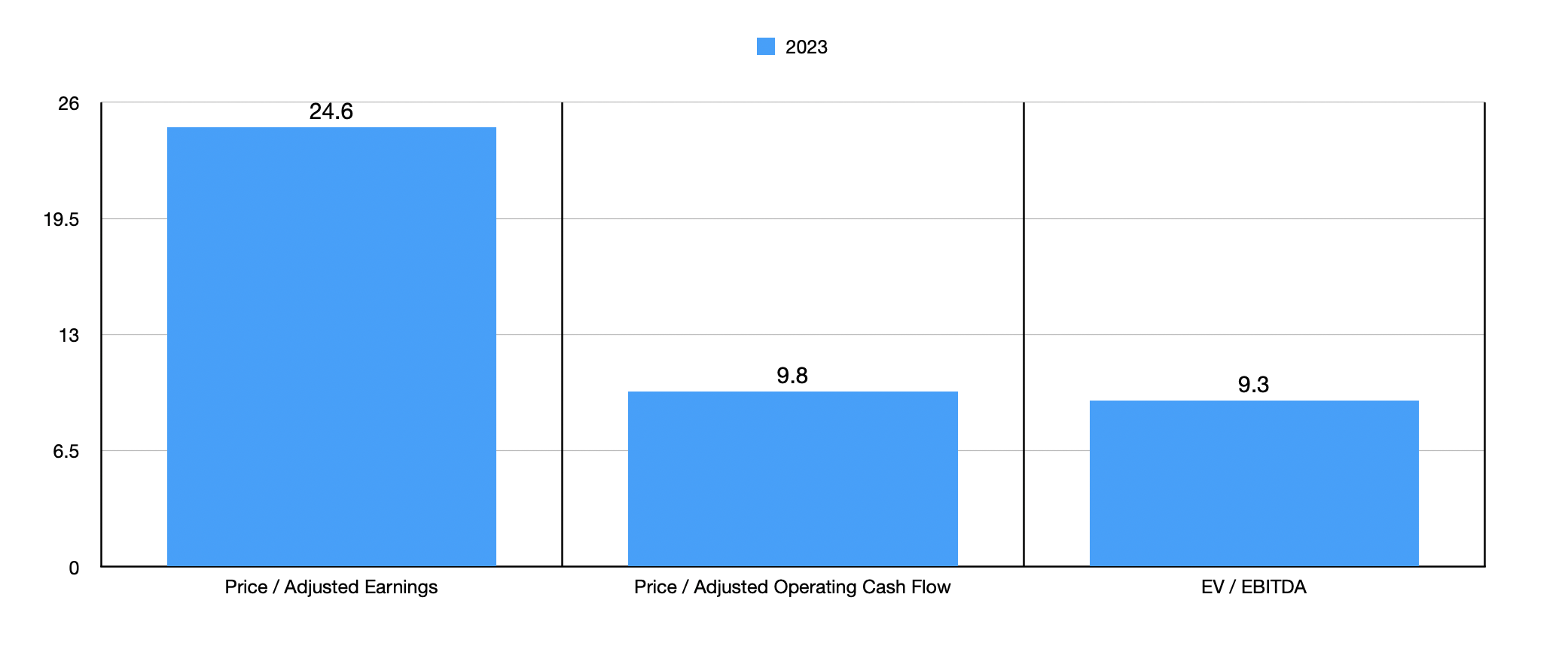

As for the current transaction, we can use updated data provided by the management teams of both firms to evaluate what all is going on. For the final quarter of the 2023 fiscal year, Masonite International reported some rather disappointing results, with revenue, profits, and cash flows all worsening year-over-year. But even with that, the company still managed to generate $418.6 million worth of EBITDA and $290 million of adjusted operating cash flow. Net profits were $118.2 million, while adjusted profits totaled $168.2 million. Given the current terms of the buyout, we are looking at the kind of pricing for the business as shown in the second chart above, with the first showing financial results for the year.

Author - SEC EDGAR Data Author - SEC EDGAR Data

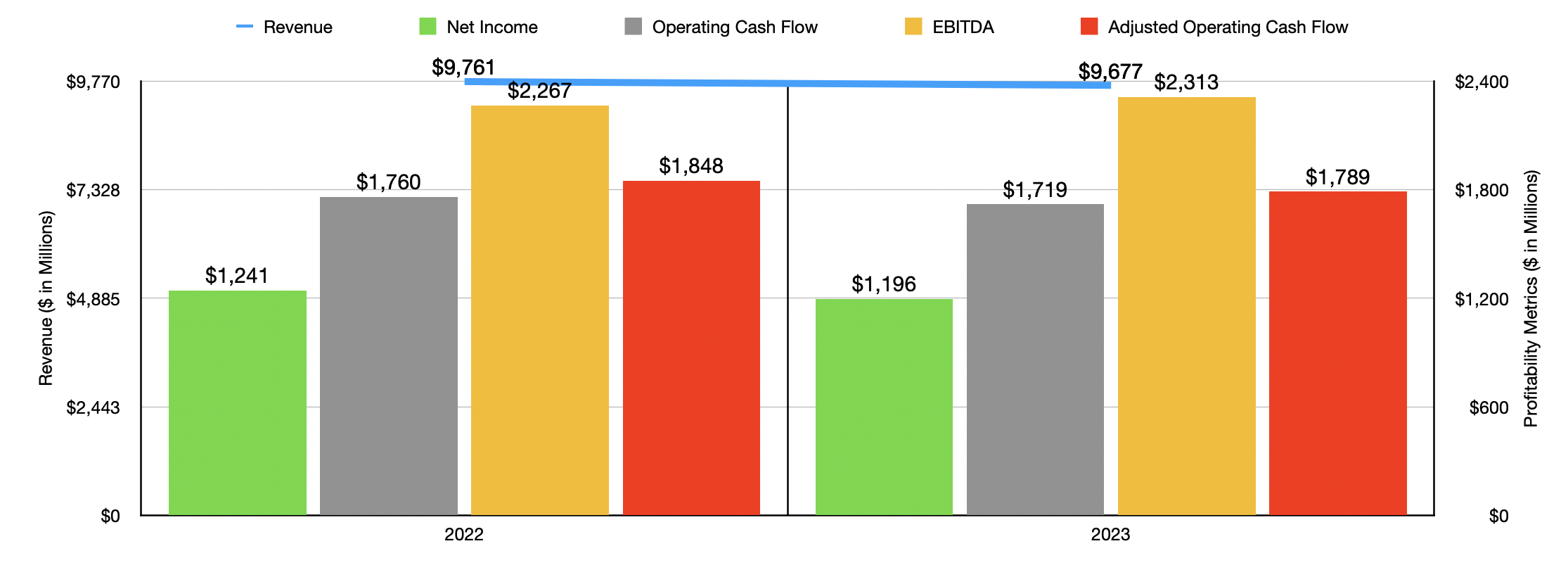

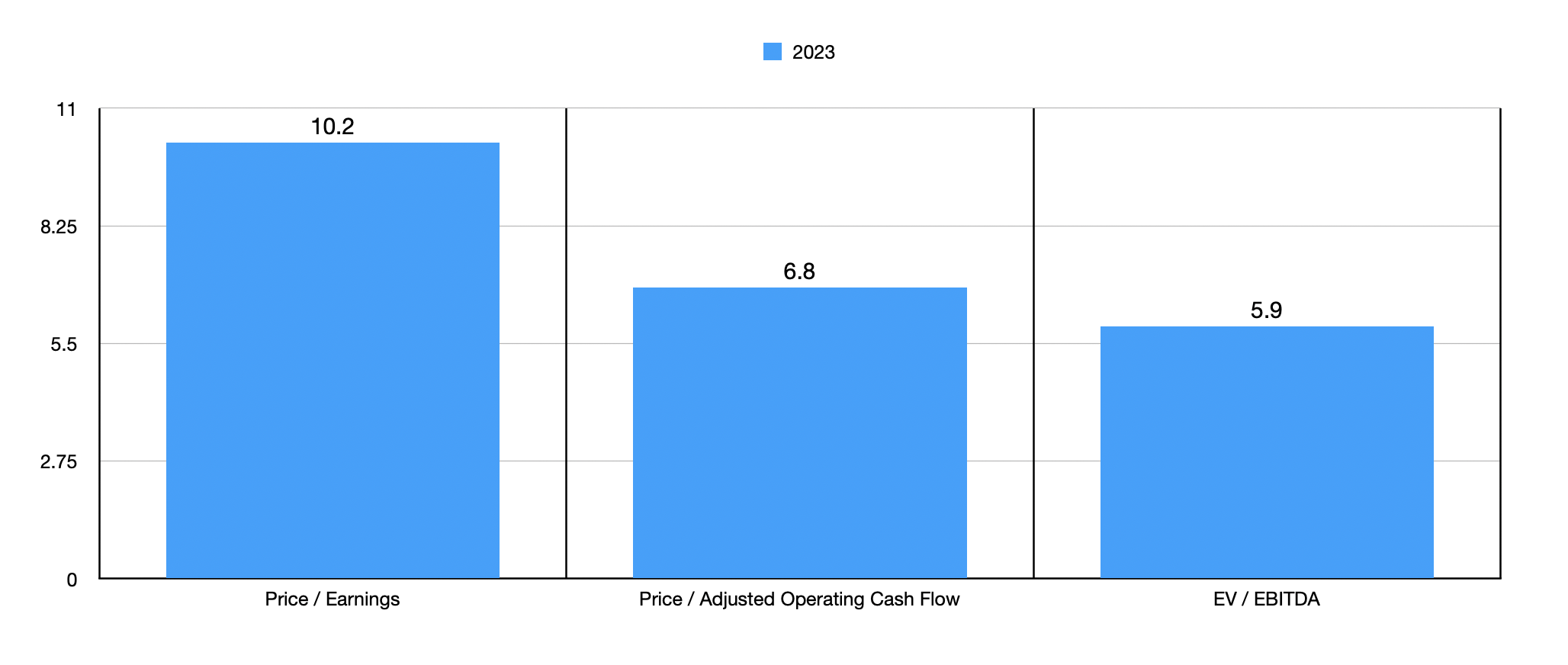

Of course, there is also Owens Corning to take into consideration. On February 14th, management announced financial results for the final quarter of the 2023 fiscal year. Revenue for the business for the year as a whole was $9.68 billion. As the first chart above illustrates, revenue, profits, and most cash flow numbers worsened year over year from 2022. But even so, the company has generated quite a bit of cash. In the second chart above, you can then see how shares are priced.

Author - SEC EDGAR Data

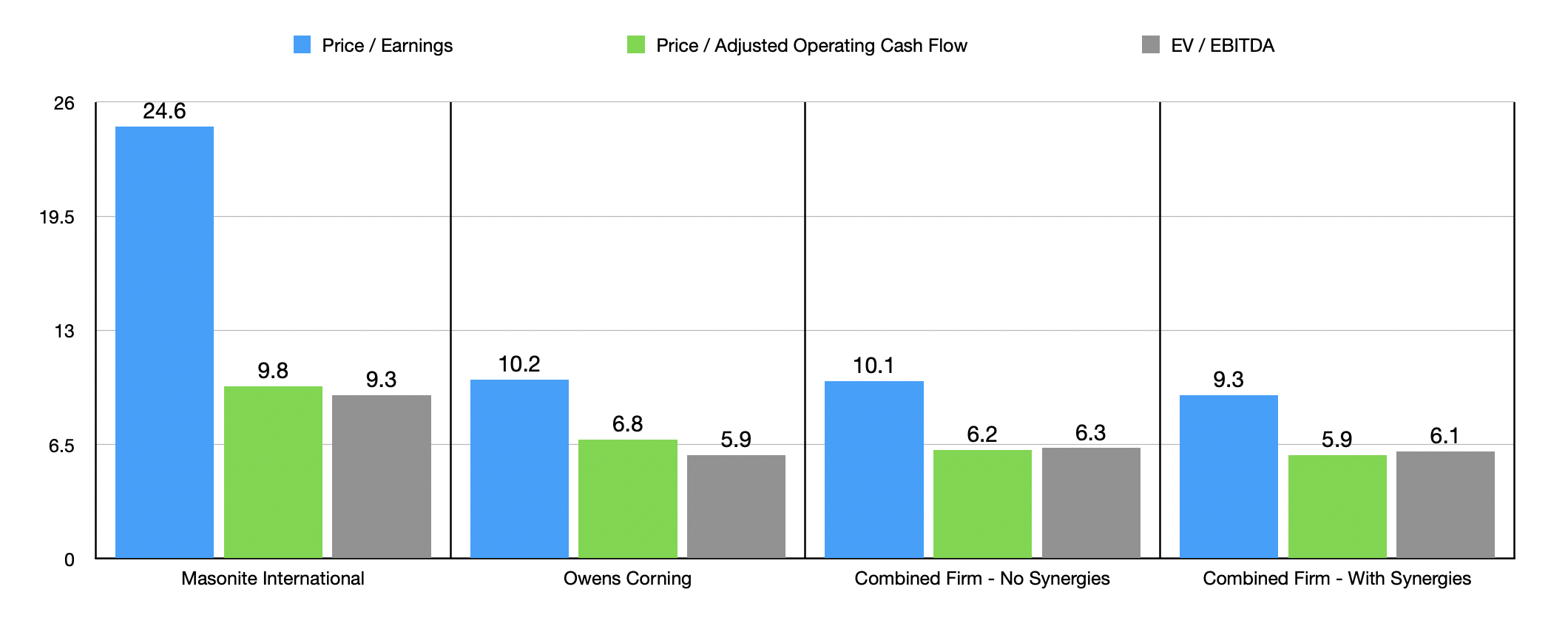

In the final chart above, you can see how each business is priced using the 2023 figures on a standalone basis. You can also see how they are priced as a combined business, both with synergies and without synergies. Keep in mind that the combined picture assumes a 7% interest rate on the debt that the company will incur on $2.9 billion. This is an estimate of mine based on the highest interest rate debt that Owens Corning currently has outstanding. Even in the best case, the acquirer is seeing is trading multiple rise as a result of the transaction. This likely explains why shares fell in response to the development, though the increase is so modest that I would argue that the market is overreacting.

As things stand, it looks as though Owens Corning is paying a bit of a premium for Masonite International, but only in relation to where its shares currently are. On an absolute basis, both companies look quite cheap, and I think that it's a bit surprising that shareholders of Masonite International would sell off their business on such terms.

For those who are bullish about this space and who believe, like me, that Owens Corning still has some room to run, it might make sense to eventually transition over to buying its shares. Of course, there is a bit of a spread, about 2.5%, between the price at which Masonite International is trading and the implied buyout price. But that's fairly small in the grand scheme of things, and Owens Corning could very well move more than that in either direction in any given day.

Because of the all-cash nature of the deal and the limited upside from here, I have decided to downgrade Masonite International Corporation to a "hold." But Owens Corning stock still makes sense to have as a "buy" for now.