mgdwn

mgdwn

Obsidian Energy Ltd. (NYSE:OBE) is projected to generate US$35 million in 2024 free cash flow at current strip prices. This relatively modest amount of projected free cash flow is due to Obsidian spending to grow production. It is aiming for approximately 12% production growth in 2024, and recently mentioned that its year-to-date production had been tracking a bit above expectations.

I had previously estimated Obsidian's value at US$9 to US$10 per share, but have reduced that by US$0.50 per share to a new range of US$8.50 to US$9.50 per share. This is due to reduced 2024 free cash flow expectations (mainly due to lower strip prices) compared to when I looked at Obsidian in September 2023. I still also believe that Obsidian could be worth around US$17 per share by the end of 2026 if it carries out its three-year growth plan effectively. There is more uncertainty around that, though, as commodity prices over the next few years and operational results could both significantly affect that growth plan. This report is in U.S. dollars unless otherwise mentioned. The exchange rate used is US$1.00 to CAD$1.36.

Obsidian noted that its recent results have been relatively strong. It provided an update on its 1H 2024 development program and indicated that its current production had reached 36,500+ BOEPD and that 2024 production (until late February) was tracking slightly ahead of year-to-date expectations despite the negative impact of cold weather on its January production.

Obsidian's Pembina (Cardium) 7-36 Pad (four wells) had initial peak pad production of over 2,000 BOEPD (89% oil). However, some of its other wells didn't perform as strongly. For example, Obsidian's Willesden Green (Cardium) 12-30 Pad (two wells) had average IP-30 production of 154 BOEPD (60% oil) per well. Overall, though, Obsidian noted that its Cardium program was meeting expectations.

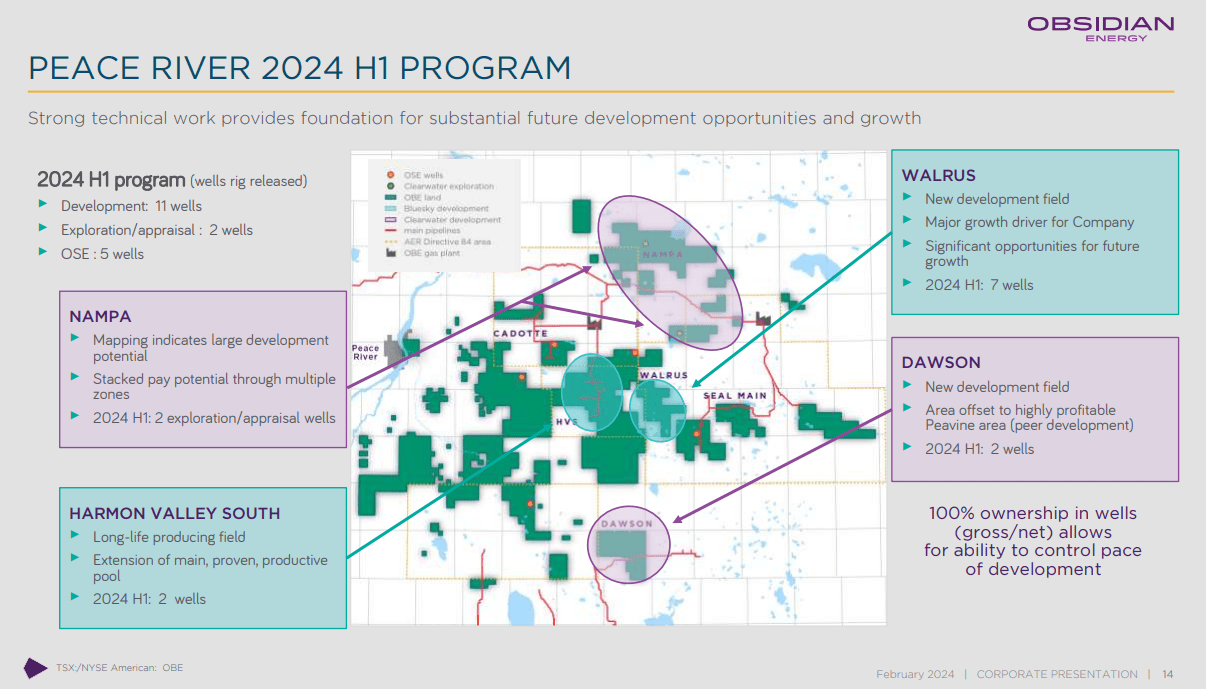

Obsidian also noted that its first exploration/appraisal Nampa area well (Peace River) targeting the Clearwater formation was performing well with an IP-15 of 210 BOEPD (100% oil). Obsidian said that the Nampa oil had an API gravity of 16 degrees, which it expected to fetch CAD $6 to $8 (US $4.41 to $5.88) per barrel more than its existing Bluesky production. Baytex has said that its Bluesky oil has API gravities ranging between 9 to 12 degrees.

Obsidian's Peace River Program (obsidianenergy.com)

Obsidian expects to average approximately 36,000 BOEPD in production during 2024, which would be a 12% increase from its 2023 production levels. Light oil makes up approximately 38% of its projected production, while heavy oil makes up another 22%. NGLs account for 8% of Obsidian's 2024 production, while natural gas makes up the remaining 33%.

At current strip prices of $76 to $77 WTI oil, I estimate that Obsidian will generate US$590 million in revenues after hedges. Obsidian is mostly unhedged on oil, except for a small amount of WCS basis hedges. This revenue estimate also assumes that the WCS differential ends up at around negative US$15 later in 2024 with the Trans Mountain Pipeline expansion coming online.

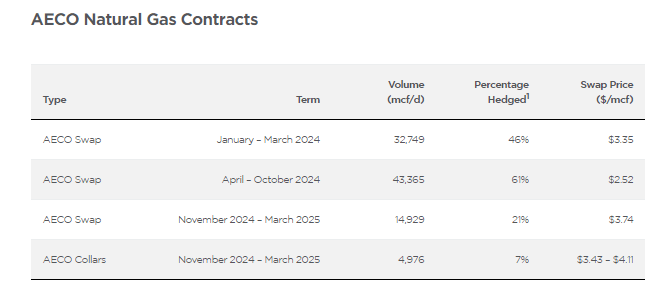

Obsidian's Natural Gas Hedges (obsidianenergy.com)

Obsidian does have natural gas hedges covering around 52% of its 2024 natural gas production, and these hedges may have around US$6 million in positive value at current strip prices.

Type | Units | $ US/Unit | $ Million US |

Light Oil And NGLs [BBLs] | 5,986,000 | $68.00 | $407 |

Heavy Oil [BBLs] | 2,847,000 | $47.00 | $134 |

Natural Gas [MCF] | 25,842,000 | $1.65 | $43 |

Hedge Value | $6 | ||

Total Revenue | $590 |

This results in a projection that Obsidian can generate US$326 million in 2024 EBITDAX at current strip.

$ Million US | |

Revenue | $590 |

Less: Operating Expense | $135 |

Less: Transportation | $34 |

Less: Royalties | $79 |

Less: Cash G&A | $16 |

EBITDAX | $326 |

Obsidian expects US$257 million in 2024 capital expenditures, along with US$17 million in decommissioning expenditures. About US$18 million of the capex budget is for exploration and appraisal activity that has minimal associated production volumes in Obsidian's guidance.

This results in an estimate that Obsidian can generate US$35 million in 2024 free cash flow at current strip prices after factoring in its interest costs.

This is a bit higher than Obsidian's prior free cash flow estimates for 2024, due to slightly improved oil prices compared to the US$75 assumption that Obsidian used.

Obsidian reported having CAD$330 million (US$243 million) in net debt at the end of 2023. Obsidian's projected 2024 free cash flow would reduce this to approximately CAD$283 million (US$208 million) in net debt at the end of 2024 before factoring in any spending on share repurchases. This would leave Obsidian with around 0.6x leverage.

Obsidian renewed its normal course issuer bid recently, allowing it to repurchase up to 7.56 million shares over the next twelve months. Given Obsidian's relatively limited projected free cash flow for 2024 though, it may repurchase less than this allowed amount.

Obsidian repurchased 2.2 million shares in Q4 2023 and appears to have repurchased another 0.285 million shares during the first couple months of 2024 (up to February 21st).

If Obsidian puts all its 2024 free cash flow towards share repurchases, it may end 2024 with around 74 million shares outstanding after factoring in share-based compensation. This situation would also leave it with US$243 million in net debt at the end of 2024 and leverage of 0.7x.

I now estimate Obsidian's value at approximately US$8.50 to US$9.50 per share. This is a US$0.50 per share reduction compared to when I looked at Obsidian in September 2023. Obsidian's 2024 production results have been tracking a bit better than expected, but oil strip prices for 2024 were around US$5 higher back in September.

Thus, the reduction in near-term cash flow expectations affects Obsidian's rate of potential debt reduction and also trims its value a bit despite its solid production results.

Obsidian Energy's early 2024 results have been fairly good, and its current production has reached over 36,500 BOEPD. It is attempting to grow production by 12% year-over-year, and this spending on growth will likely leave it with relatively limited free cash flow.

I am currently projecting Obsidian's 2024 free cash flow to be around US$35 million at 2024 strip prices, and it may put much of that free cash flow towards share repurchases. Obsidian's leverage looks okay at current strip prices though, with its year-end 2024 leverage projected to be 0.6x to 0.7x depending on its spending on share repurchases.

Despite the solid early 2024 results, I am trimming Obsidian Energy Ltd.'s estimated value by US$0.50 compared to my September 2023 estimates. This is due to lowered near-term free cash flow expectations with oil strip prices dropping by around US$5 and Obsidian having no oil hedges outside of a small amount of WCS basis hedges. I now estimate Obsidian's value at US$8.50 to US$9.50 per share.