mbbirdy

mbbirdy

The New York Times Company (NYSE:NYT) has produced modest revenue growth but improved operating results in recent quarters.

Management has focused on the opportunities of bundling various products and increasing its licensing revenue.

However, topline revenue growth rate has continued to drop post-pandemic.

Until management can reignite growth, either through product development or acquisition, I’m Neutral (Hold) on NYT.

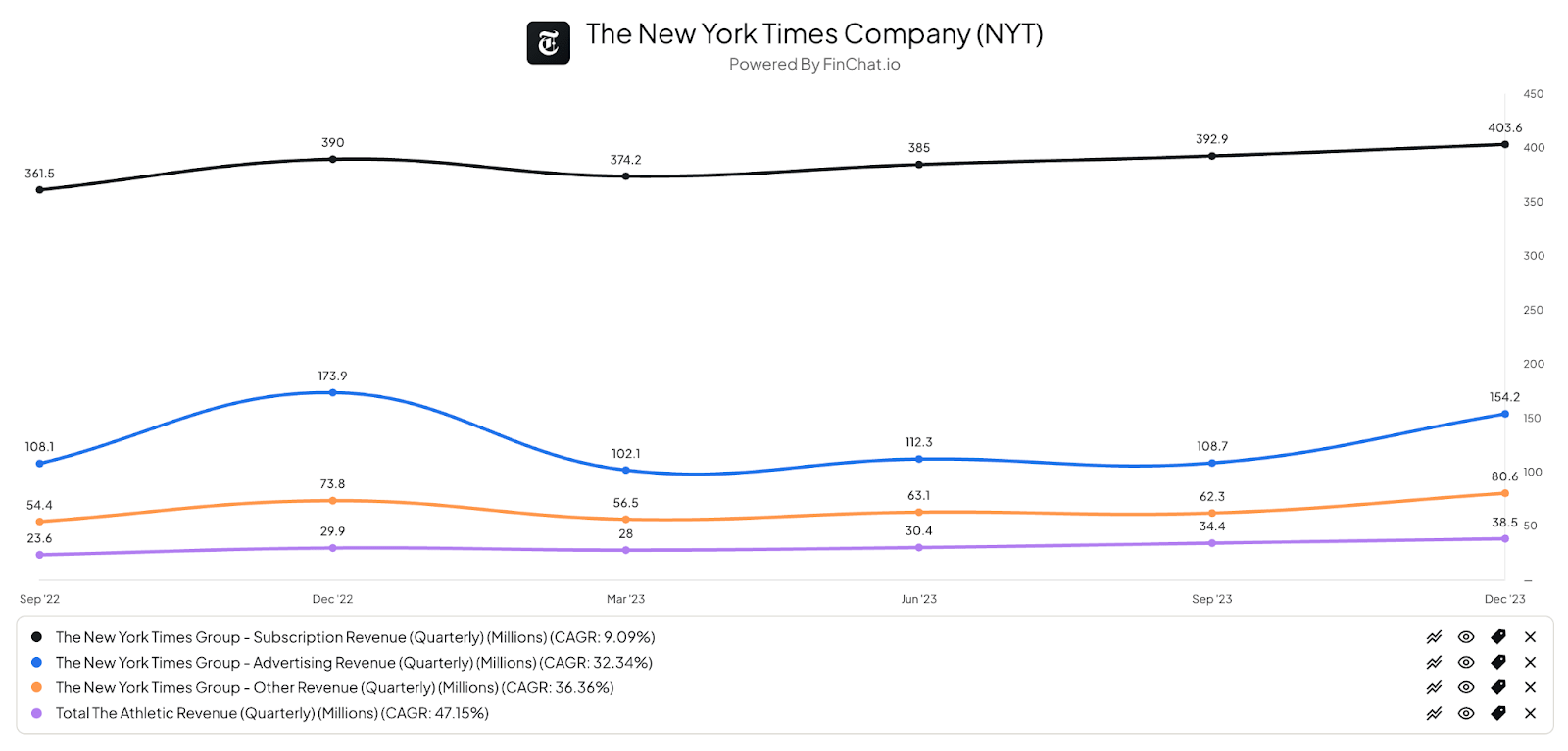

The New York Times derives revenue from various sources such as Subscription, Advertising, the Athletic and Other revenue.

FinChat.io

Notably, the fastest growing segment in percentage terms is from The Athletic while its largest revenue segment, Subscription, is growing at the slowest rate of growth.

The second-fastest growing segment, Other Revenue, includes licensing or syndication revenue from selling feeds to services like Apple News+ and others.

The company is focused on maximizing this revenue, as these large deals are almost "found money" to content producers like the NYT.

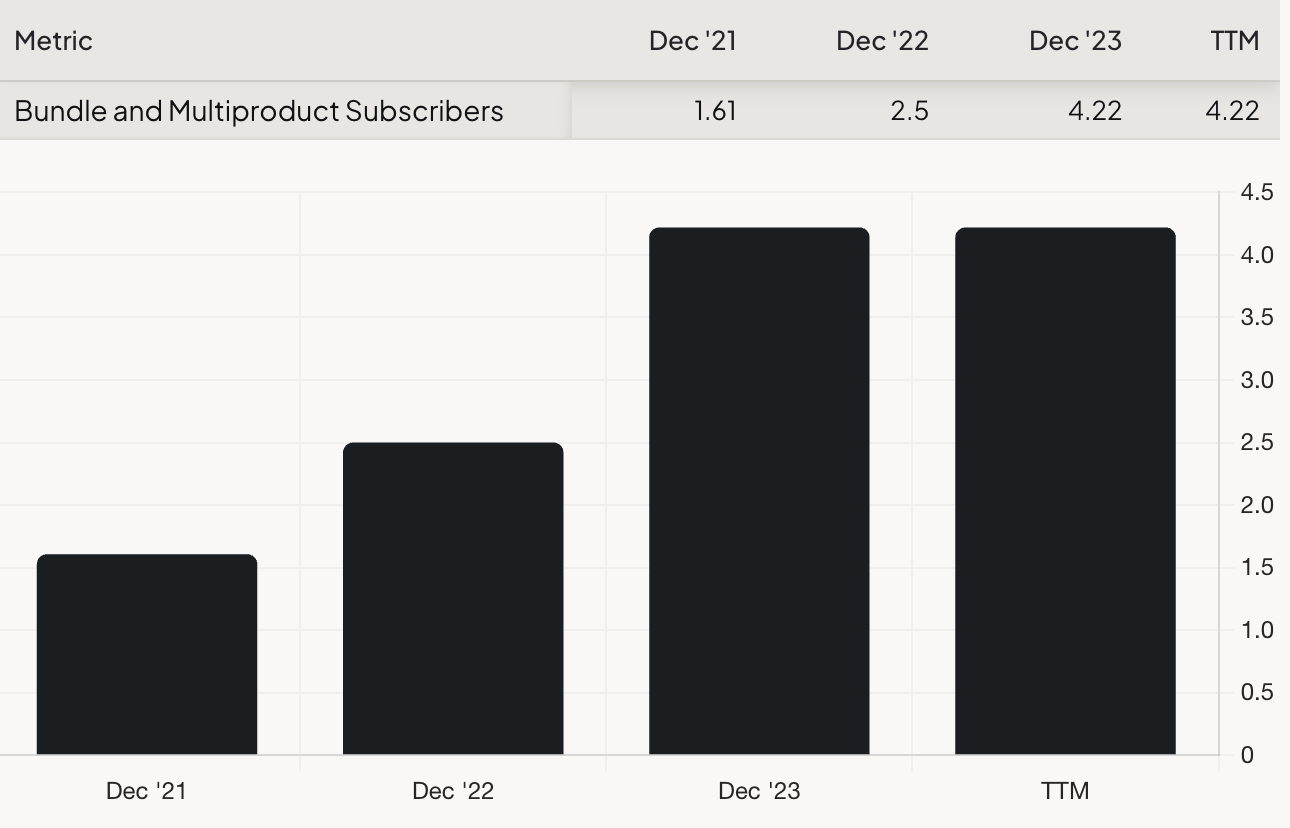

Management has been focusing on bundling various offerings in order to increase customer loyalty, drive revenue diversification and provide opportunities for cross-selling and upselling.

It has made good progress, with 4.2 million subscribers out of its 9.7 million purchasing more than one product or buying a bundle, per the chart as of the end of 2023 shows below:

FinChat.io

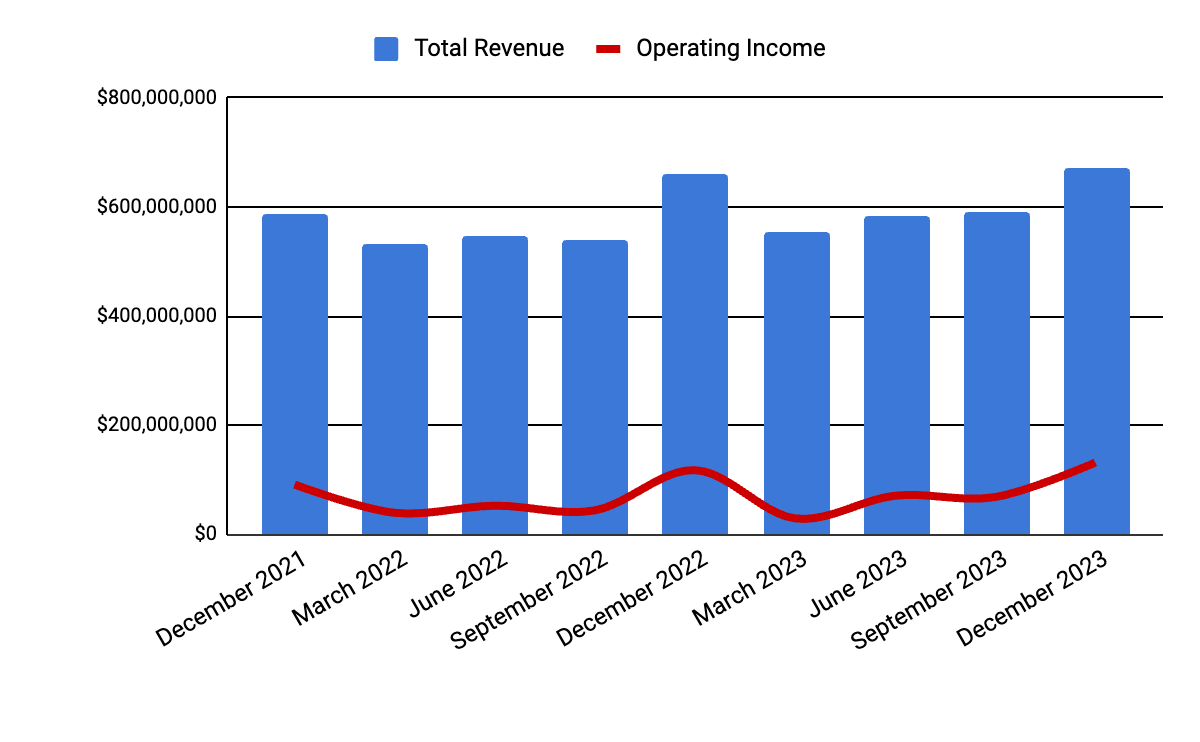

Total revenue by quarter (columns) has risen only moderately due to relatively muted growth in its major revenue segment of Subscriptions. Operating income by quarter (line) has turned up because of a rise in gross profit, likely due to its increasing revenue in non-Subscription segments.

Seeking Alpha

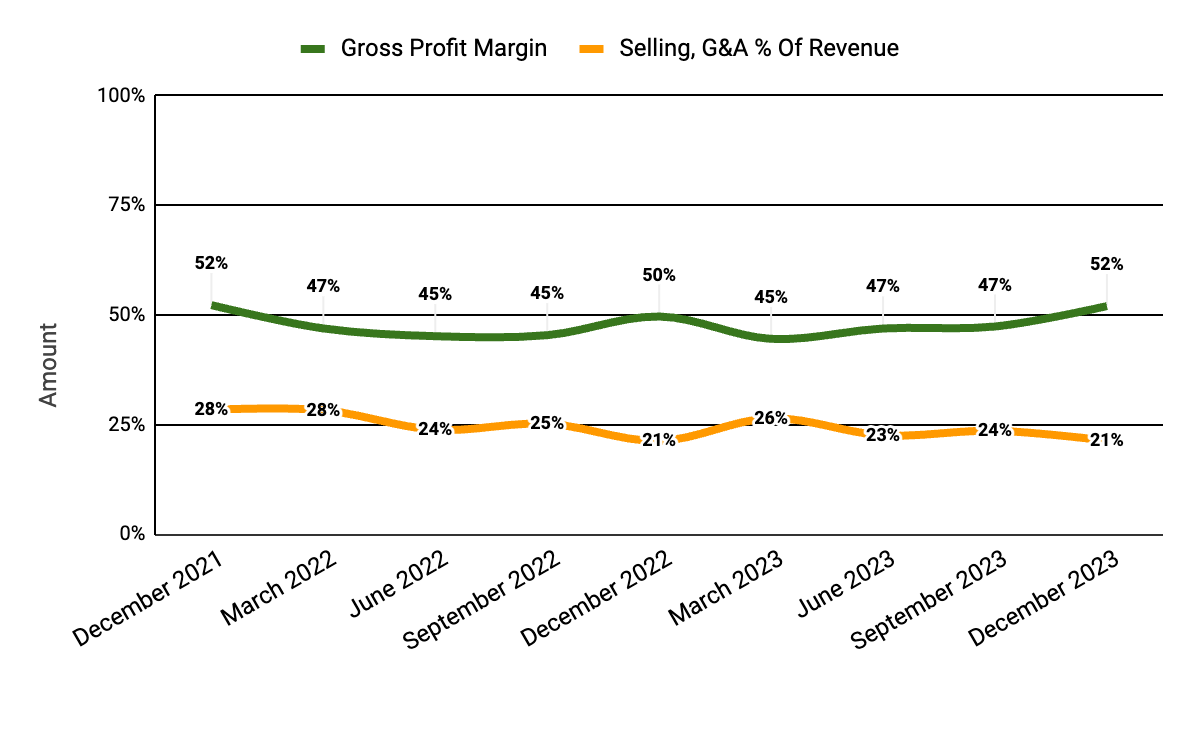

Gross profit margin by quarter (green line) has risen as a result of improved cost discipline; Selling and G&A expenses as a percentage of total revenue by quarter (orange line) have produced higher paid marketing results due to bundling and increased opportunities for greater marketing efficiencies.

Seeking Alpha

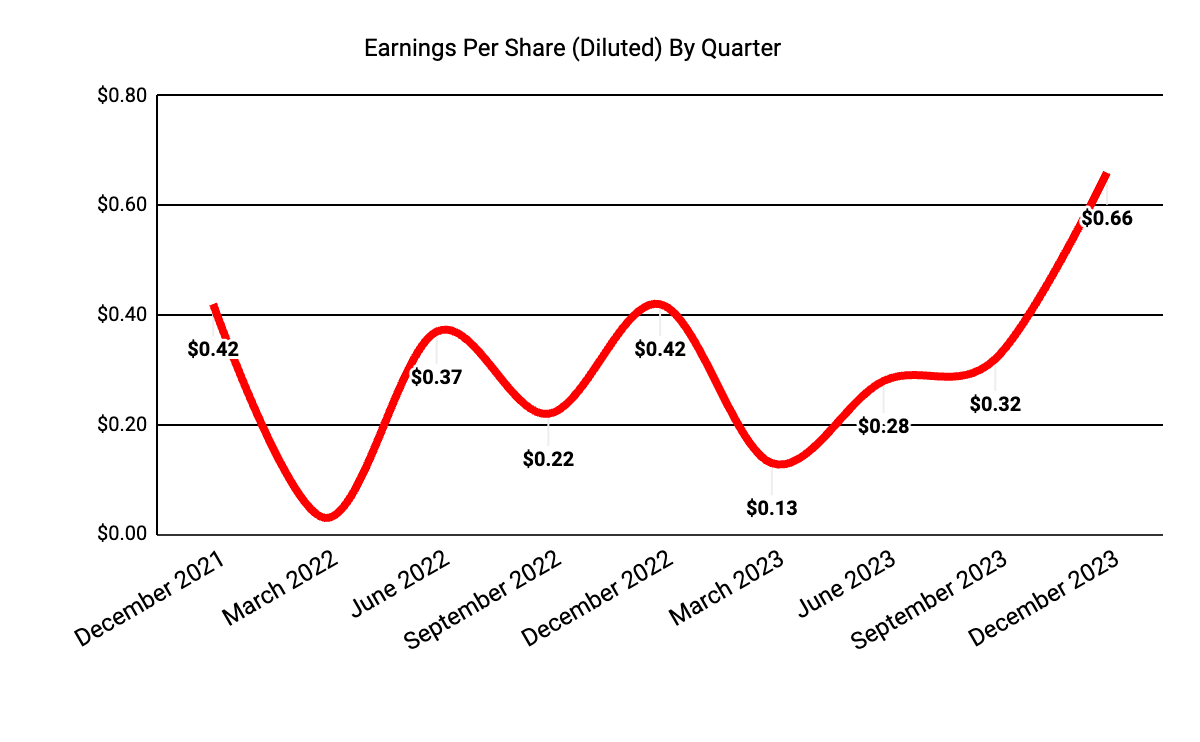

Earnings per share (diluted) have moved up sharply as a result of increasing operating leverage on moderately growing revenue:

Seeking Alpha

(All data in the above charts is GAAP.)

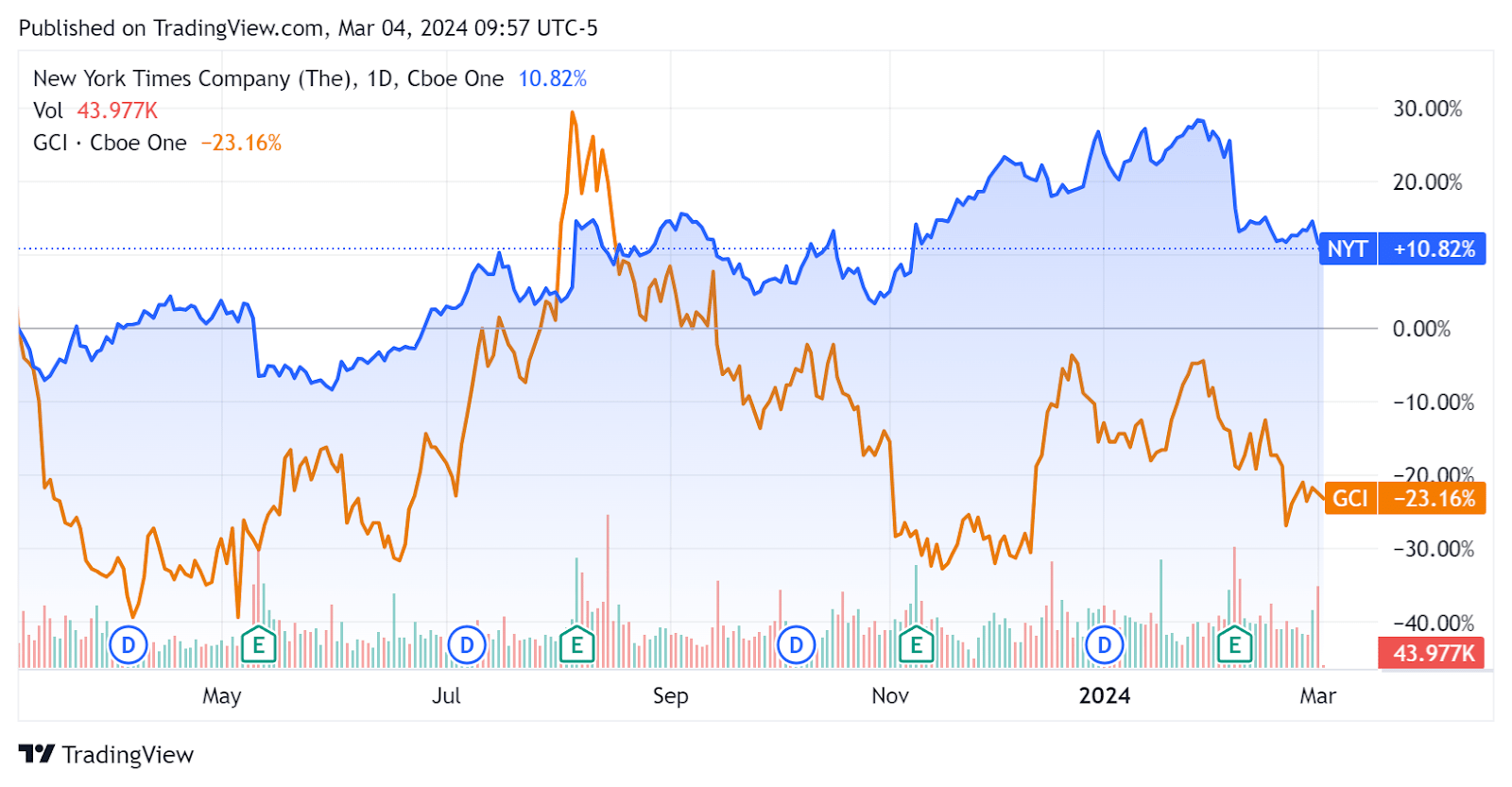

In the past 12 months, NYT’s stock price has risen 10.8% versus Gannett Co.’s (GCI) fall of 23.16%:

Seeking Alpha

The major metrics table is shown here and indicates strong free cash flow but moderate revenue growth:

Metric | Amount |

EV/Sales ("FWD") | 2.5 |

EV/EBITDA ("FWD") | 15.1 |

Price/Sales ("TTM") | 3.0 |

Revenue Growth ("YoY") | 5.3% |

Net Income Margin | 9.7% |

EBITDA Margin | 16.0% |

Market Capitalization | $7,080,000,000 |

Enterprise Value | $6,420,000,000 |

Operating Cash Flow | $360,620,000 |

Earnings Per Share (Fully Diluted) | $1.39 |

2024 FWD EPS Estimate | $1.68 |

Rev. Growth Estimate ("FWD") | 5.6% |

Free Cash Flow/Share ("TTM") | $2.05 |

Seeking Alpha Quant Score | Hold - 3.12 |

(Source: Seeking Alpha)

Although NYT isn’t an enterprise software company, the Rule of 40 performances illustrates its growth versus operating margin results, and is shown here, with revenue growth being relatively muted and pulling down this metric’s performance:

Rule of 40 Performance (Unadjusted) | Q4 2023 |

Revenue Growth % | 5.3% |

Operating Margin | 19.7% |

Total | 24.9% |

(Source: Seeking Alpha)

NYT management appears to have done a good job in maximizing the bundling, cross-selling and upselling revenue potential of its customer base.

It also has assembled a variety of online properties or products that assist in that bundling strategy.

But it can only go so far and only provide so many more opportunities on an existing customer base, and I’m seeing relatively modest revenue growth even with that success.

In my view, NYT will need to develop or likely acquire additional properties to include in the bundle, broadening its audience and addressable market in the process if it wants to meaningfully increase its topline revenue growth.

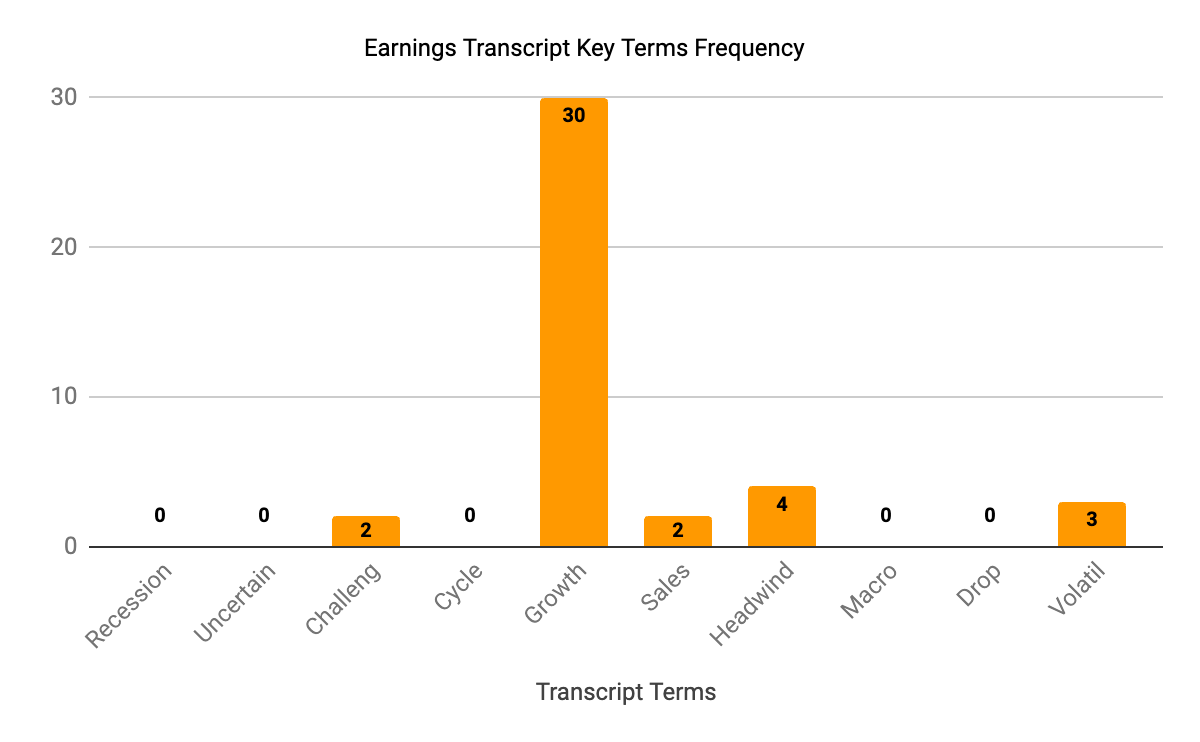

I prepared a sentiment visualization from management’s most recent conference call:

Seeking Alpha

Management has reported "headwinds" and "challenging" conditions in the online advertising market, which makes up a significant portion of the company's revenue, and it will always be subject to "volatile" conditions in the ad market.

That volatility will tend to be a drag on the stock, all other things being equal, as investors generally place a premium on predictable and stable results and discount stocks that exhibit greater volatility.

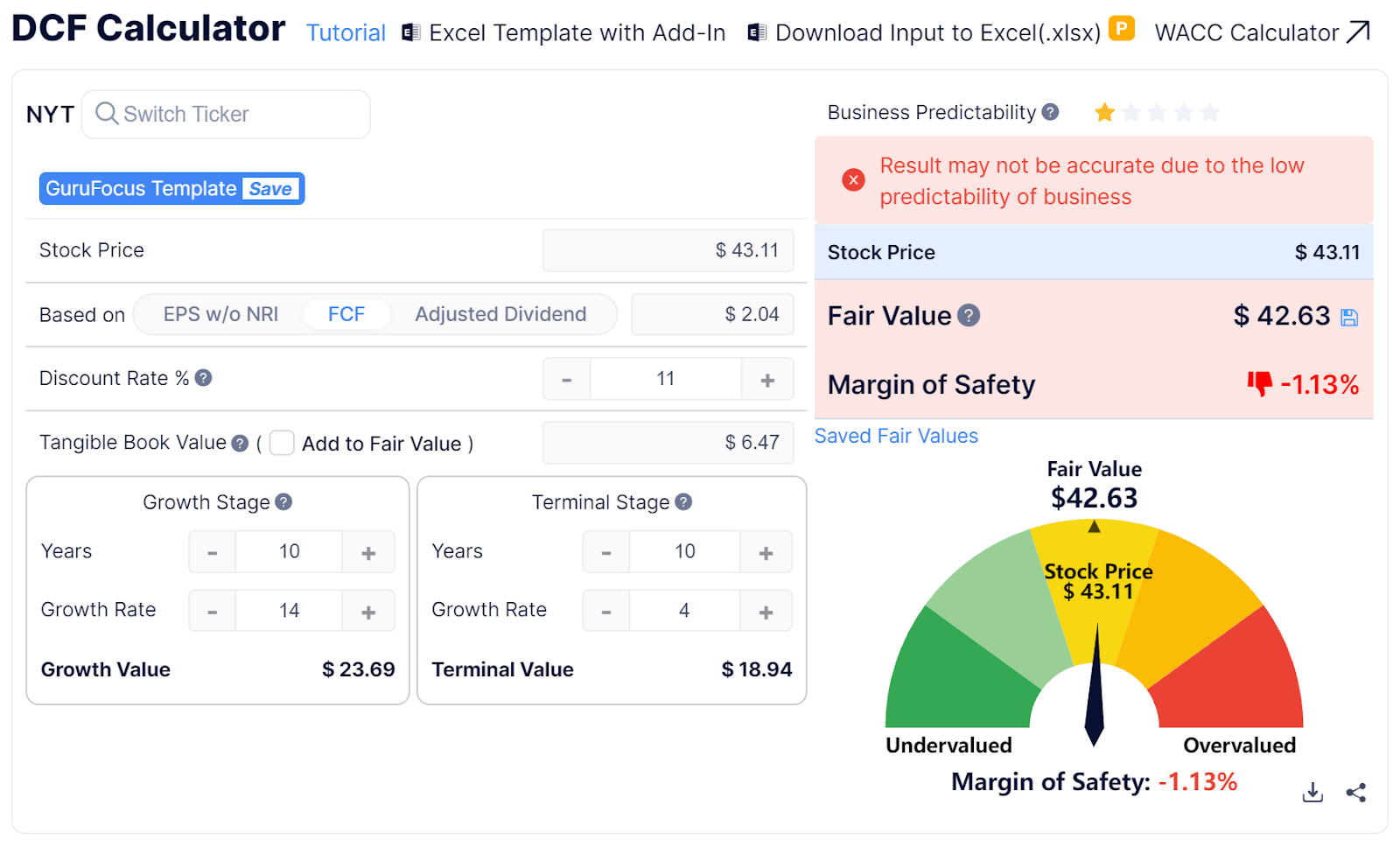

As to a potential valuation of NYT, my calculation indicates the stock may be fully valued on a free cash flow basis, given generous growth assumptions:

GuruFocus

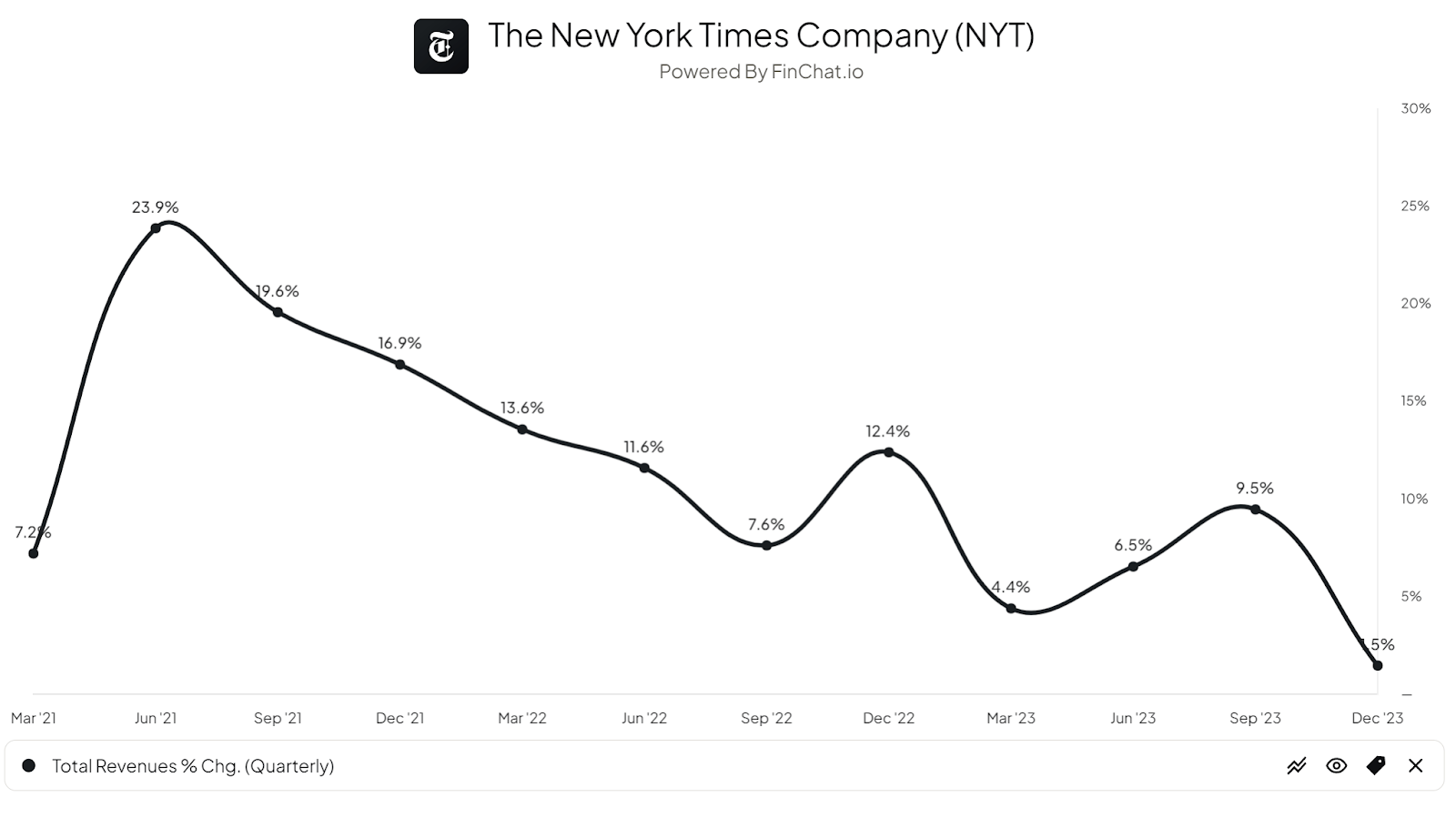

The biggest takeaway investors should have regarding NYT’s prospects can be shown in the dropping revenue growth percentages, as shown in the chart here:

FinChat.io

Although the NYT produced reasonably strong revenue growth during the pandemic, its year-over-year growth results have generally continued to drop in its aftermath.

With the most recent earnings release, the stock has dropped materially, perhaps as investors have been unimpressed by its anemic growth results and downward trend.

So, until management can develop or acquire meaningful topline revenue growth, I’m Neutral (Hold) on NYT.