JamesBrey

JamesBrey

NexPoint Diversified Real Estate (NYSE:NXDT) is a great example of a REIT that we believe the market is skeptical of. The current discount to NAV is close to 70% compared to the reported net equity value of the last 10-Q. Clearly, there is substantial doubt around the fair value of the highly diversified pile of assets of the company, and how and if this value can be unlocked.

However, we believe that while the common stock might seem not so attractive despite the discount, the preferred equity is becoming increasingly interesting. With some potential catalysts coming up, and the chances of higher RE valuation ahead, NXDT preferreds present a nice risk/reward ratio.

NexPoint, as the name suggests, is a diversified REIT. It has different kinds of properties, but also different kinds of assets representing these properties. Indeed, it is usual for them to acquire a stake through various instruments, from senior loans, LP interests, or even common and preferred stocks, or eventually mezzanine debt.

This is what is probably concerning the market, as it is very difficult in this period of high rates and low RE valuations to have a clear view of NXDT's portfolio fair value.

However, there are some contributors that are larger than others in the computation of the NAV, let's see them.

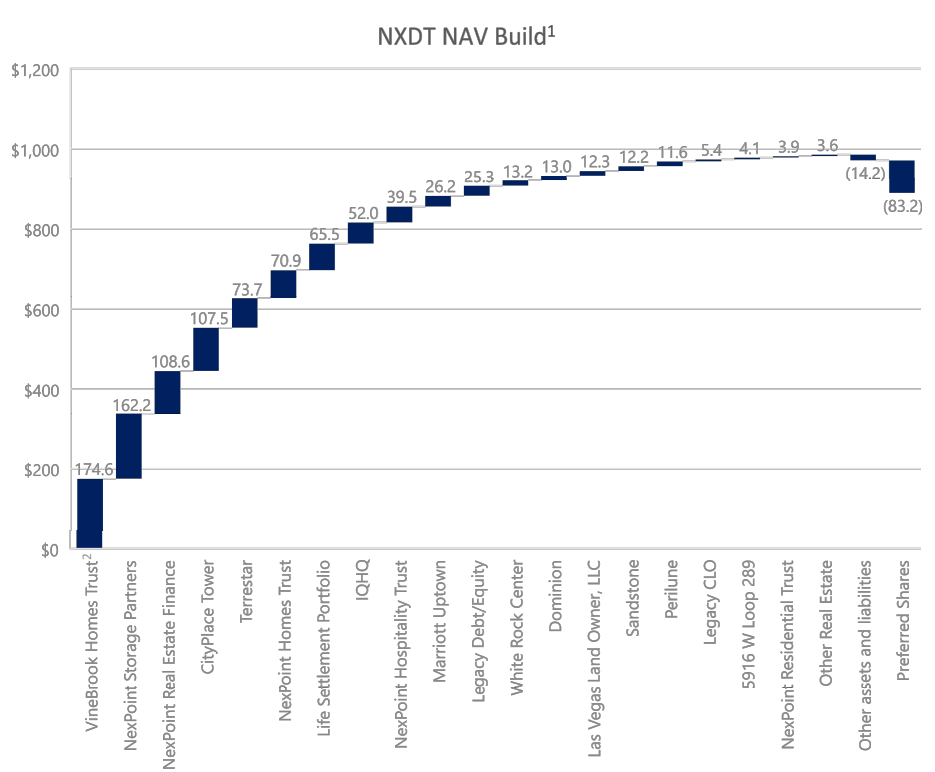

NXDT NAV (Latest Presentation)

We can note that VineBrook Homes Trust and NexPoint Storage Partners are the two largest assets, contributing close to $400 million. The first one is an LP interest in a Single-family rental business. NXDT owns 11% of this trust which is very large and it has a diversified exposure to various markets in the US.

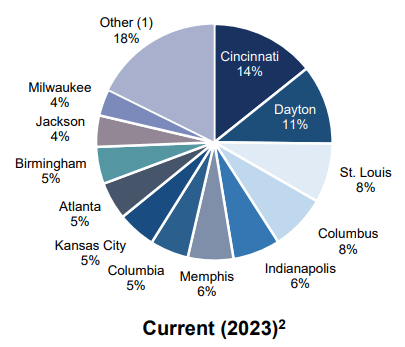

NXDT - VineBrook Portfolio (VineBrook Presentation)

This is a map that shows the major locations of the VineBrook Home Trust portfolio. It looks fairly diversified and the single-family market is definitely less distressed than other sectors like office or industrial. Then there is the self-storage LLC interest, NexPoint Storage Partners, where NXDT owns around 30%. This is another interesting sector that seems to still be attracting some capital despite high rates.

"Despite the rising cost of debt, capitalization rates for self-storage remain relatively stable, averaging 5.1% in the second quarter of 2023"

We are thus encouraged by the fact that these two assets which represent close to 40% of the entire NAV of NXDT have no signs of distress and are not office or industrial-related.

Let's now move to the income side of the story. It is very important to look at how much NOI is available to eventually pay dividends to preferred shareholders.

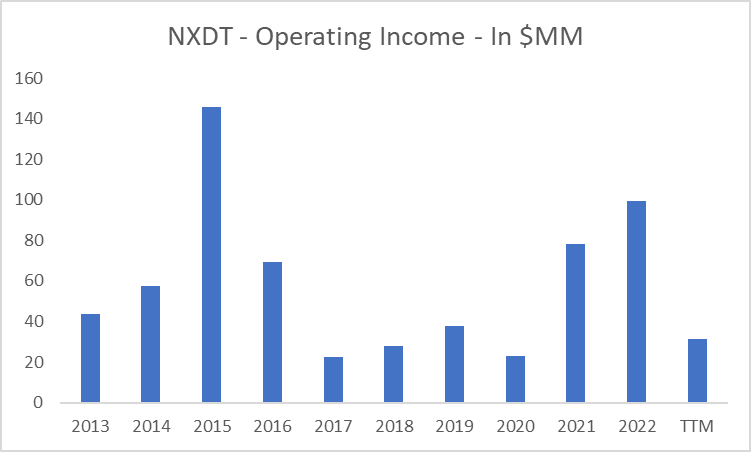

NXDT - Operating Income (Seeking Alpha)

As one can notice NOI has been on roller coasters in the last decade. After a period of very depressed levels between 2017 and 2020, higher valuations helped a lot in the 2021 and 2022 periods, and NOI increased substantially. However today it is back to around $30 million for the last 12 months, which translates into a P/NOI of around 10.

NXDT offers quite a risky profile for two main reasons: (1) a balance sheet very difficult to value, and (2) a highly volatile NOI. This is also why the common stock is down 25% YTD, and 60% in the last 5 years. The uncertain NOI also creates concerns around total return for the common stock, as dividends are cut to accumulate liquidity or pay others across the capital structure.

This is why we believe that investors should take a different approach and perspective, by looking at the preferreds. NexPoint issued these stocks in 2021, with a coupon of 5.5%, and a liquidation preference (not par value) of $25 per share. The terms dictate that the company is free to redeem - at $25 per share - the preferreds starting on December 15, 2023.

Now let's visualize these terms along with a YTM computation to see why we like this opportunity.

Liquidation preference | $25 |

Coupon | $1.37 - 5.5% |

Current yield | 9.7% |

Estimated maturity | 10 years |

YTM | 13.6% |

To give a better perspective we made some assumptions to also derive a YTM. This is the yield that takes into account the repayment to the liquidation preference at the end of the period. Preferreds do not have expiration, but we think that there are a number of scenarios where the company wants to dispose of these securities:

To simplify the capital structure. Given that the common stock trades at deeply depressed levels in terms of discount to NAV, it would make sense to use some extra liquidity in the future to redeem these shares.

In case of a change in control. Many REITs are acquired, and it is not unlikely that NXDT will change hands given its high discount. In this case, preferreds will be likely redeemed to clean the capital structure.

This data definitely looks interesting. We are granted a current yield of 9.7%, above the 7% of the common and also with a liquidation preference higher than the common. YTM assuming something happens in the next 10 years is above 13%.

If we were to estimate a shorter time frame, likely in the form of an acquisition in the next 5 years or so, the YTM would skyrocket to around 19%. Definitely a good potential return.

We believe that NXDT presents a very low probability of things going really bad. This is because they have a relatively conservative leverage ratio, with only $200 million in liabilities and more than $1.1 billion in assets. Now we could discount these assets as much as we would like, but an LTV of less than 20% provides a huge margin of safety.

Plus we need to consider that we are buying preferreds, which sit above common stock in the capital structure. These securities not only have a mandatory accruing coupon but are also liquidated before the commons and right after debt in case of liquidation/bankruptcy.

However, we spot one main risk: depressed NOI for a prolonged time. This is the case of income and revenues depressing again below pre-Covid levels, and not allowing for timely coupons on the preferreds. This of course decreases the time value of those payments, thus lowering the YTM.

NexPoint Diversified Real Estate is trading at deeply depressed levels of its NAV. We believe that the markets are concerned about the true fair value of many of their assets. However, instead of looking at the common stock, we think the preferreds offer a much more attractive risk/reward ratio. These securities offer an attractive potential yield to maturity in the 13-19% range, depending on if/when they are redeemed.