Smith Collection/Gado/Archive Photos via Getty Images

Smith Collection/Gado/Archive Photos via Getty Images![]()

I believe Newell Brands Inc. (NASDAQ:NWL) deserves a buy rating. While the 4Q23 results were mixed, FY24 could be the turning point for the business in both revenue growth and margin expansion. Management FY24 core sales guidance, adjusted for the exit of unprofitable business units, implies sales growth has somewhat stabilized. Given how the January’24 performance is, along with the expected product launches and contribution from distribution wins in late 23, I expect FY24 to meet management guidance easily. NWL restructuring efforts and growth strategies also set up a good outlook for FY25 and beyond.

NWL is a consumer goods company that mainly sells house-related products (housewares and home furnishings) and office-related products (office supplies, tools, and hardware). Some of the key brands in NWL’s portfolio are Rubbermaid, FoodSaver, Coleman, Graco, etc. NWL is a global business but has most of its revenue coming from North America (69% in FY23), 15% in EMEA, 9% in LATAM, and 7% in APAC.

At first sight, NWL seems to have done well relative to consensus in 4Q23, as it reported EPS of $0.22, beating consensus expectations of $0.17 and management's own guidance of $0.20 at the high end. However, the beat was mainly due to a normalized tax benefit that should not repeat in the future, and notably, NWL core sales continue to decline by 9.3% (although this was better than guided) driven by weakness across all segments. Home & Commercial Solutions (H&C) saw an 8.2% decline, Learning & Development (L&D) saw a 7.7% decline, and Outdoor & Recreation (O&D) saw a 21.8% decline. That said, a positive area was that gross margin saw 570bps of expansion to 32.3%, and this deserves to be mentioned because it is the second consecutive quarter of sequential margin expansion. The strong gross margin performance also drove EBIT margin to improve to 7.7%, a 280bps expansion vs. 4Q22.

I believe FY24 could be the inflection point for NWL. Management is guiding core sales to decline by 3 to 6% (4Q23 earnings transcript). While it is going to stay negative, note that the guide marks a big “recovery” step up from the -11.5% organic sales growth seen for FY23. Also, I should also bring up the fact that FY24 core sales are going to be impacted by expected distribution losses and product line exits as NWL is exiting unprofitable businesses. This exit impact is expected to outweigh any distribution gains by 200 bps. If we adjust for this, at the high end of the guide, it almost implies that NWL has reached a stabilized point of this cycle (high end of guide: -3% organic decline, adjusted for 200 bps = -1% expected organic decline).

Redfox Capital Ideas

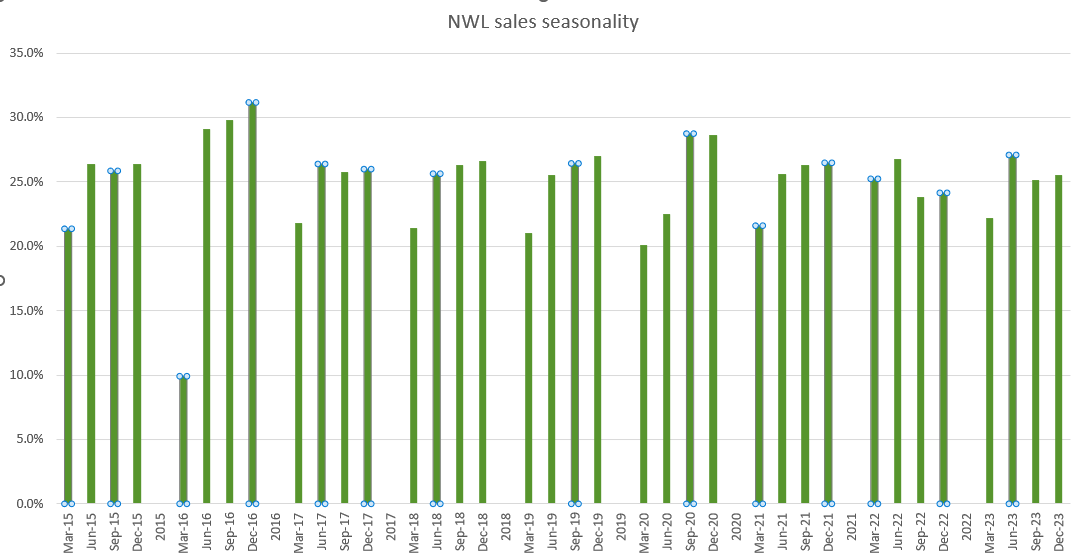

NWL appears to be tracking well against this sales guide, as management mentioned they are off to a better-than-expected start in January than implied in the guidance. Remember that January is a light-season month and 1Q is typically the smallest quarter (relative to other quarters of the year), which means we should see a similar trend for the rest of the year (if seasonality for FY24 remains the same as in the past). There are two other reasons why I believe FY24 will have a better performance than FY23. Firstly, this year, NWL will launch eight innovations, including some new products and services. For example, the Sharpie creative markers will be available in March, and the rest of the innovations will mainly be launched in Q2 and Q3. Secondly, the new distribution wins with new customers that were announced in late 2023 will begin to be delivered in FY24.

In addition, there are other qualitative aspects that make me believe that FY24 is going to set up a good year for FY25 and beyond.

Firstly, it is the planned organizational restructuring at NWL, which was announced in January. Management will be implementing a cross-functional brand management structure for its top 25 brands, which will include departments such as supply chain, customer strategy, finance, and brand management. This will improve execution across the board. I really like this new structure as it allows for a more holistic view of demand, trends, and approaches to driving insights on consumer purchases. As NWL streamlines and standardizes its regional structure, more decentralization of authority is anticipated as a result of this restructuring effort, which should also have a significantly positive impact on NWL international business. Unlike in the NWL homegrown market (North America), speed in decision-making and having ownership in making key decisions are important for international markets as the management team on the ground is more well-versed than the team in North America.

Second, the anticipated number of Tier 1/Tier 2 in 2024 (4Q23 earnings transcript), as opposed to zero in 2023, demonstrates that NWL is shifting its innovation strategy to concentrate on bigger initiatives and bigger bets. I anticipate that NWL will maintain its commitment to this, increasing the number of launches planned for FY25. This should aid in maintaining and expanding upon the market share achieved in FY23 (management noted increasing market share in 8 of the top 25 brands in FY23.

Part of management’s guidance is for another 100 bps of EBIT margin expansion (implied from the EBIT guide at the midpoint) and for gross margin to expand by even more than 100 bps. I believe this margin expansion is possible given that NWL is shedding the unprofitable business, generating a lot of cost savings so far from improvements in productivity, and going to benefit from higher gross margins from the new product launches.

Normalized gross margin improved sequentially each quarter and inflected positively in the back half, driven by record-setting productivity performance and the July pricing action to proactively address situations where unit economics were untenable.

Amidst a challenging operating environment, during 2023, we drove record productivity across the supply chain, significantly improved cash flow by right-sizing inventory, further reduced Newell's SKU count, and took decisive actions to strengthen the company's front-end commercial capabilities.

So, for example, if you look at the eight Tier 1 and 2 initiatives that we have planned to launch this year, every one of the eight initiatives is a significant improvement to gross margin versus the business that it's in.

4FQ23 earnings, Chris Peterson (CEO)

Redfox Capital Ideas

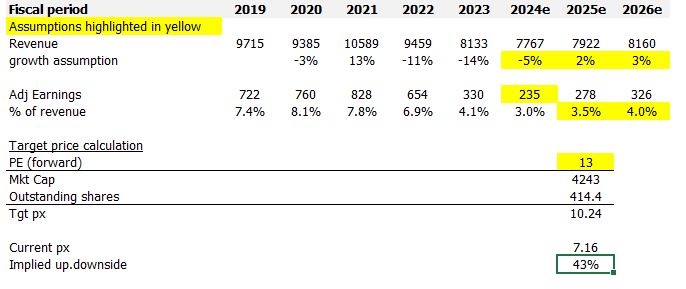

I think the upside opportunity here is quite attractive if we see continuous acceleration in growth and margin improvement. In my opinion, if NWL executes well on its growth opportunities (new product launches and distribution won in late FY23), growth should turn positive by FY25 (FY24 to come in line with guidance) and further acceleration in FY26. My growth assumptions follow the NWL's most recent recovery cycle (post-2009), where the first year of recovery was in the low-single-digit percentage range, followed by modest improvements. For margin, I am expecting further expansion over the next few years as the factors I discussed above bear fruit. I believe that NWL can eventually reach its historical margin level, but since a part of NWL's growth strategy is to roll out new products, I expect management to step up on reinvestments. Hence, I don’t expect the margin to reach back to historical levels in the near term. My model assumes NWL net margin to recover to FY23 levels by FY26 and FY24 to follow management guidance (calculated from its guided adj EPS at the midpoint). Lastly, with anticipation that NWL performance is going to get better in the coming years, I attached a 13x forward PE multiple to NWL, which is where it is trading today, and also its average.

NWL could continue to face demand weakness for discretionary categories if the inflationary and high interest rate environments sustain for longer than expected. The latest inflation data shows that inflation is sticky, and the Feds might pull off any rate cut until they see solid proof of inflation easing. In addition, the current restructuring efforts might take a bigger toll on the near-term margin if not executed well. Lastly, NWL valuation has recovered from the low end of its valuation curve back to average, implying that the market is expecting some form of recovery. If NWL fails to meet expectations, it might hurt the stocks’ sentiment.

I recommend a Buy rating for NWL as I anticipate FY24 to be a turning point for the company. Despite mixed 4Q23 results, management's core sales guidance for FY24, adjusted for the exit of unprofitable business units, suggests stabilized sales growth. January's better-than-expected performance, upcoming product launches, and distribution wins position NWL for a better FY24. The organizational restructuring and a shift towards larger innovation initiatives set up a positive outlook for FY25 and beyond. I do think that margin expansion is plausible, driven by shedding unprofitable businesses, cost savings, and higher gross margins from new products. Risks include prolonged demand weakness in discretionary categories and challenges in restructuring.