gorodenkoff/iStock via Getty Images

gorodenkoff/iStock via Getty Images

NVR, Inc. (NYSE:NVR) is a leading home construction company in the United States. The company operates through its various subsidiaries, including Ryan Homes, NVHomes, and Heartland Homes, and primarily focuses on the construction and sale of single-family homes, townhomes, and condominiums in key markets across the country.

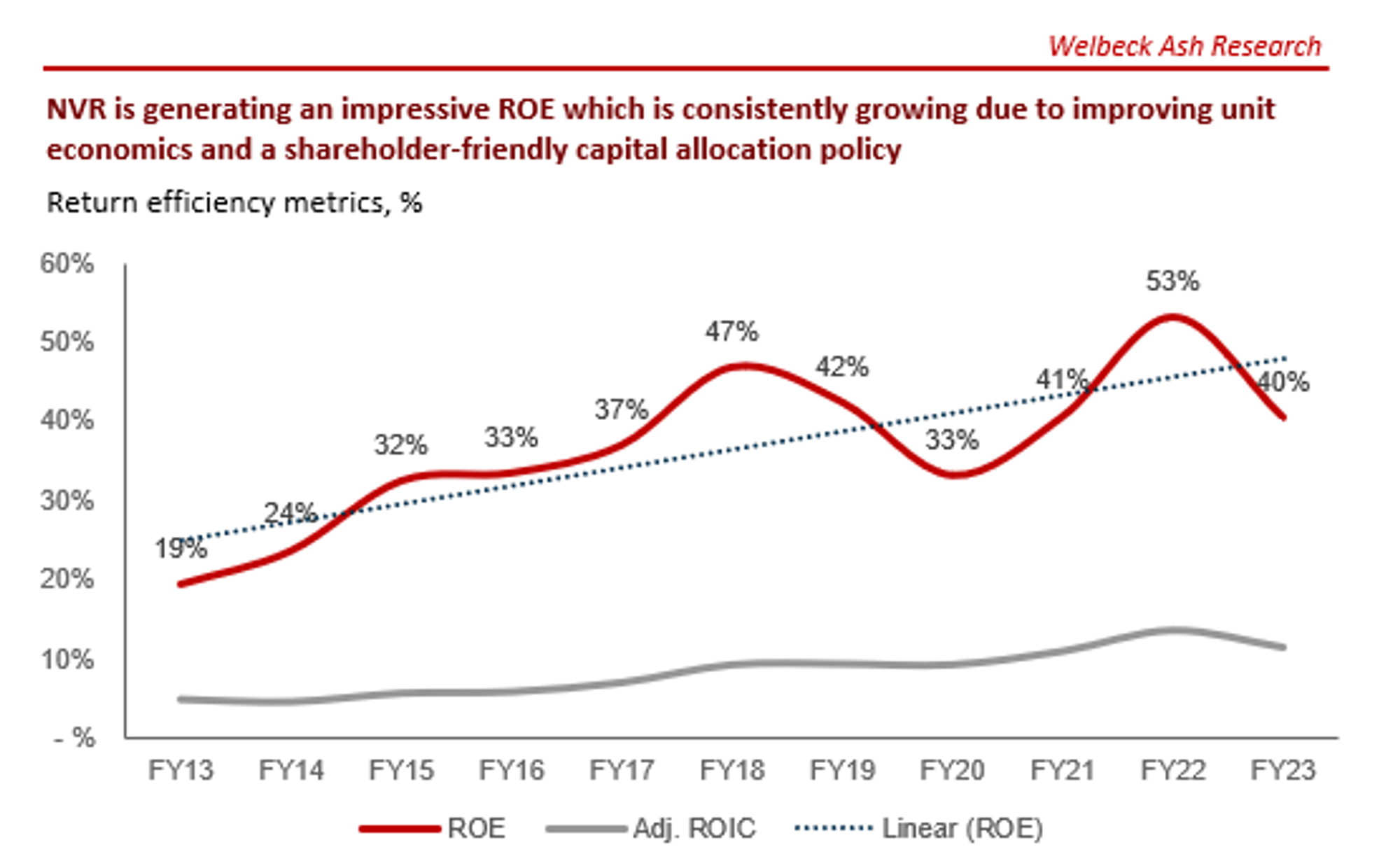

NVR is a market-leading business, with all the hallmarks of a long-term compounder. Management is efficiently allocating capital, while its approach to operations de-risks the cyclicality that comes with homebuilding. We do not believe investors are materially losing out with NVR and its ROE illustrates the efficient nature of its returns.

We believe the housing industry will experience another upward cycle, allowing for returns to accelerate. The pipeline is strong and consumers are awaiting an end to these elevated rates, which appears within touching distance.

At a current FCF yield of ~7% and a return to growth appearing imminent, we believe investors can enjoy healthy returns in the coming decade. For this reason, we rate the stock a buy.

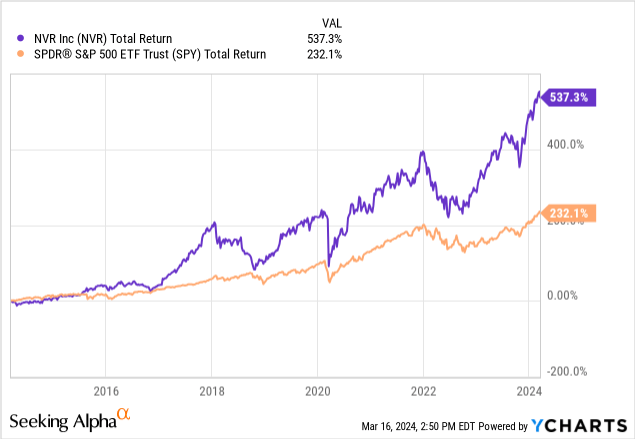

NVR’s share price performance has been magnificent, materially outperforming the S&P500 and soaring to over 500% returns. This is a reflection of its impressive financial development during this period and compounding tailwinds that position the business well for long-term returns.

Capital IQ

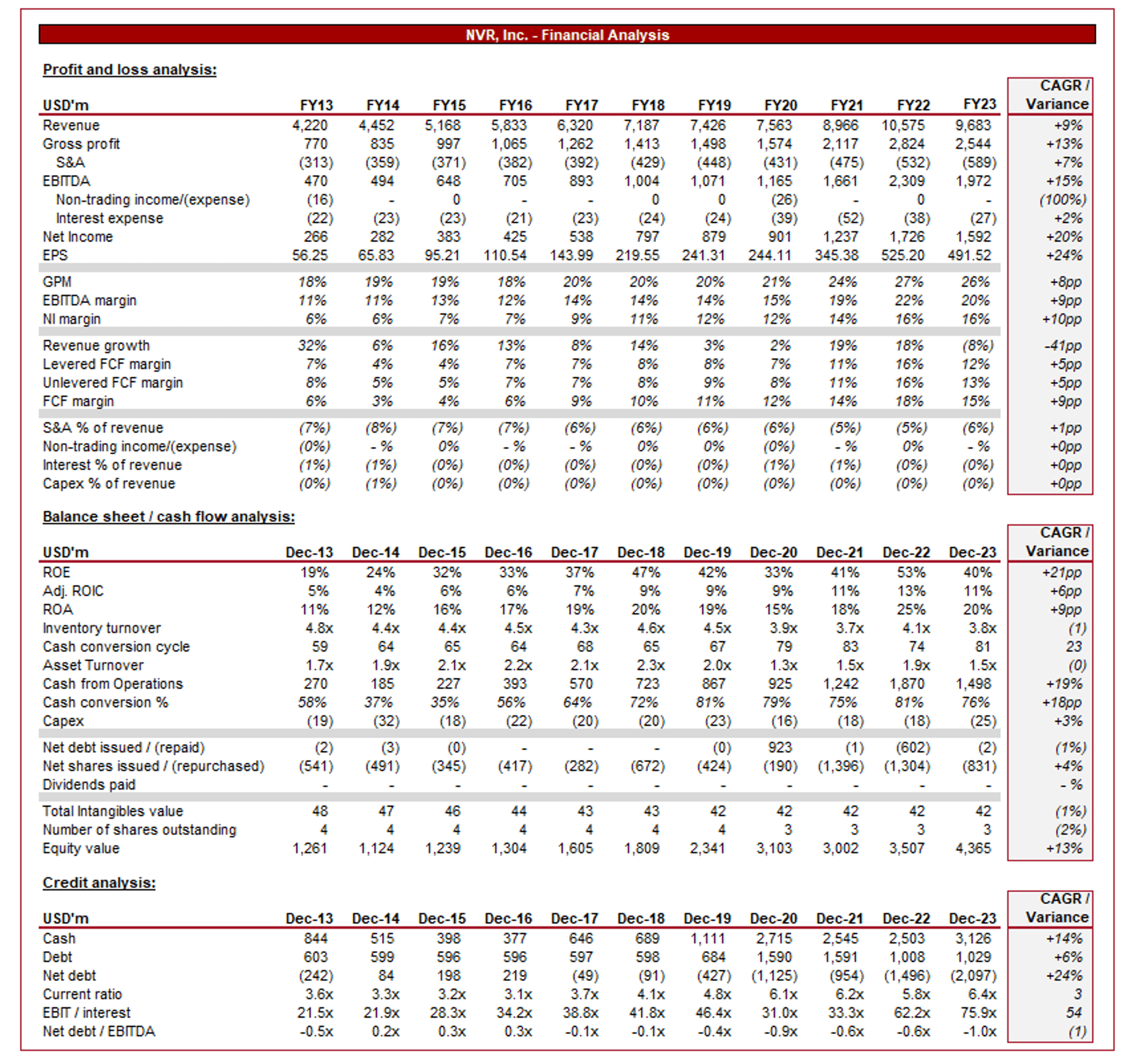

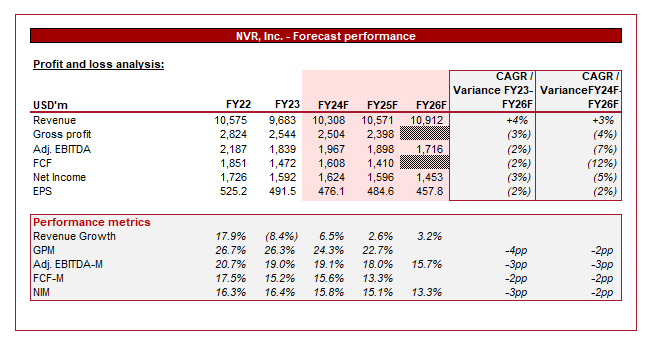

Presented above are NVR's financial results.

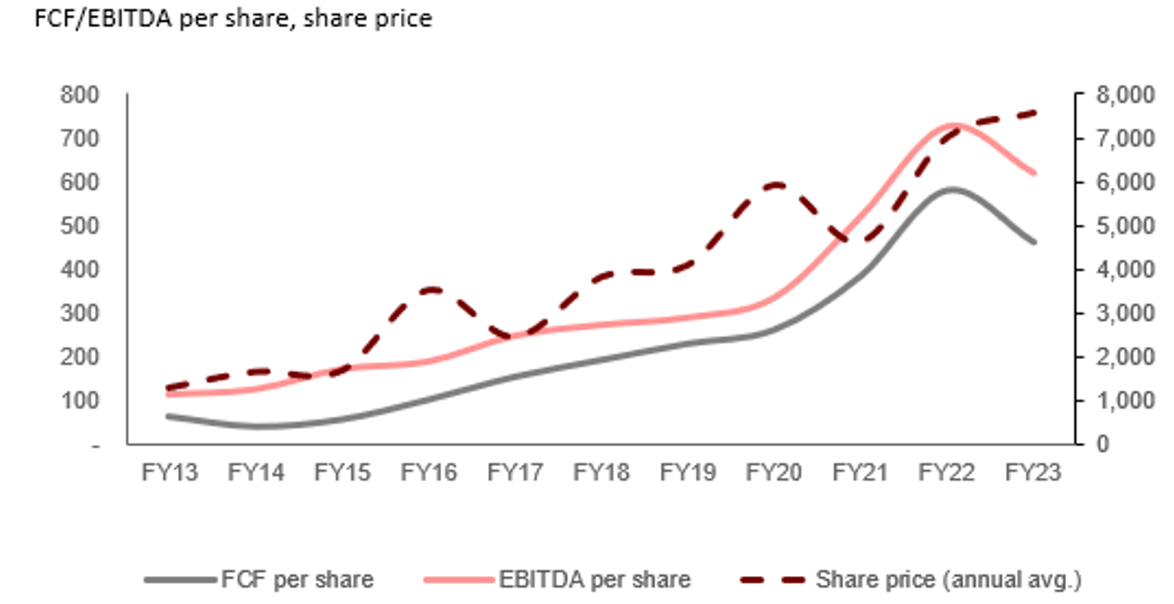

NVR’s revenue has grown well during the last decade, with a CAGR of +9% into FY23 and a linearity to time of 1, reflecting its supreme consistency. EBITDA has exceeded this at +15%.

NVR specializes in the construction and sale of single-family homes, catering primarily to homebuyers in the United States. The company operates in sixteen states through its various subsidiaries, including Ryan Homes, NVHomes, and Heartland Homes.

Operating multiple distinct brands allows NVR to target different market segments and geographic regions, differentiating its market offering while allowing each brand to benefit from shared competencies and group-level capabilities.

NVR's business model fundamentally involves acquiring land in desirable locations and developing residential communities that appeal to homebuyers. The company carefully selects sites based on factors such as location, demographics, market demand, and regulatory considerations to maximize the value of its investments. The key factor differentiating NVR, at least from significantly smaller peers, is its ability to identify and acquire sites quickly and at a substantial scale. NVR has considerable financial and human capital it commits to the development of its land pipeline, a feat very few in the industry can rival. Further, unlike many of its larger peers, NVR operates a “land-light model”, using LPAs (lot purchase agreements) to limit its direct exposure to land, which inherently has risks associated with valuation and development potential (such as inability to get permission to build or the discovery of issues). Further, this means NVR does not borrow to fund land acquisitions, another riskier approach. A succinct explanation of its approach can be found below.

NVR enters into option contracts with land developers that give it the right, but not the obligation, to take down finished lots at a predetermined price and pace. NVR attempts to structure its purchase agreements so that it takes ownership of the lots on a just-in-time basis, immediately before building a sold home. The only recourse to NVR is a nonrefundable cash deposit up to 10% of the full purchase price.

This allows the company to boast a substantially higher ROE due to its asset-light model relative to the conventional ownership approach, while de-risking land ownership as it only takes the land on-balance sheet once a sale is certain.

Further, the company has transitioned away from a vertically integrated model but maintains a centralized approach, allowing for a de-risked cost profile and efficiency through optimization. The company manages key aspects of the homebuilding process in-house, including land acquisition, architectural design, sales, and customer service, while outsourcing many key manufacturing tasks. Whilst it could be cheaper to vertically integrate here, NVR would then assume further risk. Instead, the company has reduced its cost in other areas to offset the impact.

NVR’s competitive position is primarily based on its scale and capabilities in homebuilding at an attractive cost, underpinned by the quality of its land bank acquisition approach. Importantly, NVR is a lower-risk option for investors, as evidenced by its incredibly consistent growth and ability to remain profitable during all cycles, evidenced during the financial crisis where NI and EBITDA remained positive.

Whilst the leading players within the industry do compete for land, they generally operate within their specific segments, such as geographies, keeping out of each other’s way (to an extent) and allowing all to prosper. NVR, as an example, is razor-focused on its specific geographies and seeks to dominate these markets, rather than taking a broad-brush approach across the US.

The US homebuilding industry is forecast to grow at a CAGR of +5% in the coming decade, driven by population growth, economic development, and urbanization. During the last 2 decades, there has been considerable immigration into the West, alongside demand for homes as investments as well as for living due to record-low rates, contributing to soaring prices and a growing delta between supply and demand.

This is not an issue that will be imminently resolved, owing to inefficiencies in the market, including the NIMBY movement amongst other factors. This should allow for consistent growth in the coming years, which we suspect could easily exceed the 5% level forecast, with quality land acquisition paramount to success.

A lesser consideration within this industry is the evolving nature of homes. Consumers are increasingly turning to modular / pre-built homes due to supply-side issues, while regulation and changing social ideals are contributing to the need for green homes. These factors have the potential to disrupt the status quo, which thus far has only benefited from the industry’s inefficiencies.

Major competitors of NVR include other homebuilders such as Lennar Corporation (LEN), D.R. Horton (DHI), PulteGroup (PHM), and Toll Brothers (TOL). These businesses broadly differentiate themselves through the quality of their homes, namely location, build quality, and options. To a lesser extent, brand perception, customization options, and customer service. As we discussed, competition is primarily at the land acquisition level, with sufficient “room” in the US for all large firms to win currently.

NVR’s recent performance has materially slowed relative to its historical trajectory, with top-line revenue growth of -7.0%, -10.8%, -6.3%, and -9.5% in its last four quarters. In conjunction with this, its margins have softened, albeit remaining above FY21 levels.

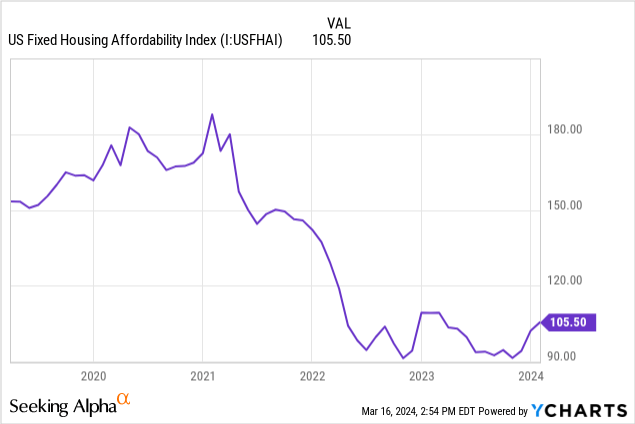

This decline is a reflection of economic conditions we believe, with a YoY decline in units settled of -7.2% in Q4, alongside a decline in average settlement price of -3.5%. With elevated interest rates and inflation, consumers have suffered from a cost-of-living crisis, as wage inflation has struggled to keep pace. This is best reflected in the US FHA index, which fell below 100 (parity of home affordability relative to income) for the first time in 2022, remaining below until recent months. With such an attack on finances, many consumers were/are clearly not in a position to afford home ownership in our view.

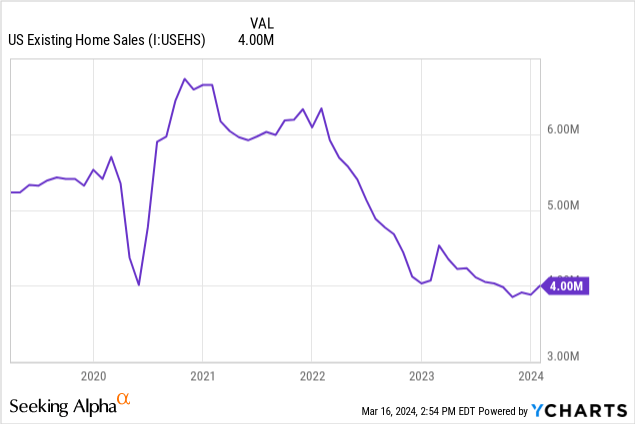

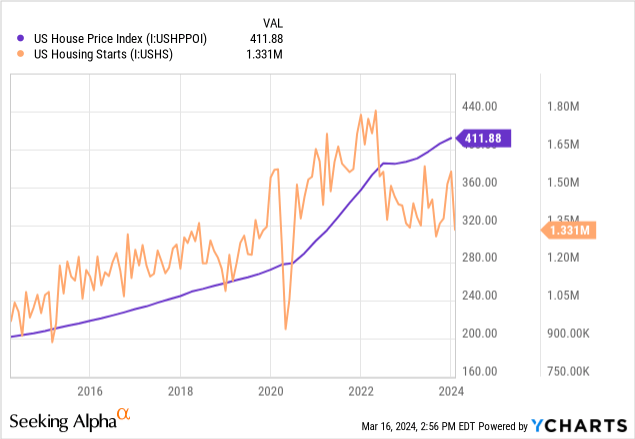

The biggest factor clearly, however, is the level of interest rates. Following a decade of record-low levels, consumers have seen the cost of ownership soar, pricing many out. Further, the nature of the mortgage market in the US means those who do own a home are locked in for the long term (10Y+), and so to move home would require foregoing said record low rates for double or triple the monthly costs. As the following illustrates, there has been a material decline in home sales, reflecting this decline.

Unsurprisingly, this has led to a retreat of homebuilders (decline in starts seen below), as they are unable to achieve their target ROI, seeking to instead delay until which time market conditions improve.

This said, we are not overly bearish despite the clear slowdown and potential for lasting damage from inflation. As the below shows, US home prices have broadly increased during this period (see below), which we believe is because of the impact of tailwinds offsetting these factors. Consumers likely know the value of home ownership now more than ever due to the shortage, so are hunkering down and awaiting an end to this higher interest rate environment. All signals suggest rates will decline in 2024, supporting this thesis.

Looking ahead, we believe NVR could achieve meaningful growth as early as H1’24. New orders by unit were up 25.0% in Q4 while the average price was only down 1.8%. This implies an already improving situation, which will only be accelerated by rates falling.

Analysts are forecasting a growth rate of +4% into FY26F, while margins are expected to step down. We believe these assumptions to be reasonable, particularly as a hot market with record low rates allowed for potentially unsustainable margins in FY21-FY23.

Capital IQ

As we have touched on, NVR’s low-risk approach has allowed for a fairly safe balance sheet. Management has allocated capital exceptionally, however. Shares have declined by ~22% due to buybacks, while maintaining a net cash position. These buybacks have underpinned NVR’s impressive share price trajectory, with scope to maintain this going forward (~56% of FCF utilized in FY23 and ~70% in FY22).

Capital IQ

Seeking Alpha

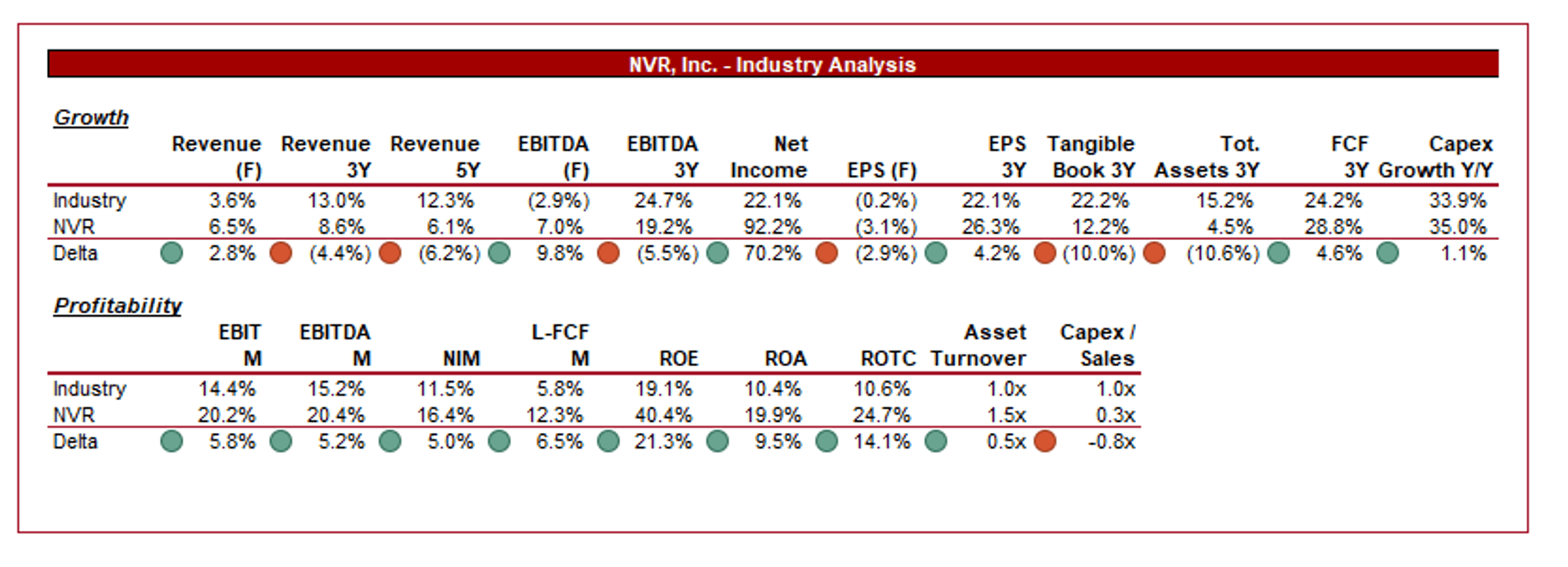

Presented above is a comparison of NVR's growth and profitability to the average of its industry, as defined by Seeking Alpha (24 companies).

NVR’s strategy and scale have allowed it to materially outperform its peers, with superior margins and slightly worse growth. Importantly, the company’s ROTC is considerably higher, while its FCF margin has sufficient buffer.

Whilst NVR may not be able to grow as quickly as its more aggressive peers, the company’s ability to maximize returns, particularly on a risk-adjusted basis, makes its offering compelling. We see good justification to suggest a valuation premium is warranted.

Capital IQ

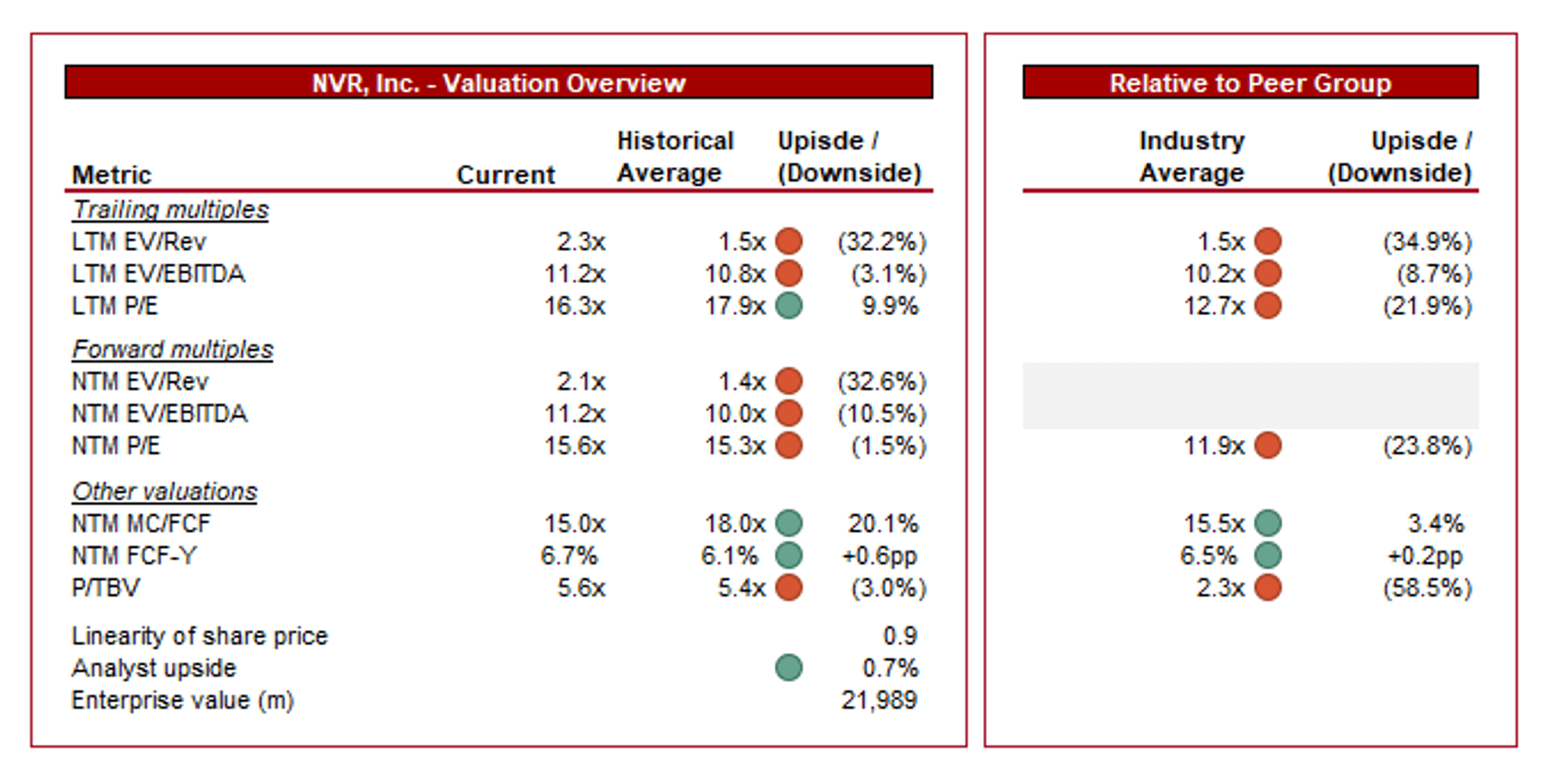

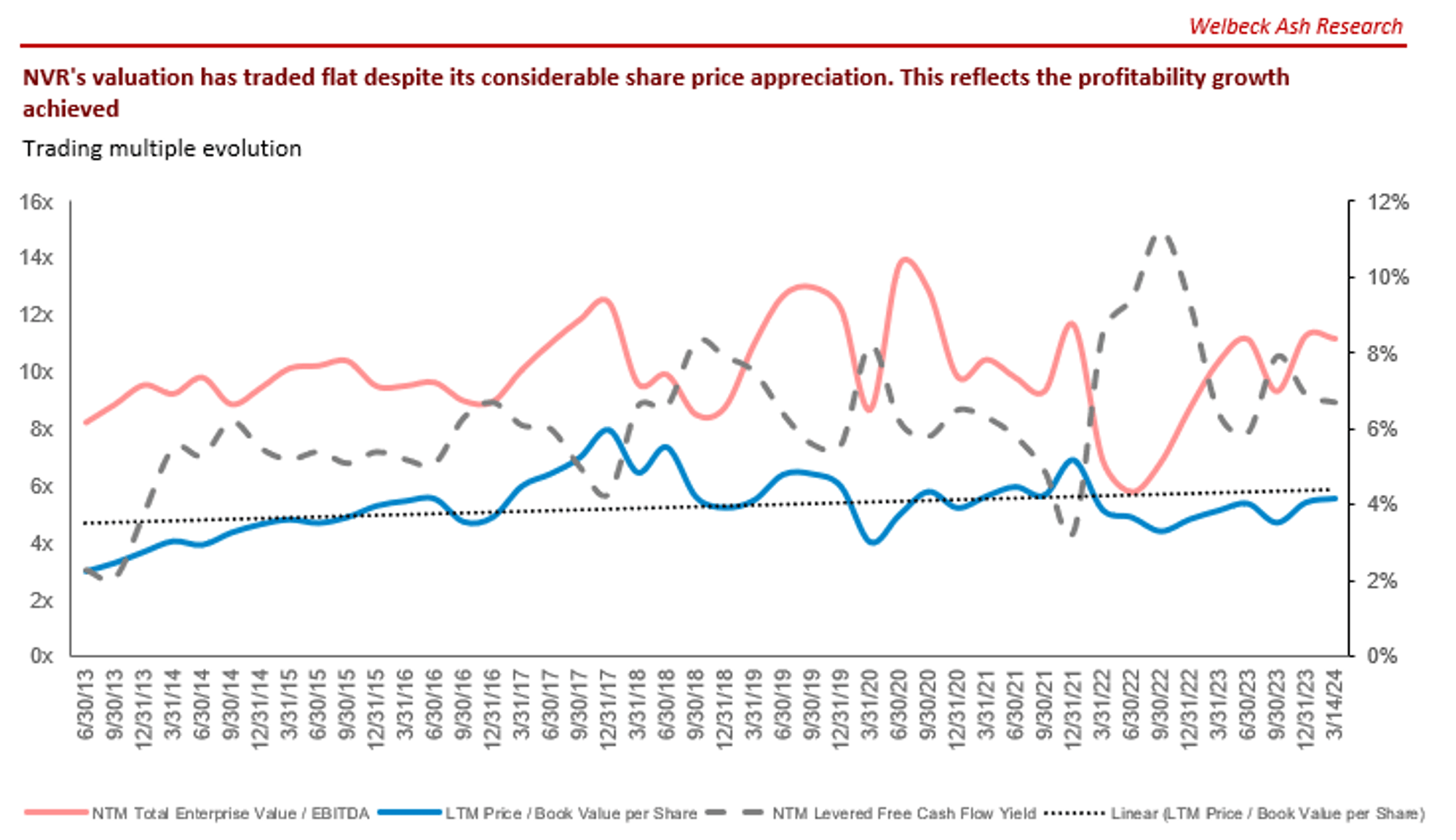

NVR is currently trading at 11x LTM EBITDA and 11x NTM EBITDA. This is a premium to its historical average.

A premium to its historical average is justifiable in our view, owing to the company’s financial development and likely ability to normalize at higher margins. Whilst better growth was likely priced in, potentially offsetting our argument, we believe tailwinds could mean NVR pushes toward its decade-average of ~9%.

Further, NVR is trading at a premium to its peers, with a ~9% EBITDA delta and ~24% P/E delta. We believe this underappreciates NVR’s earning potential, which is an advantage that is unlikely to subside. A degree of this is likely due to the expectation for margin deterioration, however, we still believe ~24% leaves some upside.

Finally, NVR is trading at a FCF yield discount to its historical average, a highly important indicator we feel given how FCF has been utilized thus far.

Capital IQ

Overall, we believe NVR is likely slightly undervalued, if not trading within range of its fair value. This said, we believe its earning potential remains attractive and has shown a FCF yield of ~6% can deliver market-leading returns.

Capital IQ

The risks to our current thesis are:

Overall, we believe NVR is a fantastic business, underpinned by its considerable scale and expertise, as well as its portfolio of land. What differentiates NVR from the other leading options globally is its approach, which is best observed in its market-leading efficiency metrics. NVR is incredibly well-run and provides investors with exposure to a growth segment in an attractive risk-adjusted manner.

Whilst we do not see considerable upside, and concede there could be financial drag from economic conditions in most of FY24, we believe the stock is a winner long-term and so rate it a buy.