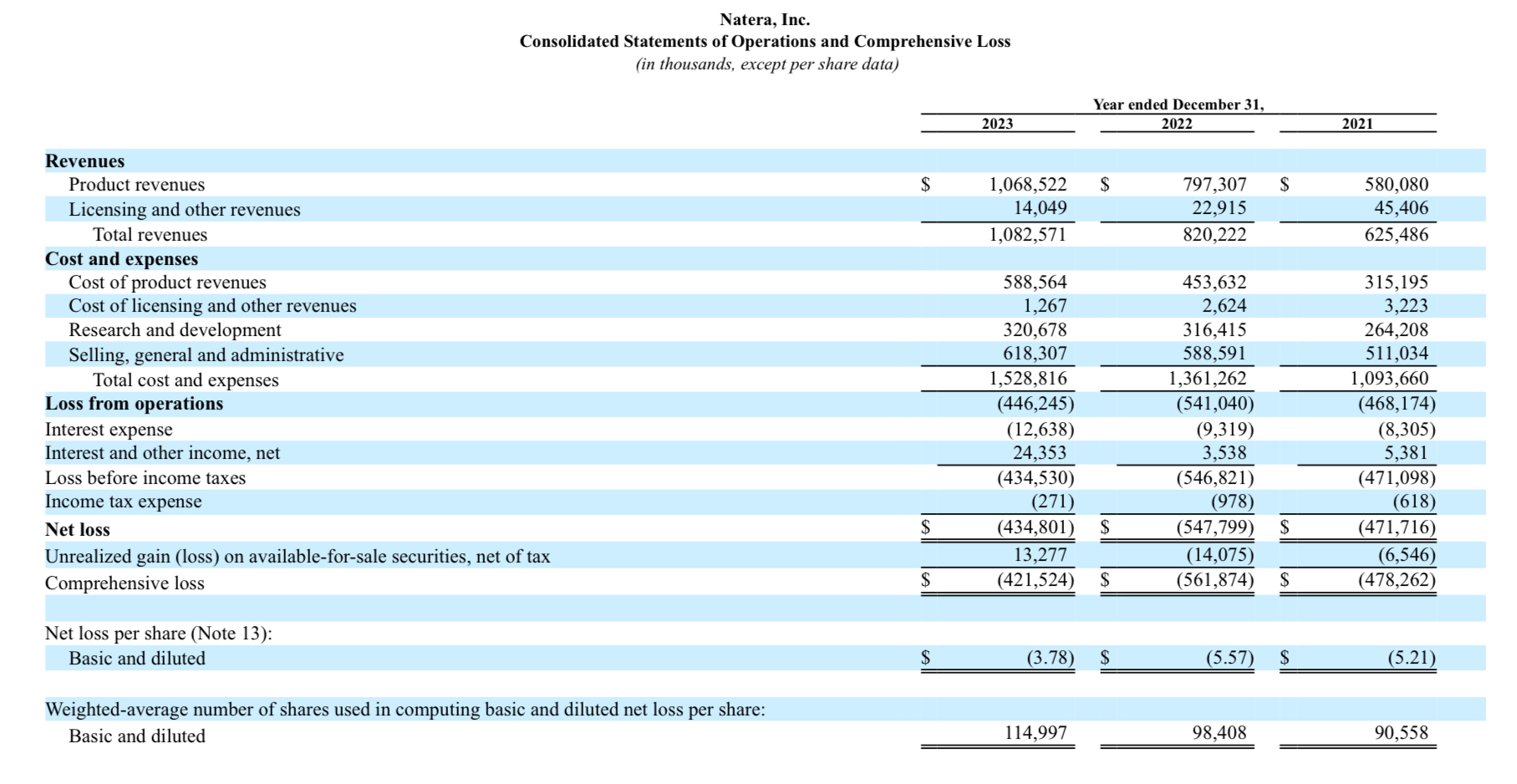

Natera, Inc. consolidated statements of operations and comprehensive loss (Natera, Inc.’s Q42023 report)

Since inception, Natera (NASDAQ:NTRA) has incurred sustained losses, with their cash burn rate being one of the largest concerns to investors. However, the company seems to be on the verge of becoming profitable for the first time in its history. In my opinion, this is mostly due to the growth of the personalised medicines, particularly in oncology, together with the recently approved biomarkers law in 13 U.S. states. Thus, I consider that Natera as a “buy,” despite the risks associated with it.

In 2023, the global market size of personalised precision medicines has been estimated at $578 billion, with the projections estimating it to grow with a CAGR of 8.10% for the next ten years, reaching up to $1,233.23 billion by 2033. Particularly, in North America, the personalised medicines market increased over 45% just in 2023, being oncology the application with the largest growth.

Natera Inc. is a diagnostic company who utilises molecular biology and bioinformatics to detect altered biological markers, associated with pathological conditions in samples as small as single cells. Nowadays, the company focuses on three main areas: women’s health, oncology and organ health. Their three major revenue drivers are: Panorama, a non-invasive prenatal test (NIPT), aiming to identify foetal genetic anomalies utilising blood-samples from the pregnant person. Horizon, a carrier screening test, aiming to identify if a person carries an altered gene that may impact their child. And Signatera, which is a personalised highly-sensitive molecular residual disease (MRD) test, that enables the early detection of cancer relapses by identifying circulating tumour DNA in peripheral blood samples.

Natera has been incurring in sustained net losses, however in their most recent earnings call, the management ratified the company’s commitment to achieve “cash flow break even by Q3 2024 or sooner.” Within their Q42023 report, they reported revenues of $311 million just in that quarter (accounting for a 43% year-on-year increase), with a product revenue increase of 44.3%, and total 2023 revenue of $1.08 billion. Moreover, Natera’s cash burn, in 2023, was reduced by $193 million when compared against 2022. Thus, addressing one of the major financial concerns most investors have when assessing the company’s performance.

Since Signatera’s launch in 2017, the company has been growing its footprint in the field of MRD tests, becoming one of the field’s leaders. Fast-forward to 2024, and now Signatera is one of the largest revenue drivers of the company. The MRD tests are recurrent diagnostic assays performed prior, during and post treatment. Hence, having a larger potential to generate continuous revenue than the NIPTs which are usually a one time only diagnostic tool. Indeed, according to Natera’s Q42023 report:

The total addressable market in the United States for recurrence and treatment monitoring for solid tumour cancers is over $15 billion.

In addition, 13 states, including Texas, New York and California, have approved new laws enforcing all healthcare plans to cover biomarker testing for diagnostics and recurrent disease monitoring, thus facilitating the access to precision-personalised medicine to more patients. Taking together the market size of personalised medicines, the boom of molecular diagnostics in healthcare and particularly in oncology, it is quite easy to agree with the management’s decision on adding these types of tests to their repertoire despite the significant cost associated with their development and validation.

According to Seeking Alpha, Natera’s market cap as per today is USD 11.02 billion, with a share price standing at $91.26. During the last 5 years, the company’s share price has seen an increase of 363.72%, meanwhile the revenue has only grown 32.61% in the same period of time. Those investors, following Natera’s performance over years would be aware that despite the continuous revenue increase, their total expenses have also been increasing rapidly, as consequence of their investment on R&D (which includes buying equipment, cost of reagents and cost of long clinical trials), as well as the increase of the interest rate on their loans. Hence, Natera Inc. has, so far, been operating with negative numbers since inception. In this sense, in their 2024 guidance, the management has announced a further reduction of the cash burn, to be in the $50-$75 million range, and to achieve breakeven by Q32024 or sooner.

I personally welcome the management’s commitment to reduce the operating expenses, while increasing profit margins and revenue, however I am slightly sceptical about their enthusiasm regarding the cash flow, as in my opinion, achieving cash flow breakeven, for the first time in the company’s history, has more to do with external catalysts than Natera’s management doing. The catalyst factors are, among others, the positive personalised medicines momentum, the coverage of certain biomarker’s tests (such as Signatera) by insurance companies (such as Medicare), and the potential boost of new patients thanks to the new biomarker’s legislation. Nevertheless, it is also true that the company wouldn’t be able to capitalise on those catalyst factors if their products were not gaining adoption between healthcare professionals and their patients. In this sense, Natera’s overall test run increased by 430 000 more tests in 2023 when compared against 2022. In particular, Signatera, observed a year-on-year increase of 34 000 more tests in 2023, for a total of 98,000 tests. The company has attributed this last increase to Signatera’s adoption by 40% of the U.S. oncologists.

Digging deeper into Natera’s Q42023 report, there are strong signs of growth that may result in better returns on investment and overall financial performance in the future. In particular, in their table of consolidated statements of operations and compressive loss (see below), the company reported an overall loss of USD 421 million, with a negative EPS of $3.78 for 2023. In comparison, in 2022 the overall loss was $561 million, with a negative EPS of USD 5.57. Thus, accounting for an EPS increase of USD 1.79 and a loss reduction of USD 140 millions year-on-year. On the other hand, as per their last report, Natera holds USD 879 million in cash and cash equivalents, and their long term assets have continued the upward trend shown in the last 10 years, to now account for USD 1.44 billion.

Natera, Inc. consolidated statements of operations and comprehensive loss (Natera, Inc.’s Q42023 report)

So, considering all these positive trends, where is the dirt? Why is Natera still showing negative earnings if their revenue, profit margins, and sales are increasing? Well, the answer to that can be found within their operating expenses figures, in 2023 they reported total operating expenses of USD 939 million, which is 3.76% more than the figure reported in 2022. Despite the management’s guidance to become cash flow breakeven this year, analysing their numbers it is clear that their operating expenses have continued to rise since 2020. Nonetheless, it is also true that the rate of increase has slowed down, as the year-on-year change in 2022 was 16.74%, 92.02% in 2021 and 57.81% in 2020. Another interesting piece of data is the TTM EV/sales which stands at 9.58, 142.95% higher than the sector median. Taking all together, I consider that Natera Inc., is on a good track, their share price seems to have reacted positively to the latest financial results report, but they still need to demonstrate their capacity to turn negative figures such as EPS from negative to positive.

In general, when analysing the company’s performance during the last 5 years, it looks like they have the potential to deliver good results in the medium term. However, as I have mentioned earlier in this article, they haven’t been able to drive net profits yet.

Currently, the ratings for Natera Inc. are a bit mixed. For instance, 15 out of 17 Wall Street analysts rate the company as a “buy” to “strong buy”, with only one analyst recommending a “sell”. Wall Street analyst’s average target share price for the next twelve months is $94.82, a 3.90% higher than the current share price. On the other hand, Seeking Alpha’s Quant rating is currently valuing the company as a “strong buy”. The consensus for Natera Inc. is that their forward EPS will reach -2.33, accounting for $1.45 increase from the current figures.

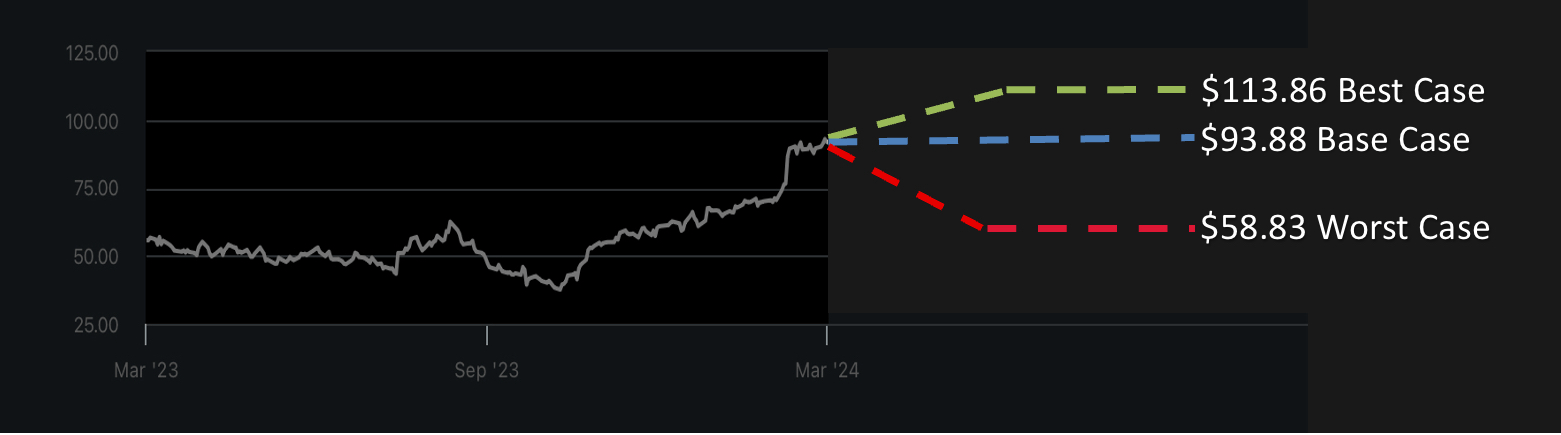

Given that Natera is not making profits yet, all valuations have a speculative factor. Thus, instead of utilising the figures for EPS, I have based my calculations on their TTM P/S figures (9.58), and a 25% discount rate in order to perform similar calculations to those I used when analysing Takeda Pharmaceuticals and Voyager Therapeutics.

For the worst case scenario, I estimated a 5-years growth of 6% (Natera’s year-on-year sales profits margin growth), and 10-years growth of 8% given the expected 10-years market size growth of personalised medicines. Thus, the worst case scenario target share price is $58.83, or 35.53% overvalued.

Similarly, for the best case scenario, I considered a 8% 5-years growth, a 32% 10-years growth based on Natera’s 5-years revenue growth. Hence, the best case scenario target price is $113.86, or 24.76% undervalued.

For the base case scenario, I have used the same 8% expected 5-years growth and 16% 10-years growth based on the Natera’s 5-years revenue growth toned down by their expectations of increasing their sales & administrative expenses by approximately 300%. Then, my base case scenario target price is $93.88, or 2.87% undervalued.

Intrinsic Value projections for Natera Inc. (Seeking Alpha’s graph modified by the Author)

Finally, my fair value price for Natera Inc. is $92.86, meaning that the stock is currently 1.75% undervalued.

Investors considering including Natera Inc. into their portfolios should be aware of the company’s continued failure to transform revenue increases into net profit. As mentioned multiple times in this article, although the company has been delivering good results in terms of revenue, their net profit is, to date, still negative. In this regard, if/when Natera becomes cash flow breakeven in 2024 for the first time, it will be very well received by investors.

In my view, the company has done very well expanding their products into the MRD and organs health areas, given their recurrent needs for testing and their expected growth globally. However, this has been associated with continued increases in R&D and total operating expenses that have been growing faster than revenue. Thus, investors are still waiting for the company to capitalise on its leadership in the molecular diagnostics area. In this regard, the new biomarkers law approved in 13 states, might be the catalyst that helps Natera boost their revenue to overtake operating expenses’ growth.

Finally, one of the most alarming risks associated with this company comes from a statement reported in their Q42023 results:

Based on our current business plan, we believe that our existing cash and marketable securities will be sufficient to meet our anticipated cash requirements for at least 12 months after February 28, 2024.

I personally have no doubt about Natera’s capacity to raise funds to secure the continuity of its business beyond 12 months; however, investors have to be aware of a potential share dilution, which will potentially have a negative impact on their investment returns.

Natera Inc. is a biotechnology company focused on the development of diagnostic tests powered by molecular biology and bioinformatics. Since inception, they have incurred continued losses, mostly attributed to the increase on R&D and operating expenses. The strongest revenue drivers within their product line are non-invasive prenatal tests (NIPTs), but more recently products such as Signatera, a personalised test for early detection of tumour relapse, are seeing a spectacular growth. In this sense, the company had reported not only a growth in Signatera’s adoption between U.S. oncologists but also a growth in their profit margins mostly driven by their sales strategy and the coverage of the test by health insurance plans such as those offered by Medicare. In addition, the new biomarkers’ law, might help Natera to capitalise further on their molecular diagnostics leadership position.

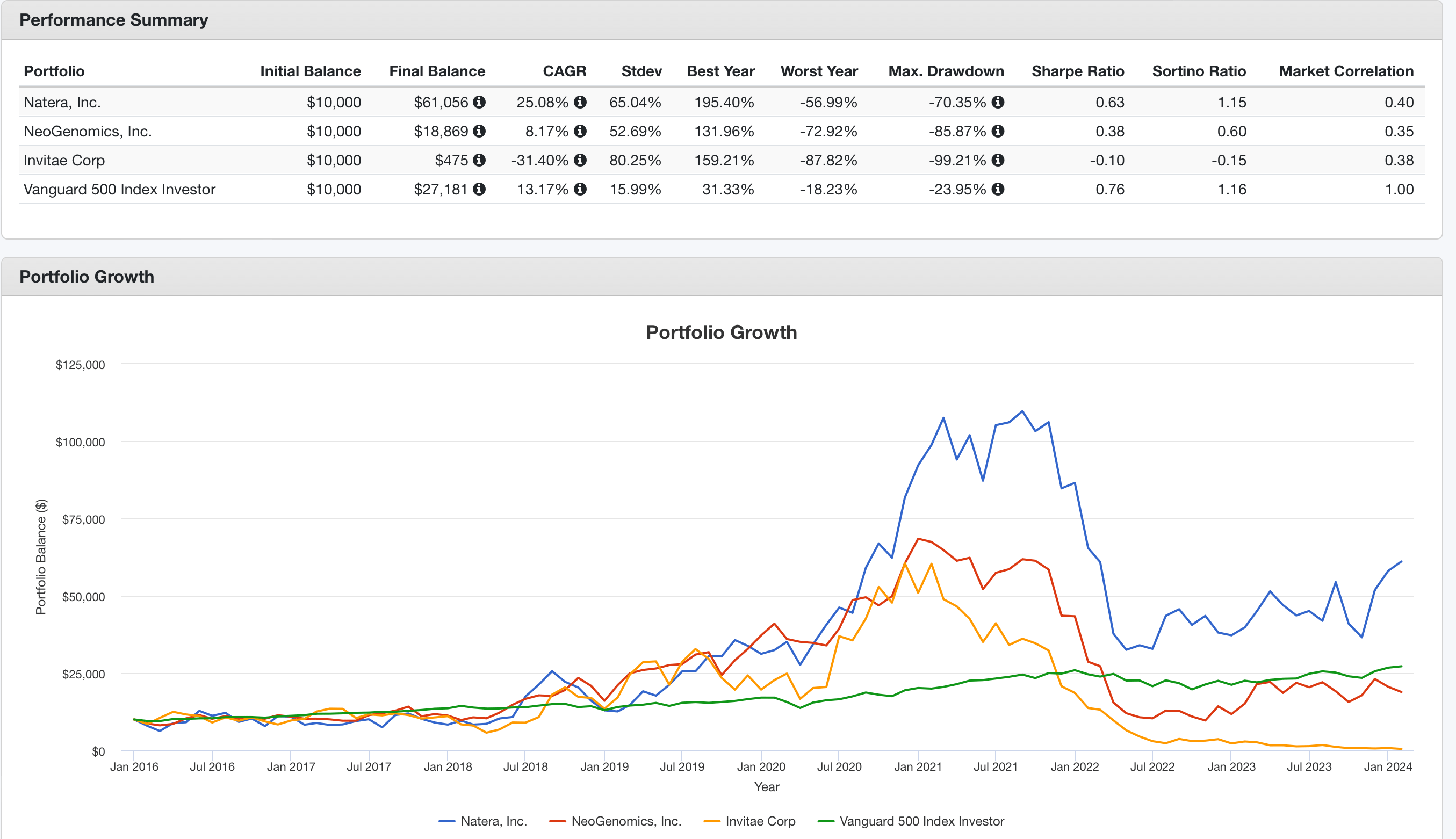

Although, past performance does not guarantee future results, the results of a hypothetical investment of $10,000 on Natera Inc., versus doing it on Neo Genomics (NEO) or Invitae (NVTA) are pretty favourable to Natera, as you can see in the chart below (plotted using portfolio visualizer back test tool).

Natera, Inc.’s hypothetical results on investment 2016-2024 (Portfolio Visualizer)

In summary, investing $10,000 on Natera Inc. in January 2016 resulted in a 25.08% CAGR growth (USD 61 056 final balance), outperforming the SP500, and Natera’s competitors in the MRD area (Neo Genomics) and NIPT area (Invitae), which have resulted in CAGRs of 13.17%, 8.17% and -31.40% respectively.

To conclude, I rate Natera Inc. as a buy, taking into account my overall valuation (1.75 % undervalued), the market growth of personalised medicines, the peers comparison, and the expected positive returns on investment if/when the company manages to have a positive net profit. However, in my opinion, should you consider buying this stock, you may want to start a small position, while averaging down if/when the share price decreases, as in my opinion the company is likely to continue raising funds by issuing new shares, i.e. diluting the current shareholders’ position.

ArtemisDiana