NetScout Systems, Inc. Beat Revenue Forecasts By 10%: Here's What Analysts Are Forecasting Next

Investors in NetScout Systems, Inc. (NASDAQ:NTCT) had a good week, as its shares rose 3.5% to close at US$22.48 following the release of its third-quarter results. NetScout Systems beat revenue forecasts by a solid 10% to hit US$218m. Statutory earnings per share came in at US$0.82, in line with expectations. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

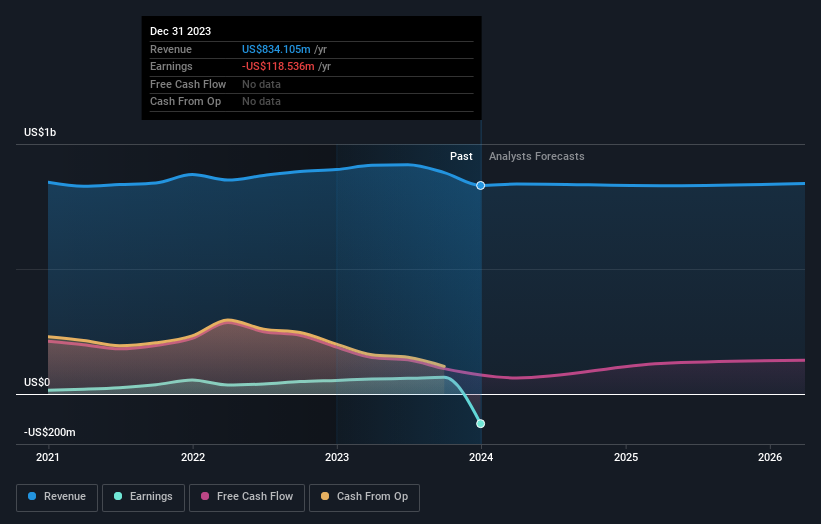

Check out our latest analysis for NetScout Systems

Taking into account the latest results, NetScout Systems' three analysts currently expect revenues in 2025 to be US$833.0m, approximately in line with the last 12 months. Earnings are expected to improve, with NetScout Systems forecast to report a statutory profit of US$0.90 per share. Before this earnings report, the analysts had been forecasting revenues of US$838.2m and earnings per share (EPS) of US$0.96 in 2025. So it looks like there's been a small decline in overall sentiment after the recent results - there's been no major change to revenue estimates, but the analysts did make a small dip in their earnings per share forecasts.

It might be a surprise to learn that the consensus price target was broadly unchanged at US$23.92, with the analysts clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values NetScout Systems at US$25.00 per share, while the most bearish prices it at US$22.75. This is a very narrow spread of estimates, implying either that NetScout Systems is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. One thing that stands out from these estimates is that shrinking revenues are expected to moderate over the period ending 2025 compared to the historical decline of 0.4% per annum over the past five years. Compare this against analyst estimates for companies in the broader industry, which suggest that revenues (in aggregate) are expected to grow 3.8% annually. So it's pretty clear that, while it does have declining revenues, the analysts also expect NetScout Systems to suffer worse than the wider industry.