aimy27feb/iStock via Getty Images

aimy27feb/iStock via Getty Images

Natura (NYSE:NTCO) is a Brazilian beauty company with a global reach and relevant size in the industry. It operates in a market that generated $430 Billion in revenues in 2022 and is expected to grow at a 6% compounded rate throughout 2027, to $580 Billion.

The firm, on the other hand, has abandoned some of its luxury franchises in favor of the integration of Avon, a mass-market beauty company. This integration failed to produce results, up to now, that justify the cost leadership needed to compete in such a market.

Besides the above-mentioned growth engine, some parts of the beauty segment may also be characterized by demand resiliency and pricing power. There are mainly two reasons for this effect. The first is that part of the utility related to some luxury goods is related to its status symbol, something described in economics as Veblen goods. The second is that this sector is constituted by powerful brands in terms of identity with customers, implying potential loyalty to its products.

On top of that, current societal trends related to social platforms proliferation and a hedonistic lifestyle also play an important role in creating even more momentum for such economic activities and products. When all these effects are combined, gross margins may be expected to range from 50% to 70% in skin care and up to 90% in fragrances.

The combination of growth, profitability, and customer loyalty makes the case for having part of equity portfolios allocated to this industry. Geographical distribution and the potential of new entrants may contribute to a diversified approach within the sector, that can contemplate both established incumbents and smaller niche companies.

The company has typically operated with a direct sales model and an idea of locally produced goods that achieved commercial success, competing directly with Avon and supermarket brands in the mass segment. As the beauty sector changed, the company started an efficacious premiumization of its brand, which had new attributes developed mostly related to the use of natural ingredients from Amazonia, cruelty-free, linked with community support in places where raw materials were extracted, and sustainability. This brand shift was adherent to new customer values, especially focused on Gen-Zs and Millennials. In fact, a 2015 report depicts leading scores for brand attributes such as Reconnection with Nature, Strengthening Social Ties, Exalts Brazil's Elegance and Creative Fusion, Innovation, and Refinement.

In terms of the commercial model, the company expanded its reach to flagship stores in some important commercial areas of Brazil besides Buenos Aires, Santiago, and New York and incorporated an e-commerce platform to capture the rising demand since in this channel, expected to grow 12% per year, therefore faster than the whole market.

With this movement, the company succeeded in repositioning itself on the top masstige / low prestige segment. With such, yearly revenues increased an accumulated 61.2% between 2011 and 2019 (only Natura brand). In addition, the acquisition of Aesop and later The Body Shop allowed the company a relevant additional revenue stream, a reinforcement of brand positioning on luxury-driven segments, and a more international reach (especially in China and the U.S., the largest markets in the world) that could imply a platform for international expansion of Natura brand as well. In addition, while Natura's gross margin in 2019 was 67.4%, The Body Shop registered 76.5% and Aesop 90.6%.

The Natura brand is still a value engine for the firm. On the other hand, the company seemed to have lost its focus on value since 2020. The company acquired Avon in 2019 for a $ 2 Billion valuation, a 28% premium over the closing share price before the transaction. At that point, management claims pointed to the $ 200 - 300 Million potential synergies, resulting in economies of scale (it would become the 4th largest beauty firm on the planet) and overlapping, as the main decision driver.

The company is, nevertheless, still struggling with the integration of Avon. An initiative called Wave 2 was recently implemented in the smaller markets of Peru and Colombia and should be started in Brazil. The portfolio of Home and Style, included as a potential growth driver in the acquisition moment, is to be discontinued. The focus right now seems to be on logistic cost reduction and the integration of the sales force (consultants in the direct sales model). Margins for Avon consultants are lower than Natura's, including the fact that is negative for entry levels (1 and 2 stars).

Additionally, the company announced the sale of Aesop in 2023 for $2.5 Billion, and more recently of The Body Shop for $254 Million. This movement resulted in some strategic implications for Natura. Initially, the company descends in the quality spectrum to focus on mass and masstige segments, where it will face fiercer price competition. In such a way, operating efficiency is the name of the game. As stated, the company is struggling to find the synergies and efficiency from this merger. Without fast improvement in results, the company keeps important financial constraints. As per Seeking Alpha Quant grading, the company scores a C- rating on growth, with still a risk of dropping revenues as some consultants are eliminated from the network, and a D+ rating on profitability, including an F on Cash From Operations.

The second important point is that Natura has become a company more concentrated in Brazil and Latam, moving away from large-density markets such as China. In case there is doubt about the potential of Natura in international markets, the competition offers some examples. L'Occitane group, for example, launched Sol de Janeiro in 2015, inspired by Brazilian products and "spirit", resulting in a bestseller for the group. Actually, Sol de Janeiro is the second brand in the group with Brazilian inspiration, after L'Occitane au Bresil.

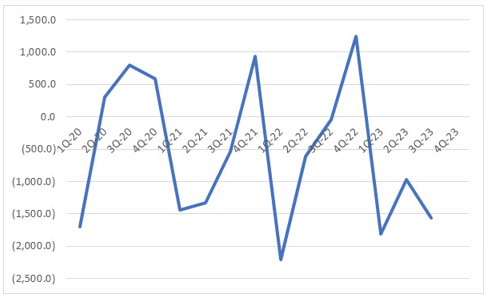

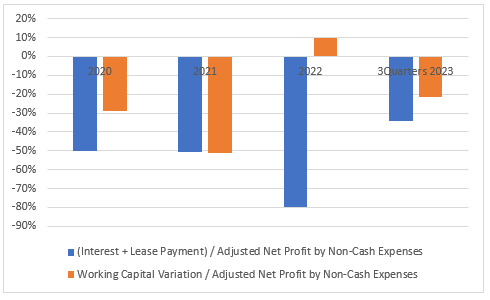

Since Avon's acquisition, the firm has recorded recurrent negative free cash flow, despite some exceptions, as depicted in Figure 1. In general, financial leverage imposes an important cash disbursement in the form of interests. Also, the synergies cannot be observed in Working Capital, another line of net investment since 2020. Figure 2 depicts the weight of interests and leasing expenses and working capital variation on the already adjusted Net profit due to non-cash expenses, as in the case of depreciation.

Figure 1: Free Cash Flow (Company Data) Figure 2: Selected Ratios of Cash Disbursement (Company Data)

Looking specifically at the last report, the firm continued the trend of cash destruction, even considering the inflow from the sale of Aesop. Revenues reduced organically 10.5% YoY in the quarter, and Aesop represented an additional topline loss of more than BR$ 600 Million. The company is expected to report Q4 in March/12/2024.

The evaluation of Figures 1 and 2 leads to the conclusion that the company has destined between 55% (3 quarters of 2023) and 102% (2021) of its adjusted profit to interests, leases, and working capital increases. In this situation, the operations concluded for Aesop and The Body Shop can be viewed more as financial imperative than proper strategy drive, resulting in the elimination of potentially some of the best assets the company used to have.

Personal care and beauty is a growing and high-margin industry that should be considered in equity portfolios. It benefits from societal trends and presents the potential to outperform the general economy in the coming years.

Natura is an established player in this market but seems to be out of pace in the strategic direction. On one side, it abandoned profitable, high-growth franchises with strong brand awareness, loyalty, and desirability, moving to a more price-driven segment. On the other, it struggles to find efficiencies that could result in an advantage in such a competitive segment. As a result, Natura doesn't seem to be the best allocation for this portion of equity portfolios.

A last point that investors may need to know is related to two material facts issued in 2024. In the first, the company announces plans to delist from NYSE and in the second it announces plans to separate Natura and Avon in two independent traded companies. These additional uncertainties corroborate a careful stance on the asset.