Jeremy Poland/E+ via Getty Images

Jeremy Poland/E+ via Getty Images

I continue my focus on renewable energy producers by analyzing Sunnova Energy International (NYSE:NOVA), an American company that installs and operates photovoltaic systems. Innergex (TSX:INE:CA) (OTCPK:INGXF) and Enlight Renewable Energy (NASDAQ:ENLT) have government agencies, and corporations as their main customers and operate utility-scale plants. Sunnova, on the other hand, offers its products to the retail segment through a wide range of options meeting the customer's needs. I believe this is a very attractive business, able to provide high marginality.

NOVA continued to increase its debt, and the poor results recorded in FY 2023 highlighted the difficulties the company is facing. Management appears satisfied with the performance in the Q4 results conference call and anticipated an increase in internal cash flow generation through cost rationalization in the coming years. This is intended to be achieved through decreasing Capex, expected to be stable at c.a. $5B, an increasing use of tax equity financing, and asset sales. In my opinion, the current financial situation makes the plan hard to implement, and also the market seems not to have appreciated the Q4 results, with the stock price losing more than 42% in the week after publication. I overall rate NOVA as a Sell, waiting for improvement in financials and the implementation of the plan presented by management.

Sunnova provides photovoltaic systems, serving more than 400,000 customers in the United States, with a total installed capacity of 2292 MW. It operates through a network of dealers and partners carrying out installations of solar panels, battery storage and other electrification-related products.

NOVA usually advances all (or part) of the system construction costs, retaining ownership of the system and power generation. Against the initial investment funded, it then obtains cash flows from its customers based on Leasing or PPA contracts. Moreover, Sunnova offers the option of acquiring ownership of the installed system through loans having a term of 10, 15, or 25 years. In this case, it receives a periodic stream of interest and principal amount. NOVA also serves a range of maintenance and energy efficiency services, also addressed to third-party customers not involved in leasing, PPA, or loan plans.

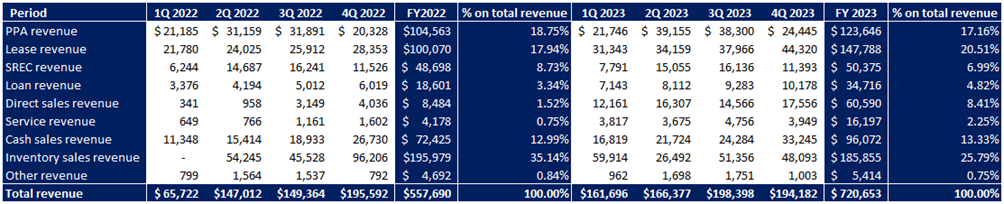

As of December 2023, 37% of NOVA's customers have loan agreements, 24% lease agreements, 24% PPA agreements, and 12% service plan agreements. The segments contributing the most to FY2023 total revenues are leasing (20.5% of total revenues), PPA (17.2%), Inventory Sales (25.8%) consisting of direct sales to dealers or other parties, and Cash Sales Revenue (13.3%), attributable to direct sales to customers of PV systems.

NOVA SEC Filings and Author's Analysis

Given the large amount of capital required by this business structure, Sunnova finances itself mainly through debt, securitization, and, in recent years, through tax equity financing. The latter has become prominent as the Inflation Reduction Act introduced a 30% ITC (investment tax credit) on solar panel and battery installation costs. NOVA also has $3.7B in customer notes receivable, an asset that can potentially provide liquidity through the sale of receivables to third parties.

NOVA SEC Filings, Refinitiv Eikon, and Author's Analysis

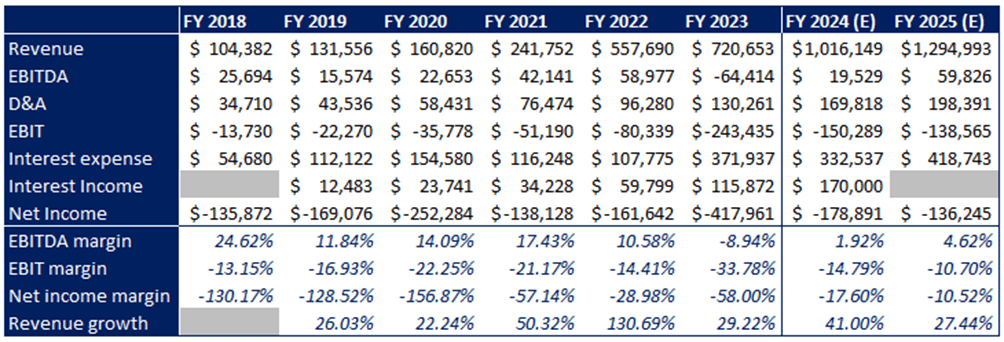

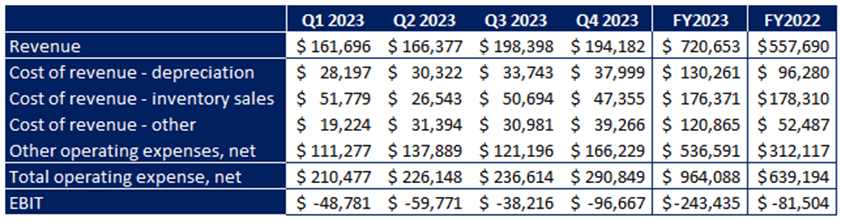

FY2023 was particularly bad for Sunnova, as a result of both the slowdown in the PV market due to rising interest rates and the higher module and installation costs. The situation is gradually improving, but revenues and marginality experienced both a downturn. Q4 2023 was particularly affected by an increase in operating expenses, being $290m, up 22.9% from Q3 2023. Full-year OpEx rose to $964m vs. $639m in FY2022, up 50.8% YoY. The main drivers of this increase are personnel costs, +$74m vs. FY2022, +$60m in operation & maintenance costs and +$68m other various items.

Revenues in FY2023 grew by 29.22%, below analysts' estimates and NOVA's historical performance, but at a higher rate than its competitors. The higher cost increase as a % of revenues had a destructive effect on margins, with a FY2023 EBIT margin of -33.8% vs. -14.4% in FY 2022.

According to management's recent statements, the goal is to lower operating costs by about 20% between 2024 and 2025, through an increased use of automation and through upgrading IT platforms. In my opinion, these statements are rather vague and achieving such a significant improvement in such a short time is hard to believe. My view is that operating margins will remain negative in FY2024, with an EBIT of around -$150m.

NOVA SEC Filings and Author's Analysis

In addition, FY2023 interest expense reached $372m, up 245% from FY2022. The increase is partly due to unrealized losses on hedging derivatives worth $87m and to a 38% increase in total debt, now equal to $7.7B. NOVA also collected $115m in interest income from loans, up 93% from FY2022.

Cash flow analysis also leads to poor outcomes, with an operating cash outflow of $279m and Capex of $1.8B in FY2023, for a total negative FCF of about $2B. The result is, of course, affected by the Sunnova business model, requiring large initial investments, from which it obtains PPA and Leasing contracts cash inflows over a period of up to 25 years. Nevertheless, yearly operating cash outflows of about one-fifth of revenues are, in my view, a major concern for a company's financial stability.

The large amount of capital needed to finance the business led to a significant increase in debt, going from $959m as of Dec. 2018 to $7.7B as of Dec. 2023. Against it, Sunnova holds $5.7B in PP&E, $3.7B in debt-related assets, and c.a. $300m in cash, meaning coverage of 125% of total debt.

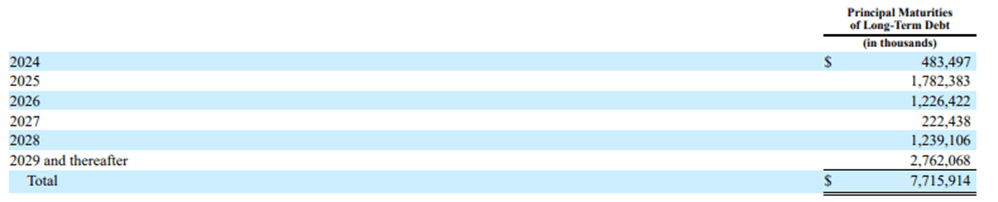

$2.2B of debt will mature between 2024 and 2025, including a convertible bond that could lead to strong dilutive effects for current shareholders. A considerable amount of capital will therefore be required, with a debt refinancing virtually obligated, as admitted by management itself in the last conference call.

NOVA FY2023 Annual Report NOVA Fourth Quarter and Full Year 2023 Earnings

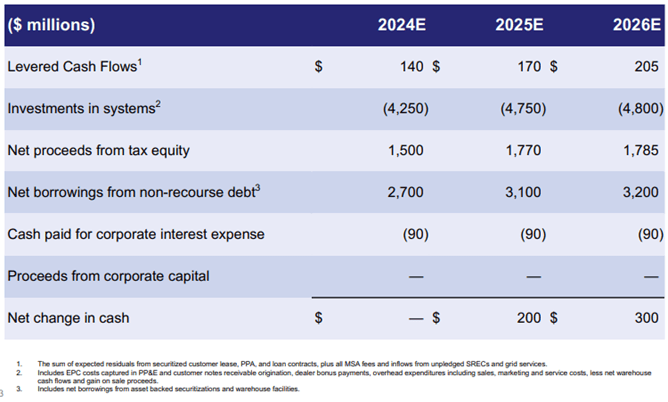

The forecasts provided by management highlighted how the need for capital will further exacerbate during 2025 and 2026, with an additional demand of about $9B. Management, however, estimates a potential to raise about $5B through tax equity financing, an important source of capital in the coming years. They also anticipated a reduction in CAPEX compared with current rates, which is expected to stand at about $5B in the medium term.

Management wants to focus on internal cash generation in the next few years, including through cost rationalization and asset disposal. As specified in the conference call, these sales will largely involve loans rather than securitized products, as the latter have been an excellent source of low-cost financing, currently difficult to match. I believe that, without significant improvement in operating results and the liquidation of some assets, NOVA will experience a growth in interest expenses even if benchmark interest rates decrease.

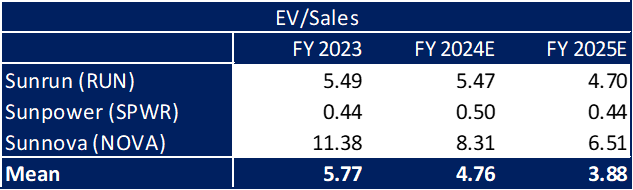

Sunnova's extremely negative financial results and cash flows make it difficult to analyze EV/EBITDA, EV/EBIT, and implement a DCF. I therefore used the EV/SALES ratio (using data provided by seekingalpha.com) to compare NOVA's price relative to its two largest peers: Sunrun (NASDAQ:RUN) and SunPower (NASDAQ:SPWR). Sunnova FY2023 EV/sales are 11.38x, significantly higher compared with both its peers, 5.49x and 0.44x respectively. This result is affected by the large amount of debt that is added to the market cap in the EV calculation. Over the next 2 years, NOVA's higher expected revenue growth should narrow the gap between its valuation and that of its competitors.

seekingalpha.com and Author's Analysis

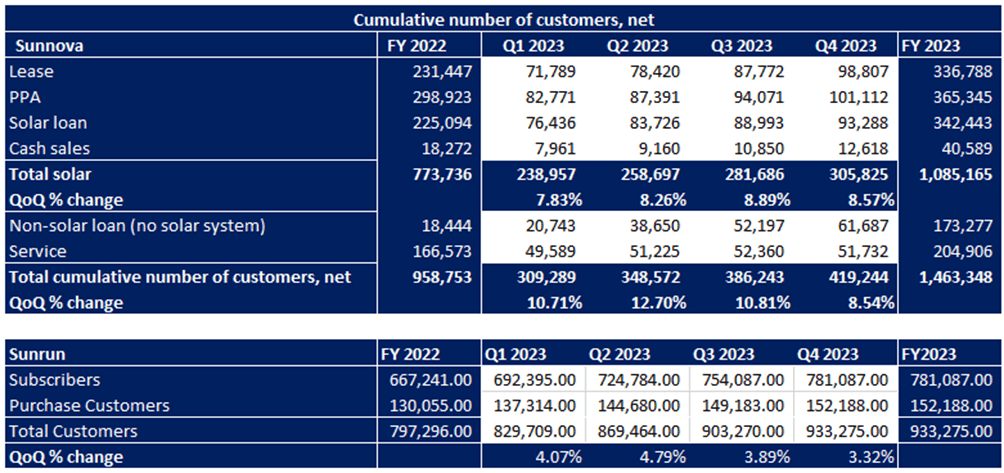

The difference in growth between Sunnova and Sunrun seems consistent with the number of new customers in FY 2023: Sunnova grew at more than twice the rate of Sunrun, which is currently a significantly larger company.

Companies SEC Filings and Author's Analysis

In my opinion, NOVA stock is characterized by too high financial risk. The asymmetry between the timing of cash outflows and inflows may continue to bring pressure on financial performance, hindering the achievement of a profitable condition and requiring continuous capital injection. The competition from companies such as SunPower and Sunrun is an additional uncertainty in play; in my opinion, it is currently difficult to identify which type of business will be able to better meet the needs of U.S. customers.

Although the stock has declined sharply, currently at c.a. $7.2 a share (down from $50 a share in early 2021), I do not believe that this constitutes a valid reason to justify an investment in the company. In the near future, lower interest rates could positively drive marginality, but the benefits of this will only be maximized if good cash management takes place in 2024 and 2025. I overall rate NOVA as a Sell, awaiting further information showing an improvement in financials in line with the plan presented by management; for the time being, this improvement has not been so evident.