Suphanat Khumsap

Suphanat Khumsap

Navios Maritime Partners L.P. (NYSE:NMM), headquartered in Monaco, owns and operates a vessel fleet for global maritime transportation. NMM has 176 diverse ships with an average age that is less than the standard for the industry, with reasonable charter rates. Geopolitical events, such as the Houthi attacks in the Red Sea, the Panama Canal drought, and Ukraine's war, have modified the trade routes, producing longer trips and higher revenues for NMM and other shipping companies. The result was a Q1 2024 financially stronger than expected, influencing the company's strategies, like fleet renewals, debt reduction, and securing long-term contracts to ensure stability. In my valuation analysis, I concluded that NMM seems excessively undervalued despite its risks, so I gave it a “Buy” rating.

Navios Partners owns and operates dry cargo and tanker vessels for seaborne transportation of iron ore, coal, grain, fertilizer, and containers worldwide. The company has a varied mix of bulk carriers and container ships, giving it some operational flexibility. As a result, NMM charges various charting rates, which align with the rest of the industry. Moreover, since its fleet is also on par with its sector, NMM is mostly a play on seaborne transportation services worldwide.

Source: Navios Maritime Partners Fourth Quarter & Full-Year 2023 Earnings Conference Call.

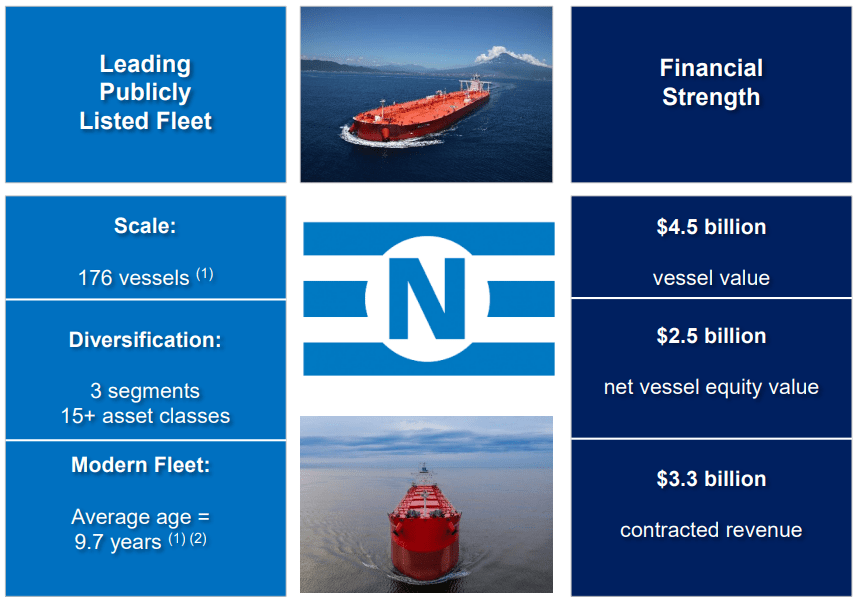

If we look at the company’s fleet, NMM has 176 ships, according to its website and latest earnings presentation. However, as of its November 17, 2023, SEC filing, its fleet included 80 dry bulk vessels, 47 containerships, and 53 tanker vessels (180 total ships). NMM is also building 16 tanker vessels to be delivered through 2027 and 11 extra container ships through 2025. Nevertheless, for our analysis, what matters is that NMM’s fleet is relatively diversified in capabilities, offering NMM operation flexibility and access to different charting rate strategies. For example, Capesize ships with a total deadweight [dwt] of 6.3 million can be used for coal and iron ore cargoes. Dwt is the ship’s capacity for carrying a total weight, including the cargo, fuel, water, provisions, crew, and passengers. However, Capesize vessels are too large to cross the Panama or Suez Canal and travel through the Cape of Good Hope or Cape Horn routes. So, looking back at NMM, it seems well positioned for various routes and charting arrangements, which likely mitigates cyclical risks embedded in the seaborn transporting business.

NMM’s dry bulk vessels, totaling 9.6 million dwt, carry unpacked cargo such as grains, coal, ore, steel coils, and cement. The company’s container ships have a total capacity of 235,414 twenty-foot equivalent units [TEU] to transport cargo, which means that the combined fleet can carry the equivalent of 235,414 standard twenty-foot shipping containers. NMM´s tanker vessels have 6.0 million dwt for transporting crude and products related to light-refined petroleum derivatives. Likewise, NMM has 5 Handymax vessels, mainly for grains or steel cargo. Hence, as a whole, NMM is a significant player in its industry despite its relatively small market cap of just $1.04 billion.

Source: Navios Maritime Partners Fourth Quarter & Full-Year 2023 Earnings Conference Call.

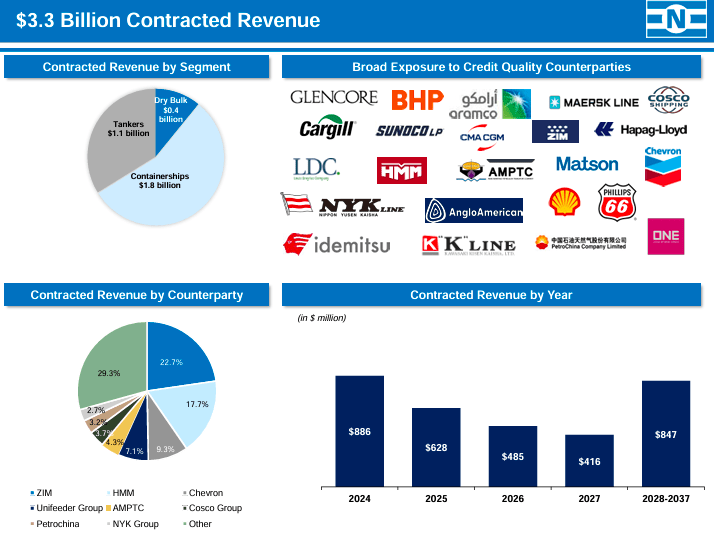

Furthermore, NMM's fleet seems relatively new, with an average age of 9.7 years in 2023, below the industry standard. The company has fleet renewal strategies that include the investment in new vessels and the sale of older vessels. NMM’s “Newbuilding Program” resulted in a $1.6 billion investment: 1) $736 million for ten containerships, nine to be delivered in 2024, and 2) $885 million for 16 tankers, four of which will be delivered in 2024. The financial strategy is to lock in future earnings and use long-term charters to pay the new vessels. For containerships, there is roughly $900 million in contracted revenue; for tankers, there is approximately $500 million in contracted revenue from ten vessels. Thus, NMM’s long-term prospects appear solid, with a steady set of diversified revenue streams and a healthy renewal of its PPE.

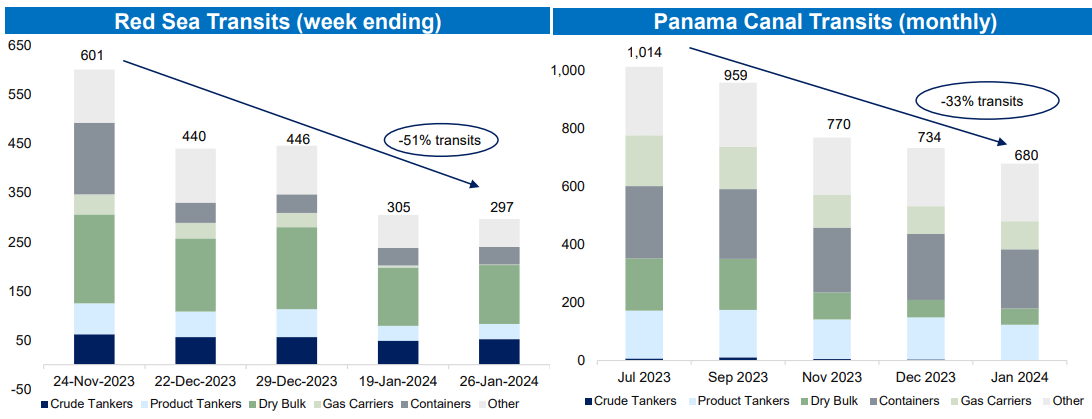

The Red Sea is an important trade artery, with a 51% reduction due to the Houthi attacks on commercial vessels. The attacks of Yemen's Houthi rebels in the Red Sea are causing changes in the shipping routes and could lead to inflation due to increased shipping rates and transit times. Currently, most international cargo has long-term contracts that mitigate immediate price increments for goods. However, the added costs, such as longer routes and expanded maritime security, will eventually be passed to the consumer, and could produce inflation.

Additionally, there’s some disruption in the Panama Canal because of a severe drought that led to a 33% reduction in vessel passages in January 2024 compared to July 2023. Additionally, the Ukraine war has forced changes in world trade, causing longer-haul routes to increase.

Source: Navios Maritime Partners Fourth Quarter & Full-Year 2023 Earnings Conference Call.

Overall, the upheavals in the Red Sea, the Panama Canal, and the war in Ukraine have positively impacted NMM’s financials. Also, the ten top world economies have enjoyed positive growth in 2023, with China leveraging its exporting strength. Moreover, the changes in global shipping patterns have temporarily increased revenues for NMM and other shipping companies that benefit from higher spot market rates and longer voyages that generate more revenue per trip.

Source: Navios Maritime Partners Fourth Quarter & Full-Year 2023 Earnings Conference Call.

So far, it’s fair to say that macroeconomic conditions have been positive for NMM, but the global scenario could change rapidly due to geopolitical factors. Investors need to consider this implicit risk in NMM’s business model when evaluating it as a potential investment. In the last Earnings Call, these events were discussed as they have contributed to a stronger-than-expected Q1 2024 and are impacting NMM's strategies, such as fleet renewal upgrading with more efficient vessels, debt reduction, and securing long-term contracts for stability to preserve financial health in a changing market.

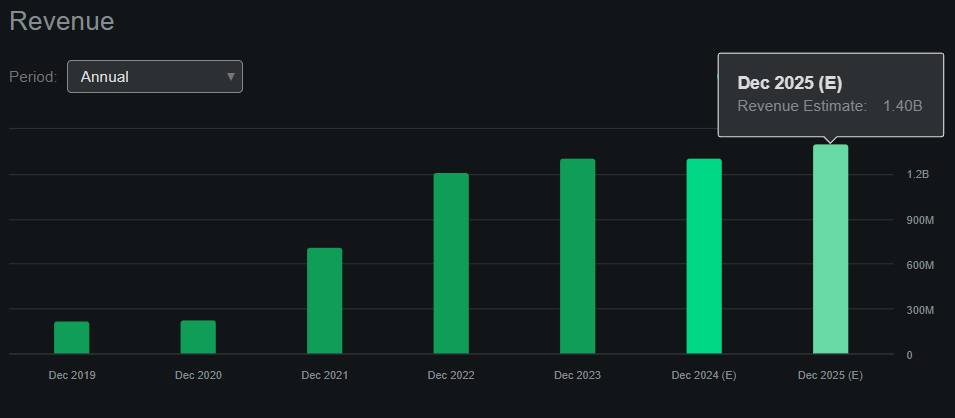

All of this context brings us to the critical question of whether or not NMM is a good investment at these levels. The company currently trades at roughly a $1.04 billion market cap. According to Seeking Alpha’s dashboard on NMM, the company will do approximately $1.40 billion in revenues by 2025. Thus, NMM trades at an implied forward P/S ratio of 0.74, which is encouraging as it’s below 1. Moreover, NMM’s sector median forward P/S ratio is almost twice as high at 1.43, corroborating the undervalued thesis.

Source: Seeking Alpha.

Naturally, this assessment excludes the impact of debt. Indeed, NMM is inherently leveraged, bringing an additional risk layer to it as an investment. Currently, NMM holds $296.2 million in cash and equivalents against $1.86 billion in total debt. We can use the market cap figure mentioned to obtain NMM’s implied enterprise value of $2.60 billion. Thus, NMM trades at a forward EV/Sales ratio of 1.86, which seems more in line with the sector median forward EV/Sales multiple of 1.80. Thus, after considering the company’s leveraged balance sheet, its current valuation makes more sense.

Yet, one factor ultimately leads me towards giving NMM a “Buy” rating. Its equity book value is worth roughly $2.77 billion, which means it’s trading at a P/B ratio of 0.38! Whenever an asset trades below its book value, it usually denotes it’s undervalued. Moreover, since NMM’s sector median P/B ratio itself is 2.68, then I conclude that NMM does indeed appear cheap at these levels. Additionally, I think the company’s vessels are well diversified for various macroeconomic conditions, with a healthy investment in maintenance CAPEX, as evidenced by the ships built through 2027. Lastly, NMM is cash flow positive as of the latest report, generating about $139.3 million in cash flow. I estimated that figure by adding the company’s CFOs and Net CAPEX. So, I’m comfortable giving NMM a “buy” rating for now.

Nevertheless, as mentioned previously, NMM can be risky mostly due to its high exposure to macroeconomic cycles. I believe the business is moderately hedged against this through its diversified fleet and operational flexibility. However, it’s nonetheless an industry highly sensitive to fluctuations in world economic activity. Also, there’s some headline risk involved as geopolitical tensions increase, and some of NMM’s fleet could become targets or suffer attacks, causing shareholder losses. Lastly, NMM is a relatively indebted company, which compounds the previously mentioned risks.

I also think it’s worth pointing out that an activist investor in NMM believes there might be a conflict of interest in the board of directors. Whether this is true or not, this can add uncertainty to the stock’s prospects, leading to an “uncertainty” discount in the shares. Also, it introduces drama into the investment proposition, as there will be an ongoing back and forth between the activist investor and the board. Naturally, if there are indeed conflicts of interest, this will likely lead to loss of shareholder value.

The market has recently turned positive on NMM’s shares. (Source: TradingView.)

Overall, I think NMM is a promising company in its sector, but it’s not without its issues. On the positive side, I reckon its fleet is well positioned for the long run and enjoys operational flexibility despite the ongoing macroeconomic and geopolitical uncertainties. NMM has undoubtedly benefited so far from the trade shifts caused by different macro events, but this is not guaranteed in the future. Moreover, NMM is indebted and highly sensitive to world economic cycles. Lastly, some stakeholders seem to be discontent, particularly an activist investor and NMM’s board, which adds uncertainty to the equation. Yet, on balance, I lean towards a “buy” rating for NMM, and I think it’s indeed exceedingly cheap at these levels, making it a worthwhile investment.