marchmeena29

marchmeena29

The central bank held short-term interest rates steady at this week’s Fed meeting and reaffirmed its desire to shoot for three rate cuts in 2024. With interest rates poised to normalize in the latter part of the year, I think that mortgage real estate investment trusts like Ellington Residential Mortgage REIT Inc. (NYSE:EARN) could make a comeback and become more compelling yield investments for passive income investors.

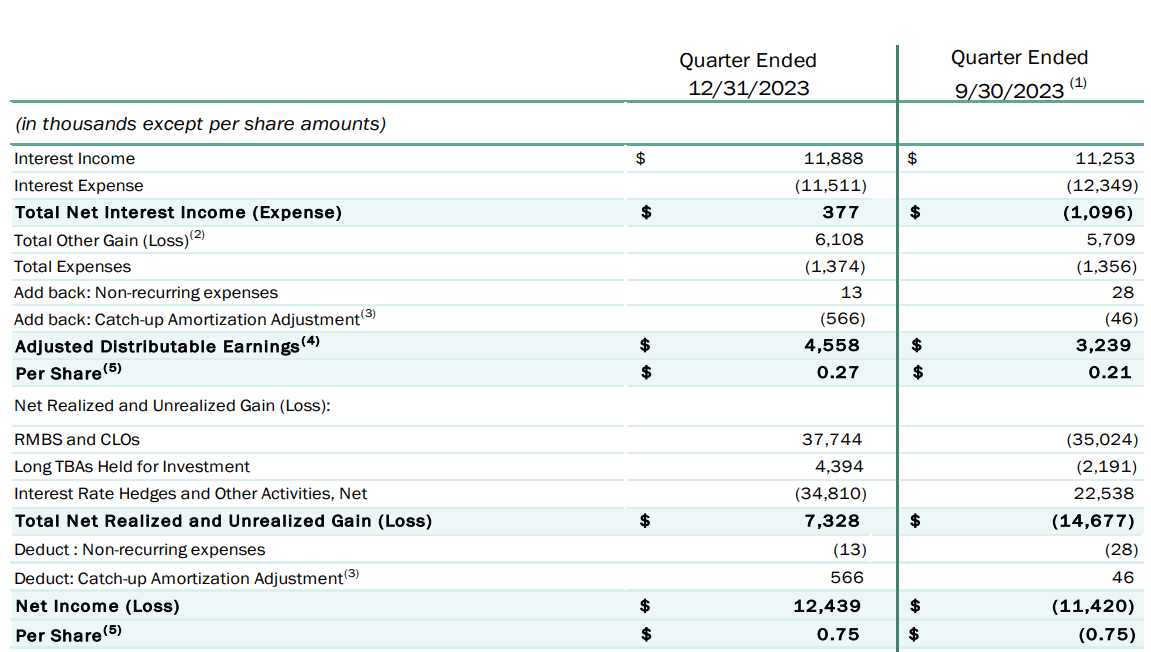

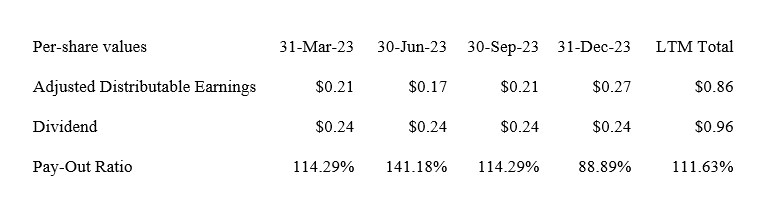

The mortgage trust’s dividend pay-out metrics already improved in the fourth quarter as Ellington Residential covered its $0.24 per share cumulative dividend pay-out with adjusted distributable earnings and lower short-term interest rates point to re-pricing potential for rate-dependent mortgage-backed securities.

With an improved pay-out metric, a dividend cut has also become substantially less likely. As a consequence, my stock classification for Ellington Residential remains Buy.

I have a long position in Ellington Residential Mortgage REIT which I established after the mortgage trust slashed its dividend by 20% in June 2022.

The trust has paid a stable $0.08 per share per month dividend since and Ellington Residential’s pay-out metrics improved in 4Q-23, a main reason why I maintain my current Buy stock classification.

I see the trust’s monthly dividend as sustainable and with a Fed rate shift anticipated for the latter half of the year, Ellington Residential’s pay-out metric may even incrementally improve in 2024.

Ellington Residential is structured as a mortgage real estate investment trust and has a specialization in the acquisition, investment and management of residential mortgage-backed securities and other real estate-related assets.

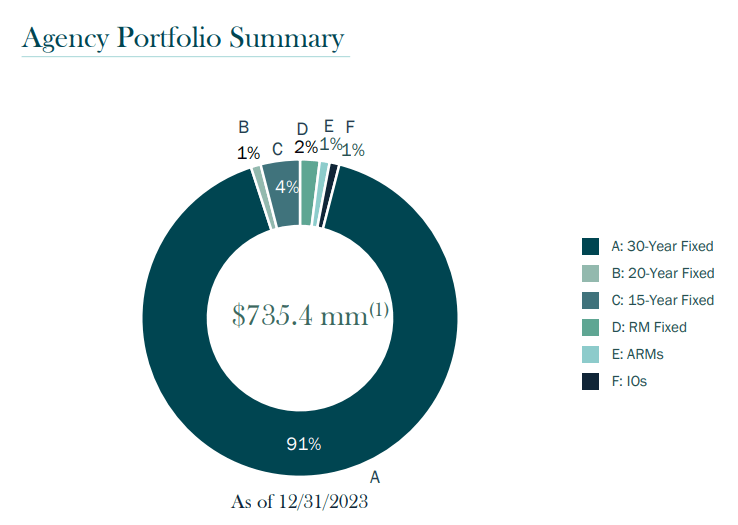

Ellington Residential’s investment portfolio as of December 31, 2023 had a fair value of $735.4 million and consisted mainly of 30-year fixed rate mortgage-backed securities. The trust’s investments also include collateral debt obligations, but agency residential mortgage-backed securities are the trust’s bread and butter.

Lower short-term interest rates are a re-pricing catalyst for mortgage-backed securities as their values tend to increase in a falling-rate environment.

Portfolio Summary (Ellington Residential)

Rate cuts could translate into lower interest expenses for the mortgage trust which amounted to $11.5 million in the fourth quarter and thereby improve Ellington Residential’s net interest income.

With three rate cuts coming in 2024 and with a rate-dependent mortgage-backed security-dominated investment portfolio, the earnings outlook for Ellington Residential has substantially improved in the last couple of months.

Earnings Outlook (Ellington Residential)

Ellington Residential out-earned its dividend with adjusted distributable earnings in the fourth quarter which was the first and only quarter in 2023 in which the pay-out ratio was below 100%.

The pay-out situation has therefore substantially improved and the central bank’s upcoming short-term interest rate cuts should be a boost to the mortgage trust’s spread profile as well.

The trust’s dividend pay-out ratio in the last twelve months was 111.6%, so Ellington Residential still has a considerable amount of dividend risk, though this risk seems to have decreased compared to the mortgage trust’s prior quarters.

With three interest rate cuts on the horizon in 2024, I don’t anticipate Ellington Residential to slash its dividend pay-out.

Dividend (Author Created Table Using Trust Information)

Annaly Capital Management Inc. (NLY) and AGNC Investment Corp. (AGNC), two of the largest mortgage real estate investment trust in the United States, have worked their way back to premium valuations with a re-rating being triggered primarily by the central bank stating in December 2023 that it was willing to consider rate cuts in 2024.

Ellington Residential is presently selling for a 7% discount to GAAP book value ($7.32 as of 4Q-23) whereas both Annaly Capital Management and AGNC Investment are selling at small premiums to book value. I peg $7.32 as Ellington Residential’s intrinsic value as mortgage real estate investment trusts are required to report their underlying assets at fair value.

The reason why NLY and AGNC are priced at a higher P/B ratios than Ellington Residential is that they are the biggest mortgage trusts with long dividend records and large Agency-focused mortgage-backed security portfolios which are poised to profit from lower short-term interest rates.

Ellington Residential so far seems to be headed for a more accommodating operating environment in 2024 than last year. With lower short-term interest rates on the horizon and the trust already seeing an improving trend in its pay-out ratio, the risk to the dividend has decreased.

A dividend cut is therefore now much less likely even in the third quarter which is when the pay-out ratio exceeded 114%. Delayed rate cuts, possibly related to an ongoing inflation flare-up, could be a reason why the investment thesis might not play out as anticipated.

The main reason why I think that Ellington Residential won’t slash its dividend in 2024 is because the pay-out ratio slid below 100% in the fourth quarter and Jerome Powell clung to its earlier remarks of three rate cuts coming in 2024 which could be a re-pricing catalyst for the trust’s underlying MBS portfolio.

The central bank didn’t touch short-term interest rates at its March meeting, but Jerome Powell’s words very welcomed in the mortgage trust sector which relies heavily on costly short-term debt.

I think that the 7% discount to net asset value further improves the risk/reward relationship. Buy.