Vithun Khamsong/Moment via Getty Images

Vithun Khamsong/Moment via Getty Images

New Jersey Resources Corporation (NYSE:NJR) is trading at the lower end of its 52-week stock price range. This has come mostly from the past 6 months when the energy sector has seen a secular downtrend following both lower oil and gas prices, but also capital moving into more high-growth sectors like tech. I hold a lot of conviction that this has left a lot of solid opportunities to be picked at low multiples, NJR included. The company is 23.88% below its 5-year average earnings multiple. Along with being a fantastic dividend payer for 28 consecutive years, NJR is at an appealing price point too. The recent earnings were a reiteration of the long-term growth rate of EPS for NJR by 7 - 9% and the FY2024 EPS estimate was increased by $0.15 to $2.85 - $3. I will be assessing NJR as a buy here, based both on the qualitative aspects it has as a dividend payer along the appealing price point.

NJR is included in the utilities sector, and more specifically in the gas utilities industry. This part of the market has seen quite a lot of weakness to begin the year as the focus has been going into earnings and during earnings season been on tech stocks, I think. The poor start could be attributed to lacking outlooks for the sector, or just not the same explosive growth that was seen in some other years.

As for what NJR does, it operates as an energy service company that distributes natural gas to keep it simple. The company has divided its operations into 4 various segments, those being: Natural Gas Distribution, Clean Energy Ventures, Energy Services, and lastly Storage and Transportation. The first segment has collected around 576 000 customers in some counties in New Jersey and this segment is responsible for the largest amount of earnings generated, at $51 million for the last quarter. This was a slight decrease YoY of $3 million. A lot of growth was seen in the clean energy ventures segment, netting $10 million in earnings, up from a negative $3 million a year prior. NJR has been investing heavily in this part of the company, as it seems to be the future of energy. Last year, the company celebrated the largest solar array together with its partner New Jersey American Water.

Company Segment (Earnings Report)

Worth mentioning as well is that the energy services segment is expected to make up a much larger source of net financial earnings in FY2024, at 38 - 43% in total. The earnings for the segment look poor as the Q1 FY2022 results included unusually high results following the Winter Storm Elliot. The raised guidance for 2024 was largely due to the strong performance of the energy services segment to begin 2024. The additional $0.15 in EPS guidance could therefore largely be coming from just this segment, one could assume. The segment benefited from volatility in the natural gas markets along with contributions from an asset management agreement signed in 2020. The agreement includes that NJR will be releasing transportation contracts for fees of around $500 million, which will be payable to NJR for 10 years in cash. The reasoning behind this was largely due to efforts in de-rising the segment and securing reliable cash flows. I would have to say the agreement ensured both of these are a reality. Over half will be paid between 2022 and 2024, which is why the company expects higher guidance, as the general operative performance has been strong so far. Between 2025 and 2031 there will be $34 million annually in cash payments for the segment. This is an over 10% additional contribution to the TTM net income that NJR has generated.

Operating Expenses (Income Statement)

Worth looking at the next quarters will be the operating expense for the company, along with an update on the base rate filing that NJR filed on January 31, 2024, seeking a $222.6 million increase to its base rate. The filing is based on an overall return of 7.57% and a ROE of 10.42% for the business. The positive news here would potentially be bullish for the stock price in the short term. Margins have been growing steadily for the business and were a key reason for the net earnings for the gas distribution segment maintaining robust results, even as operating expenses and depreciation increased.

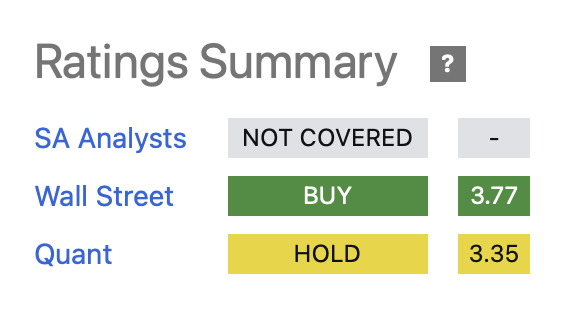

Ratings Summary (Seeking Alpha)

The rating summary for NJR is a hold on the quant at 3.55 which is the combination of a lot of valuation based on historical metrics for the business, but growth estimates for the company are not very strong. The same gas prices as in early 2022 I don't think will be seen anytime soon, and this means growth is lacking somewhat. What NJR has going for itself though is strong margins. TTM net margin of 13.96%, compared to a 5-year average of 8.55% for NJR. This I think will be further robust as the additional cash that NJR receives from its energy service segment will help boost the bottom line. Gross margins are also high at 34.49%, a 78.89% difference from its 5-year average.

Dividend Summary (Seeking Alpha)

When I assess the value that you get with a company, it comes down to two things, a dividend or a buyback program. With NJR you get one of these right now. For the past 28 years, NJR has been raising its dividends, even during the pandemic when a lot of companies related to energy services were struggling badly. The 5-year growth of the dividend is also within the long-term targeted EPS growth range of 7 - 9% for NJR. I do anticipate the dividend to grow similarly to this sale over the long term. The payout ratio is 70.43% which isn't alarmingly high I don't think. It's high, but still leaves NJR with around $70 - $80 million annually to spend on asset expansion. The yield is 4.07%. NJR has however been diluting shares for the past several years. The last 5 years have meant an average annual dilution of 1.78%. Together this means that should this continue, the combined value that investors get right now is 2.29%, along with an 8% average EPS growth over the long term. This means that the expected return that I see for investing in NJR right now is 10.29%, a very solid and reliable return over the next decades.

The annual expected return of 10.29% is higher than the median expected GAAP EPS growth for the utilities sector, which is 5.95% currently. With such an outperformance, I would expect NJR to also be valued at a premium to it. Currently, NJR is valued 7.44% below based on earnings. I would argue a 10% premium is within the realm of possibility for NJR and can be argued reasonable given the long-term outlook. At a 10% premium, the P/E would be 17, and mean a price target of $48 with FY2024 EPS estimates of $2.87, which is the lower end of the guidance. If NJR manages to meet the higher end of the guidance, the price target for me rises to $51 instead, leaving an upside of 23.5%.

The bear thesis with NJR right now revolves around lacking growth in the asset base which would help drive future EPS growth. If NJR can't expand its customer base, it will have less potential to meet its 7 - 9% EPS terminal growth rate. Natural gas volatility in prices would be a risk for the company, but we have seen the positive impact this has had on the energy services segment before, so the risk for this seems somewhat hedged, actually. A larger cash position would be further de-leveraging the balance sheet too. $2.74 million is nothing in cash when the market cap is over $4 billion.

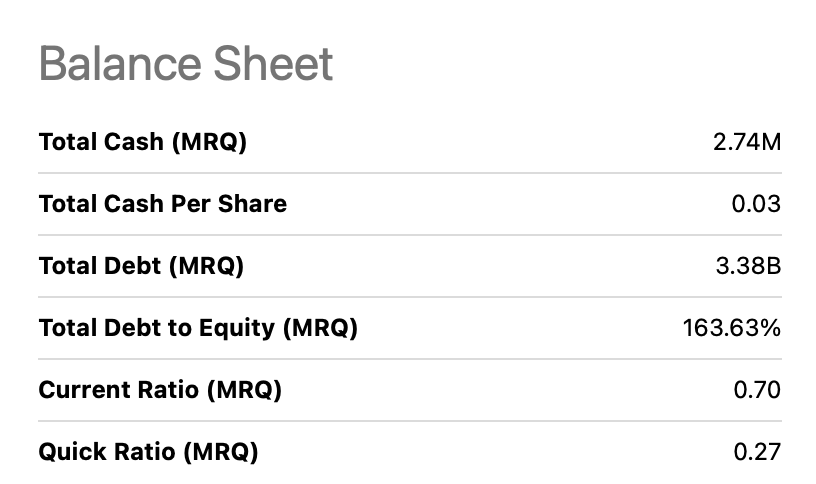

Balance Sheet Highlights (Seeking Alpha)

The balance sheet seems to be the weak spot for the company currently. The current ratio is at 0.7 which is worrying. Over 1 is almost necessary for a business. But I think NJR can get a pass given the reliable earnings they will see in the coming years for most of its segments, and the additional input of $34 million annually in energy services can be used to tackle current liabilities. Accounts receivable along with inventory make up the largest amount of current assets for the business. Current liabilities are largely made up of debt, around $490 million in total. This means that NJR might have to continue to dilute shares to meet its obligations. EBITDA is at $528 million, though, which might mean that dividend raises will be in the lower range of 7 - 9% for the next 24 months. The business of NJR seems reliable and EBITDA has been climbing steadily for the past 5 years and should be able to handle these debts. I do think the stock price will once again start climbing once these hurdles are passed and the sector hopefully receives some love from the market.

NJR has been in a steady downtrend for the past 12 months and trades at the lower end of its 52-week range. The last report was solid and contained EPS raises for FY2024 following a strong performance in the second-largest earnings contributor segment, Energy Services. The value that investors get along with the long-term EPS growth rates leaves a solid upside potential. I will be assessing NJR as a buy.