Philip Steury

Philip Steury

On Sept. 9, 2021, I bought my first shares of telehealth company Hims & Hers Health, Inc. (NYSE:HIMS).

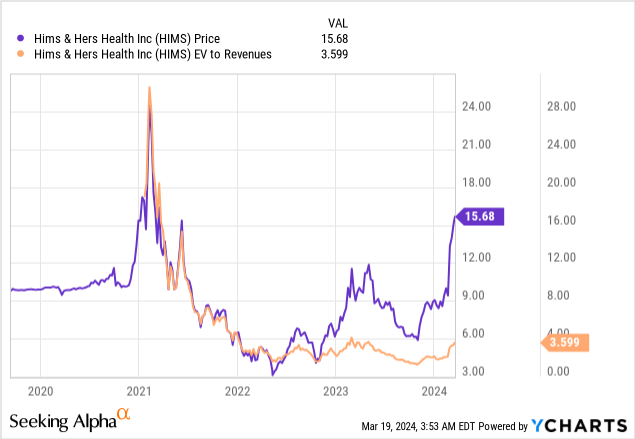

The stock was down from $25 to $8.27 in no time, which I saw as a generational buying opportunity.

I immediately made this promising growth stock the largest position in my portfolio. By far.

On May 12, 2022, Hims & Hers reached an all-time low of $2.79 despite continuously improving fundamentals. My position was down -66% in no time.

On that day, I privately wrote:

We are highly confident that investors who can weather this storm and focus on fundamentals instead of the stock price will look back at this period with a big smile."

Here we are today, with a big smile, being up 462% since that all-time low and more than doubling over the past six months.

I still own my full position and recent developments have increased my conviction that this growth stock can (still) generate significant wealth for investors holding on for 10 years or longer.

Why? Let me share the five reasons that make Hims & Hers such a promising stock for the long term.

Buying a great business is one thing.

Buying the business at the right time, without being impacted by your emotions, is another.

Just think about this staggering fact:

$10,000 invested in Amazon.com, Inc. (AMZN), one of the greatest businesses of all time, on 01/01/2000 would now be worth $488,000.

However, not buying at peak greed of this dot.com bubble and just waiting until 01/01/2002, when peak fear hit the market, would have turned this $10,000 into $3,225,000.

Understanding the impact of investor emotions, alongside fundamentals, is key to generating wealth in the market.

So, why is this relevant for Hims & Hers?

The stock IPOed in 2020 and was caught up in the 2021 bubble, which as I explained in my previous articles, was very similar to the dot.com bubble.

Its price rose from $10 to $25 in no time.

At peak greed, investors paid 30 times sales for Hims & Hers, a company growing revenues by +74% and generating -16% EBITDA margins.

This bubblicious valuation was unsustainable, which led the stock to plunge from $25 to $2.89.

As such, the valuation dropped to 1.3 times EV/sales, while revenue growth stood at +87% and EBITDA margins improved to -7%.

In other words, the valuation ratio plunged from 30x to 1.3x in the course of two years, while the business fundamentals improved drastically.

Or as Jeff Bezos, CEO and founder of Amazon, put it so well:

"The company is not the stock and the stock is not the company."

HIMS stock during peak greed and peak fear of the 2021 bubble:

| Q1 2021 | Q2 2022 | |

| Revenue TTM ($ mln) | 171 | 374 |

| YoY revenue growth | +74% | +87% |

| EBITDA ($ mln) | -8,6 | -7,5 |

| EBITDA margin | -16% | -7% |

| Market capitalization ($ mln) | 4,600 | 641 |

Fear and greed in the market have led to an unusual buying opportunity in Hims & Hers that we would have never gotten if human emotions didn't exist.

And even now, after two years and a +465% rally, that opportunity is still vivid as the EV/sales ratio remains attractive at 3.6x.

Fear is still not entirely gone and the recovery from this bubble bust will likely continue going forward as the valuation remains too low.

The single most important driver for long-term returns of a stock is revenue growth.

And consistency is much more important than the rate of growth.

For compounding to do its work, it may never be interrupted.

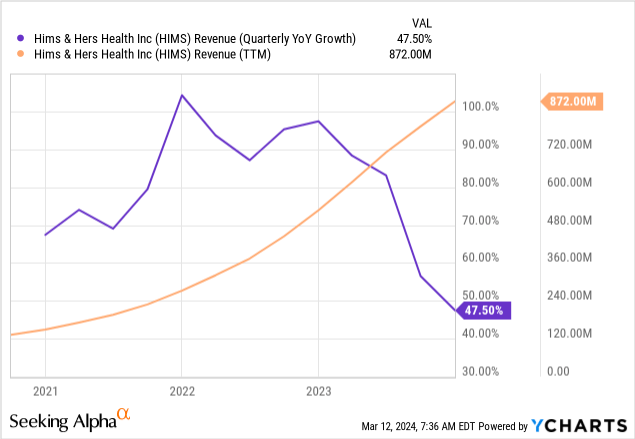

HIMS has been absolutely firing on its growth metrics. Sales expanded from $150 mln to $850 in three years as the annual growth rate never dipped below +67% during all these quarters.

This hypergrowth was nice to see as a shareholder, but it was clearly unsustainable. I always looked forward to the point when sales would slow down to a more sustainable level and at which level this would be.

This crucial moment arrived at the end of 2023 as management guided for lower growth than +50% for the first time ever.

The sales guidance for 2024 was a "make or break" moment for me because this would give us a first indication of how "normal" growth rates could look like for HIMS in the long term.

Management guided revenues of $1.17 to $1.20 bln in 2024, which implies a growth rate of +34% to +38% compared to 2023.

Of course, it is still early days and the future remains unknown, but this 2024 guidance is major positive news for shareholders.

It indicates that HIMS is not falling off a hyper-growth cliff, but is transitioning well from a hyper-growth company to a consistent compounding machine.

Most of the time, a growth stock which is facing increased losses while scaling is a broken business. Avoid them as much as possible.

As strange as it sounds, you don't want profits to be too high either with young growth companies. This indicates that the company is not seeing attractive long-term growth opportunities to re-invest its capital into.

For example, the IPO of sector peer GoodRx Holdings, Inc. (GDRX) on paper looked better than HIMS, with sales growth of +50% and 41% EBITDA profit margins.

However, this meant that GoodRX already was optimized for profits at its early stage, which is a warning sign.

I swiped left on GoodRX (-87% since its IPO) and right on HIMS (+68% since IPO), which I believe was situated at the "golden spot" of growth stocks:

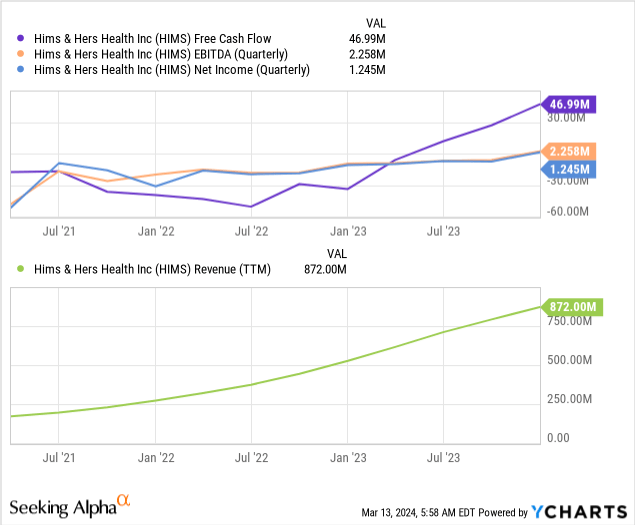

HIMS was looking poor in 2022 with -5% EBITDA margins.

This kept many investors away from the stock, including Jim Cramer. During his Lightning Round on March 19, 2022 (when the stock traded around $5) Cramer said that HIMS "does not work for me" as he "does not recommend stocks that lose money."

What Cramer and others bears did not notice is that these losses were not structural but purely caused by long-term growth investments. These losses were improving as the business scaled and would turn into a profit sooner than later.

Indeed, after having reduced the losses each quarter, Hims & Hers reported its first-ever positive net income during the fourth quarter of 2023.

The stock market reacted surprised with a +31% daily gain on February 27, 2024. Investors that followed the profitability trend already saw it coming from miles away.

After the first quarter of profitability in Q4 2023, we should expect 2024 to become the first full year of profitability as profit margins continue to swell.

This is a structural change for the investment case, which will likely pull in an increasing amount of investors who only buy profitable stocks.

Numbers are not the most important thing to analyze with growth companies like Hims & Hers.

What is the most important thing?

You need to understand the underlying business dynamics and management team on a deep level.

If the business model does not make sense and/or management does not execute the growth plans properly, your investment will go to zero.

I strongly encourage you to free up 1 to 1.5 hours each quarter to listen to the earnings call of the company. You can find this on the investor relations website or here on Seeking Alpha.

Listening to the management gives you great insights on the business dynamics and whether the team is focused on the right things to generate wealth for shareholders in the long term.

HIMS' earnings calls are one of the best I listen to.

(I have to admit that I like Airbnb, Inc. (ABNB), led by Brian Chesky, a tat more.)

The combination of a young, visionary founder-CEO, backed up by experienced people in the sector, is the dream team you need for the business to succeed.

And that is exactly what you have at Hims & Hers.

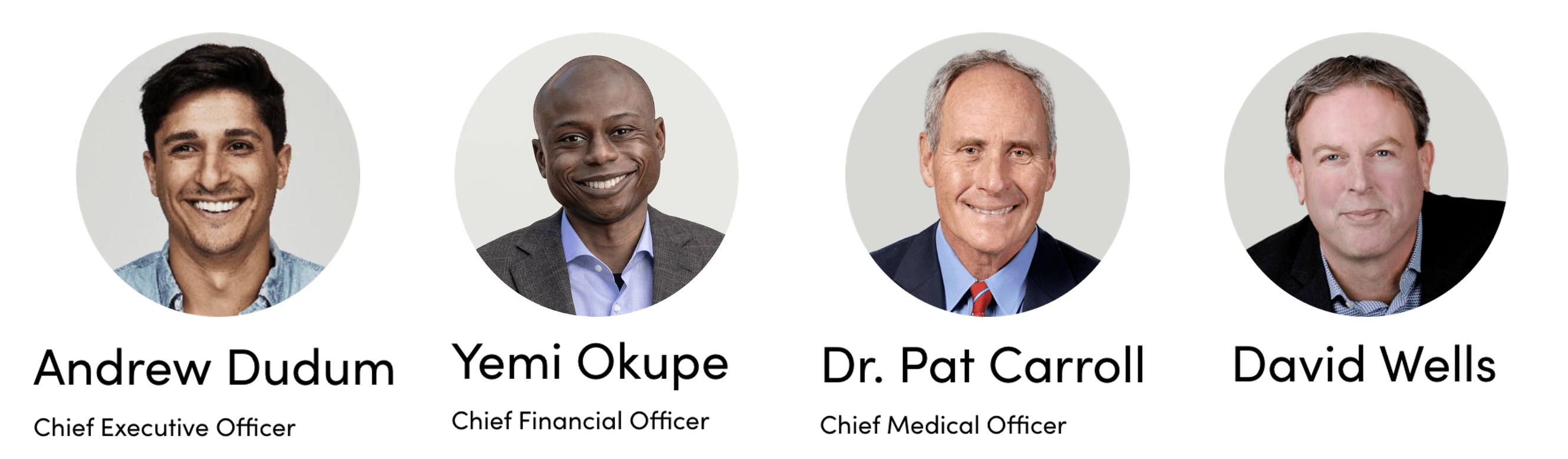

Andrew Dudum founded the company in 2017 and still owns 6.3% of all class A shares outstanding (worth $169 mln today) as the CEO.

At the beginning of 2022, CFO Spencer Lee was replaced by the more experienced Yemi Okupe, to transition toward profitable growth.

Mr. Okupe sounds like a very capable CFO in the earnings calls. He clearly learned a lot as Finance Manager/Lead at eBay Inc. (EBAY) and Alphabet Inc. (GOOG), (GOOGL) and later as divisional CFO at Braintree and Uber Technologies, Inc. (UBER).

What about the board? In 2020 and 2021, Hims & Hers hired experienced businessmen in the medical and consumer services sectors.

Patrick Carroll shares his best practices from medical industry giant Walgreens Boots Alliance, Inc. (WBA) and David Wells has literally been the financial genius behind one of the most successful growth stories of all time, as ex-CFO of Netflix, Inc. (NFLX).

David Wells seems to see a lot of potential in HIMS as he purchased approximately $3 mln worth of HIMS shares after his appointment in 2021.

Fun fact: The insider purchase by Wells is what put HIMS on my radar and what convinced me to immediately start a large position in the stock. As an expert in insider trading, I wanted to be invested by the side of this bright man.

From left to right: Dudum (CEO), Okupe (CFO), Carroll (director) and Wells (director) (Hims & Hers Investor Relations website)

I have read plenty of books and articles about moats, but I have never seen anyone listing "superior customer experience" amongst them. I strongly believe it should be.

Superior customer experience can lock in happy customers for the long term who feel connected with the brand.

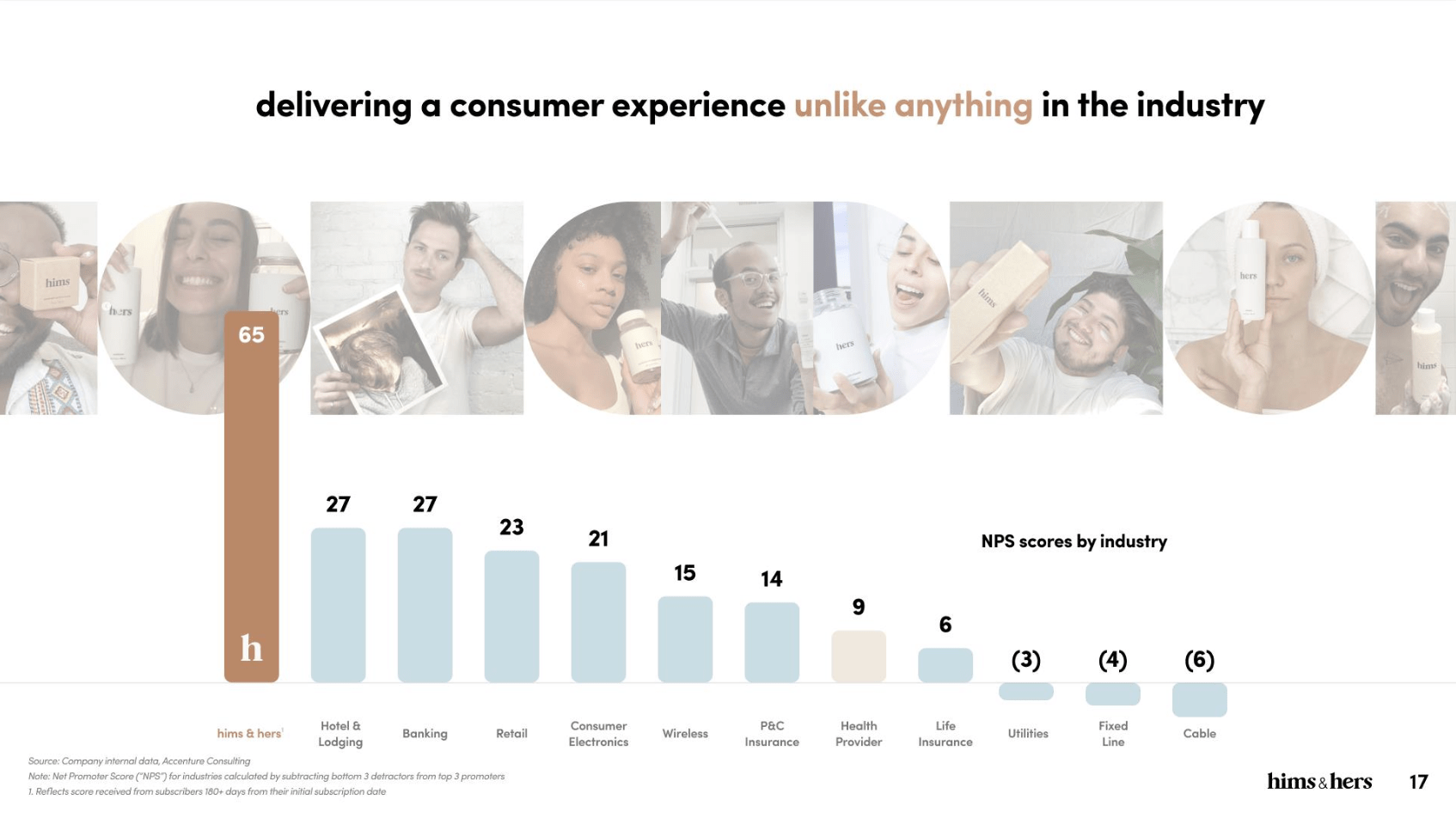

One of the most accurate parameters to measure customer experience, is the Net Promotor Score ("NPS"), which basically subtracts the number of unhappy customers from the happy ones.

It's not a coincidence that leader Apple Inc. (AAPL) has an NPS of 50, while laggard Samsung Electronics Co., Ltd. (OTCPK:SSNLF) only has 35.

Or that leader Amazon.com, Inc. (AMZN) has an NPS of 49, while laggard Walmart Inc. (WMT) scores an 8.

So what about Hims & Hers? It depends on what source you use and when it is tracked.

In its investor presentation from 2020, Hims & Hers shared that it had a high NPS of 65, far above the industry average of 9.

Hims & Hers Investor Presentation

If we look beyond the numbers, we can indeed see that management is rigorously focused on the customer experience.

For example, due to customer experience concerns, they're not participating in the GLP-1 weight loss hype, while competitors like LifeMD, Inc. (LFMD) do. This is what CEO Dudum had to say about it during the Q2 2023 conference call:

The platform is being built to support both existing GLP-1s and future pharmaceutical innovation. But given the instability of the current supply chain inconsistent reimbursement and outstanding safety valuations, these products likely will not be available at launch. Dr. Craig Primack joined us this week as our new Medical Director in Weight Management, bringing to our organization nearly two decades of optimizing treatment protocols for the complex underlying factors driving weight gain.

I was very happy to hear this news. HIMS could bring in tens of millions of revenues and profits with GLP-1s, but prefers not to (yet), given the supply and safety concerns. This increased my trust in this long-term growth story a lot.

Clearly, other investors were not happy with it as the stock plunged by -19% on Aug. 8, 2023. on this news.

The difference between a long- and short-term mindset.

The GLP-1 news was not the only thing that brought down the stock in August while simultaneously making me increasingly excited.

On that day, CEO Andrew Dudum also announced that they would lower subscription prices by as much as 25% to 30%.

Like I said at the start, our mission is to make the world feel great through the power of better health. An often underappreciated aspect of this mission is the necessity of ensuring our platform can reach as many people as possible. The level of scale that we have combined with the efficiency of our affiliated pharmacies enables us to orient users to a model with a treatment-based construct versus a pill-based construct at an exceptional value to them.

This will continue to become more meaningful as we move further away from subscribers with one treatment to subscribers with multi-category treatment. As part of this mission and our ambition to reach as many people as possible, we're excited to share that in the past few months, we've begun to systematically lower prices for many of our longer-duration offerings to make our more personalized subscriptions even more mass market accessible.

It's clear Hims & Hers chooses long-term value from loyal customers instead of being greedy and focusing on short-term profitability.

Does Hims & Hers have a lot of competition from the likes of LifeMD, Inc. (LFMD), Teladoc Health, Inc. (TDOC) and even big giants like Amazon Clinic? Yes!

But personal care is highly personal and in this industry customer satisfaction can be a very significant moat.

The five above-mentioned characteristics are not random.

They have been shaping the success of the best long-term growth stories in the stock market.

Hims & Hers reminds me a lot of many success stories, but mostly of Amazon over the past two decades.

#1 Benefiting from the bubble bust and recovery.

Amazon was, similarly to HIMS, caught in the rise and fall of a market bubble. The price/sales ratio of Amazon plunged from 28x to 0,7x in two years, from the peak to the trough of the dot com bubble, despite improving fundamentals. This led to a generational buying opportunity in 2001.

#2 (Consistent) revenue growth

Amazon was a hypergrowth company in the late Nineties, but has never achieved more than +40% revenue growth after 1999. Nonetheless, its sales grew from $3 bln in 2001 to $575 bln in 2023. How? Because sales growth never dropped below +20% either for two decades, which led to consistent compounding in the long run.

#3 The switch to profitability

Amazon has faced steep losses until the end of 2001 when it decided to transition toward a profitable, more sustainable growth company. On Jan. 18, 2002, the day of its first-ever reported quarterly profits, Amazon also ripped higher by +24%.

#4 A management dream team

Amazon was led by a dream team, including founder-CEO Jef Bezos, who hired a new experienced CFO, Tom Szkutak from General Electric Company (GE). He also added experienced members to the board, including William B. (Bing) Gordon, Chief Creative Officer of Electronic Arts. Gordon. Just like Mr. Wells with HIMS, Mr. Gordon was clearly a fan of Amazon, as he bought $861,000 worth of shares after his appointment in August 2003.

#5 Obsessive attention to the customer experience

If there is one thing that Amazon is about, it is obsessive attention to the customer experience - Bezos

A very good quote of Bezos during an interview in 1999. And I have more interesting insights into how he thinks about customer experience:

" Percentage margins are not one of the things we are seeking to optimize. It's the absolute dollar-free cash flow per share that you want to maximize, and if you can do that by lowering margins, we would do that.

We've done price elasticity studies, and the answer is always that we should raise prices. We don't do that because we believe that by keeping our prices very, very low, we earn trust with customers over time, and that actually does maximize free cash flow over the long term.

Obviously, the businesses of Amazon and Hims & Hers are far from the same. But the resemblance between the two stocks is striking.

It's no surprise for me that Hims & Hers is up +63% in the first 10 weeks of 2024.

The revenue growth guidance and the first quarterly profits that were reported on Feb. 26, 2024, were game changers for the long term.

The perception of Mr. Market on Hims & Hers has (finally) shifted drastically.

Less and less will Hims & Hers be viewed as a Viagra and hair growth SPAC hype. More and more will it be seen as a holistic all-in-one personal health platform with a massive total addressable market ($350 bln) and high profitability potential (20%-30% long-term EBITDA margin target).

Indeed, today only the men's sexual health and dermatology categories contribute more than $100 mln in revenues. However, management has the goal to increase this to five categories by 2025, also including Women's dermatology, mental health, and weight loss. The optimization of long-term value out of each customer seems to be working.

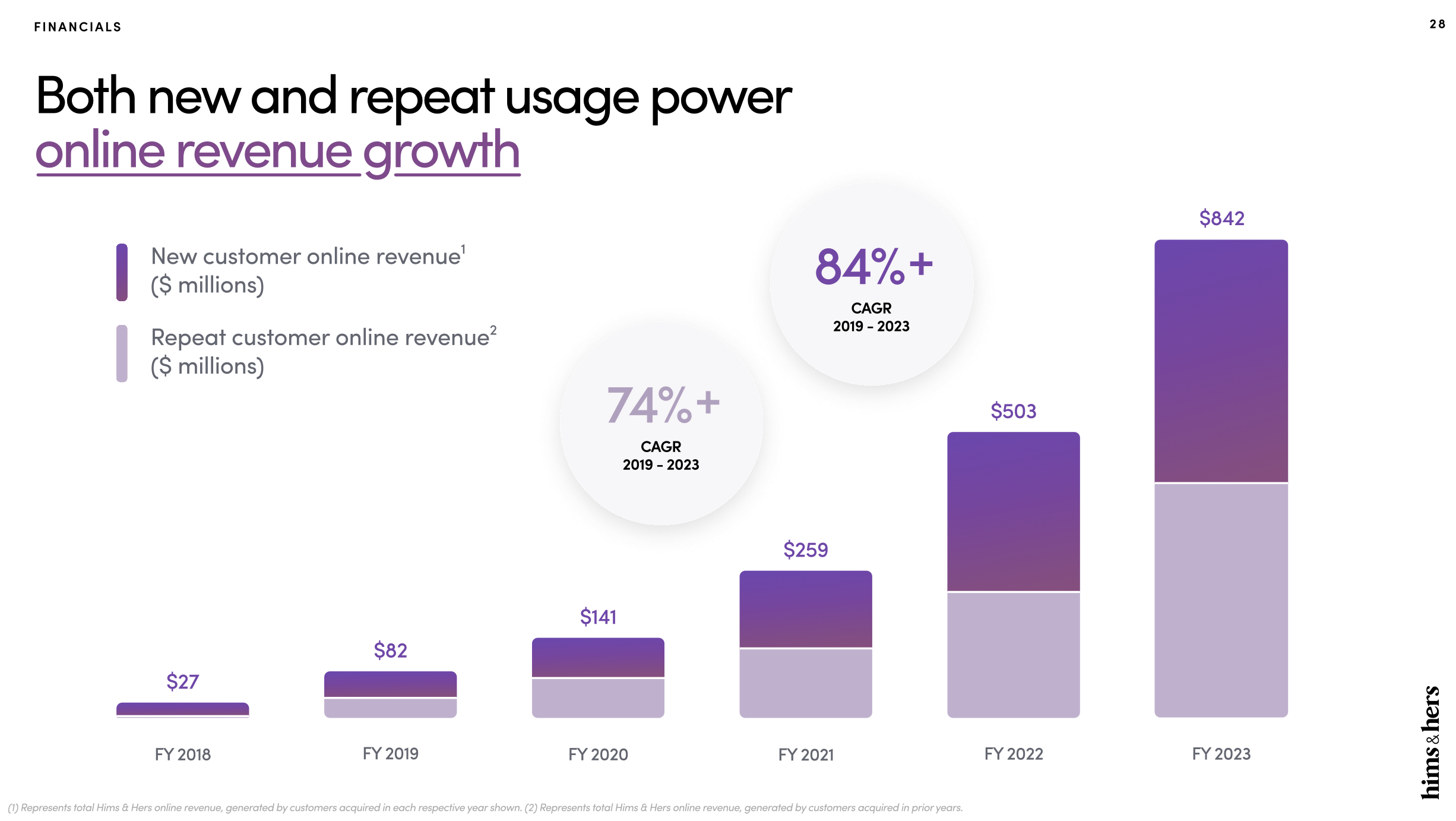

The biggest question for me remains the retention of customers, which management hasn't really provided much data about. The only data we know is that long-term customers have a retention of 85%. But we don't know how many new customers stop their subscriptions in the short term, and I think it's still way too high.

This is very important because Hims & Hers won't be able to scale to large numbers just with new, one-time purchases. We need recurring revenues for the compounding magic to continue.

If recurring revenues don't happen, revenues will plateau at some point and profitability will not be reached due to the continued need for marketing investments.

Hims & Hers investor presentation

I have always seen the release of the app in 2022 as a big game changer for retention given that it puts the company much closer to the end customer.

And now the roll-out of personalized products, which are compounded based on the individual needs of the customer, will be extremely important as well.

It is good to see that management has the right focus as cash flow and retention have been discussed respectively nine and 11 times during the last conference call.

If the management team remains focused and committed to the long-term vision, and they continue working on improving the retention rate, I believe that my original investment case can be achieved: A 100x return in 13 years (by 2034).

Initial projections of HIMS' long-term numbers, made in 2021. (Robbe Delaet)

How did I come up with this number?

In 2021, I laid down my projections that revenue growth would slow down from +78% in 2021 to +55% in 2022 and gradually towards +17% by 2034. This would result in $12.7 bln of annual sales by 2034.

If HIMS reaches a 30% profit margin and the market gives it a 40x P/E multiple by then, Hims & Hers can reach a market capitalization of $152 bln, or 100x what I bought it at in 2021.

How do I look at this now, three years later?

Hims is well ahead on revenues, having reported $872 mln in sales versus the $616 mln in expected for 2023.

It's slightly behind on profitability as it has invested more heavily in future growth than I anticipated. I expected $12 mln in net profits for 2023 and they did -$23 mln. However, I believe they will be ahead on both of my 2024 targets.

I still feel comfortable about the revenue and P/E projections I made for 2034. The profit margin of 30% might have been too aggressive as management later gave 20%-30% EBITDA margin projections for the long term.

If net profit margins come in at 15-20%, we would need either more growth, a higher P/E or just wait a couple more years of compounding to achieve my 100x target.

I would like to end this article about Hims & Hers with a last quote from Bezos:

Given a 10% chance of a one hundred times payoff, you should take that bet every time.

I gave Hims & Hers a 20% chance of a one hundred times payoff in 2021.

I increased that chance to 33% today.

Keep in mind that this means that the chance of failure still stands at 67%. Risks are above-average for young companies like Hims & Hers which still have a lot to prove. The path to long-term success is very long.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.