NicoElNino

NicoElNino

Certain utilities offer investors reliable dividends, as well as a less risky way to invest in the energy transformation increasingly required by regulation. NiSource (NYSE:NI) is one of those utilities evolving and adapting to new ways of producing and delivering energy. With a current yield of 4%, NI offers income investors an indirect way to invest in infrastructure spending. Pure solar, wind, and hydrogen-related companies have, thus far, produced disappointing stock performances. Comparatively, NiSource is quietly adopting many of these alternative ways of generating energy with the benefit of being a public utility that enjoys regulatory approval of rate adjustments and supportive financing. If steady income, along with a diluted way to invest in energy infrastructure spending is your objective, NiSource is a credible candidate.

NiSource's history reflects the M&A activity often seen when reviewing utilities. Predecessor companies date back as far as 1847 but it's NI's changes in the last 9 years that are key to a positive outlook for the utility. In 2015, NI split off its interstate pipeline business (the Columbia Pipeline Group) from the company's natural gas and electric utility subsidiaries. The intent was to become a pure-play utility and NI emerged from the separation as one of the largest fully regulated utility companies in the United States. Further change took place in 2020 when Columbia Gas of Massachusetts was sold to Eversource Energy. These slimmed down changes have started to show up in NI's earnings and stock price over the past 3 years since 2021.

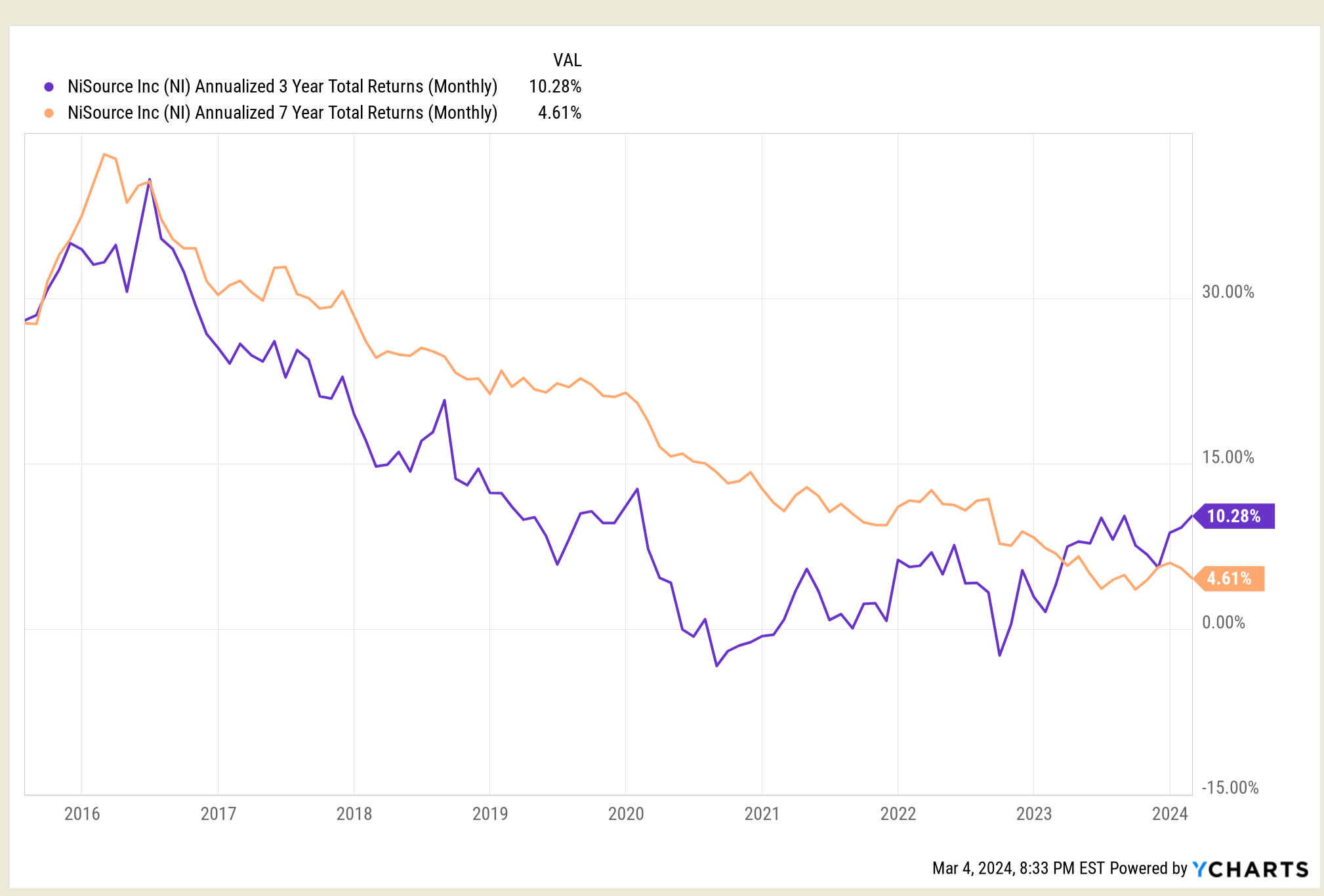

The graph below shows the relative performance of NI's stock in the last 3 years when compared to the utility's annualized returns since 2015.

Ycharts.com

Since 2021, NI has been able to annualized a total return over 10%, doubling what the annualized total return has been since becoming a fully regulated utility. The table below, courtesy of NI's website, details the stock's performance since 2015.

| BREAKDOWN | NYSE:NI |

|---|---|

| Start Date | Jul 15, 2015 |

| End Date | Mar 1, 2024 |

| Start Price/Share | $16.98 |

| End Price/Share | $26.13 |

| Total Return | 53.89% |

| Compound Annual Growth Rate | 5.12% |

| Starting Investment | $10,000.00 |

| Ending Investment | $15,388.69 |

| Years | 8.6 |

Although in the last 6 months NI has returned a flat ~ 1%, this is a better performance than most other utilities still impacted by high-interest rates and the competition from money markets, CDs and short-term Treasuries. Seeking Alpha's "buy" quant rating reflects NI's relative strength compared to peers.

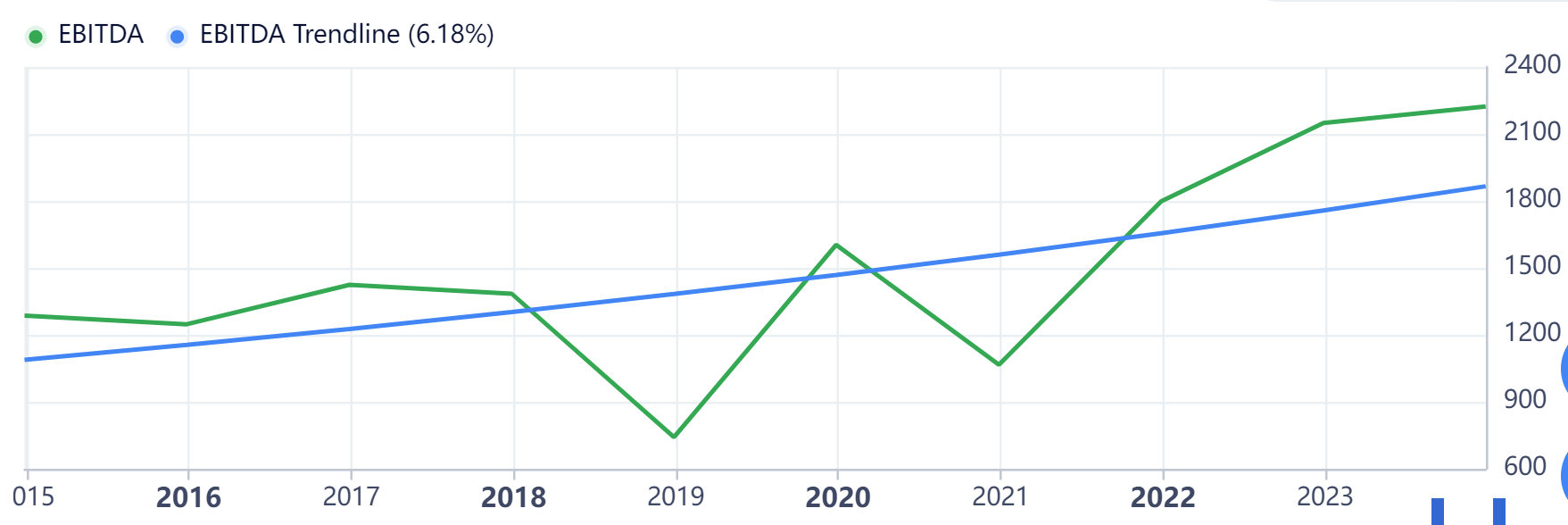

The "Infrastructure Investment and Jobs Act" and the "Inflation Reduction Act" contain considerable federal funding opportunities for companies like NiSource. Besides financing help, these legislative measures set a favorable tone for how regulators view rate adjustment requests. Supportive federal funding, combined with less resistance to rate increases, paves the way for NiSource to continue its improving earnings growth. NI generates revenues and earnings from its natural gas distribution operations (70% of sales) and electric division (30%). Revenues can be variable year to year due to the underlying commodity's price ups and downs. Last year's 6% decline in revenues reflect natural gas' most substantial percentage decline since 2006. On the other hand, 3 favorable rate increases for both segments in 2023 and operational efficiency helped earnings increase, sustaining the 6% earnings growth trend line since becoming a pure play utility. The chart below shows the utility's EBITDA trend line since 2015.

gurufocus.com

Management estimates future earnings will continue to grow at a rate of 6 to 8% through 2028, aided by annual base rate growth of 8 to 10%. Favorable rate increases from regulators reflects federal and state-level demands for transitioning to forms of renewable energy and zero emissions by 2040. NiSource's capital expenditure program to spend $16 billion over the next 4 years takes advantage of this supportive government backing. In a muted way, the Infrastructure Bill and Inflation Reduction Act enable NiSource to be viewed as a mellow growth company.

Spending more on capital expenditures than a company's market capitalization seems an ambitious undertaking. For NI, however, governmental funding and favorable rate reviews (to offset the capex) turbo charges the utility's prior moves to renewable forms of energy generation and system upgrades. For example, in 2018, NI began implementing one of the fastest coal transitions in the energy industry: 74% of NI's coal-fired electric generation will be being reduced to 0% by 2028, replaced by a mix of low emission sources like solar and wind-powered assets. Indeed, the utility has fully embraced the "net zero by 2040" goal with a range of projects: reviewing renewable natural gas producers and ways to interconnect them with NI's distribution system; actively considering hydrogen hub proposals across their six-state operating territory; continuing their pipe replacement priority and improving on methane detection; and, investing in ways of storing energy via batteries and gas peaking plants.

Late last year, Moody's rating agency predicted the 28 utility companies they follow will spend $745 billion on energy infrastructure over the next 5 years. And, they cited an important consideration for these utilities:

Regulatory support, as well as a company’s ability to navigate state legislative developments and to develop capital investment plans that are aligned with [a] state’s decarbonization initiatives, typically ensures timely recovery of investment costs which increases internally generated cash flow."

Thus far, NiSource has shown the ability to navigate the varying legislative bodies in their six-state territory and receive favorable regulatory relations. As for capital needs, last year's sale of 20% of its Northern Indiana electric subsidiary to Blackstone's infrastructure unit (raising over $2 billion) bodes well for NI's funding needs, in addition to help from federal agencies. Furthermore, the company's experience of recovering 75% of capex upgrade spending within 18 months through rate hikes is NI's expectation for future "infrastructure modernization." Currently, the company has an investment-grade rating from Moody's and S&P's rating agency.

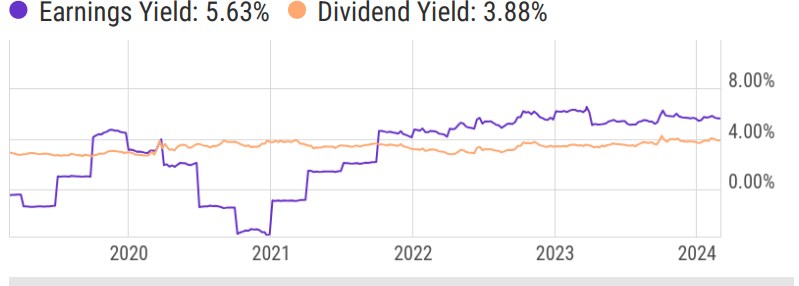

NI's current yield hovers around 4%, above its 5-year average dividend yield of 3.5%. For the past 7 years, the dividend has grown at an annualized rate of 6%, a growth path management expects to continue. The company has paid a dividend for 12 years but did lower it after selling its pipeline business and becoming a fully regulated utility. The dividend-per-share amount is now above the level prior to this strategic slimming. NI's dividend is considered safe thanks to a manageable 60-70% payout ratio, supportive earnings and favorable regulatory relations. Below is a chart showing how NI's earnings have improved relative to the company's dividend generation.

Ycharts.com

With a current P/E around 16x, NI is trading below its historical average of 18x. At $26/share, NI is slightly undervalued on a P/E basis. The stock traded over $30/share in 2022 and could get back to that price if interest rates reverse their 'higher for longer' sentiment and earnings surprise to the upside. However, it would take becoming a buyout candidate and/or an activist investors' impact for this low beta stock to rocket higher. Both of these scenarios aren't out of the picture. Blackstone's partial purchase of NI's electricity generating subsidiary could lead to more interest in the utility's other subsidiaries. And, private capital entities have been interested in natural gas distribution acquisitions. For example, Carl Icahn's positive impact on Southwest Gas Holdings (SWX) shows what an outsider can do to a utility's stock price. That said, NI is best viewed as a steady stock with an adequate dividend yield and healthy growth potential.

As long as negative momentum characterizes Wall Street's view of utilities, building positions incrementally in best-in-class utilities, like NiSource, makes sense. Eventually, short-term interest rates will not be such stiff competition to NI's current 4% yield. When this takes place (an unknown), a utility growing its dividend at a 6% rate should provide a decent total return, especially relative to the risk assumed. Thanks to the push for infrastructure spending, NI has accommodative regulatory and legislative support reinforcing its earnings and dividend stability and growth. For investors worried about a slowing economy and/or stock market correction, NI is a utility with better-than-normal growth potential over the next four years. It is a buy (best done incrementally) for a conservative investor wanting a low volatility stock with 'good enough' dividend yield.