Yossakorn Kaewwannarat

Yossakorn Kaewwannarat

The market increase over the last few months has been unmistakable and captivated investors. I don't think I have ever seen this level of "FOMO" ("fear of missing out"). Investors are jumping over each other to pour money into technology stocks at a rate equal to the great dot-com boom of the late 90s.

Check out the below chart from Deutsche Bank showing cumulative sector fund flows. Other than consumer goods, technology is the only sector with positive inflows- and they are massive!

isabelnet

The S&P 500 (SP500) is up 25% in five months. This is something that has only happened 10 times since 1929. The driver of that is the Fed's pivot expectation after they paused last year.

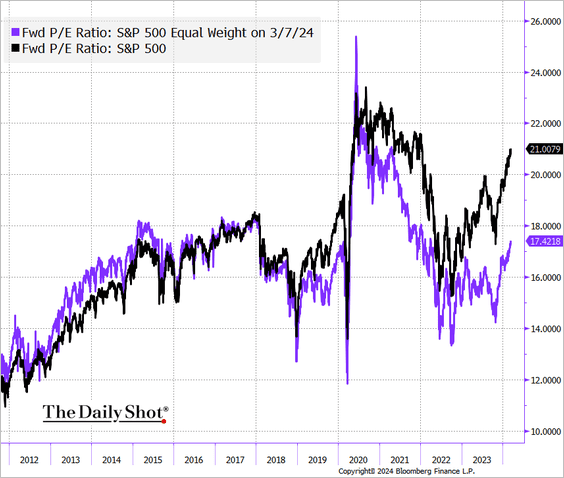

This is pushing up the forward P/E level. Remember, the forward P/E uses the next twelve months estimate for earnings, not actual historical earnings. If earnings estimates come in below those expectations, that means the market is actually more expensive than being reflected by that P/E ratio.

daily shot

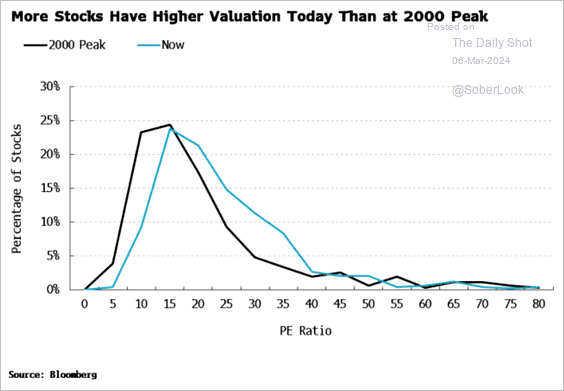

Moving back to the analogy of the late 1990s, we can see from the chart below that more stocks today have a higher valuation today than they did at the 2000 peak. While this can be interpreted and reasoned off in several ways, it is worth knowing. The main fact is that technology companies today are far more profitable today than in 2000 and many of those stocks didn't have a P/E.

Bloomberg

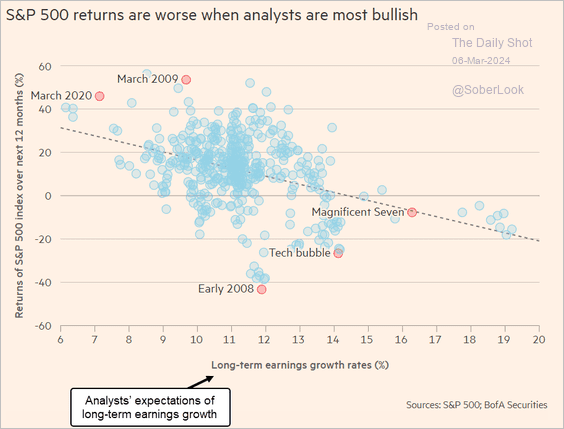

Analyst are very bullish over the next year, but the data doesn't support good future returns when that has been the case. There is a lot of good news embedded into this market.

A lot of the good news is due to the Magnificent 7 which are just booming. But we are now starting to see some of those earnings estimates being curtailed. That could drive lower valuations down the road.

FT.com

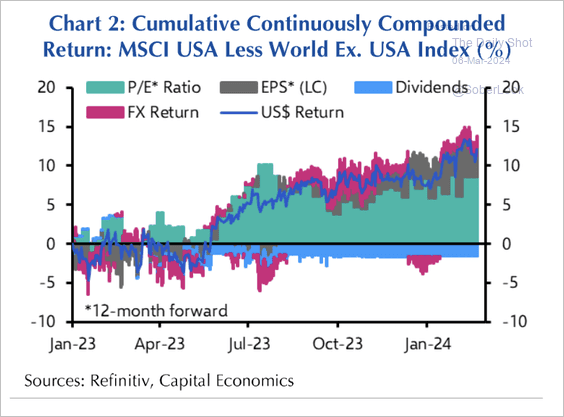

The following chart from Refinitiv and Capital Economics shows the future expectations embedded into the markets. Most of the growth in the index has been thanks to the P/E ratio expanding - i.e., on expectations for higher future growth.

Refinitiv Cap Econ

Over the long term, stocks do better. Of course, they are more risky so modern portfolio theory suggests they should do better.

And a long-term investor should be heavily invested in stocks over bonds, especially if you are in the accumulation phase of your life. Over time, the stocks will perform better and compound at a higher rate of return. The plan should be systematically adding to a portfolio and waiting.

As Morgan Housel puts it in The Psychology of Money, "shut up and wait!"

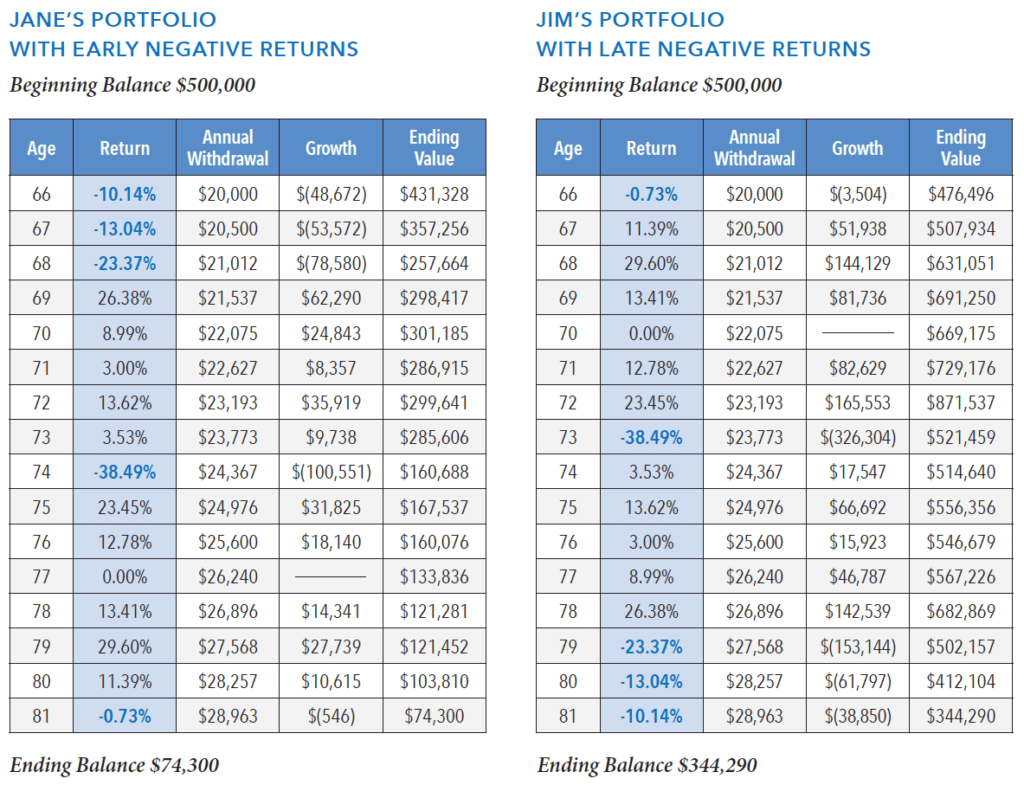

But those in retirement need to be careful. As you withdraw from your portfolio to sustain your lifestyle, you could be susceptible to sequence of returns risk. That is the risk that you sell your assets down BEFORE they recover.

That risk is most prevalent when a person is in their late 50s through 70 years of age. The group has the most years left of portfolio withdraws. Older than that, and your lifetime is shortened by mortality.

Here is a great example. Jim had negative years in his 60s as he withdrew from the portfolio and the "ending value" was permanently impaired.

The Money Advantage

For those around retirement especially, but also for those who cannot handle the volatility of all stock portfolios, bonds can be a good addition. That is most of us.

Volatility needs to be considered. The financial news media is constantly showing stocks like Amazon that have compounded at ridiculous rates of returns since their inception. But they rarely discuss the stomach required in order to realize those gains.

Since the IPO, the stock is up 180,000%. However, if you bought it then, you would have to have endured some extreme volatility. At one point in 2002, the stock was down 90%+ off its all-time high. Would you have held?

That's just one drawdown. There were two 50% or more drawdowns and five of 25% or more.

If you could hold or you're Rip Van Winkle and went to sleep for a couple of decades, you did well.

Interest rates are poised to drop after a "generational opportunity"

materialized in 2022 and 2023. The Fed, to put out the fire they partially caused in their 2020 response to Covid throwing massive amounts of stimulus into the economy, had been raising to combat inflation.

In early November, they announced that they were done raising rates.

PGIM believes this means we are entering a Golden Age for fixed income with very strong risk-adjusted returns. This is because stocks have NOT fallen as is typical when the Fed pivots (due to the economy slowing and maybe entering a recession). Instead, they are at all-time highs.

At the same time, the Fed is poised to cut rates (the timing and magnitude remain up for debate). This is a rare environment where stocks are high and the Fed is likely to cut rates significantly.

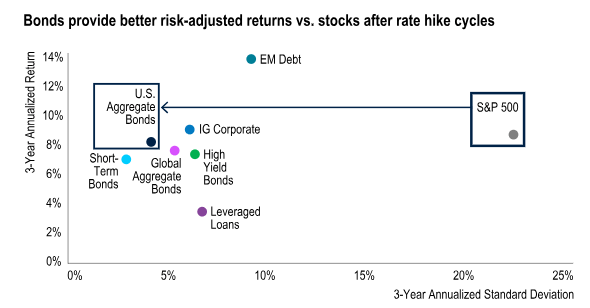

The chart below shows how, historically, when the Fed is done hiking rates, bonds provide much better returns on a risk-adjusted basis. In other words, you can almost the same return in bonds as you can in stocks with far less risk.

For those in that age zone mentioned earlier, it may be prudent to shift some assets to bonds to protect against downside moves in the portfolio as you withdraw from it.

PGIM

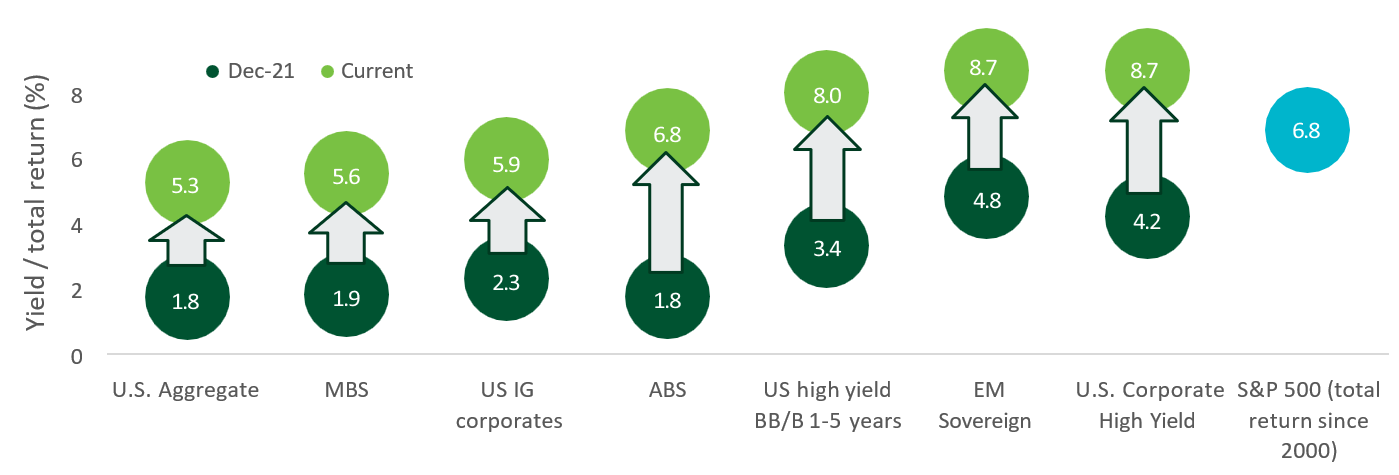

If you don't believe PGIM, here is AAM with a similar assessment:

There are currently potential rewards out the curve. Bond yields look equity-like (Figure 2) at a time that equity ironically might not. Volatility is a constant threat against a backdrop of high rates, quantitative tightening, and an economic slowdown. We think locking in returns through fixed income could be a smart move.

Advisors Asset Mgmt

My largest individual bond position is with Main Street Capital (MAIN). This is a high-quality and well-run business development company ("BDC") that is investment-grade rated. You can lock in 6.6% for the next 5 years with very little overall risk.

My second pick is National Health Investors (NHI) and their 2031 notes. These are a bit longer at 7 years, a BBB- investment grade rating, and a 6.4% yield to worst. The stock has done well over the past year rising 16%. The common shares carry a 6% dividend yield, which is helpful to any bond investor as that will get cut first.

Nobody should be 100% out of stocks given the high inflation, but investors in that precarious age zone of 55 to 70 should consider adding high-quality (read safer) bonds to their portfolio and lock in 6% for the next five to seven years. Why not have that floor on your portfolio?