Wolterk

Wolterk

Natural Grocers by Vitamin Cottage (NYSE:NGVC) is a retailer of natural and organic groceries and dietary supplements that aims to provide consumers with affordable, high-quality products. Although NGVC’s revenue growth has been accelerating over the last three years, it has not reached its 10-year median growth. On the flip side, margins have remained robust. In 1Q24, it continued to report revenue growth, with margins expanding slightly year-over-year. Looking ahead, US organic food demand is expected to remain strong, which will provide the tailwind needed for NGVC to continue growing. However, with my target price close to its last traded price, there is not enough margin of safety. Therefore, I am recommending a hold rating.

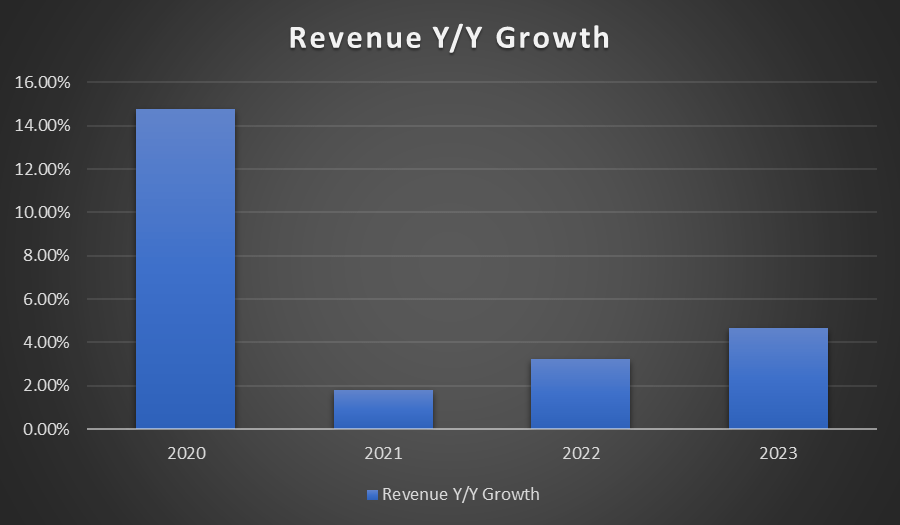

Based on the following chart, it is clear that NGVC’s revenue growth in the last three years is lower than its 10-year median. In 2020, revenue growth was 14.75%, and it was driven by customers’ reactions to the COVID-19 pandemic. In 2023, although revenue was still growing at 4.68%, it was lower than its 10-year median of 9.71%.

Author's Chart Seeking Alpha Author's Chart

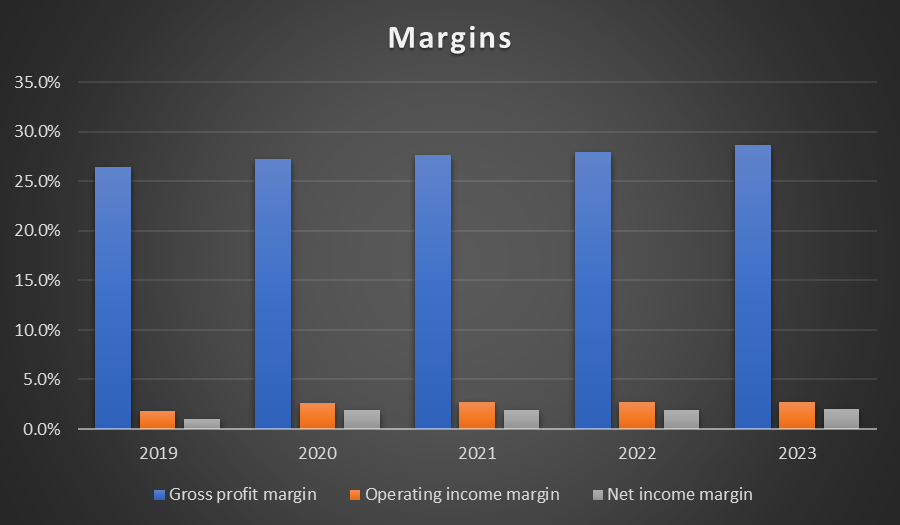

In terms of margins, they remained robust throughout the years. In 2023, the reported gross profit margin [GPM] was 28.07%, a slight improvement compared to 2022’s 28%. The expansion was driven by effective pricing and promotions, which led to a higher product margin. However, 2023 store expenses grew 0.4% year-over-year, driven by higher labor expenses. In addition, administrative expenses also expanded by 0.3% year-over-year due to higher compensation, amortization, software, and legal expenses. As a result, the 2023 operating income margin and net income margin stayed relatively flat year-over-year despite GPM expansion. Operating income margin and net income margin reported for 2023 were 2.8% and 2%, respectively, which is the same as 2022.

NGVC reported its latest 1Q24 result on 8 February 2024. Total revenue reported was $301.8 billion, which grew 7.6% year-over-year. The revenue growth was attributed to the growth in its daily average comparable store sales, which grew by 6.2%, as well as the growth in new store sales. The growth in daily average comparable store sales was driven by growth in transaction count and transaction size, which were up 3.4% and 2.7%, respectively.

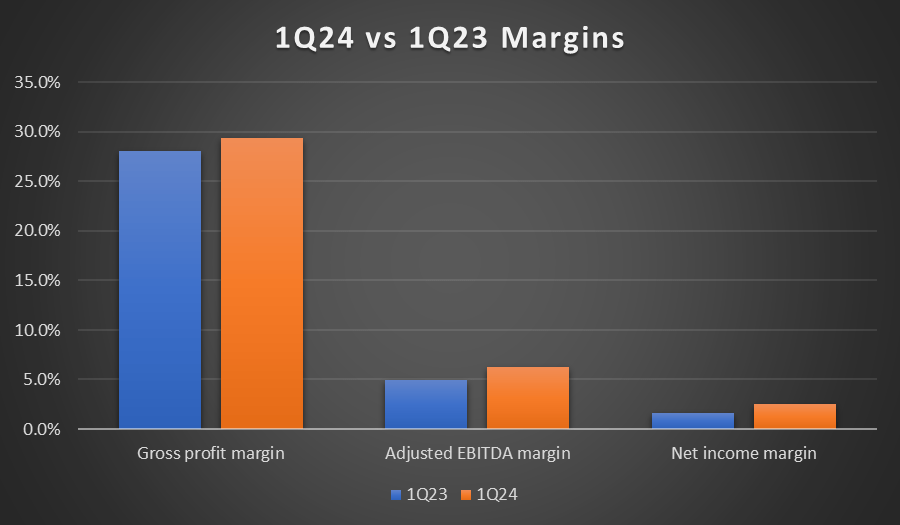

In terms of profitability, I will be looking at its gross profit margin, adjusted EBITDA margin, and net income margin. From the following chart, it is clear that its margins expanded year-over-year across all three categories. In 1Q24, its gross profit margin expanded to 29.4% from the previous period’s 28.1%. The improvement was due to increased product margins driven by effective promotions and pricing and leveraging on store occupancy expenses.

As a result of gross profit margin expansion, it contributed positively to its adjusted EBITDA margin, net income margin, and diluted EPS. Its adjusted EBITDA margin expanded from 4.9% to 6.2%, while its net income margin expanded from 1.6% to 2.6%. In terms of diluted EPS, it grew from $0.19 to $0.34, which represents a year-over-year growth of 78%.

Author's Chart

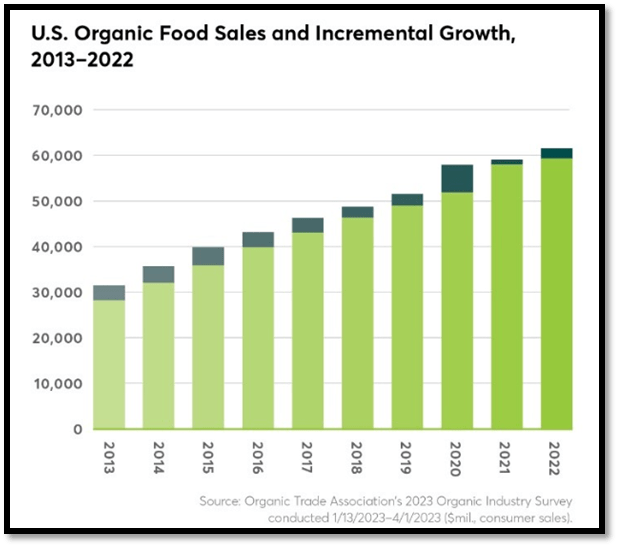

From the following chart, sales of organic food in the US have been consistently growing and showing a strong demand trend. In 2013, sales were approximately $31 billion, and by 2022, they had surpassed the $60 billion mark, hitting another high-level mark for the resilient organic sector. From 2013 to 2022, US organic food sales’ CAGR was approximately 7%.

Despite macroeconomic uncertainties and difficulties, such as rising inflationary pressures and the 2021 global supply chain crisis caused by COVID-19, the US organic food market grew. This demonstrated the resilience of this market and its ability to grow. Looking ahead, I anticipate this trend to continue, which will provide NGVC with the tailwind needed to bolster its growth outlook.

Organic Trade Association

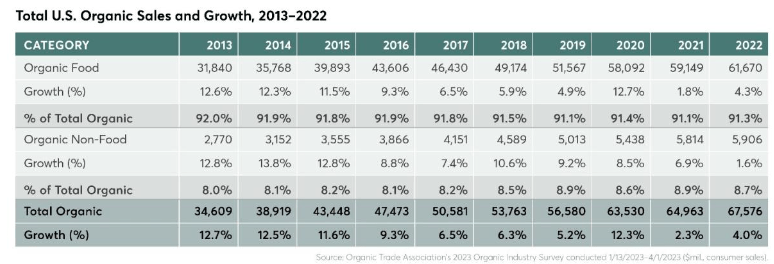

Based on the following table, it is clear that organic food forms the largest share of the total organic market, which stood at 91.3% in 2022. Under the organic food category, organic produce is the top seller. In 2022, organic produce sales were reported at ~$22 billion, which represented ~15% of all fruit and vegetable sales in the US.

Coming in second were organic beverages, as sales in 2022 were ~$9 billion, which grew 4%. Under this category, organic coffee is the leader, as sales increased 7% year-over-year. The third-best-selling produce under the organic food category was dairy and eggs, which reported sales of ~$7.9 billion and grew 7% year-over-year. Organic dairy and eggs accounted for ~8% of the total dairy and egg market. Over the years, the organic food category has been consistently growing despite macroeconomic challenges, and it accounts for more than 90% of the total organic market. Looking ahead, this strong trend is expected to remain robust and bolster NGVC’s growth outlook.

Organic Trade Association

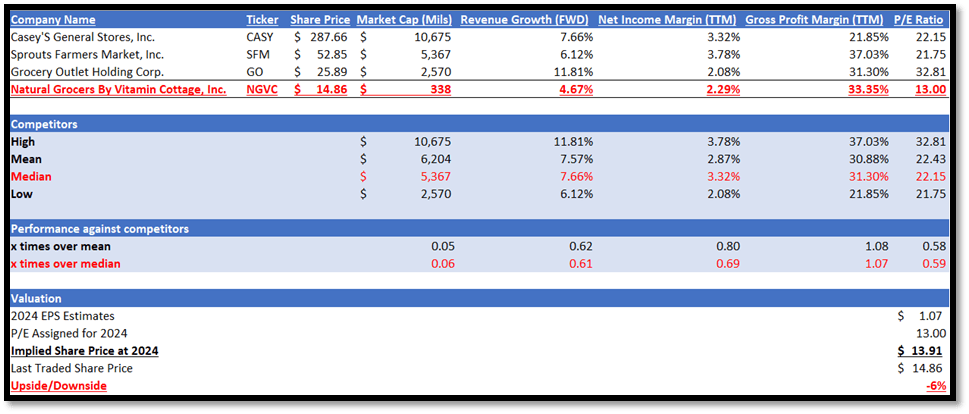

First, I would like to compare NGVC’s growth outlook against its peers. In terms of forward revenue growth outlook, NGVC’s forward revenue growth rate of 4.67% is lower than its peers’ median of 7.66%, which is 39% lower.

When it comes to profitability margins, NGVC did not fare well either. Although its gross profit margin TTM of 33.55% is slightly higher than peers’ median of 31.30%, NGVC’s net income margin TTM of 2.29% is lower than its peers’ median of 3.32%.

Currently, NGVC’s P/E ratio of 13x is trading lower than its peers' median of 22.15x, which, in my opinion, is fair given that NGVC underperformed in terms of growth outlook and net income profitability. NGVC’s 5-year average P/E was 16.98x, but given that its forward growth rate is significantly lower than its historical 10-year median, I argue that it should not be trading at that level. Therefore, it is fair for NGVC to be trading at its current level.

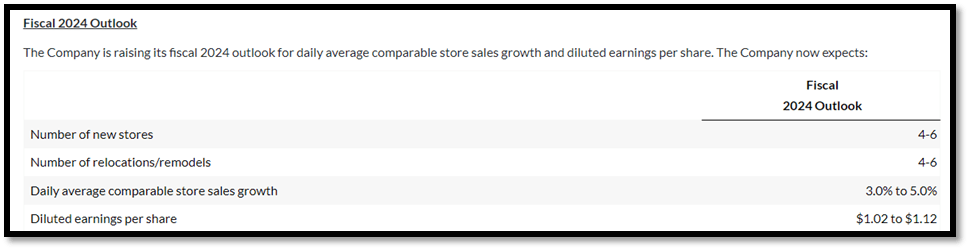

For the 2024 outlook, management guided diluted EPS to be in the range of $1.02 to $1.12, which has a midpoint of $1.07. Given the growth catalysts discussed above, such as the strong US organic food market and consistent growth seen in organic food produce, the higher estimate is justified. By applying its current P/E to its 2024 EPS estimate, my target price is ~$13.91, which does not provide a sufficient margin of safety when compared to its last traded share price.

Investor Relations Author's Relative Valuation Model

One upside risk in relation to my hold recommendations pertains to the strong demand and growth potential of the organic food market. Currently, NGVC’s revenue growth rate remains below its 10-year median. However, it has been gaining momentum since 2021. Given the consistent growth in demand for organic food products, if NGVC were to report accelerating growth in the upcoming years that approaches or is reaching its median growth rate, the market might revise its expectations upward.

In conclusion, NGVC’s revenue growth has been expanding over the last three years, but it is still below its 10-year median growth rate. Despite fluctuating revenue growth, its margins have remained robust over the years, driven by effective pricing and promotions, which led to a higher product margin. In 1Q24, it reported revenue growth of 7.6% year-over-year, with margins expanding when compared to the previous period.

Looking ahead, the strong and consistent growth in the US organic food market over the years indicates that the demand in this sector is strong and resilient. In addition, more than 90% of the organic market is dominated by produce, which NGVC specializes in. For the 2024 outlook, management expects comparable store sales to continue growing at ~3% to 5%. However, despite all these tailwinds, my valuation model indicates no upside potential in its share price. With a lack of margin of safety, I am recommending a hold rating.