mixmotive

mixmotive

Paramount Global stock (NASDAQ:PARA / NASDAQ:PARAA) has fallen significantly over the past year. In addition to its business' inherent sensitivity to secular declines in linear TV and intensifying competition in the capital-intensive direct-to-consumer streaming business, much of PARA's pullback over the past year resulted from its slashed dividends. This was a huge setback for the stock's income-focused investor base.

The set-up continues to highlight the difficult feat of balancing between accelerating secular declines in linear TV and pushing forward its DTC streaming business to profitability amid intensifying competition. While PARA management continues to prioritize content value maximizing, DTC profitability, and unlocking synergies for the broader company, they also have been vocal about a potential sale.

Para already has been on a selling streak for its non-core assets during the past year. This includes the recent sale of PARA's stake in the Indian TV business to its operating partner Reliance Industries. The development follows the disposition of its book publishing business, Simon & Schuster, to KKR in Q4. PARA also has recently merged Showtime with Paramount+ with an aim to unlock synergies and optimize its market share gains within the increasingly competitive DTC streaming business.

More importantly, PARA also has been courting a slew of potential buyers for the entire company. And it's not short of interest, with prospects coming from both within and beyond the media and entertainment industry. In the latest development, The Wall Street Journal has reported that Apollo Global Management, Inc. (APO) has offered $11 billion for Paramount Pictures - PARA's "crown jewel" film studio. The offer follows Apollo's previous interest in acquiring National Amusements, PARA's parent company owned by the Redstone family. The current $11 billion offer for Paramount Pictures is alone more than PARA's market cap. While the market was initially optimistic about the news, momentum had quickly fizzled, potentially indicating prospects that the latest Apollo proposal, like many others observed in the past year, will not make it out of discussion in the board room.

On one hand, Apollo's outsized offering for Paramount Pictures on both a relative basis to comparable studios' M&A activities in recent years and PARA's market cap is attractive. Yet moving forward with such a deal would be de-synergizing for the remaining business and potentially cause further negative implications for the stock. However, we're more concerned about the recent progression of interest amongst prospective buyers of PARA. Specifically, Apollo's recent transition of interest from the broader company to just Paramount Pictures potentially implies that time is running out as other arms of PARA are rapidly losing luster.

To maximize cash flows to mitigate dependence on its rapidly declining linear TV business in funding the transition to DTC streaming, PARA has been consistently offloading its non-core assets. These include the recent dispositions of its Simon & Schuster book publishing business as well as its stake in the Indian TV business. But stepping aside from the operating level, PARA's major shareholders and board members also are mulling a potential sale of the entire company.

Specifically, PARA's board has recently put together an independent committee that excludes its largest shareholder and chair, Shari Redstone, in determining the next steps for the company - which includes a potential sale. And PARA has not been short of any interest. This highlights PARA still has a game in the market despite acute secular headwinds facing its core TV media business, alongside intensifying competition in drawing eyeballs to its DTC streaming. Recently reported interests include:

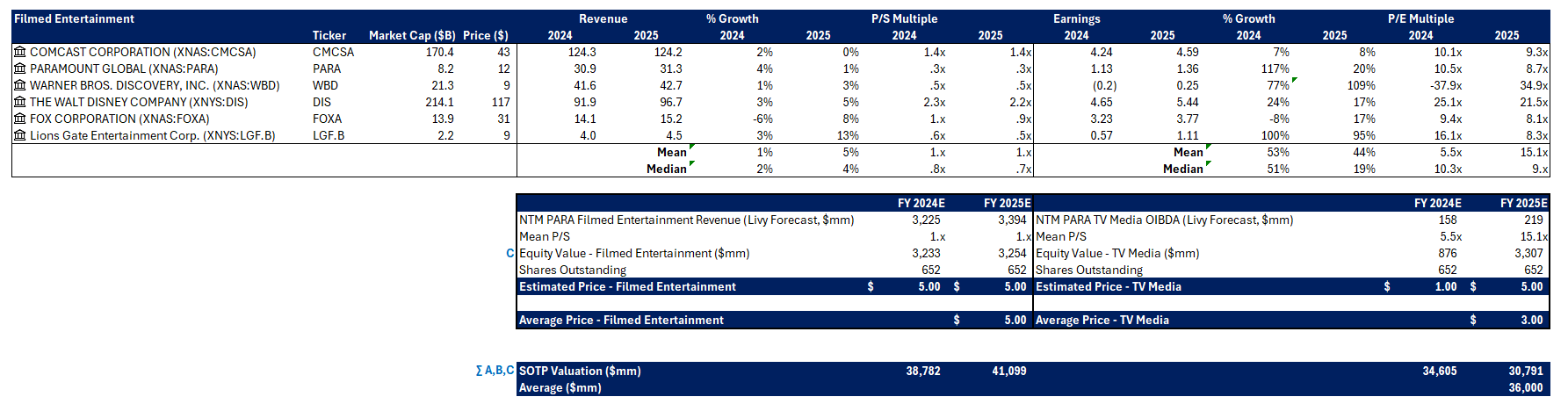

The common thread in recently proposed PARA takeover deals is that all prospective buyers are vying for Paramount Pictures, which Redstone calls the "crown jewel" of the company. This is unsurprising given Paramount Pictures' library of iconic franchises, including Top Gun, Transformers, and Mission Impossible. Despite inherent lumpiness in revenue recognition due to the uncertain timing of film releases, the IP library of Paramount Pictures is self-sufficient in generating perpetual high-margin royalties through licensing and distribution arrangements - especially with added interest in recent years from DTC streaming platforms amid the intensifying content arms race. This is critical to justifying Apollo's allegedly bold offering of $11 billion for Paramount Pictures. As mentioned earlier, the proposed consideration is equivalent to 3.7x TTM revenue and 9.13 TTM OIBDA at PARA's filmed entertainment segment. This compares to the $8.5 billion Amazon.com, Inc. (AMZN) had purchased MGM Studios in 2022, which represented 5.6x TTM revenue and 49x TTM EBITDA, and The Walt Disney Company's (DIS) acquisition of studio assets from 21st Century Fox, Fox Corporation (FOXA / FOX), in 2019 for 2.8x TTM sales and 12.9x TTM EBITDA.

Apollo's latest offer for Paramount Pictures - which exceeds the entire market cap of PARA today and is comparable to some of the largest transactions of its kind in recent years - highlights the critical role that the film and TV studio plays for not only the industry but also for PARA's survival itself. Paramount Pictures largely underpins the continued success of PARA.

Maximizing content value has been a key priority for the company. Without Paramount Pictures, PARA essentially loses a sizable amount of prospective returns capable of offsetting the accelerating decline in linear TV profits. Meanwhile, Paramount+, which remains a "cash burning" business, would need to pay incremental content licensing fees to beef up its DTC streaming catalogue in the event Paramount Pictures is carved out from the PARA's portfolio. This would accordingly yield negative implications for its ambitions to achieve profitability in the domestic U.S. market by mid-decade. Note that this profitability timeline already is struggling to catch up to and/or behind peers like WBD, Disney, and Netflix, Inc. (NFLX).

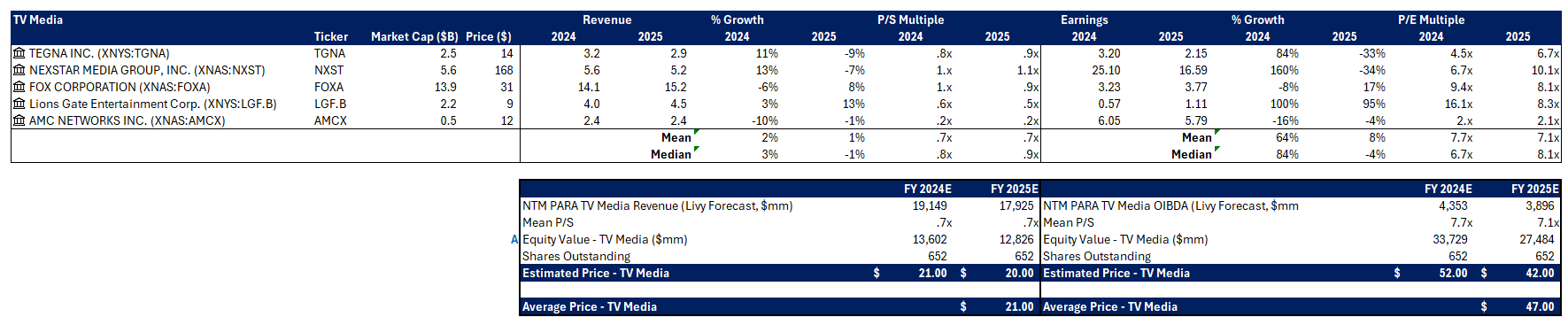

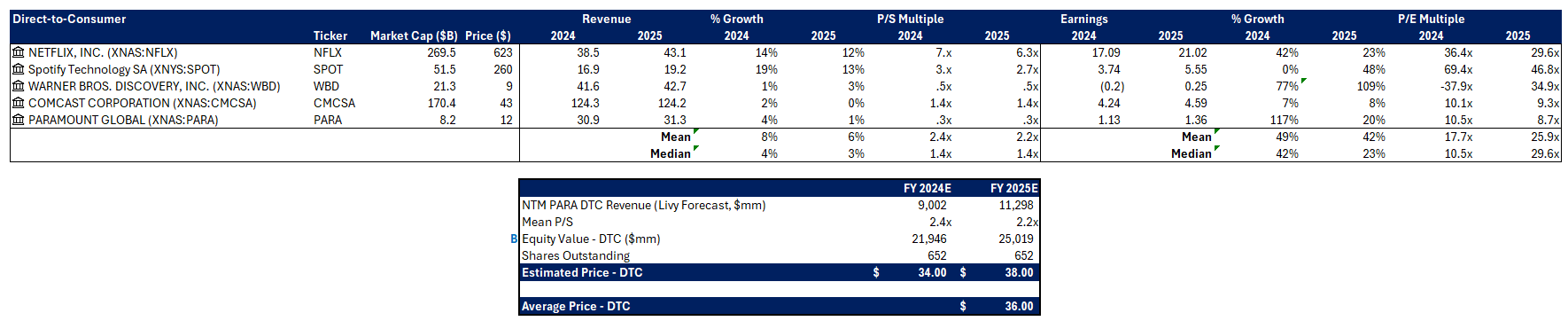

Moving forward with the Apollo proposal would simply de-synergize prospects for a recovery in the PARA stock, let alone trading back toward levels closer to its sum-of-the-parts valuation. This figure totals as high as $30 billion when considering comparable multiples, which is admittedly a huge premium from current levels, but also a huge haircut from PARA's 2021 all-time peak valuation reflective of its prospective value if the linear TV wind-down and DTC build-up could restore balance.

Author Author Author

The latest outright purchase proposal for Paramount Pictures from Apollo is an attractive offer that will unlikely close. Instead, we would like to shift focus to the dire reality facing PARA. Specifically, we believe Apollo's latest offer for Paramount Pictures highlights the potential transition of prospective buyers' interest from initially PARA as a whole to now only its most valuable asset. This underscores rapidly diminishing intrinsic value attributable to PARA's DTC and TV media businesses without leverage from Paramount Pictures. This is not a good outlook for PARA, underscoring significant execution risks ahead for management's turnaround plans, which will likely continue to weigh on the stock's performance.